An Annual Escrow Account Disclosure Statement provides a detailed summary of your mortgage escrow activity over the past year. It tracks property tax payments, insurance premiums, and any required balance adjustments to ensure your monthly payments remain accurate. Understanding this document helps you manage your homeownership costs effectively. To help you draft or understand these notices, below are some ready to use template.

Image cover: Mastering Your Annual Escrow Account Disclosure Statement: Samples and Templates

Letter Samples List

- Annual Escrow Account Disclosure Statement Letter

- Escrow Account Shortage Notification Letter

- Escrow Account Surplus Refund Letter

- Escrow Account Deficiency Notice Letter

- Escrow Monthly Payment Adjustment Letter

- Annual Escrow Analysis Explanation Letter

- Escrow Property Tax Disbursement Letter

- Escrow Hazard Insurance Payment Letter

- Escrow Account History and Summary Letter

- Escrow Account Transfer Notification Letter

- Escrow Waiver and Cancellation Letter

- Mortgage Escrow Account Closing Letter

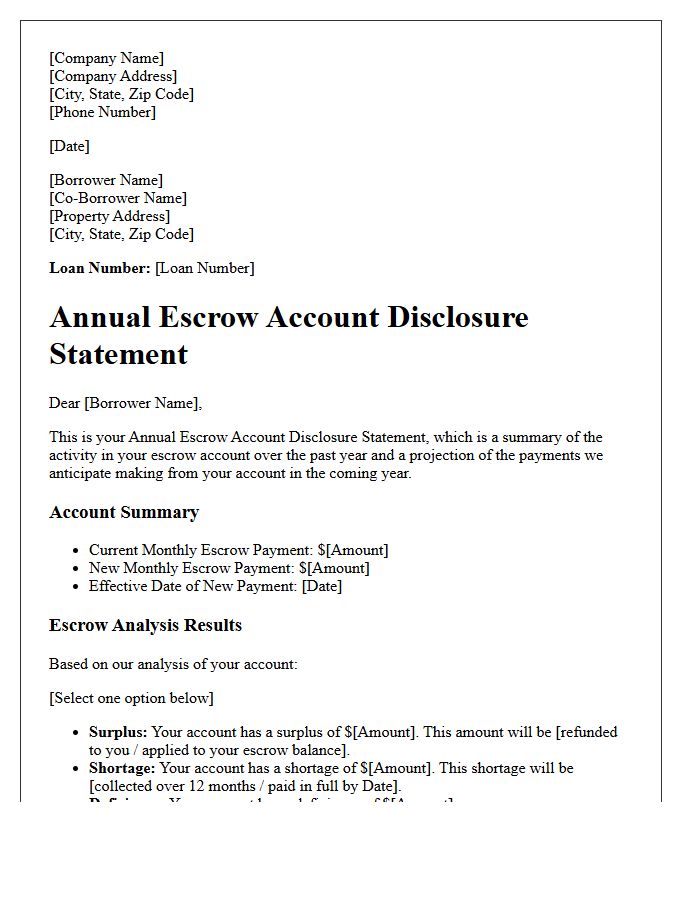

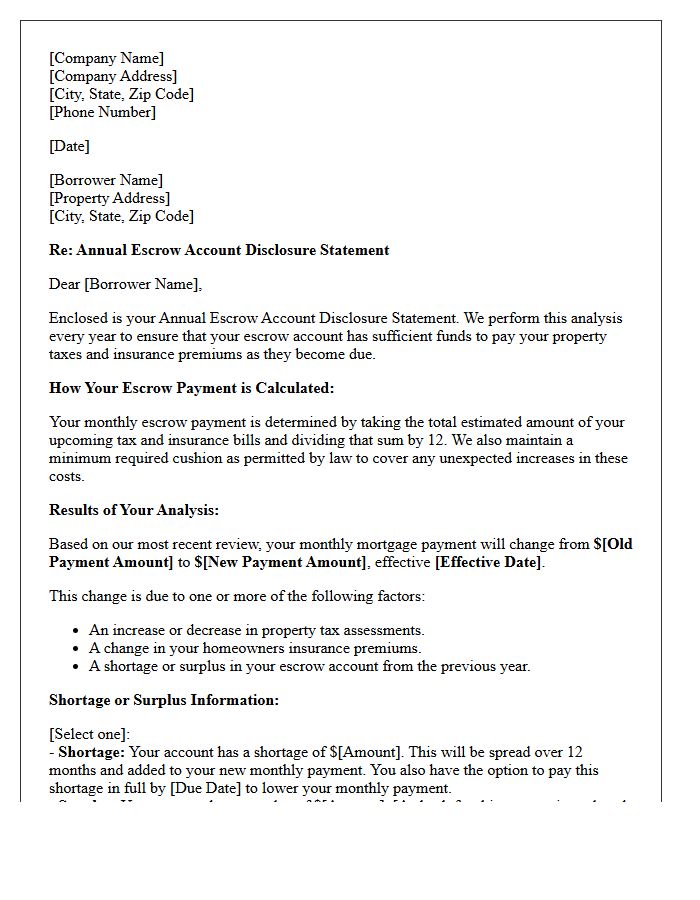

Annual Escrow Account Disclosure Statement Letter

