A Conditional Approval Pending Credit Inquiry Explanation Letter is often required by lenders to clarify recent activity on your credit report. This document allows borrowers to explain specific hard inquiries to ensure they are not seeking excessive new debt during the mortgage process. Providing a clear narrative helps underwriters assess your financial stability. Below are some ready to use templates.

Image cover: Understanding Conditional Approval: Credit Inquiry Explanation Letter Templates

Letter Samples List

- Conditional Approval Credit Inquiry Explanation Letter

- Letter of Explanation for Recent Credit Inquiries

- Mortgage Conditional Approval Inquiry Explanation Letter

- Credit Inquiry Letter of Explanation for Conditional Approval

- Pending Approval Credit Inquiry Explanation Letter

- Letter of Explanation Regarding Unrecognized Credit Inquiries

- Conditional Mortgage Approval Credit Inquiry Letter

- Credit Report Inquiry Explanation Letter for Underwriting

- Letter to Explain Credit Inquiries for Mortgage Approval

- Borrower Letter of Explanation for Pending Credit Inquiries

- Conditional Loan Approval Credit Inquiry Letter of Explanation

- Recent Credit Inquiry Explanation Letter for Mortgage Lenders

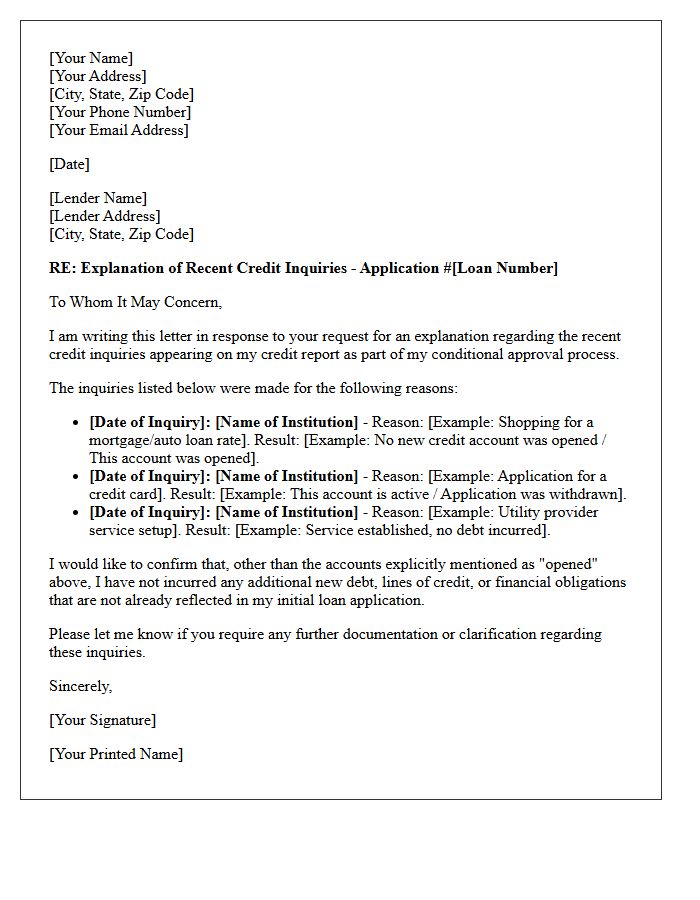

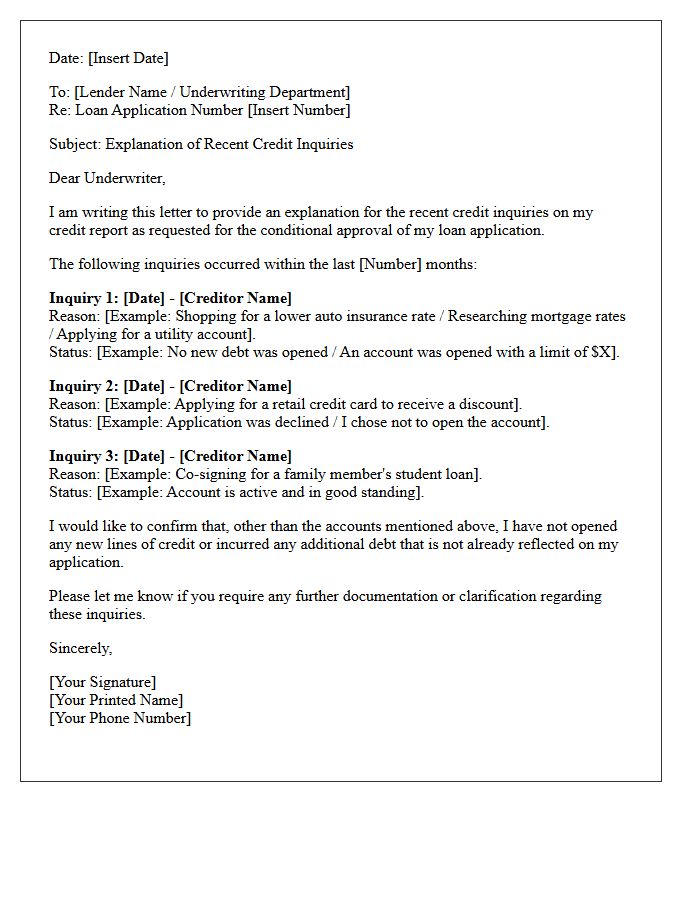

Conditional Approval Credit Inquiry Explanation Letter

A Conditional Approval Credit Inquiry Explanation Letter is a formal document required by lenders to clarify recent activity on your credit report. You must provide a legitimate reason for every hard inquiry made within the last 120 days. Lenders use this to ensure you are not opening undisclosed debt that could impact your debt-to-income ratio. Briefly explain if the inquiry resulted in new credit or was simply a rate shopping exercise. Clear documentation helps finalize your mortgage approval by proving financial stability and transparency during the underwriting process.

