A USDA Conditional Loan Approval Letter is a formal document issued by the United States Department of Agriculture indicating that a borrower meets specific eligibility requirements for a rural housing loan. This notification outlines necessary steps and documentation required to finalize the mortgage process and secure funding. To help you streamline your application, below are some ready to use template.

Image cover: USDA Conditional Loan Approval: Professional Letter Templates and Samples

Letter Samples List

- Mortgage Lender Company Letterhead

- Date of Letter Issuance

- Primary Borrower and Co-Borrower Information

- United States Department of Agriculture Conditional Loan Approval Letter Subject Line

- Maximum Approved Loan Amount and Term

- Interest Rate and Annual Percentage Rate Details

- Subject Property Address and Eligibility Verification

- United States Department of Agriculture Upfront Guarantee Fee Requirements

- Pending Income and Employment Verification Conditions

- Satisfactory Rural Development Property Appraisal Condition

- Clear Title and Homeowners Insurance Requirements

- Expiration Date of Conditional Approval Letter

- Mortgage Loan Officer Signature Block

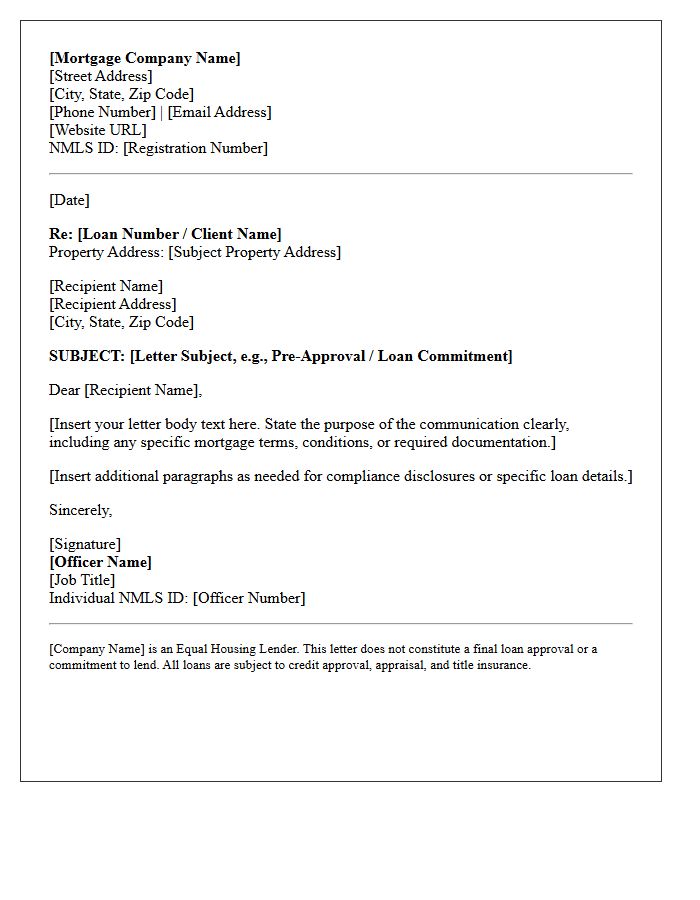

Mortgage Lender Company Letterhead

A mortgage lender company letterhead serves as a formal verification tool for official correspondence. It must clearly display the lender's legal name, corporate address, and NMLS licensing information to ensure regulatory compliance. When receiving documents like pre-approval letters or loan commitments, verify the logo and contact details to prevent fraud. This professional branding establishes trust and authenticity between the financial institution, real estate agents, and borrowers. Always ensure the letterhead includes a direct line to the loan officer to validate the document's legitimacy during the home-buying process.