The Annual Escrow Account Disclosure Statement is a vital document summarizing your mortgage account's tax and insurance payments. It provides a detailed projection of upcoming costs to ensure your monthly payments cover expected liabilities. Reviewing this statement is essential because it reveals potential shortages or surpluses, which may result in adjusted monthly mortgage installments. Understanding this year-end summary helps homeowners budget for changes in property taxes or insurance premiums while ensuring the lender maintains a sufficient minimum balance to protect the property investment.

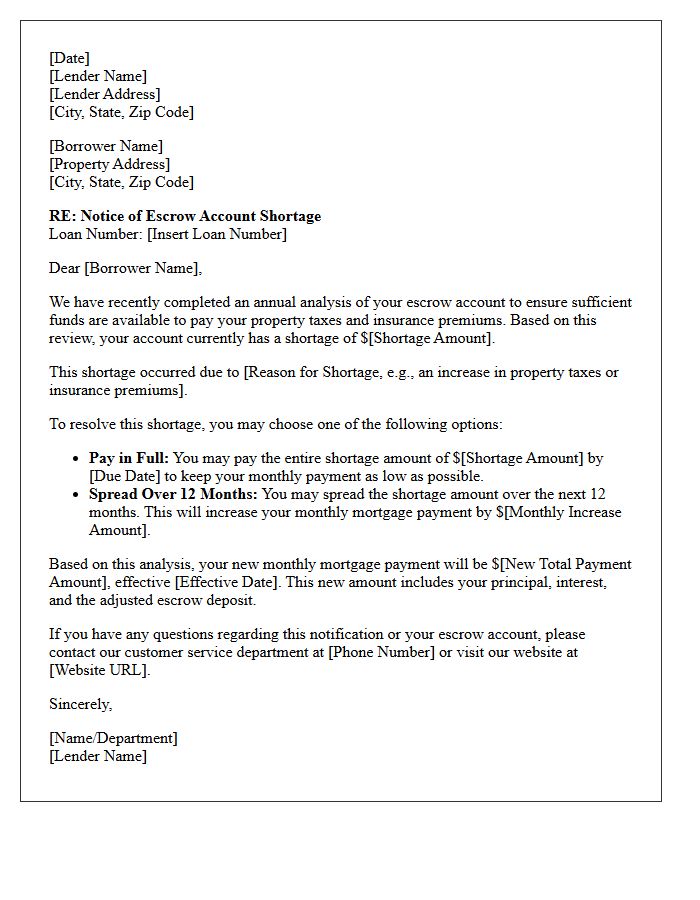

Escrow Account Shortage Notification Letter

An Escrow Account Shortage Notification Letter informs homeowners that their property tax or insurance payments exceeded the funds available in their escrow account. This occurs when escrow disbursements rise unexpectedly, creating a deficit. To resolve the gap, lenders typically offer options: paying the entire shortage amount upfront or spreading the balance across future monthly mortgage payments. Reviewing this notice promptly is essential to understand changes in your monthly housing costs and ensure your mortgage remains in good standing while maintaining adequate coverage for taxes and insurance premiums.