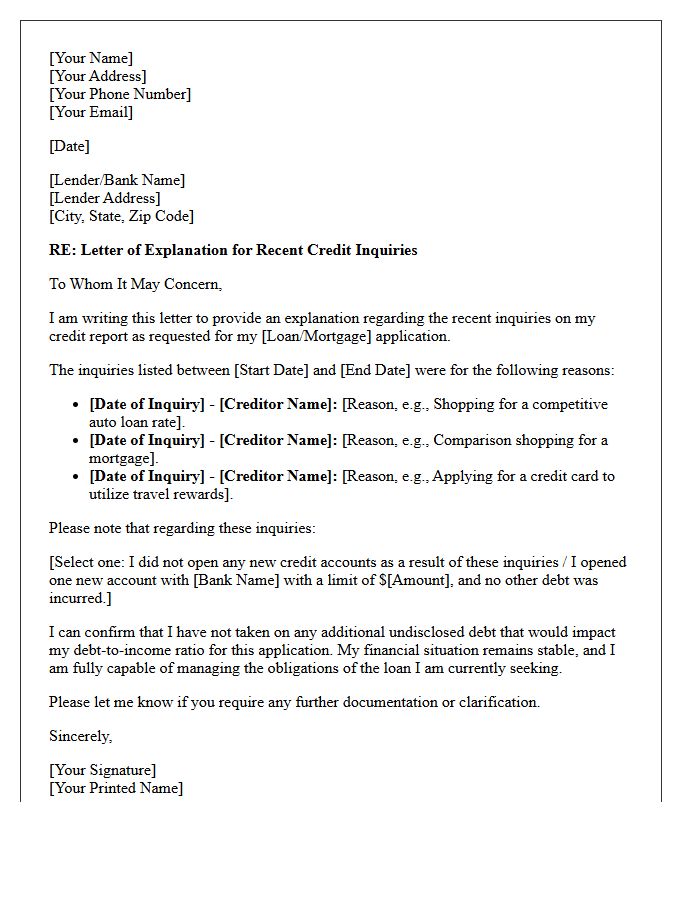

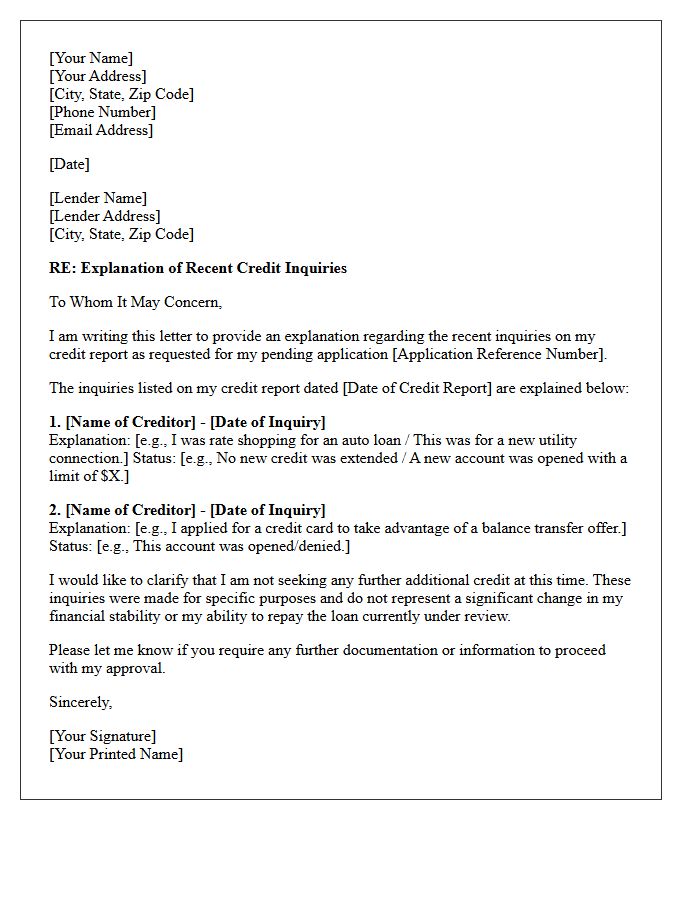

Letter of Explanation for Recent Credit Inquiries

A Letter of Explanation for recent credit inquiries clarifies why you sought new credit before a mortgage application. Lenders require this to ensure you are not accumulating undisclosed debt that could impact your debt-to-income ratio. Your letter should list each inquiry, provide a brief reason such as shopping for a car loan or insurance, and explicitly state whether a new account was opened. Professional transparency helps underwriters confirm your financial stability and ensures that recent credit activity does not jeopardize your final loan approval.

