Securing a Self-Employed Borrower Conditional Approval Letter is a critical milestone in the mortgage process. It verifies that a lender has reviewed your business income and tax returns, confirming you meet initial underwriting guidelines subject to specific conditions. This document strengthens your position when making offers on a home. To help you get started, below are some ready to use template.

Image cover: Secure Your Mortgage: Self-Employed Borrower Conditional Approval Templates and Professional Samples

Letter Samples List

- Self-Employed Borrower Conditional Approval Letter

- Certified Public Accountant Income Verification Letter

- Business Expense and Deduction Explanation Letter

- Year-to-Date Profit and Loss Statement Letter

- Primary Business Operation and Location Letter

- Letter of Explanation for Recent Credit Inquiries

- Business Continuity and Continued Operation Letter

- Tax Return Extension and Filing Status Letter

- Large Bank Deposit Sourcing and Explanation Letter

- Co-Mingled Business and Personal Funds Clarification Letter

- Declining Business Revenue Explanation Letter

- Independent Contractor Status Verification Letter

- Business Ownership Percentage Breakdown Letter

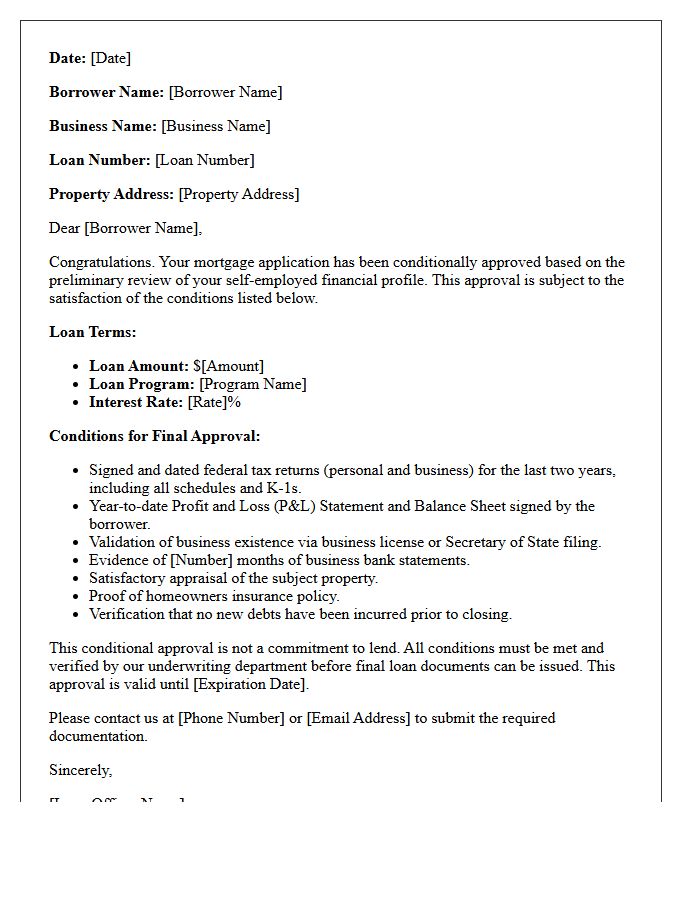

Self-Employed Borrower Conditional Approval Letter

A Self-Employed Borrower Conditional Approval Letter is a critical document indicating a lender's preliminary commitment to fund a mortgage. Unlike standard applications, this requires rigorous income verification through tax returns and profit-and-loss statements. The conditional status means the loan is approved only if specific requirements, such as business stability or updated audits, are met. It strengthens your position when making offers by proving your creditworthiness, despite the complexity of fluctuating revenue streams. Securing this letter ensures that your self-employment income meets strict underwriting guidelines before finalizing a home purchase.