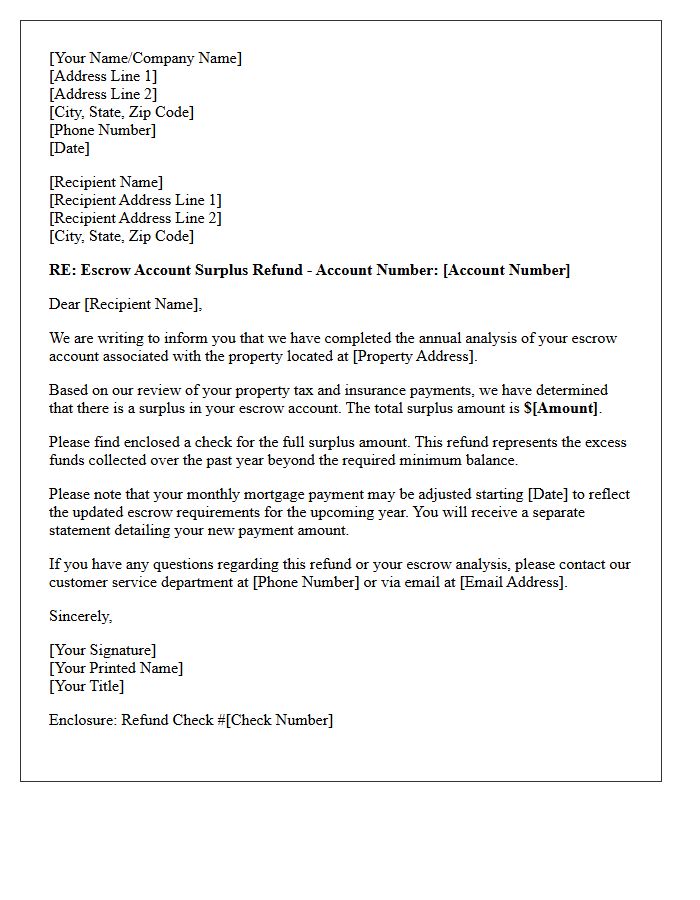

Escrow Account Surplus Refund Letter

An Escrow Account Surplus Refund Letter is an official notice from your mortgage lender confirming that your escrow analysis resulted in an overage. This surplus occurs when your actual property taxes or insurance premiums were lower than the estimated payments collected. The letter typically includes a refund check for the excess balance. It is important to review this document to understand changes in your monthly mortgage payment and to ensure your tax information remains accurate. Always verify the refund amount against your annual escrow statement for financial transparency.