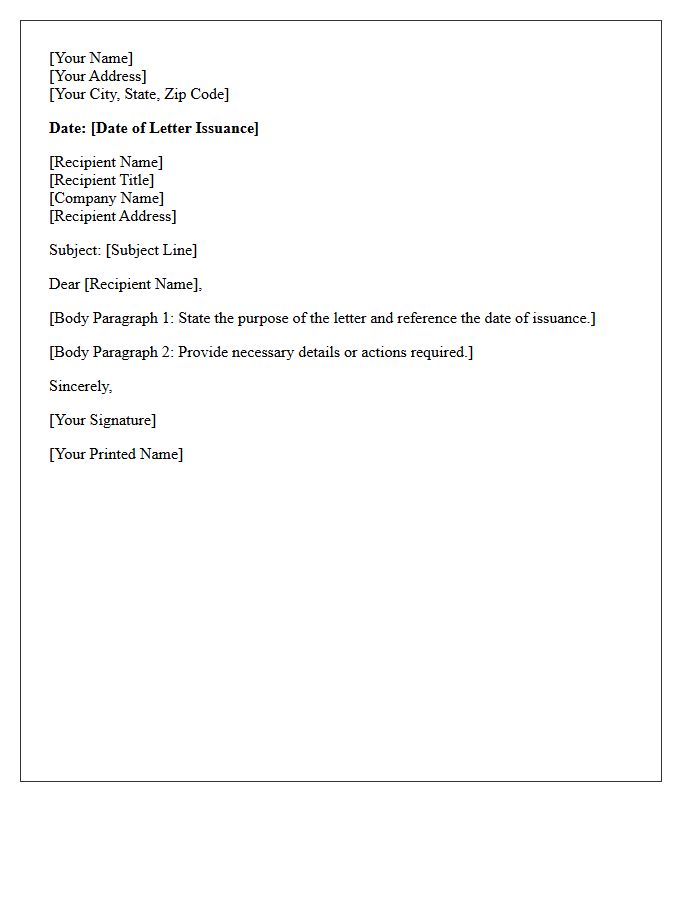

Date of Letter Issuance

The Date of Letter Issuance is the official calendar day a document is formally generated and dispatched. It serves as the primary reference for legal deadlines, notice periods, and contractual obligations. In professional correspondence, this date establishes a chronological record for compliance and tracking. Accuracy is essential, as it determines when a recipient is deemed notified, directly affecting validity and time-sensitive responses. Always verify this date to ensure alignment with statutory requirements and effective communication timelines.

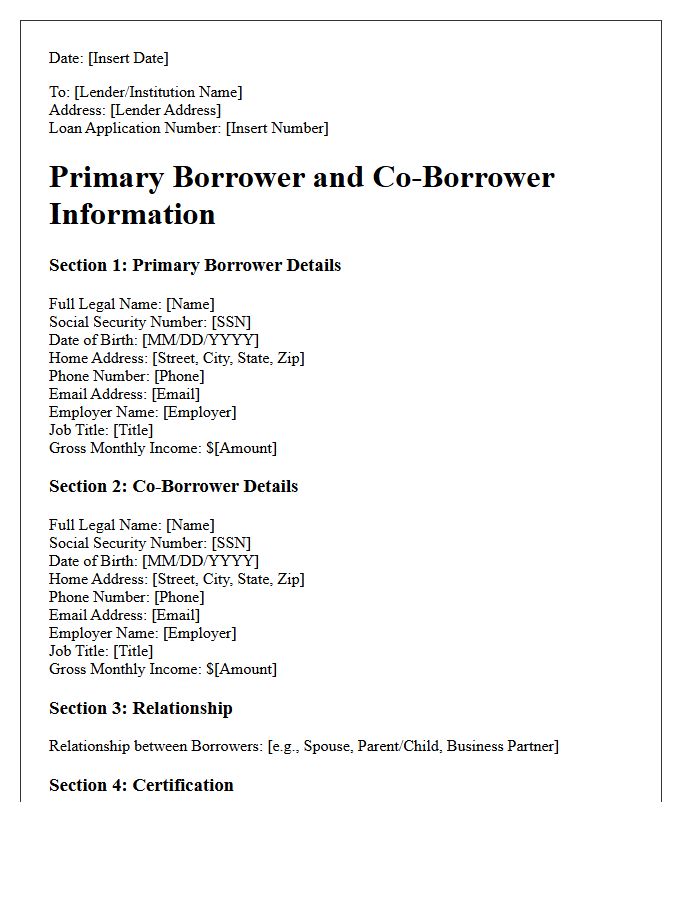

Primary Borrower and Co-Borrower Information

The Primary Borrower is the main individual responsible for loan repayment and usually the one whose credit profile determines the primary terms. A Co-Borrower shares equal legal obligation for the debt and typically has their income and assets joined with the primary applicant to enhance loan eligibility. Both parties are equally liable for the full balance, and the repayment history significantly impacts both individuals' credit scores. Understanding this joint responsibility is essential for long-term financial security and maintaining healthy credit profiles for both involved applicants.