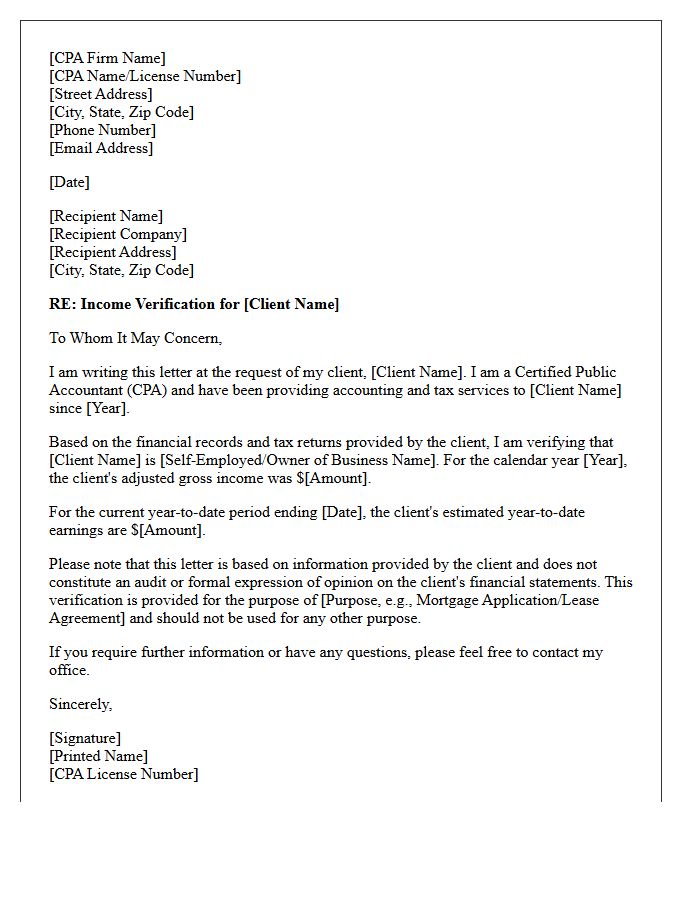

Certified Public Accountant Income Verification Letter

A Certified Public Accountant Income Verification Letter serves as official documentation to confirm an individual's earnings and financial standing. Lenders and landlords frequently require this formal statement to assess creditworthiness and loan eligibility for self-employed individuals. Unlike standard pay stubs, this letter provides a professional validation of net income, tax liabilities, and business stability. It carries significant weight because a CPA assumes responsibility for the accuracy of the financial data presented, ensuring that all reported figures align with verified tax filings and accounting records.

