A Renovation Loan Conditional Approval Letter is a formal document from a lender indicating your loan is approved pending specific requirements. It outlines necessary steps, such as submitting contractor bids or property appraisals, to finalize your funding. Understanding these conditions helps you secure financing for your home improvement project quickly. Below are some ready to use templates.

Image cover: Mastering the Renovation Loan Conditional Approval: Templates and Expert Samples

Letter Samples List

- FHA Standard Renovation Loan Conditional Approval Letter

- FHA Limited Renovation Loan Conditional Approval Letter

- Fannie Mae HomeStyle Renovation Conditional Approval Letter

- Freddie Mac CHOICERenovation Conditional Approval Letter

- Conventional Renovation Mortgage Conditional Approval Letter

- VA Renovation Loan Conditional Approval Letter

- USDA Rural Development Renovation Loan Conditional Approval Letter

- Jumbo Renovation Mortgage Conditional Approval Letter

- Investment Property Renovation Loan Conditional Approval Letter

- Primary Residence Rehabilitation Loan Conditional Approval Letter

- Second Home Renovation Loan Conditional Approval Letter

- Fix And Flip Renovation Loan Conditional Approval Letter

- Energy Efficient Renovation Mortgage Conditional Approval Letter

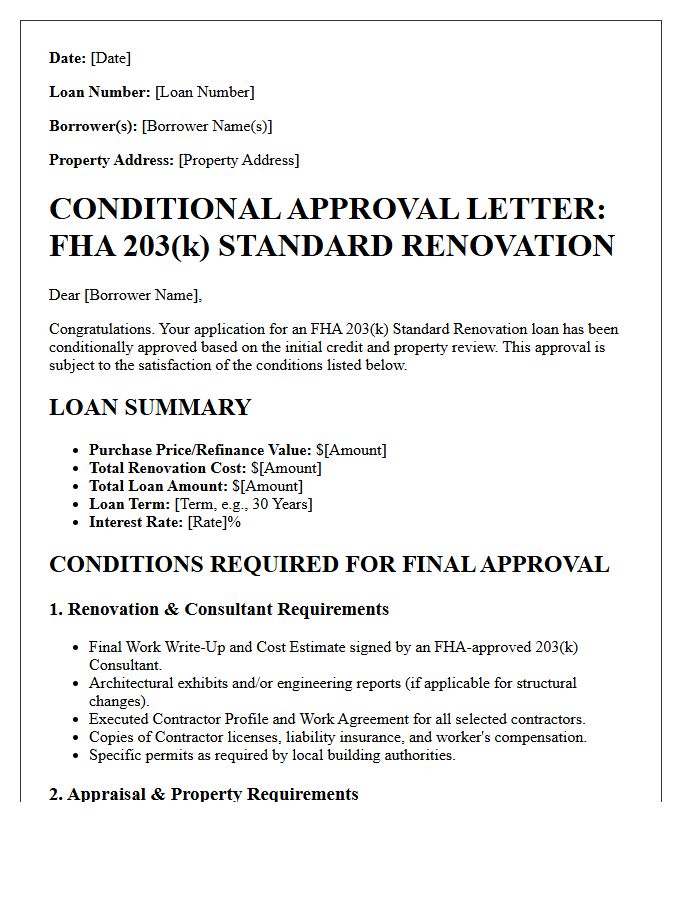

FHA Standard Renovation Loan Conditional Approval Letter

An FHA 203(k) Standard Renovation Loan conditional approval letter signifies that your mortgage application is approved pending specific requirements. This critical document outlines underwriting conditions, such as detailed contractor bids, architectural exhibits, and structural inspections. It confirms your eligibility based on credit and income while emphasizing that final funding depends on verifying the rehabilitation costs and property valuation. Obtaining this letter is a vital milestone, demonstrating to sellers and contractors that you are financially prepared to manage a complex home improvement project through a government-backed loan program.