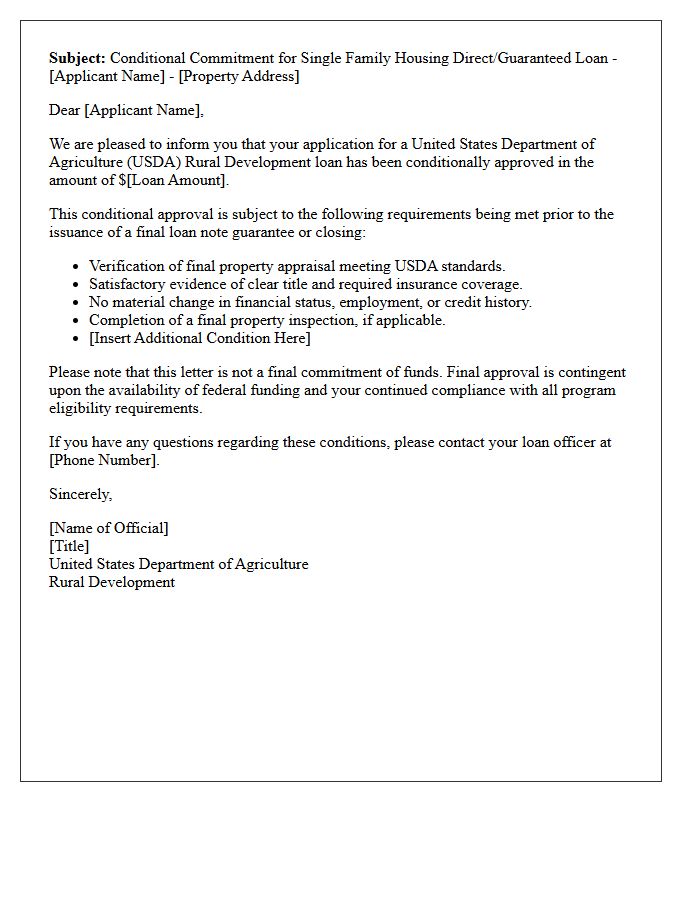

United States Department of Agriculture Conditional Loan Approval Letter Subject Line

A United States Department of Agriculture (USDA) Conditional Loan Approval Letter signifies that your mortgage application is approved, provided specific underwriting conditions are met. The subject line usually contains the USDA Case Number and the applicant's name to ensure efficient processing. This document is a critical milestone, detailing required documentation, property repairs, or financial clarifications needed before the final Loan Note Guarantee is issued. Reviewing these requirements promptly is essential to secure your home financing and proceed toward a successful closing date without unnecessary delays.

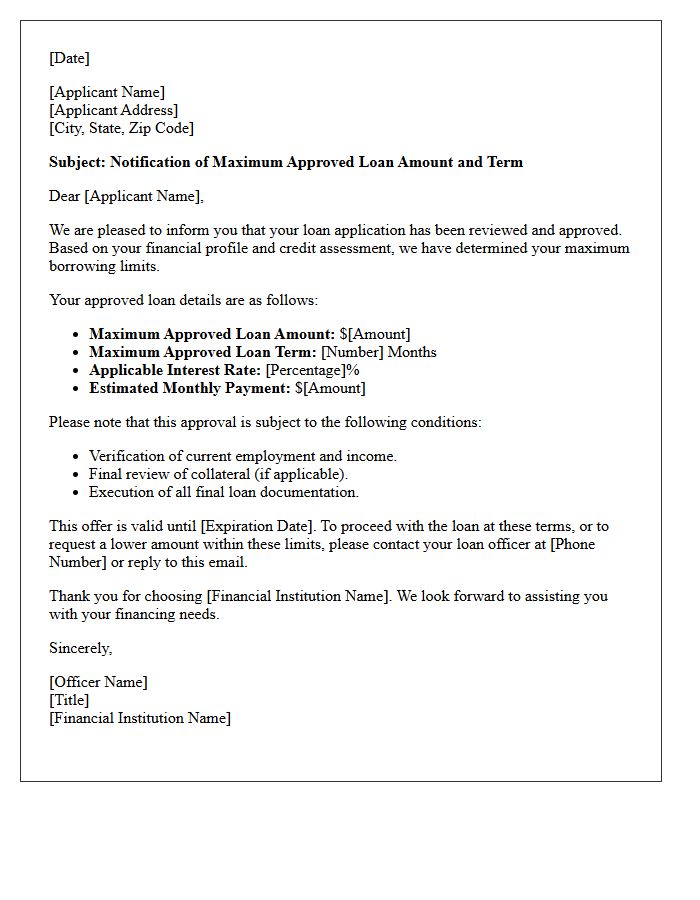

Maximum Approved Loan Amount and Term

The Maximum Approved Loan Amount represents the highest credit limit a lender offers based on your debt-to-income ratio and creditworthiness. Simultaneously, the Loan Term dictates the repayment duration, directly influencing your monthly installments and total interest costs. Lenders calculate these figures to ensure affordability while minimizing default risk. Shorter terms typically feature lower interest rates but higher payments, whereas longer terms reduce monthly burdens but increase the overall cost of borrowing. Always review these limits to ensure your financing remains sustainable within your long-term financial plan.