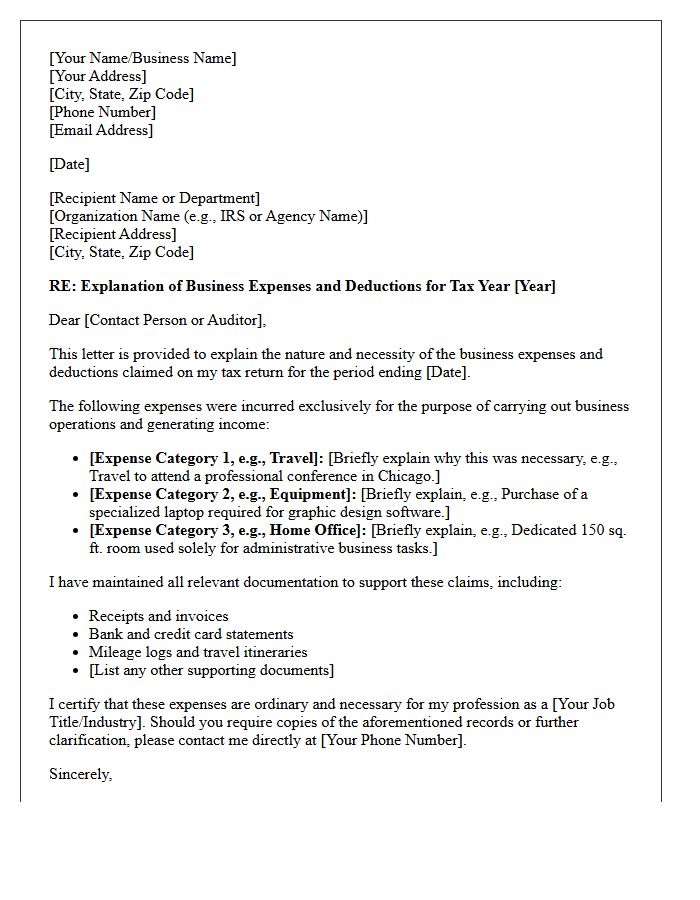

Business Expense and Deduction Explanation Letter

A Business Expense and Deduction Explanation Letter serves as a formal justification for specific costs reported to tax authorities. It provides context for unusual or high-value deductions that might otherwise trigger an audit. This document should clearly detail how each expense is ordinary and necessary for your trade. By proactively including clear descriptions and supporting evidence, you demonstrate transparency and compliance. Using this letter helps clarify the business purpose of expenditures, ensuring that your tax filings are accurately understood and defensible during a professional review or internal verification process.

Year-to-Date Profit and Loss Statement Letter

A Year-to-Date (YTD) Profit and Loss Statement Letter provides a formal financial summary of a company's performance from the beginning of the current fiscal year to the present date. It highlights total revenue, expenses, and net income, offering lenders or stakeholders an immediate view of current profitability. This document is essential for loan applications or verifying income when full-year audited statements are not yet available. Ensuring accurate categorization of costs is critical for demonstrating business stability and maintaining financial transparency during mid-year evaluations.

Primary Business Operation and Location Letter

The Primary Business Operation and Location Letter is a formal document verifying a company's physical presence and core activities. Financial institutions and regulators use this to mitigate risk by confirming that a business operates from a legitimate office rather than a mere shell address. It typically details the specific nature of services provided and the exact geographic coordinates of daily functions. Providing an accurate letter ensures compliance with Know Your Customer (KYC) protocols, facilitating smoother banking relationships and legal transparency in international commerce.

Letter of Explanation for Recent Credit Inquiries

A Letter of Explanation for recent credit inquiries is a formal document required by mortgage lenders to clarify why you sought new credit. It ensures you are not taking on undisclosed debt that could impact your debt-to-income ratio. You must list each inquiry, state the purpose-such as shopping for a car or home insurance-and confirm whether a new account was actually opened. Providing a clear, signed statement helps underwriters assess your financial stability and ensures your loan approval process remains on track without unexpected delays.

Business Continuity and Continued Operation Letter

A Business Continuity and Continued Operation Letter is a critical document that reassures stakeholders of an organization's resilience during disruptions. It outlines formal procedures to maintain essential functions, protecting revenue and operational integrity. This letter proves that the entity has proactive strategies to mitigate risks and ensure service delivery remains uninterrupted. Providing such documentation builds trust with clients and regulatory bodies by demonstrating a commitment to long-term stability and preparedness against unforeseen emergencies or systemic failures.