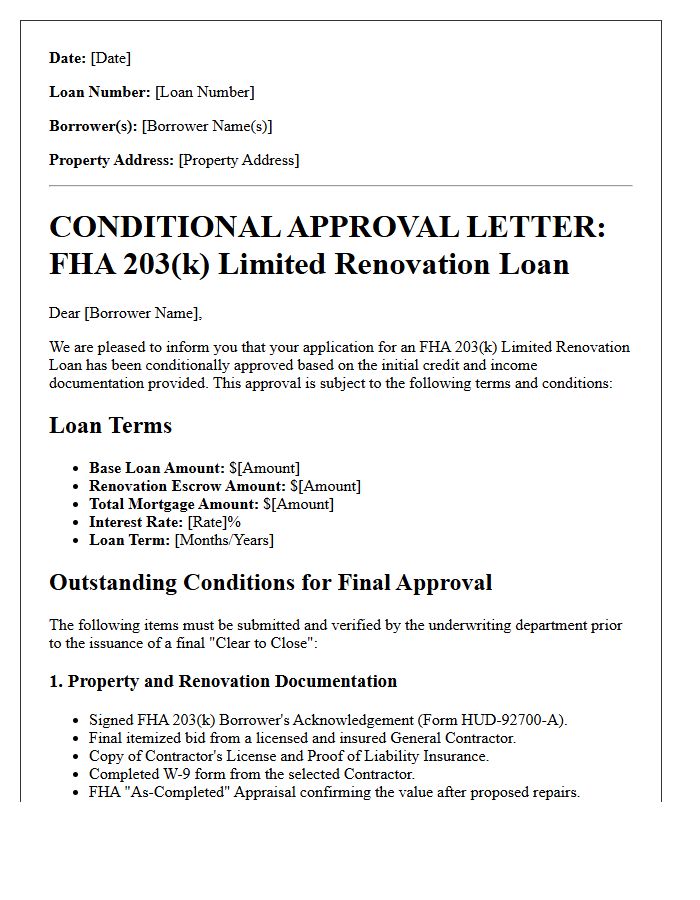

FHA Limited Renovation Loan Conditional Approval Letter

An FHA Limited Renovation Loan Conditional Approval Letter is a formal document indicating a lender's preliminary commitment to finance both your home purchase and up to $35,000 in non-structural repairs. It outlines specific underwriting conditions, such as contractor bids or updated credit documents, that must be satisfied before final funding. Receiving this letter signifies you are creditworthy, but the loan remains subject to a satisfactory property appraisal and a final review of the renovation plans to ensure the home's future value meets FHA guidelines.

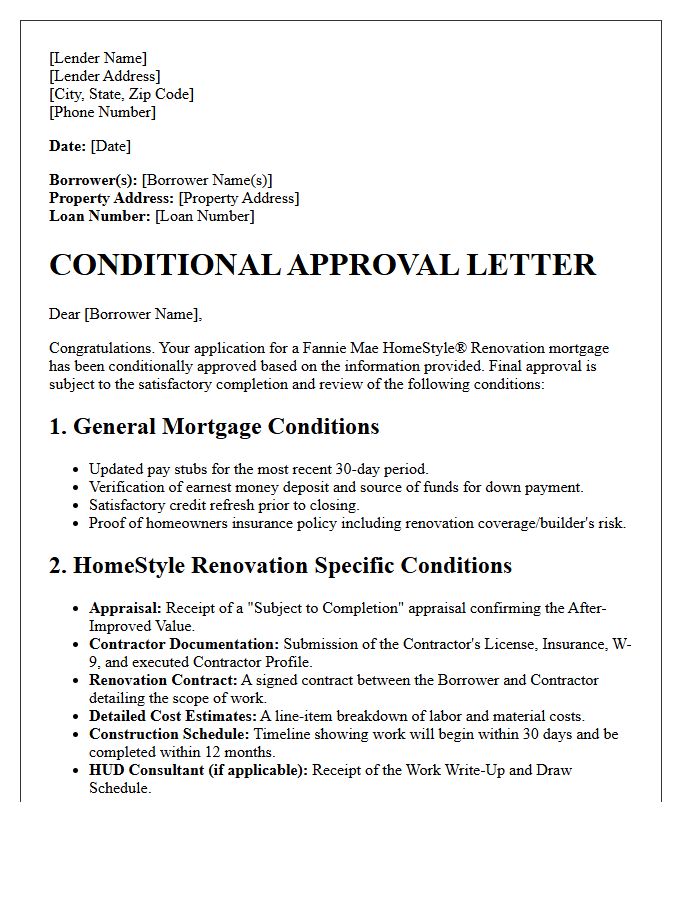

Fannie Mae HomeStyle Renovation Conditional Approval Letter

A Fannie Mae HomeStyle Renovation Conditional Approval Letter signifies that a lender has preliminarily approved your mortgage and rehabilitation funds based on creditworthiness and initial project plans. This document outlines specific underwriting conditions, such as final contractor vetting, detailed cost estimates, and a "subject-to-completion" appraisal. Receiving this letter is a critical milestone, moving you toward the final loan commitment. It confirms that both the borrower and the proposed property renovations meet GSE guidelines, provided all outstanding documentation requirements are satisfied before closing the loan.