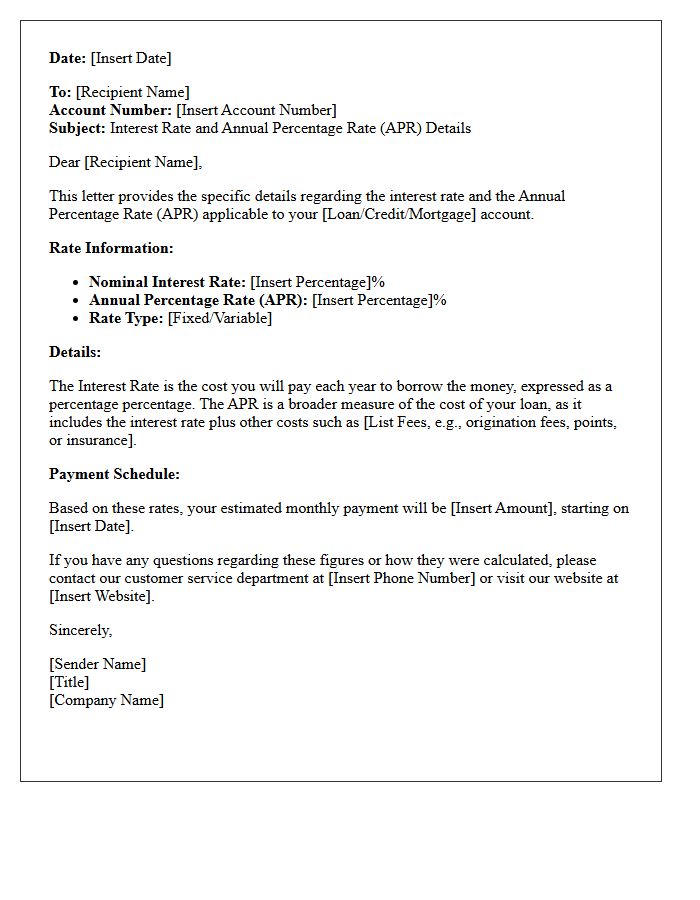

Interest Rate and Annual Percentage Rate Details

Understanding the difference between an interest rate and the Annual Percentage Rate (APR) is essential for borrowers. The interest rate represents the specific cost of borrowing the principal amount. In contrast, the APR provides a more comprehensive view by including the interest rate plus additional fees, such as points or closing costs. While the interest rate determines your monthly payment, the APR reflects the total annual cost of the loan. Comparing APR values across different lenders allows you to identify the most cost-effective financing option available.