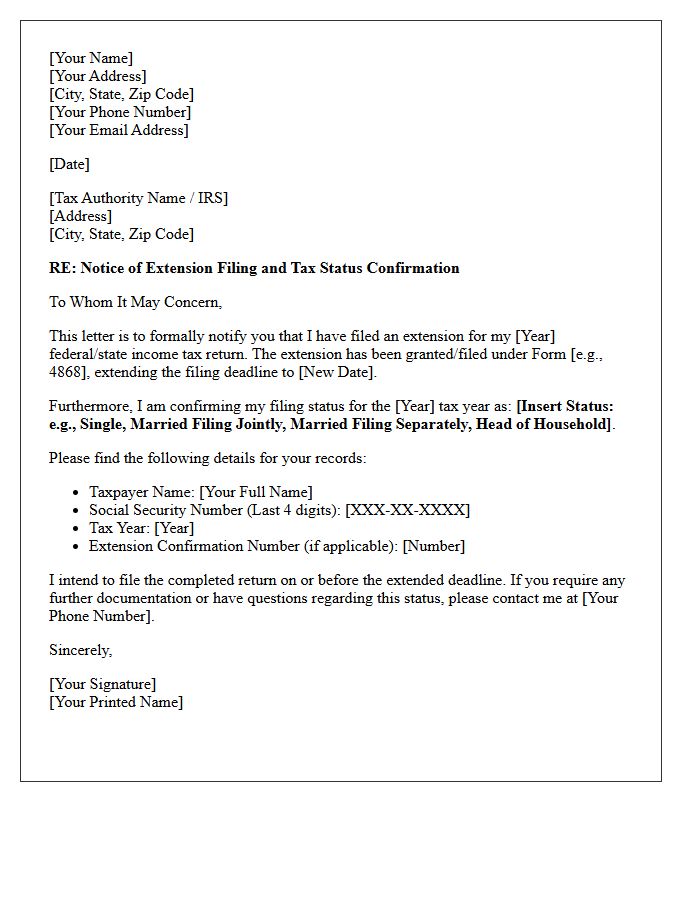

Tax Return Extension and Filing Status Letter

A tax return extension provides extra time to file your federal forms, typically moving the deadline to October 15. However, it does not grant an extension to pay any taxes owed. To verify your current standing, a Filing Status Letter acts as official IRS verification confirming whether a return was filed or if you are exempt for a specific year. These documents are essential for financial transparency during mortgage applications, student aid requests, or legal audits to prove compliance with tax regulations.

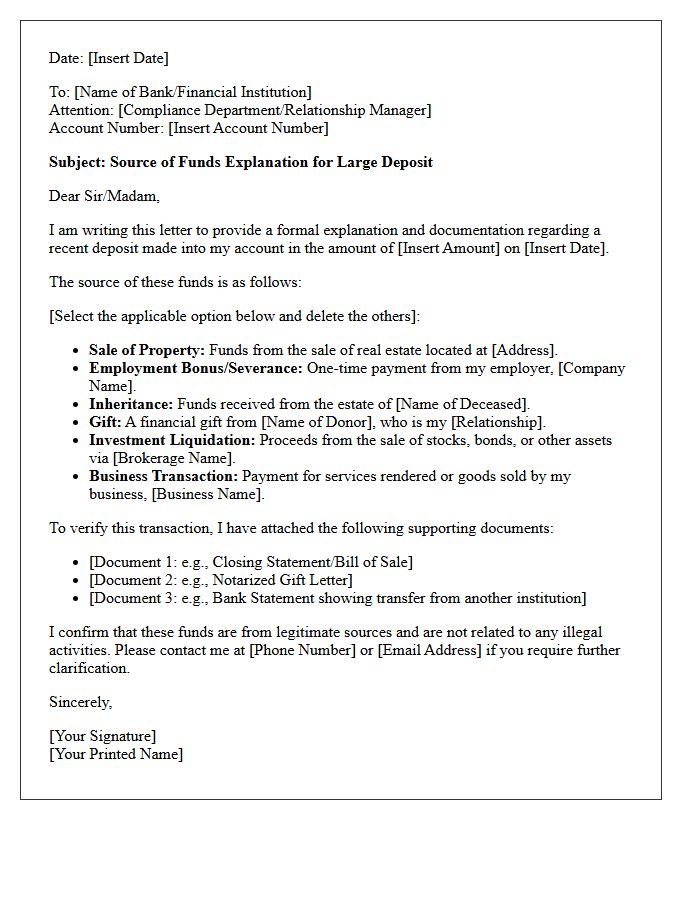

Large Bank Deposit Sourcing and Explanation Letter

When applying for a mortgage, lenders require a Large Bank Deposit Sourcing and Explanation Letter to verify the legal origin of significant funds. Any credit beyond normal payroll must be documented to ensure it is not an undisclosed loan or from an illicit source. You must provide a signed statement along with supporting evidence, such as bills of sale or gift letters. Clear documentation ensures compliance with anti-money laundering regulations and confirms your ability to cover the down payment without increasing your overall debt-to-income ratio.