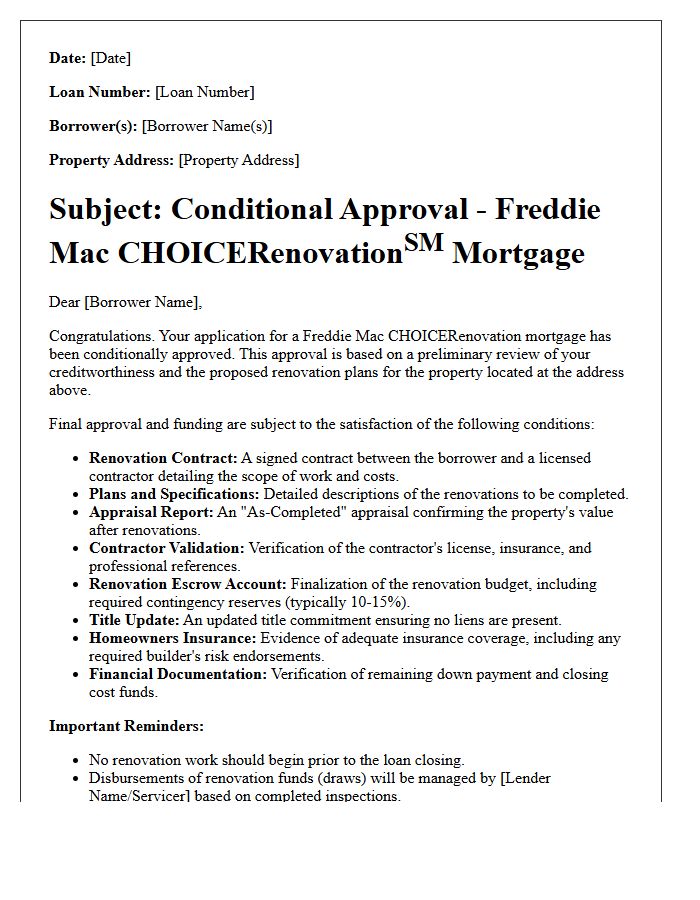

Freddie Mac CHOICERenovation Conditional Approval Letter

A Freddie Mac CHOICERenovation Conditional Approval Letter is a formal document confirming a borrower meets credit and income requirements for a renovation loan. It specifies necessary conditions, such as a HUD-certified consultant report or final contractor bids, that must be satisfied before full funding. This letter is crucial for homebuyers looking to bundle purchase costs and home improvements into a single conventional mortgage. It serves as a commitment that the lender will finance the project once all property-related contingencies and renovation plans are officially reviewed and approved.