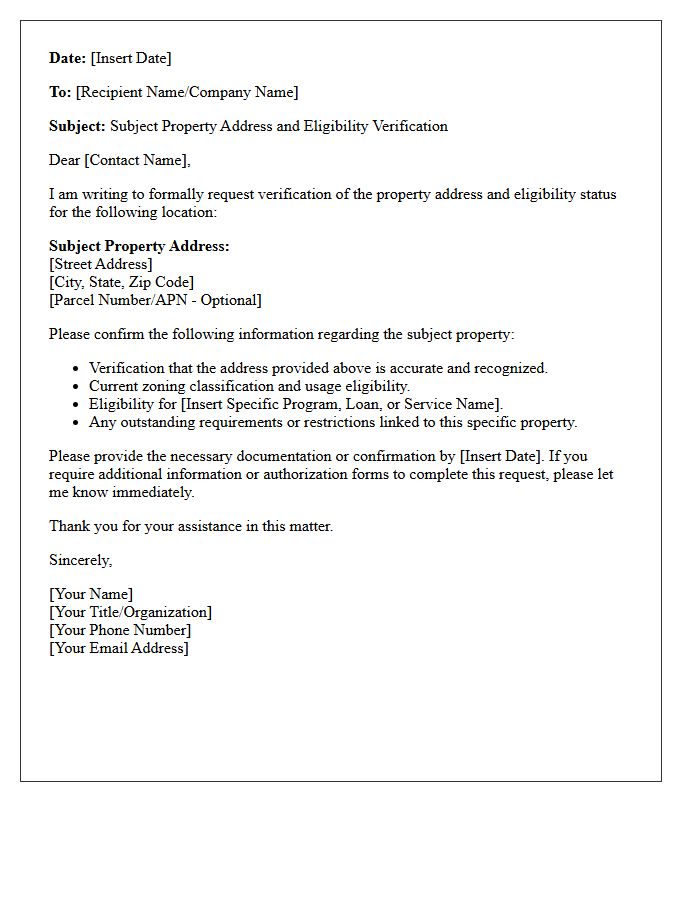

Subject Property Address and Eligibility Verification

Accurate Subject Property Address verification is critical for ensuring legal compliance and precise appraisal reporting. Lenders must confirm the physical location matches official records to prevent valuation errors. Eligibility Verification determines if a property meets specific loan program requirements, such as HUD standards or investment criteria. This process validates ownership, zoning compliance, and property condition early in the underwriting stage. Properly verifying these details mitigates financial risk and ensures the asset serves as adequate collateral for the mortgage, facilitating a seamless and secure real estate transaction.

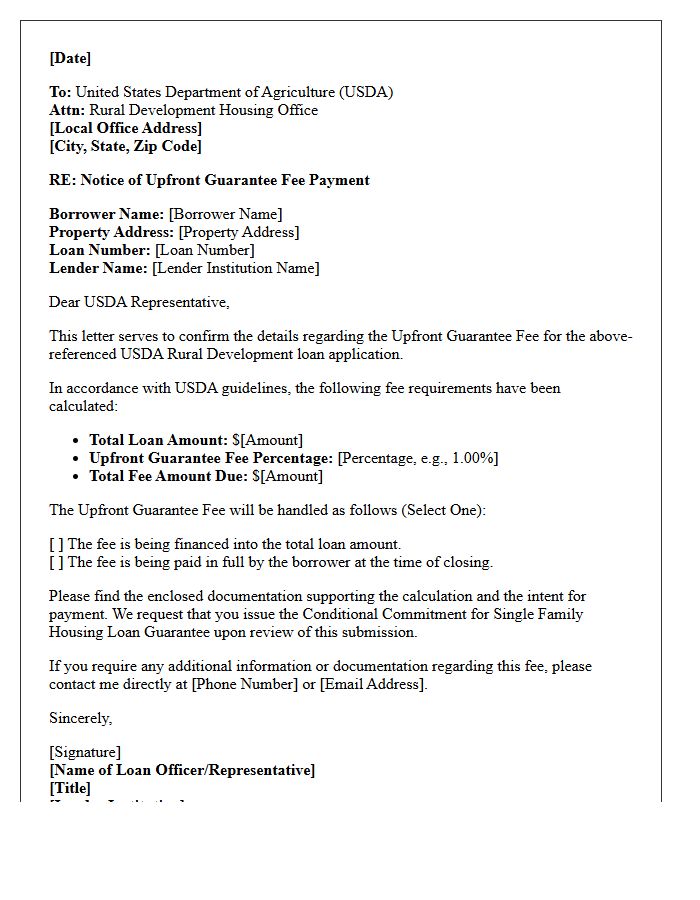

United States Department of Agriculture Upfront Guarantee Fee Requirements

The USDA upfront guarantee fee is a one-time charge required for rural development loans, currently set at 1.0% of the total loan amount. This fee is typically financed into the mortgage, allowing borrowers to avoid immediate out-of-pocket costs. It serves as insurance for the lender against default, enabling zero-down payment financing for eligible low-to-moderate income households. Borrowers must also account for an annual 0.35% recurring fee. Meeting specific property location and income eligibility criteria is mandatory to qualify for these favorable government-backed terms.