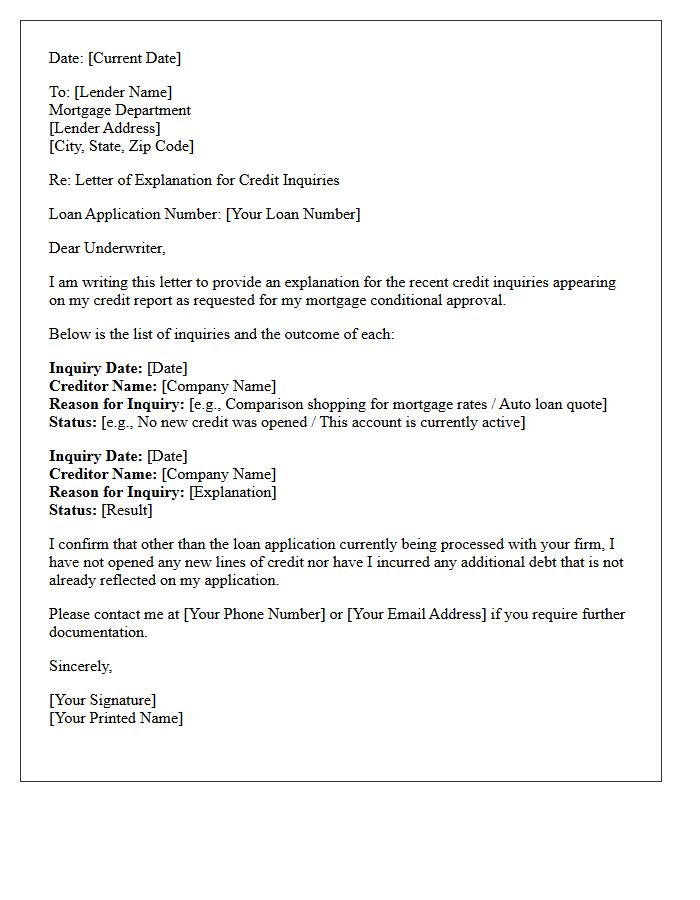

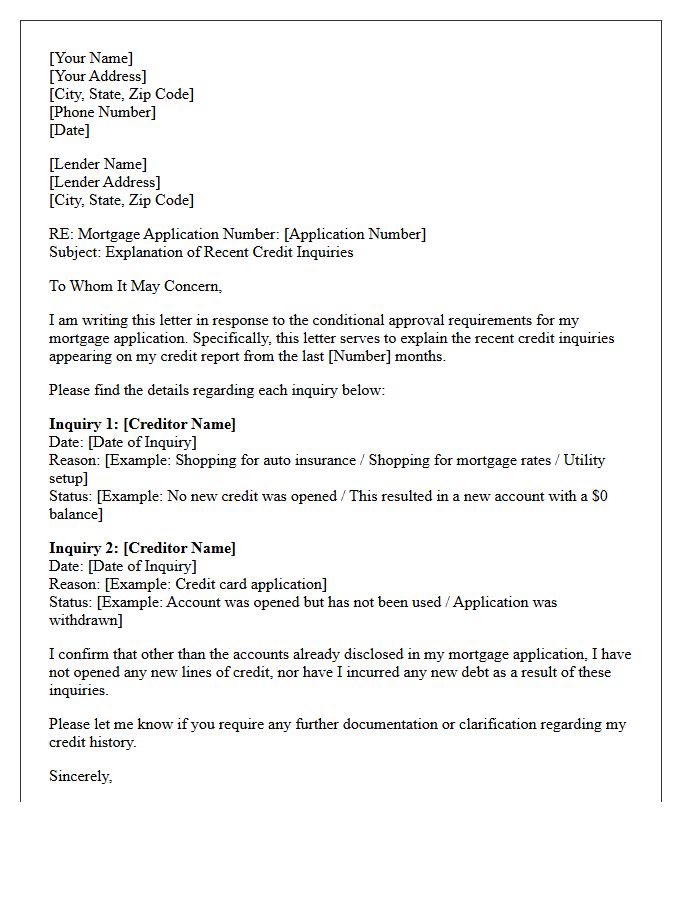

Mortgage Conditional Approval Inquiry Explanation Letter

A mortgage conditional approval inquiry explanation letter clarifies recent credit inquiries to lenders. You must explain why you sought new credit and confirm no additional debt was incurred. Providing a written statement helps underwriters assess your debt-to-income ratio and financial stability. Keep explanations brief, honest, and professional to ensure your loan file remains strong. Disclosing these activities prevents delays during the final underwriting process, ensuring the lender that your creditworthiness hasn't changed since the initial application. This transparency is vital for securing your final loan commitment.

Credit Inquiry Letter of Explanation for Conditional Approval

A Credit Inquiry Letter of Explanation is a vital document required for conditional approval when mortgage lenders identify recent hard pulls on your credit report. You must clarify whether these inquiries resulted in new debt or additional credit lines. Lenders use this to calculate your accurate debt-to-income ratio and assess financial stability. Be concise: list each inquiry date, the creditor's name, and state if the account was opened or denied. Providing this written verification ensures transparency, helping underwriters finalize your loan commitment by mitigating potential lending risks.