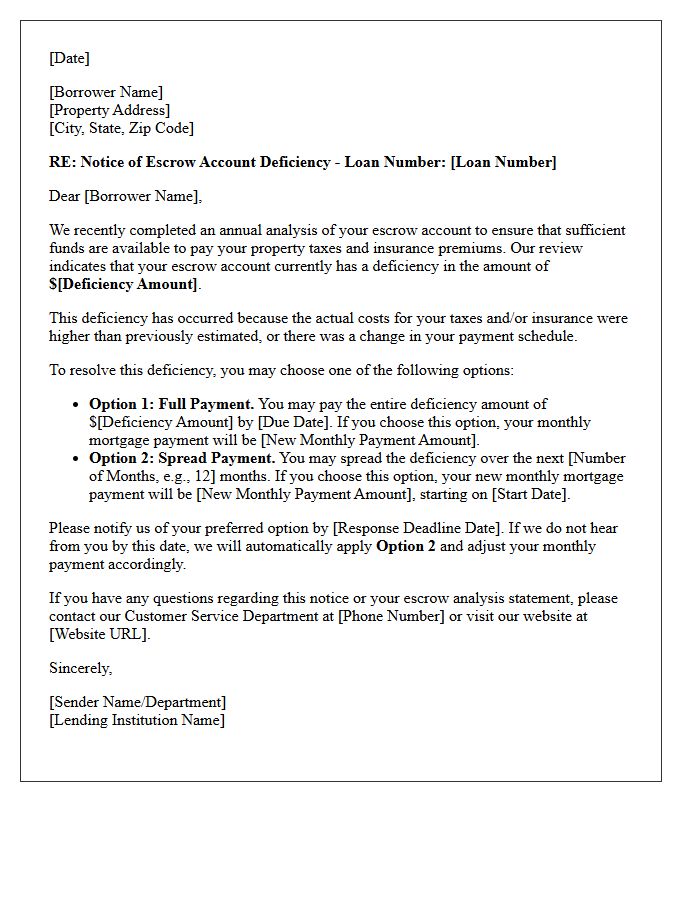

Escrow Account Deficiency Notice Letter

An Escrow Account Deficiency Notice Letter informs homeowners that their account balance is below the required minimum threshold. This typically occurs due to rising property taxes or insurance premiums. To resolve this, lenders may offer options like a one-time lump sum payment or increased monthly installments. It is crucial to review your annual escrow analysis statement to verify these changes. Promptly addressing a deficiency ensures your taxes and insurance remain fully funded, preventing potential payment defaults or unexpected financial strain on your mortgage agreement.

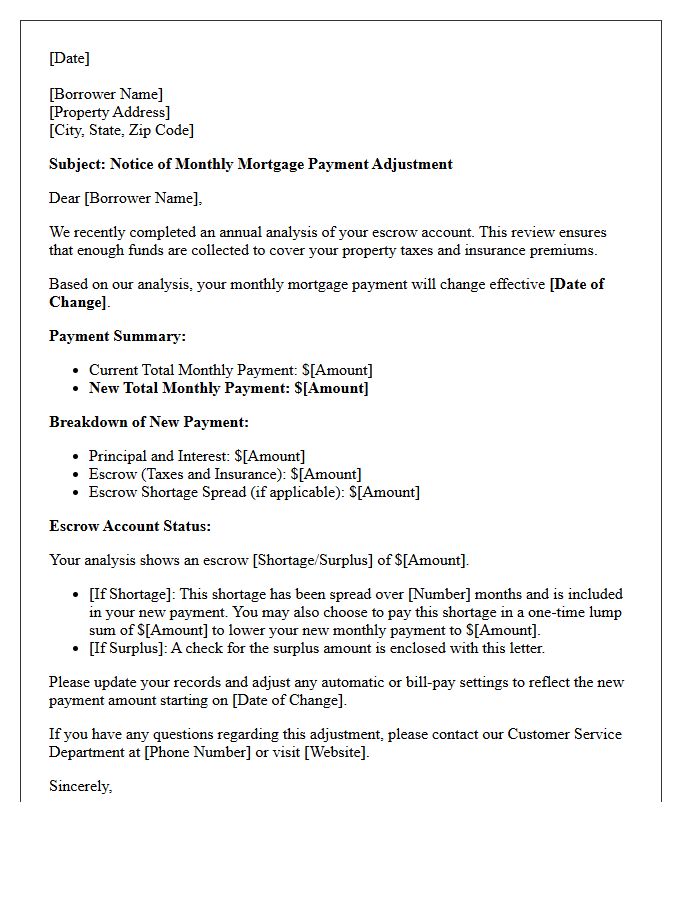

Escrow Monthly Payment Adjustment Letter

An Escrow Monthly Payment Adjustment Letter informs homeowners about changes to their mortgage payment due to an annual analysis. This review ensures sufficient funds for property taxes and insurance premiums. If these costs rise, your monthly obligation increases to cover the gap or address an escrow shortage. Conversely, lower costs may result in a surplus refund. It is essential to review this notice to understand how escrow rebalancing impacts your budget and ensures your loan compliance throughout the year.

Annual Escrow Analysis Explanation Letter

An Annual Escrow Analysis Explanation Letter is a mandatory document sent by your mortgage servicer to review your escrow account balance. This statement compares estimated property taxes and insurance premiums against actual payments made. If your costs increased, you might face a shortage, resulting in higher monthly mortgage payments. Conversely, a surplus may trigger a refund check. Reviewing this letter is essential to understand changes in your housing budget and ensure your lender maintains the required minimum cushion to cover future tax and insurance obligations.