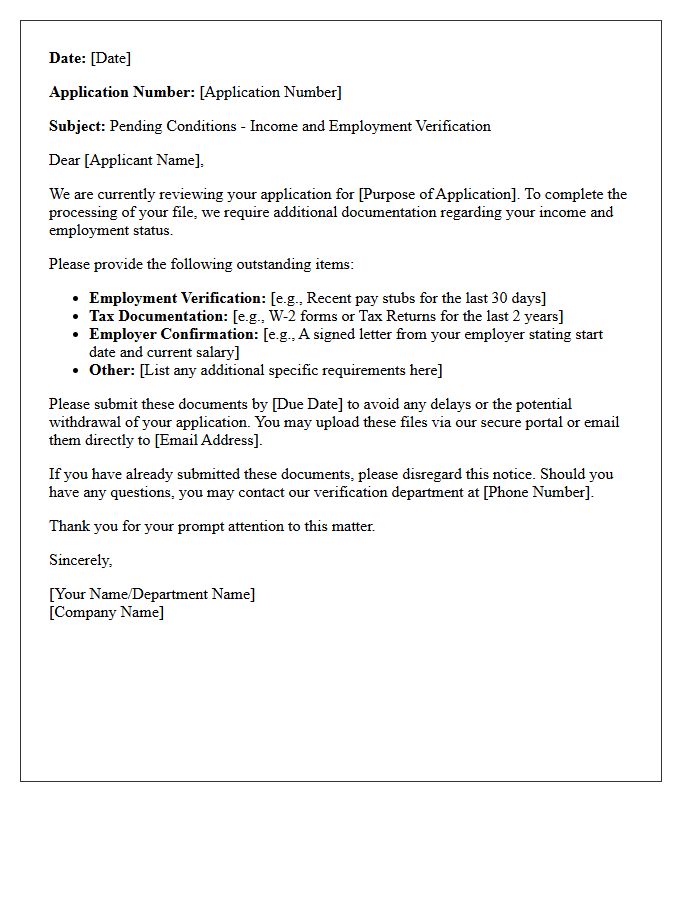

Pending Income and Employment Verification Conditions

Pending income and employment verification conditions mean a lender requires additional official documentation to confirm your financial stability. This process validates your current earnings and job status through pay stubs, tax returns, or direct employer contact. It is a critical step in underwriting to ensure you meet the debt-to-income requirements for loan approval. To prevent delays, provide accurate records promptly and avoid changing jobs or experiencing income gaps during the application phase. Cleared conditions signify that the lender has verified your ability to repay the debt.

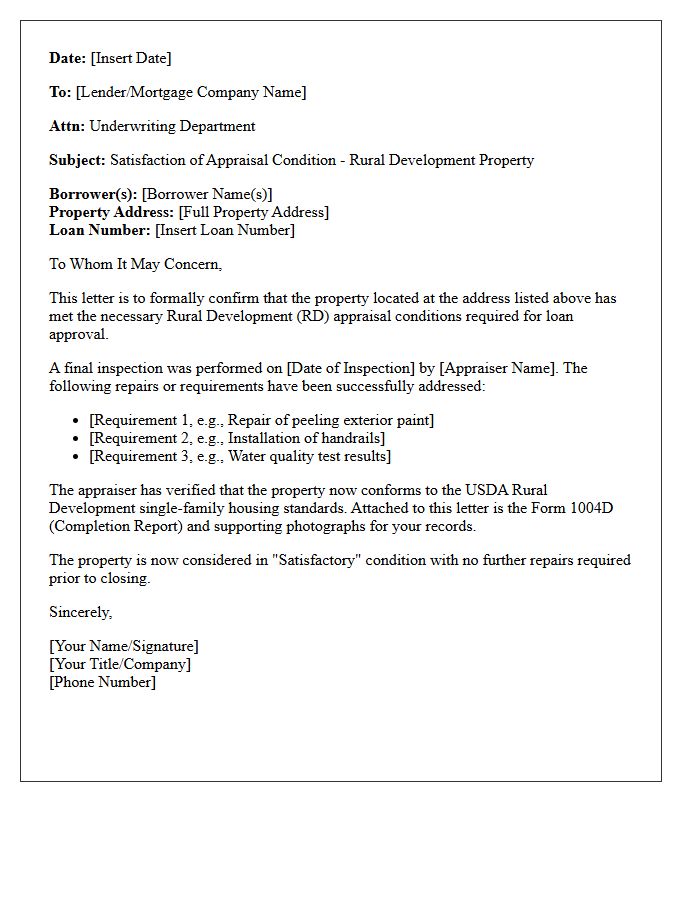

Satisfactory Rural Development Property Appraisal Condition

A Satisfactory Rural Development Property Appraisal Condition confirms that a home meets the Minimum Property Requirements (MPR) set by the USDA. The appraiser ensures the property is decent, safe, and sanitary. Key focus areas include structural integrity, functional systems, and adequate thermal performance. If deficiencies are found, they must be repaired before loan closing to protect the lender's interest and the borrower's safety. Achieving this status is essential for securing USDA financing, as it guarantees the home is move-in ready and structurally sound for rural residents.