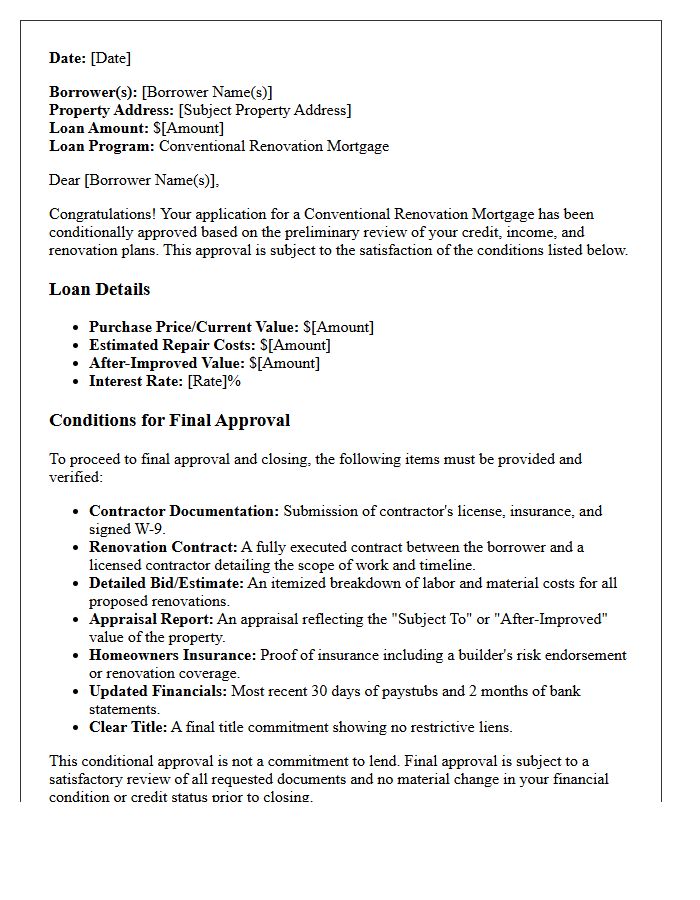

Conventional Renovation Mortgage Conditional Approval Letter

A Conventional Renovation Mortgage Conditional Approval Letter confirms that a lender is willing to finance both the home purchase and repair costs. This document specifies that final funding depends on meeting specific underwriting conditions, such as a satisfactory appraisal based on "after-improved" value and a vetted contractor's proposal. It serves as a vital signal to sellers that the buyer is financially qualified to manage a complex renovation loan. Securing this letter is the primary step in bridging the gap between a property's current state and its future potential.

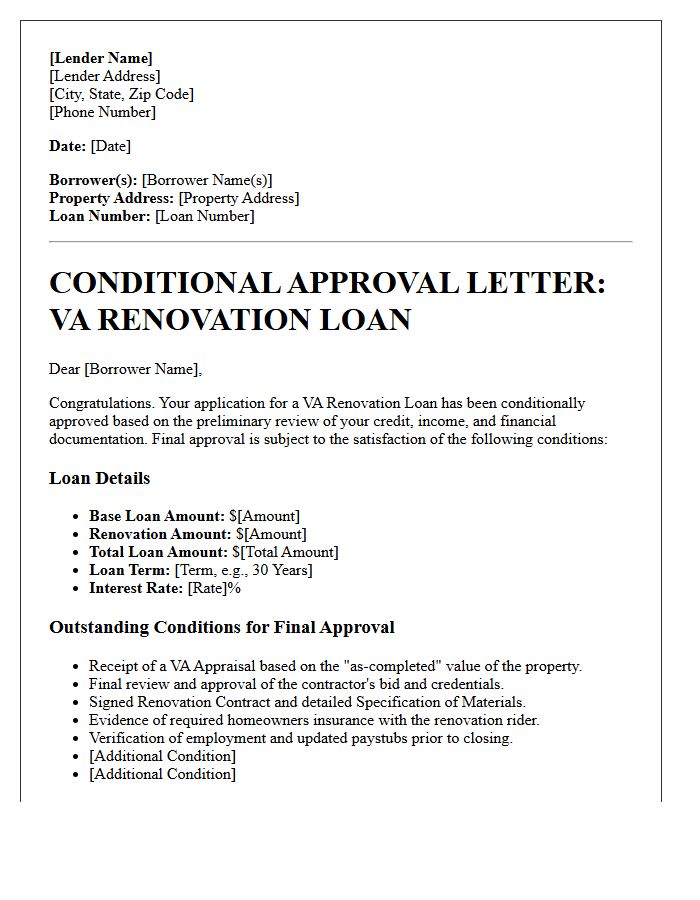

VA Renovation Loan Conditional Approval Letter

A VA Renovation Loan Conditional Approval Letter is a critical milestone indicating that a lender is willing to finance both your home purchase and repairs. It specifies underwriting requirements that must be satisfied before final funding, such as property appraisals and contractor bid validations. This document proves to sellers that you are financially qualified, provided you meet the listed conditions. Understanding these stipulations is essential, as they often involve rigorous VA safety standards and project inspections necessary to ensure the home meets all minimum property requirements for veterans.