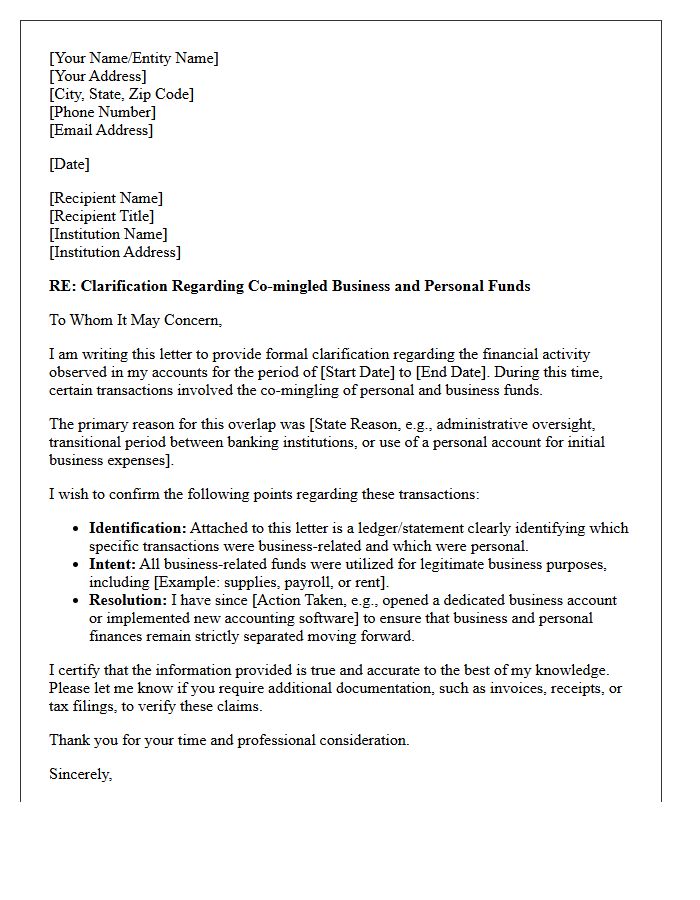

Co-Mingled Business and Personal Funds Clarification Letter

A Co-Mingled Business and Personal Funds Clarification Letter is a formal document used to explain overlapping transactions between private and commercial accounts. It is crucial for financial transparency during audits, loan applications, or tax reviews. This letter clarifies that business assets remain distinct from personal wealth, protecting the company's corporate veil and legal liability status. By detailing specific transfers and providing a clear reconciliation of funds, business owners can justify expenditures, ensure accurate bookkeeping, and maintain credibility with lenders, investors, or regulatory authorities regarding their fiscal management practices.