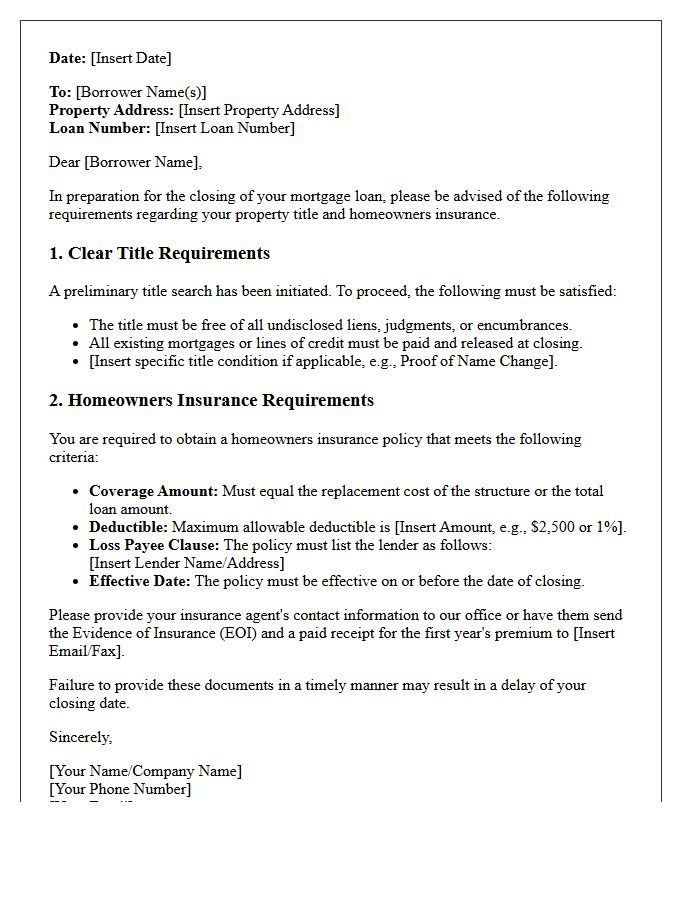

Clear Title and Homeowners Insurance Requirements

A Clear Title is essential for real estate transactions, proving the seller has legal ownership without liens or disputes. Lenders mandate a title search to protect their investment before closing. Simultaneously, Homeowners Insurance Requirements ensure the property is protected against structural damage and liabilities. Most mortgage companies require proof of a paid premium at settlement to safeguard the collateral. Both elements are critical safeguards, ensuring legal security and financial protection for the buyer and lender throughout the life of the loan.

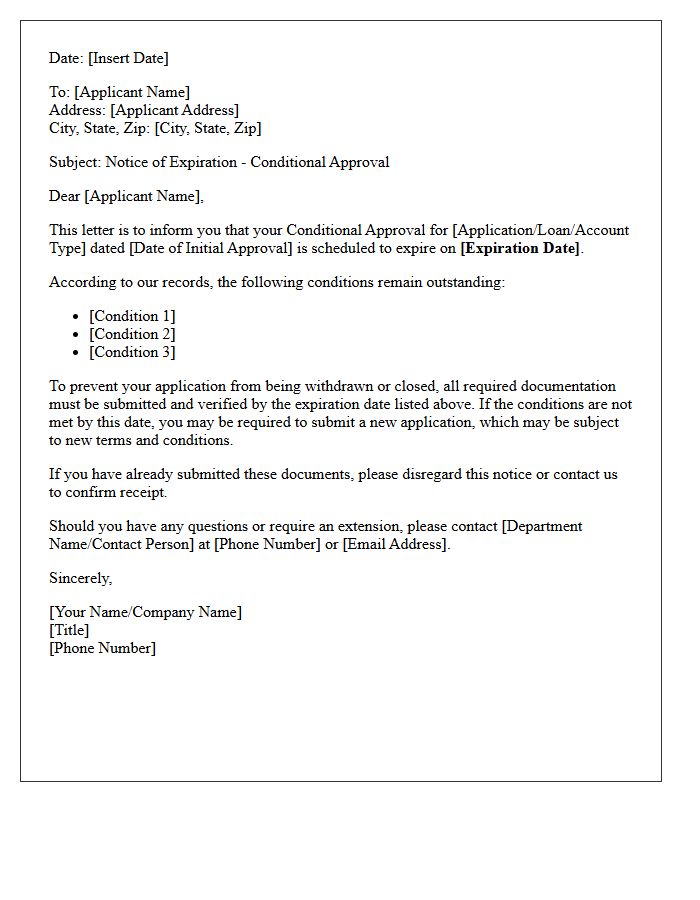

Expiration Date of Conditional Approval Letter

The expiration date of a conditional approval letter is a critical deadline, typically valid for 30 to 90 days. This timeframe signifies how long the lender's preliminary commitment remains active based on your current financial profile. If the period lapses before you secure a property, you must provide updated income documentation and credit reports for re-evaluation. Since interest rates and loan terms fluctuate, monitoring this date is essential to maintain your borrowing power and ensure a seamless transition from house hunting to final mortgage closing.