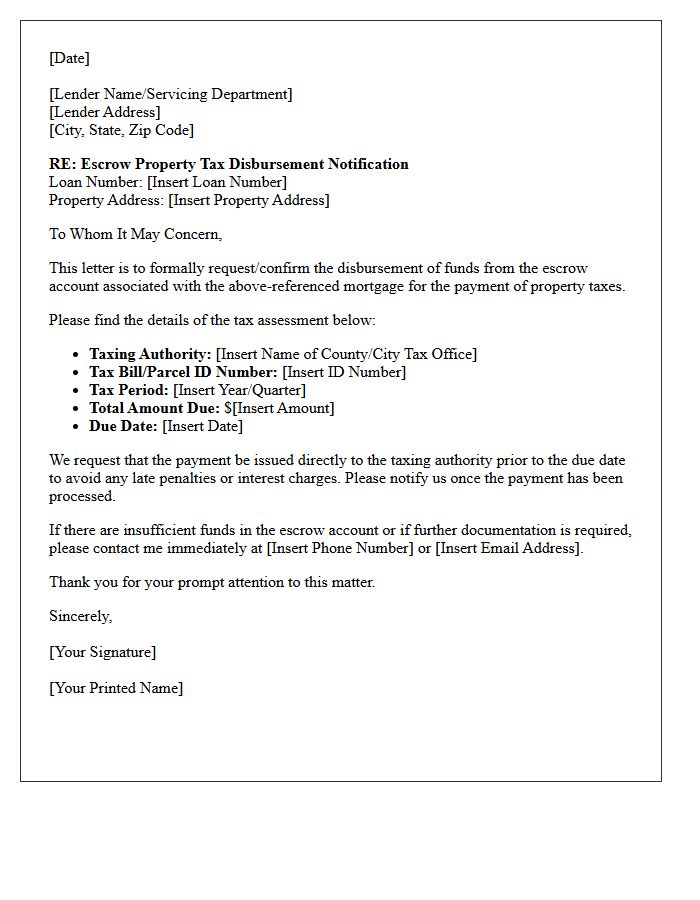

Escrow Property Tax Disbursement Letter

An Escrow Property Tax Disbursement Letter is a formal notification confirming that your mortgage servicer has paid your local property taxes using funds from your escrow account. It is crucial to verify that the payment amount and recipient jurisdiction match your tax bill to prevent delinquencies. Homeowners should retain this document for tax filing purposes, as it provides evidence of deductible expenses. If you receive a delinquency notice despite getting this letter, contact your lender immediately to resolve potential processing errors or escrow shortages.