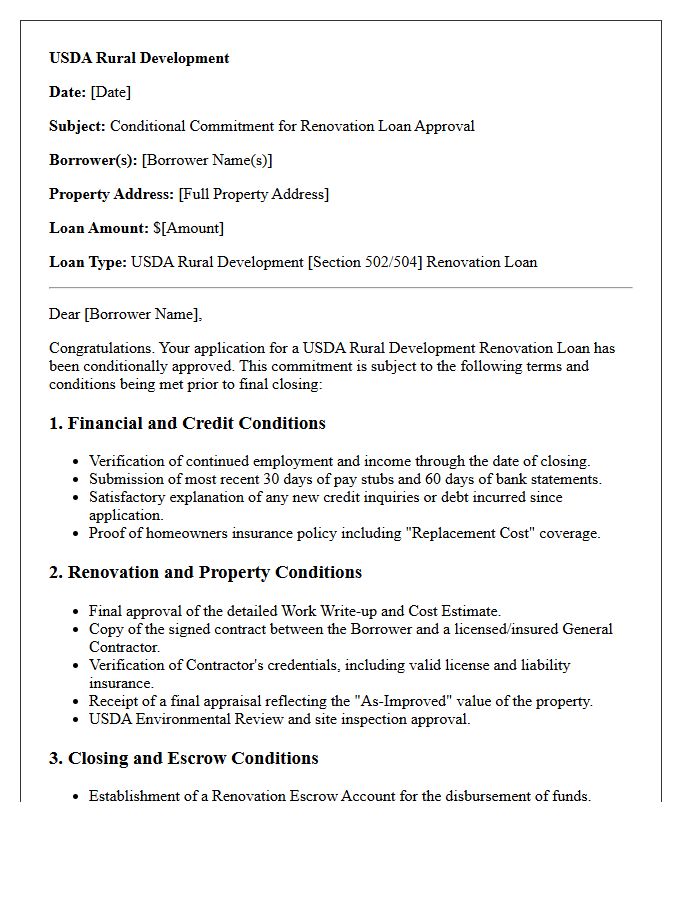

USDA Rural Development Renovation Loan Conditional Approval Letter

A USDA Rural Development Renovation Loan Conditional Approval Letter is a formal document indicating your mortgage is approved pending specific requirements. It highlights essential conditions such as final property inspections, detailed contractor bids, and updated financial verification. This letter confirms the lender's intent to fund both the purchase and home improvements, provided all underwriting stipulations are met. Receiving this document is a critical milestone, signaling that you are nearing the final commitment for your rural property renovation financing.

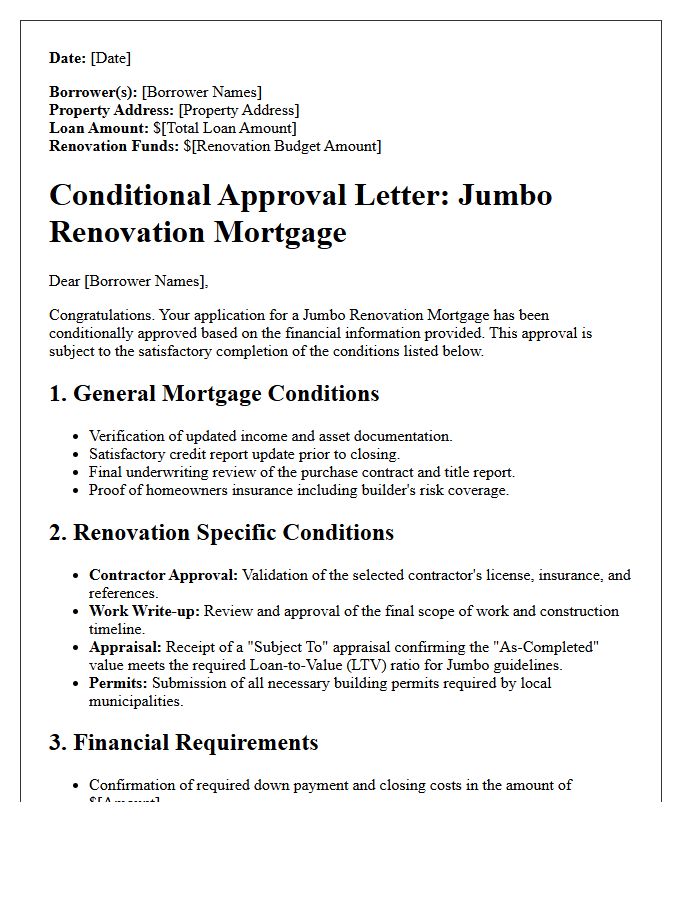

Jumbo Renovation Mortgage Conditional Approval Letter

A Jumbo Renovation Mortgage Conditional Approval Letter is a critical document indicating a lender's preliminary commitment to financing luxury properties requiring extensive upgrades. It specifies that you meet credit and income requirements, but final funding depends on satisfying contingencies. These typically include a professional appraisal of the home's "after-improved" value, a detailed contractor bid review, and underwriting verification. This letter strengthens your position when making offers, proving you have the financial backing to handle both high-balance loan amounts and complex construction costs simultaneously.