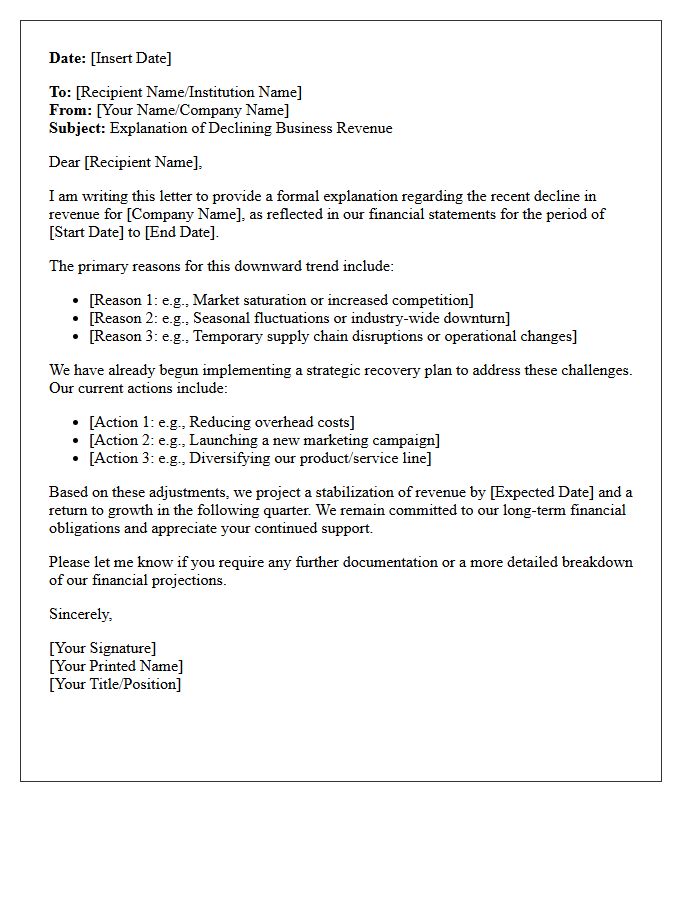

Declining Business Revenue Explanation Letter

A Declining Business Revenue Explanation Letter provides transparency to stakeholders, such as lenders or investors, regarding financial setbacks. It should objectively detail the specific causes of the downturn, whether due to market shifts, operational hurdles, or temporary economic trends. Crucially, the letter must outline a strategic recovery plan to demonstrate future viability. Maintaining a professional tone helps rebuild credibility and reassures partners of your commitment to stabilizing cash flow. Being proactive in sharing this information is essential for maintaining trust and securing continued support during challenging fiscal periods.

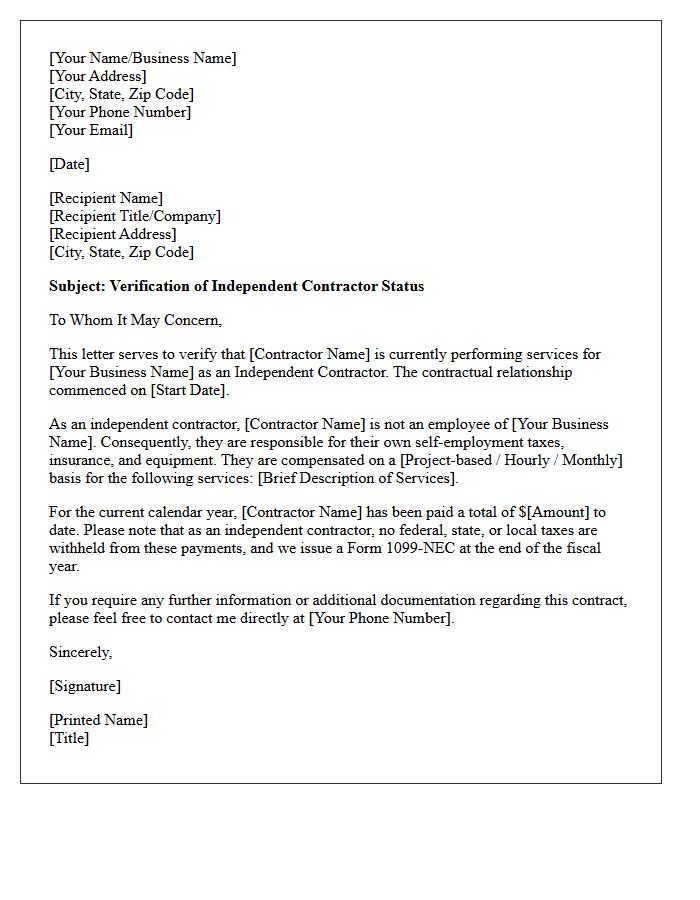

Independent Contractor Status Verification Letter

An Independent Contractor Status Verification Letter serves as formal proof that a worker is self-employed rather than a traditional employee. This document is essential for legal compliance, as it clarifies tax obligations and limits employer liability regarding benefits or withholding. It typically confirms the non-employment relationship, project-based scope of work, and financial independence of the contractor. Businesses use these letters to mitigate risks of misclassification during audits, ensuring both parties adhere to regulatory standards and independent operating procedures under labor laws.