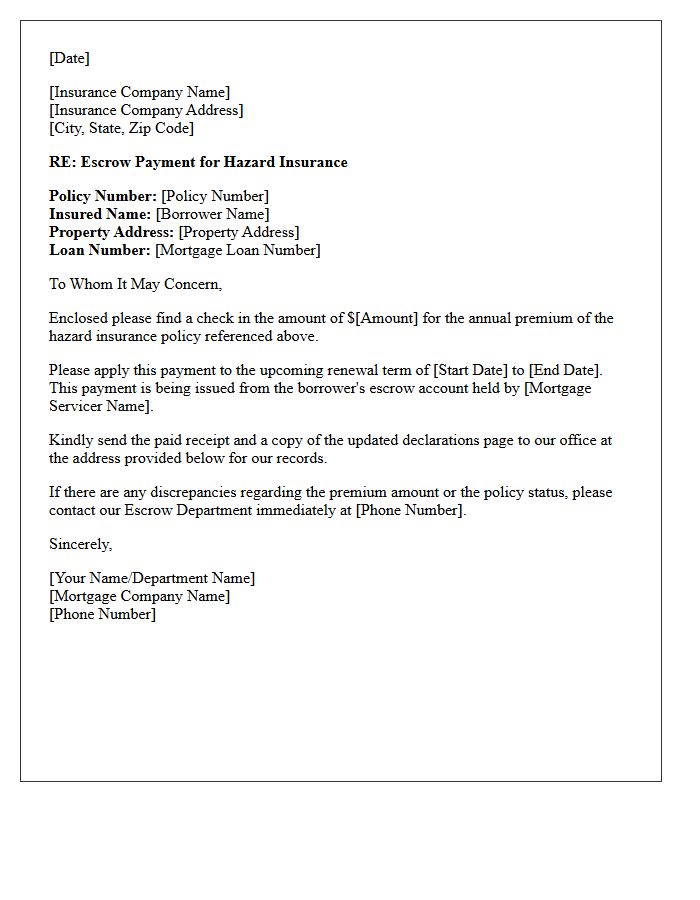

Escrow Hazard Insurance Payment Letter

An Escrow Hazard Insurance Payment Letter is a formal notice sent by your mortgage servicer confirming that your homeowners insurance premium has been paid using funds from your escrow account. It is crucial to verify this document to ensure your policy remains active and the coverage amounts meet lender requirements. If you receive a delinquency notice from your insurer despite this letter, contact your servicer immediately to prevent a lapse in protection or the imposition of costly force-placed insurance.

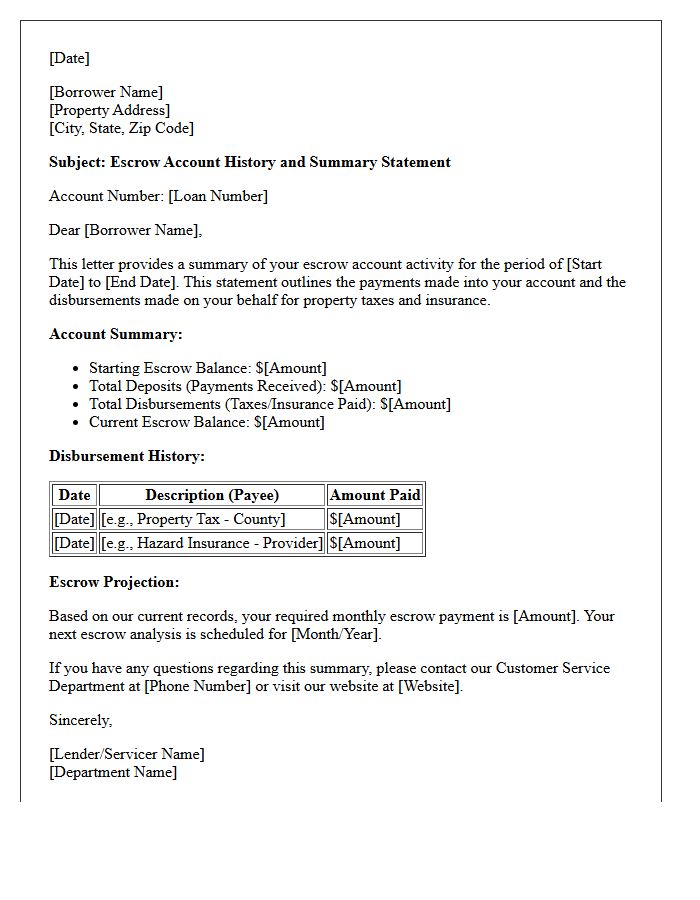

Escrow Account History and Summary Letter

An Escrow Account History and Summary Letter provides a detailed annual review of your mortgage impound account. This document outlines past payments for property taxes and insurance while projecting future costs to determine your monthly mortgage payment. It is the primary tool used to identify an escrow shortage or surplus. Reviewing this summary ensures your lender maintains adequate funds to cover essential obligations, helping you understand any adjustments to your total housing expense. Maintaining an accurate history prevents unexpected financial gaps during the fiscal year.