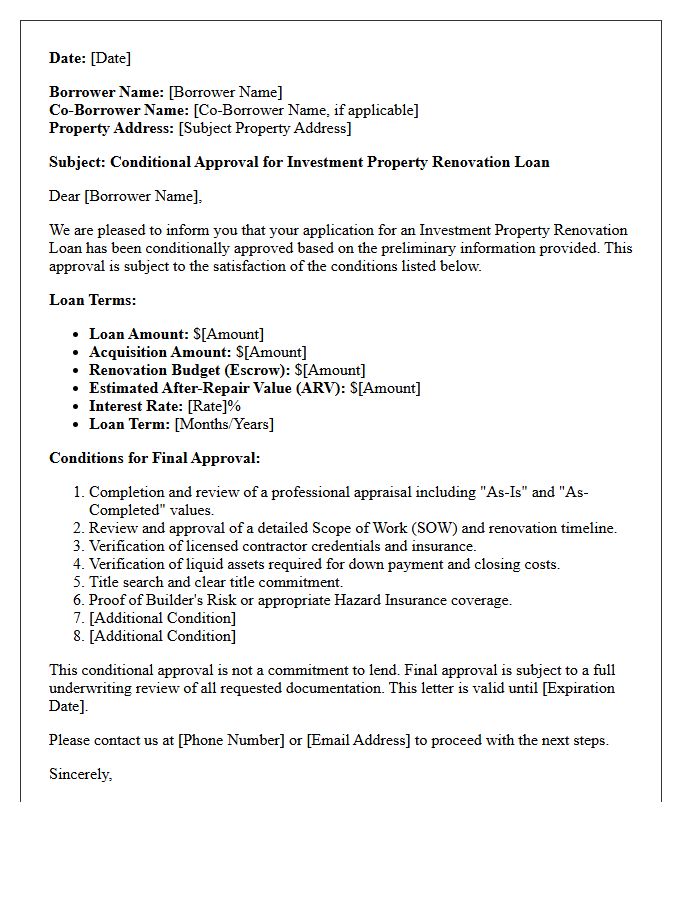

Investment Property Renovation Loan Conditional Approval Letter

An Investment Property Renovation Loan Conditional Approval Letter is a lender commitment indicating you meet primary eligibility criteria for financing. It outlines specific contingencies, such as property appraisals, detailed renovation bids, and financial verification, that must be satisfied before final funding. This document is essential for securing contractors and proving financial credibility to sellers. While it signals strong progress, it is not a guarantee of capital until all underwriting conditions are officially cleared and the loan enters the final approval stage.

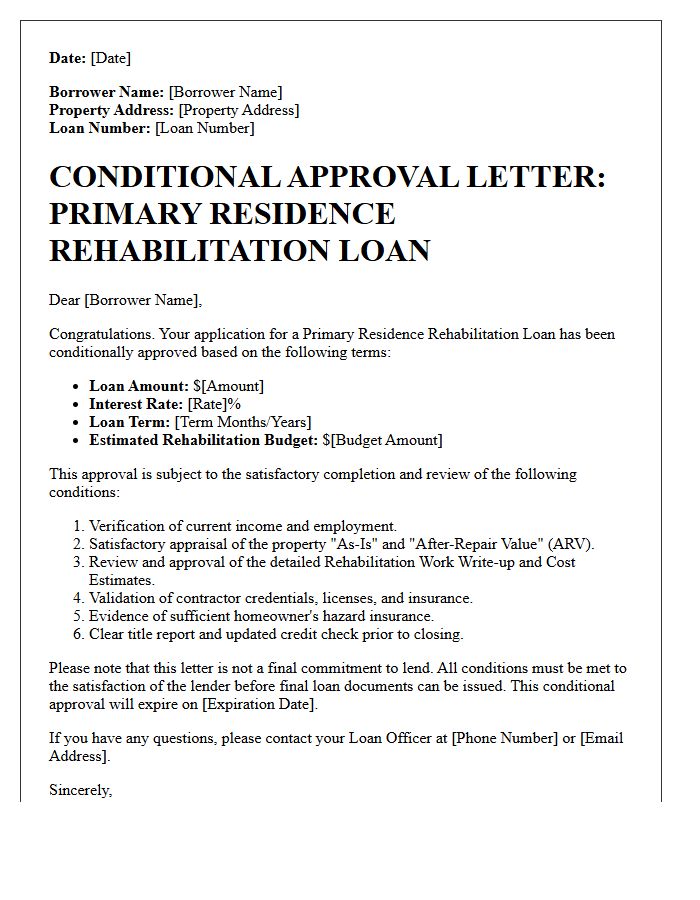

Primary Residence Rehabilitation Loan Conditional Approval Letter

A Primary Residence Rehabilitation Loan Conditional Approval Letter is a critical document indicating that a lender has preliminarily approved your financing based on initial criteria. It specifies the loan amount and interest rate, but approval remains subject to fulfilling mandatory conditions. These typically include a satisfactory property appraisal, detailed renovation plans, and final income verification. Receiving this letter is a significant milestone, proving your financial eligibility to sellers or contractors while you work toward the final loan commitment and the transformation of your home.