Pending Approval Credit Inquiry Explanation Letter

A Pending Approval Credit Inquiry Explanation Letter is a formal document sent to lenders to clarify recent credit checks. When applying for a mortgage or loan, multiple inquiries can signal financial instability. This letter allows you to provide a legitimate justification for each inquiry, such as shopping for the best rate or correcting an error. Clearly stating that no new debt was acquired helps mitigate risk concerns. Providing this proactive clarification is essential to maintaining your creditworthiness and securing final loan approval during the underwriting process.

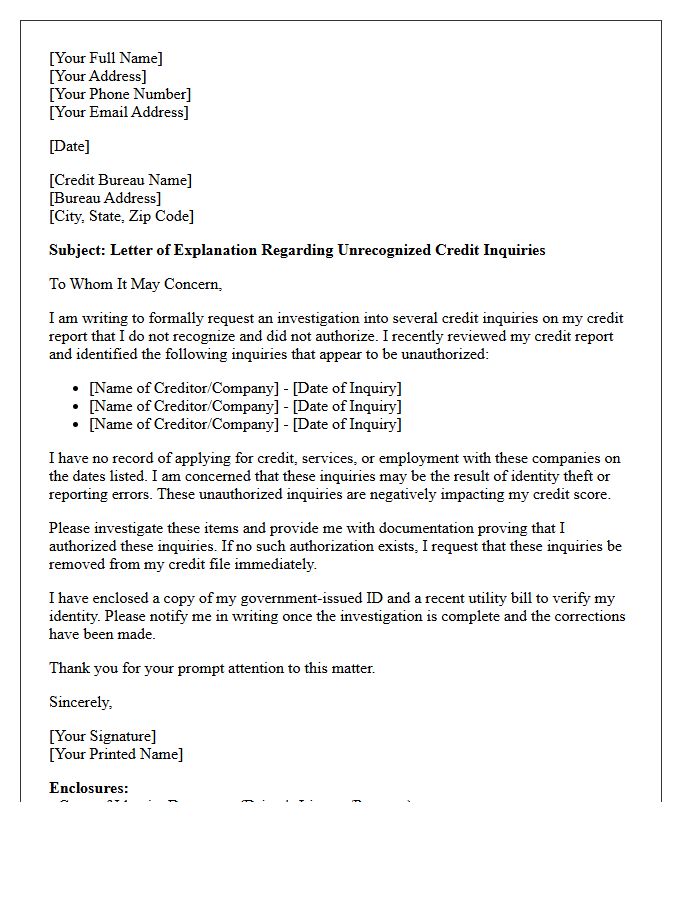

Letter of Explanation Regarding Unrecognized Credit Inquiries

A Letter of Explanation regarding unrecognized credit inquiries is a formal document used to clarify unauthorized credit checks to lenders or credit bureaus. It is essential for protecting your credit score during mortgage or loan applications. You must clearly state whether the inquiry resulted in new debt or was an error. Providing this written context helps verify your identity and proves you are not overextending your finances. Timely submission ensures lending transparency and prevents potential application denials caused by suspicious or excessive credit-seeking activity appearing on your report.