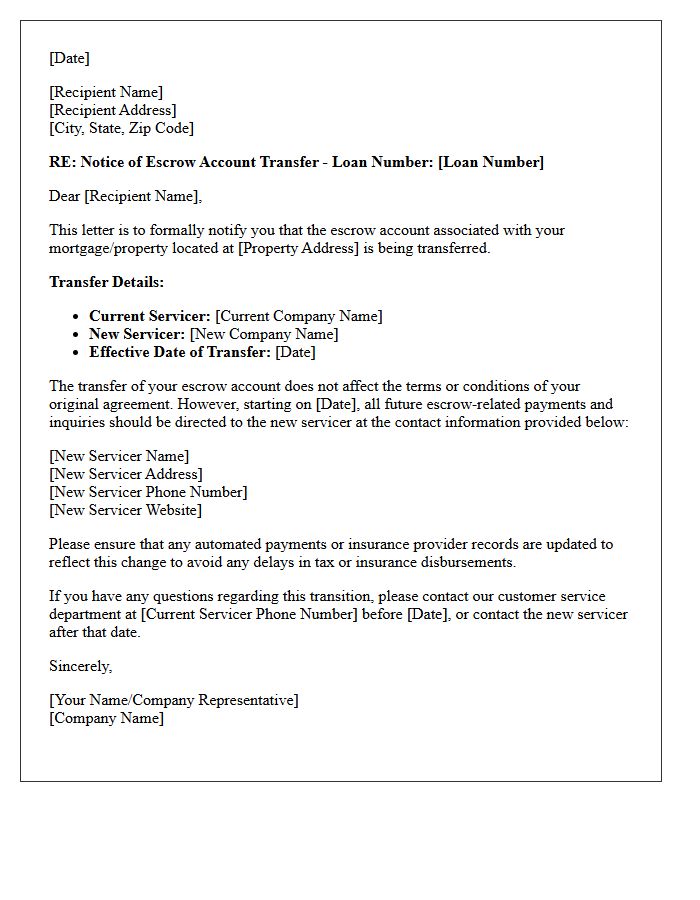

Escrow Account Transfer Notification Letter

An Escrow Account Transfer Notification Letter is a mandatory legal document informing homeowners that their mortgage servicing rights have been reassigned. It is crucial to verify the effective date of the transfer and the new payment mailing address to avoid late fees. This notice confirms that your tax and insurance funds remain secure during the transition. Review the letter carefully to update your records and ensure your loan number and payment amounts are accurate, maintaining seamless property tax and homeowners insurance coverage throughout the servicing transfer process.

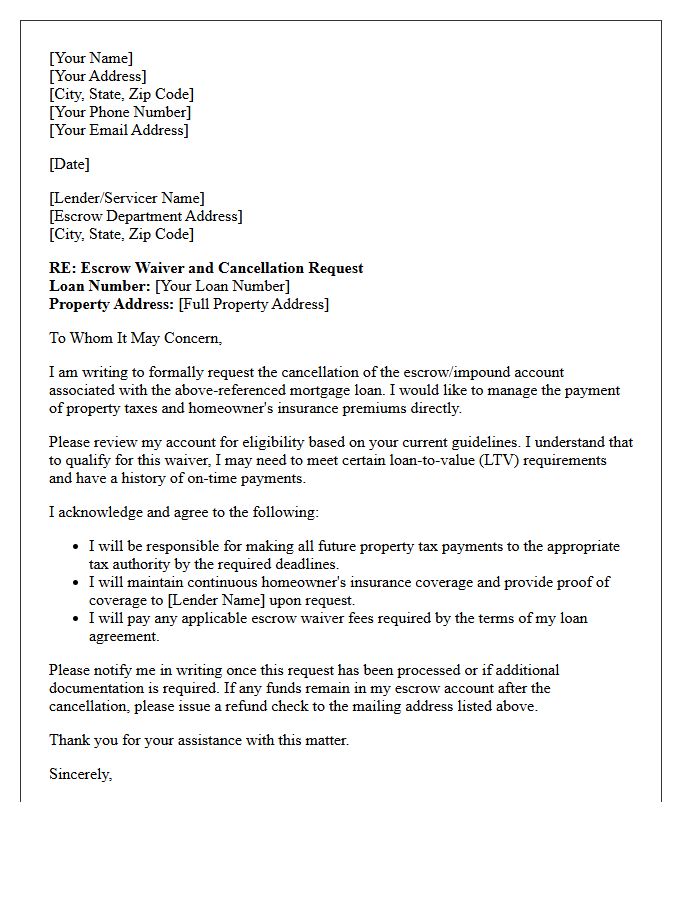

Escrow Waiver and Cancellation Letter

An Escrow Waiver and Cancellation Letter is a formal request sent to a mortgage lender to terminate an impound account. By submitting this document, homeowners seek to manage their own property taxes and insurance payments directly instead of through their servicer. To qualify, lenders typically require a minimum equity of 20% and a history of on-time payments. Once approved, the borrower assumes full responsibility for budgeting and meeting tax deadlines to avoid financial penalties or tax liens against the property. This process provides greater control over personal cash flow.