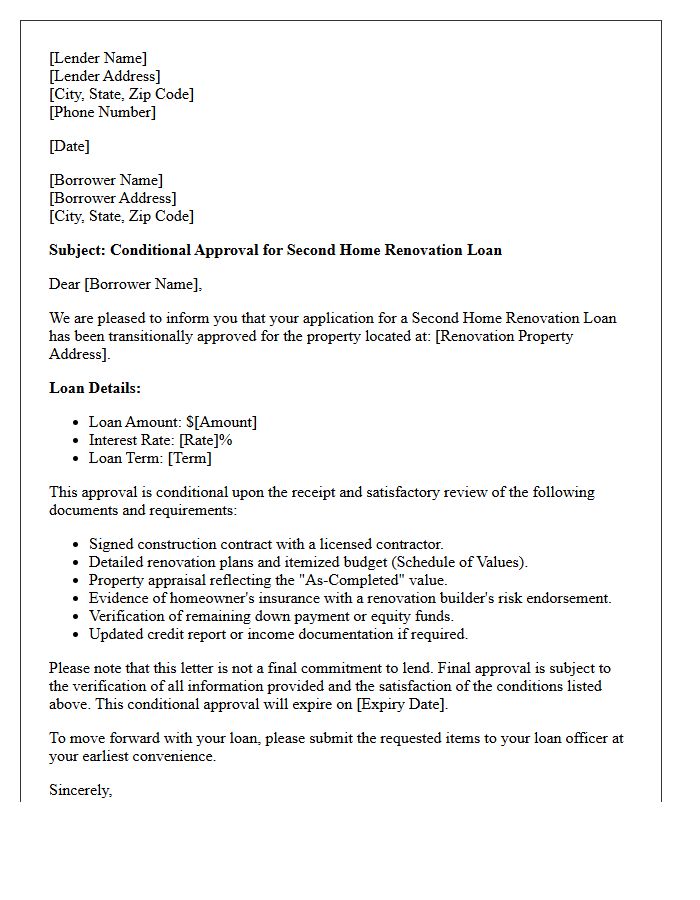

Second Home Renovation Loan Conditional Approval Letter

A Second Home Renovation Loan Conditional Approval Letter is a formal document from a lender indicating your mortgage application is approved pending specific requirements. It highlights your creditworthiness and estimated loan terms but is not a final commitment. To secure funding, you must satisfy outstanding conditions, such as property appraisals, updated financial verification, or construction plans. Receiving this letter is a critical milestone, signaling that you are close to financing your vacation property improvements once all underwriter stipulations are met and verified.