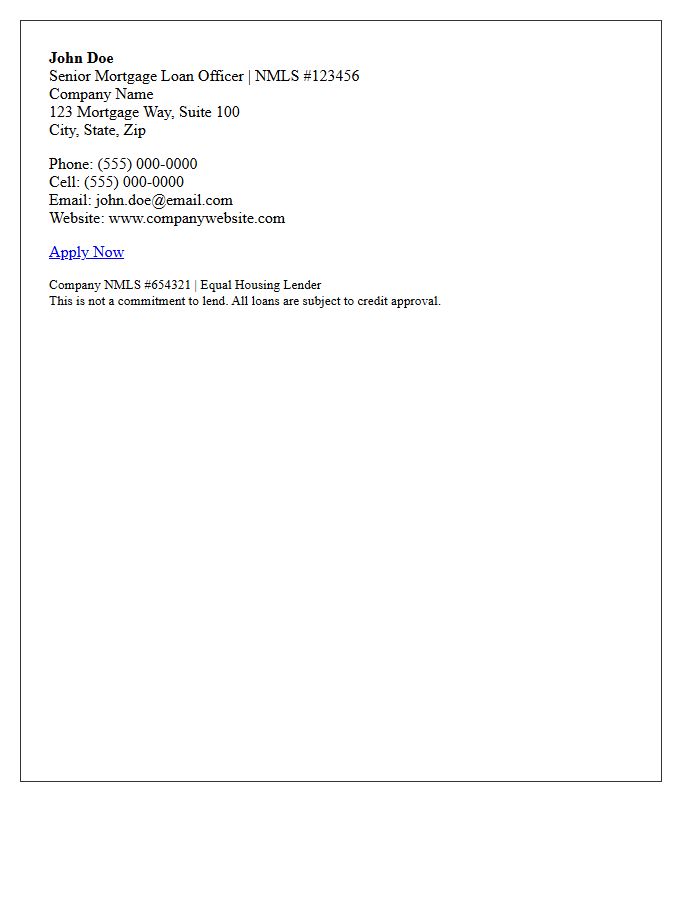

Mortgage Loan Officer Signature Block

A professional Mortgage Loan Officer Signature Block is essential for legal compliance and brand credibility. It must include your full legal name, title, and company information. Most importantly, federal law requires your unique NMLS ID number to be clearly displayed on all loan documents and correspondence. To enhance accessibility, provide direct contact details like your phone number, email, and a link to your secure online application. A well-structured signature ensures transparency, builds trust with borrowers, and meets strict regulatory disclosure requirements within the lending industry.

What is a USDA Conditional Loan Approval letter?

A USDA Conditional Loan Approval letter is a formal document issued by a lender indicating that a borrower's mortgage application has been reviewed and approved, provided that specific conditions-such as final property inspections or updated financial documents-are met before closing.

What are the common conditions listed in a USDA conditional approval?

Common conditions typically include proof of homeowners insurance, updated pay stubs or bank statements, a satisfactory appraisal report that meets USDA property standards, and a final verification of employment and credit standing.

How long does it take to receive a USDA Conditional Loan Approval?

The timeline varies by lender but generally takes between 3 to 7 business days after the initial underwriting review; however, the total process may take longer if the file must also be submitted to the USDA Rural Development office for a Loan Note Guarantee.

Does a conditional approval guarantee that the USDA loan will close?

While a conditional approval is a strong sign of progress, it is not a final guarantee; the loan will only close once the borrower satisfies all "prior-to-closing" conditions and the lender issues a "Clear to Close" (CTC) status.

What is the difference between a USDA pre-approval and a conditional approval?

A pre-approval is a preliminary estimate of borrowing power based on unverified data, whereas a USDA Conditional Loan Approval is a formal commitment from an underwriter after a comprehensive review of the borrower's actual financial documentation and credit history.

Comments