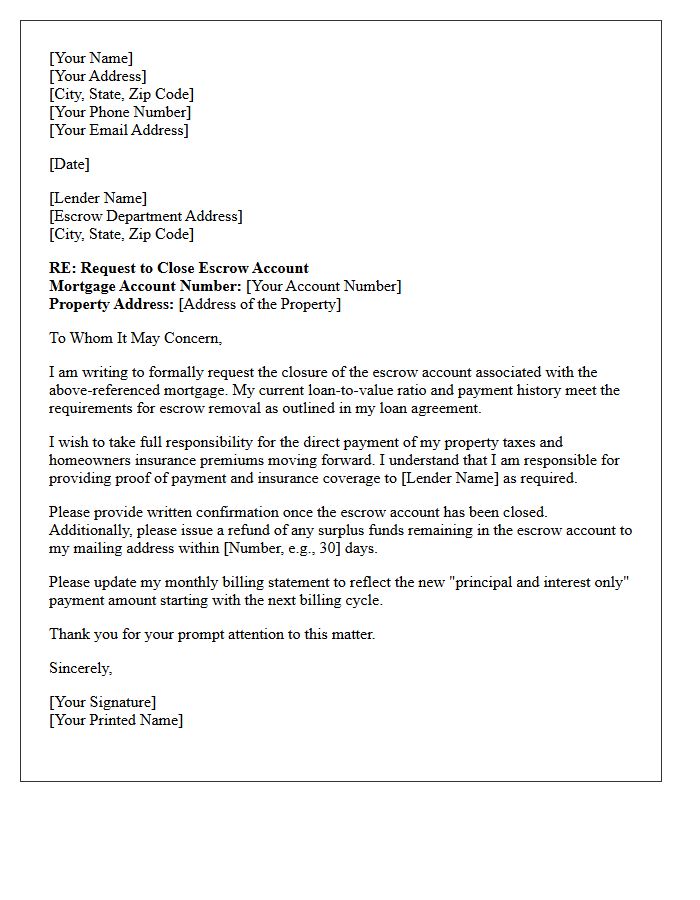

Mortgage Escrow Account Closing Letter

A Mortgage Escrow Account Closing Letter is a formal notification confirming that your servicer has finalized your escrow account, typically following a loan payoff or refinance. This document verifies that all outstanding property taxes and insurance premiums were paid. Crucially, it details any escrow refund owed to you, which must be issued within twenty days. Homeowners should retain this record to ensure their future tax payments are handled independently, as you are now directly responsible for managing those obligations once the account is closed.

What is an Annual Escrow Account Disclosure Statement?

An Annual Escrow Account Disclosure Statement is a document provided by your mortgage lender that summarizes the activity in your escrow account over the past year and projects payments for the upcoming year. It ensures that enough funds are being collected to cover property taxes and homeowners insurance premiums.

Why did my monthly mortgage payment change after the escrow analysis?

Your monthly payment may change if there is an increase or decrease in your property taxes or insurance premiums. If the projected costs for these items rise, your lender must increase your monthly escrow contribution to ensure the account remains funded according to federal guidelines.

What is an escrow shortage and how can I pay it?

An escrow shortage occurs when your account balance falls below the required minimum due to rising tax or insurance costs. You typically have two options: pay the entire shortage amount in a single lump sum, or spread the shortage amount across your monthly mortgage payments over the next 12 months.

What happens if I have an escrow surplus?

An escrow surplus occurs when the balance in your account exceeds the required amount. If the surplus is $50 or more, federal law generally requires the lender to issue you a refund check within 30 days of the analysis, provided your mortgage payments are current.

How is the required minimum escrow balance calculated?

Lenders calculate the minimum balance using "cushion" rules, which allow them to maintain a reserve of up to one-sixth (two months) of the total annual escrow disbursements. This cushion protects against unexpected increases in tax or insurance bills during the year.

Comments