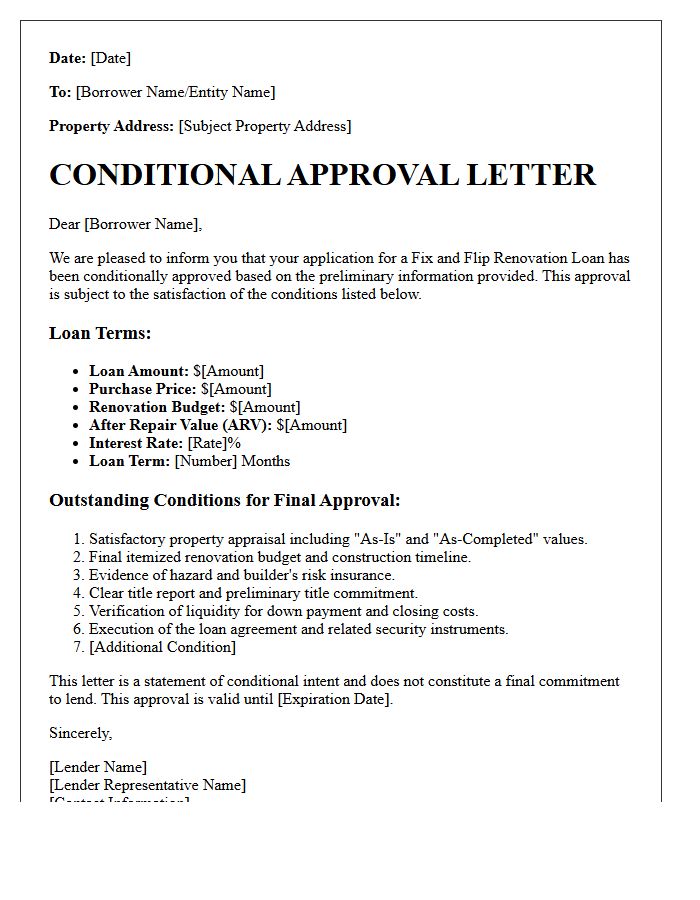

Fix And Flip Renovation Loan Conditional Approval Letter

A Fix and Flip Renovation Loan Conditional Approval Letter is a critical document issued by a lender after a preliminary file review. It signals that your real estate project meets initial underwriting standards, contingent upon meeting specific requirements. These conditions often include a final property appraisal, detailed scope of work verification, and proof of liquid assets. While not a final commitment, this letter provides the necessary leverage to make competitive offers, showing sellers you have the financing capacity to execute a successful property transformation and exit strategy.

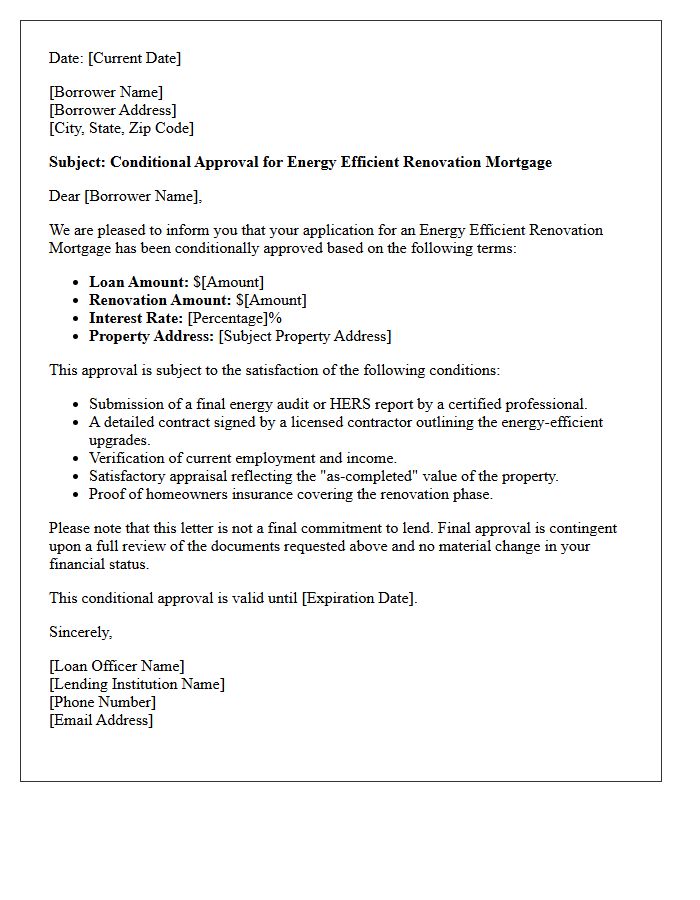

Energy Efficient Renovation Mortgage Conditional Approval Letter

An Energy Efficient Renovation Mortgage Conditional Approval Letter is a lender's preliminary commitment to finance a home purchase plus green upgrades. It specifies the maximum loan amount and necessary conditions, such as energy audits or professional quotes, required for final funding. This document proves financial readiness to sellers while ensuring the property meets specific efficiency standards. Securing this letter is the first step toward integrating sustainable improvements into your home loan, ultimately reducing long-term utility costs and increasing overall property value through subsidized green financing.

What is a Renovation Loan Conditional Approval Letter?

A renovation loan conditional approval letter is a document from a lender stating they are willing to fund your home improvement project provided you meet specific requirements, such as submitting a final contractor bid or passing a property appraisal.

What are the common conditions listed in a renovation loan approval?

Common conditions include providing a detailed work write-up from a licensed contractor, obtaining a "subject-to-completion" appraisal, verifying updated income documentation, and securing necessary building permits for the proposed renovations.

Does a conditional approval guarantee I will receive the renovation funds?

No, a conditional approval is not a final guarantee. Funding is only released once the borrower and the contractor satisfy all the underwriter's stipulations and the loan reaches "clear to close" status.

How long does it take to get a conditional approval for a renovation loan?

Typically, it takes 3 to 7 business days to receive a conditional approval after submitting your initial application and financial documents, though complex structural projects may require additional review time.

Can I change my contractor after receiving a conditional approval letter?

You can change contractors, but it will likely void the current conditional approval. The lender must vet the new contractor's credentials, licenses, and insurance, which may require a re-underwriting of the renovation portion of the loan.

Comments