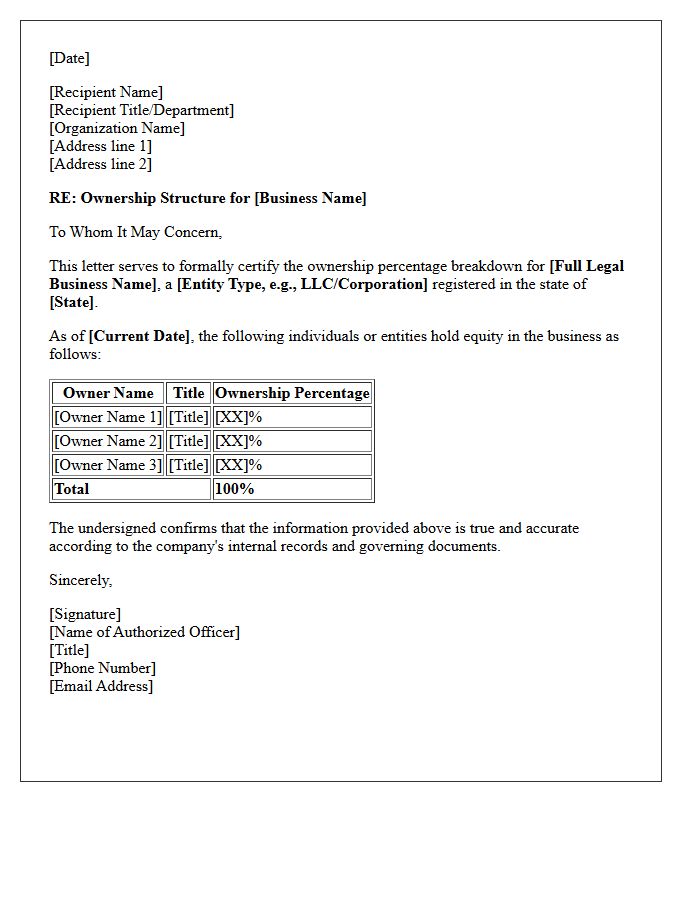

Business Ownership Percentage Breakdown Letter

A Business Ownership Percentage Breakdown Letter is a formal document verifying the specific equity distribution among stakeholders. It officially confirms each owner's share of the company, which is essential for legal compliance, tax filings, and securing bank loans. This letter must include the legal business name, individual names of all owners, and their corresponding ownership percentages. Having a signed, accurate breakdown ensures transparency during audits or partnership changes and serves as a vital record for corporate governance and investor relations.

What is a self-employed borrower conditional approval letter?

A self-employed borrower conditional approval letter is a formal document from a mortgage lender stating that an entrepreneur or business owner is approved for a specific loan amount, provided they satisfy certain requirements such as tax return verification or business debt-to-income audits.

What specific conditions are usually required for self-employed mortgage approval?

Common conditions include providing the most recent two years of signed federal personal and business tax returns, a year-to-date Profit and Loss (P&L) statement, balance sheets, and verification of business existence through a CPA letter or business license.

How does a conditional approval differ from a pre-qualification for business owners?

A pre-qualification is a surface-level estimate based on unverified data, whereas a conditional approval for a self-employed borrower involves a preliminary underwriter review of actual financial documents and tax transcripts, making it a much stronger commitment to lend.

Why do lenders require a year-to-date Profit and Loss statement for conditional approval?

Lenders require a YTD Profit and Loss statement to ensure the business's current earnings are consistent with the income reported on previous tax returns and to verify that the borrower's cash flow has not significantly declined since the last filing.

Can I use my business funds for a down payment after receiving a conditional approval?

Yes, but the lender will require a "business pull" analysis to ensure that withdrawing the down payment funds will not negatively impact the operations or solvency of the business as part of the final approval process.

Comments