Conditional Mortgage Approval Credit Inquiry Letter

A Conditional Mortgage Approval Credit Inquiry Letter is a formal document required when lenders detect recent credit checks on your report. You must explain each hard inquiry to prove you have not acquired new debt that could impact your debt-to-income ratio. This letter ensures transparency during the underwriting process, confirming your financial stability before final closing. Clearly state the purpose of each inquiry and confirm if any new accounts were opened to prevent delays in your loan funding.

Credit Report Inquiry Explanation Letter for Underwriting

A credit report inquiry explanation letter is a written statement provided to mortgage underwriters to clarify recent activity on your credit file. Underwriters require this to ensure you have not opened new debt that could impact your debt-to-income ratio. Your letter must address each hard inquiry from the past 90 to 120 days, stating whether it resulted in a new account. Providing a clear justification helps lenders assess your financial stability and ensures your loan application remains accurate during the final approval process.

Letter to Explain Credit Inquiries for Mortgage Approval

A letter to explain credit inquiries is a formal document requested by mortgage lenders to clarify recent applications for new debt. Borrowers must justify each hard pull on their credit report to ensure they haven't acquired undisclosed liabilities that could impact their debt-to-income ratio. This letter confirms whether new accounts were opened or if the inquiry was simply for comparison shopping. Providing a clear, signed explanation helps underwriters assess your financial stability and ensures you meet the necessary risk requirements for final loan approval.

Borrower Letter of Explanation for Pending Credit Inquiries

A Borrower Letter of Explanation for pending credit inquiries is a formal document required by lenders to clarify recent credit activity. It must state whether new debt was obtained or if the inquiry was merely for shopping rates. Lenders use this to verify your debt-to-income ratio and ensure no undisclosed liabilities exist before final approval. Be concise, provide specific dates, name the creditors, and clearly indicate the application outcome. Accurate explanations prevent processing delays and help maintain your mortgage eligibility during the underwriting phase.

Conditional Loan Approval Credit Inquiry Letter of Explanation

A Letter of Explanation for credit inquiries is vital for securing conditional loan approval. Lenders require this document to verify you haven't incurred new undisclosed debts that could impact your debt-to-income ratio. Your letter must clearly list each recent inquiry, stating the purpose and whether new credit was actually extended. Providing a concise, honest account of these credit checks assures underwriters of your financial stability and prevents delays in the final mortgage funding process. Accurate documentation is the key to moving from conditional status to a closed loan.

Recent Credit Inquiry Explanation Letter for Mortgage Lenders

A Credit Inquiry Explanation Letter clarifies recent credit checks to mortgage underwriters. Lenders require this document to ensure you haven't acquired new debt that could impact your debt-to-income ratio. You must list each inquiry from the last 90 days, stating the purpose and whether an account was opened. Providing a clear, honest explanation for every hard pull helps satisfy secondary market guidelines and proves financial stability. Keep your responses brief and accurate to prevent processing delays during your mortgage approval journey.

What is a Conditional Approval Pending Credit Inquiry Explanation Letter?

A Conditional Approval Pending Credit Inquiry Explanation Letter is a formal document requested by mortgage lenders or underwriters asking a borrower to explain recent credit inquiries listed on their credit report to ensure no new undisclosed debts have been opened.

Why do lenders require an explanation for recent credit inquiries?

Lenders require this explanation to verify the borrower's debt-to-income ratio (DTI) remains stable; they need to confirm that recent inquiries did not result in new credit cards, personal loans, or lines of credit that would affect the applicant's ability to repay the mortgage.

What should be included in a credit inquiry explanation letter?

The letter should include the date of the inquiry, the name of the creditor, the purpose of the credit check (such as shopping for insurance or utility setup), and a clear statement confirming whether or not a new account was opened as a result of that inquiry.

Does a credit inquiry explanation letter guarantee final loan approval?

No, the letter is a standard requirement to satisfy a "condition" of approval; final loan commitment is only granted once the underwriter reviews the explanation and confirms that no new liabilities negatively impact the borrower's qualification status.

How do I explain multiple inquiries from different mortgage lenders?

You should state that the inquiries were for "rate shopping" purposes to find the best mortgage terms; underwriters generally view multiple inquiries for the same loan type within a short window as a single event that does not represent a risk of undisclosed debt.

Comments