Losing your job creates immediate financial strain, making it difficult to manage loan payments. An Unemployment Hardship Forbearance Notice is a formal request to temporarily pause or reduce your obligations while you seek new employment. This document protects your credit score and prevents default during transitions. To simplify the process, below are some ready to use template options.

Image cover: Navigating Financial Strain: Unemployment Hardship Forbearance Notice Templates and Samples

Letter Samples List

- Initial Unemployment Hardship Forbearance Request Letter

- Mortgage Forbearance Application Acknowledgment Letter

- Notice of Missing Documentation for Forbearance Letter

- Unemployment Hardship Forbearance Approval Notice Letter

- Temporary Mortgage Payment Suspension Agreement Letter

- Forbearance Plan Terms and Conditions Letter

- Unemployment Hardship Forbearance Denial Notice Letter

- Request for Additional Hardship Evidence Letter

- Forbearance Period Midpoint Status Update Letter

- Notice of Approaching Forbearance Expiration Letter

- Unemployment Hardship Forbearance Extension Request Letter

- Post-Forbearance Repayment Plan Options Letter

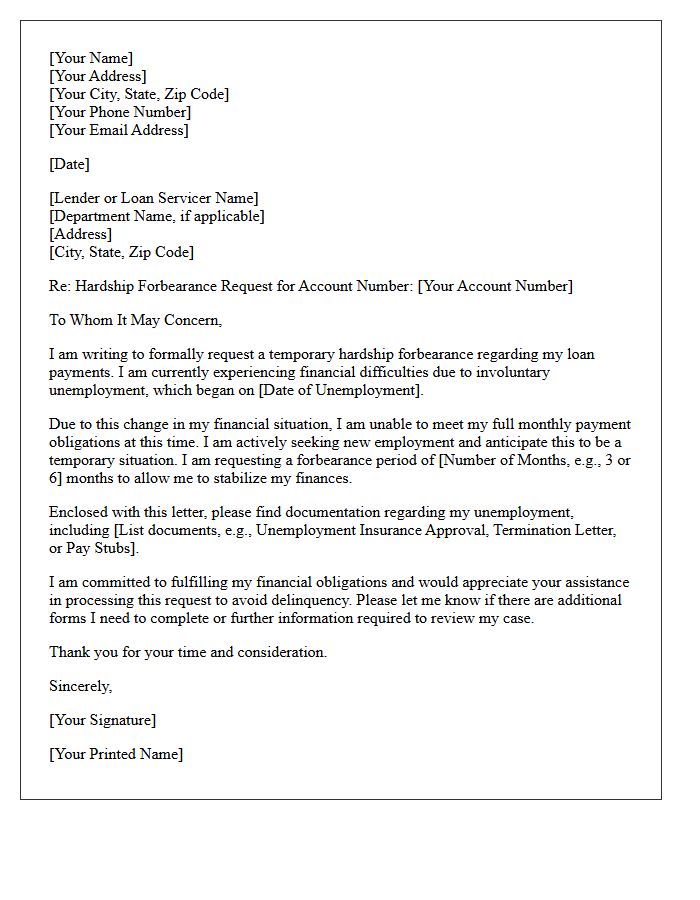

Initial Unemployment Hardship Forbearance Request Letter

An Initial Unemployment Hardship Forbearance Request Letter is a formal notice sent to lenders to temporarily pause or reduce loan payments. It is crucial to clearly state your involuntary job loss and provide supporting documentation, such as a termination notice. Explicitly request a specific forbearance period and mention your intent to resume regular payments once employed. Promptly submitting this letter helps protect your credit score and prevents loan default during financial instability. Always include your account details and current contact information to ensure a timely response from your loan servicer.

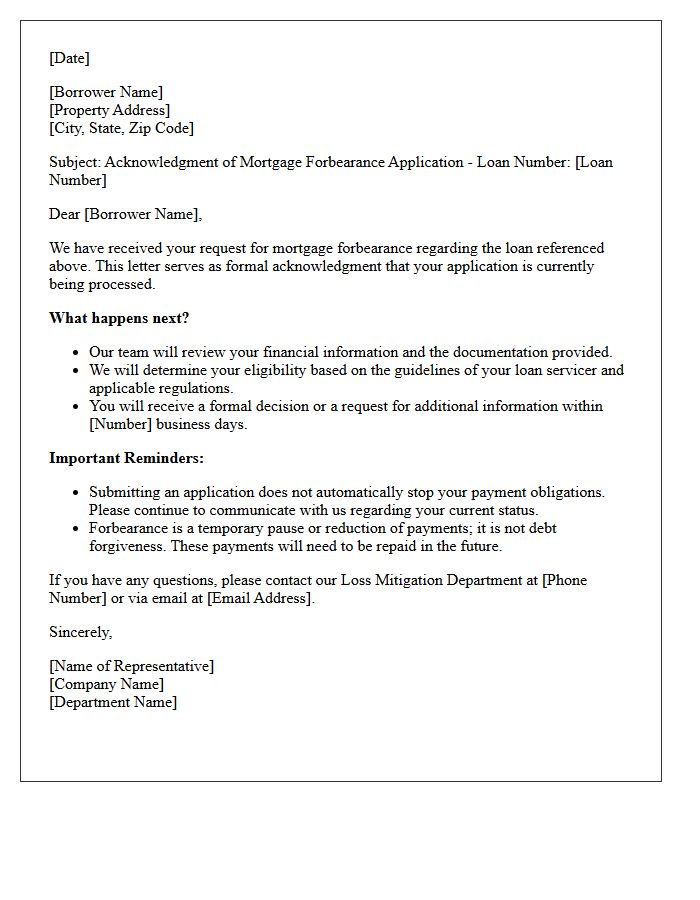

Mortgage Forbearance Application Acknowledgment Letter

A Mortgage Forbearance Application Acknowledgment Letter is a formal document from your lender confirming they received your request for payment relief. This notice serves as proof that your application is being processed and typically outlines the temporary suspension or reduction of monthly payments. It is crucial to review this letter for accuracy regarding your financial hardship details and the specified timeline. While this confirms receipt, it is not a final approval. Retain this correspondence to protect your credit rights and ensure clear communication throughout the loss mitigation process.

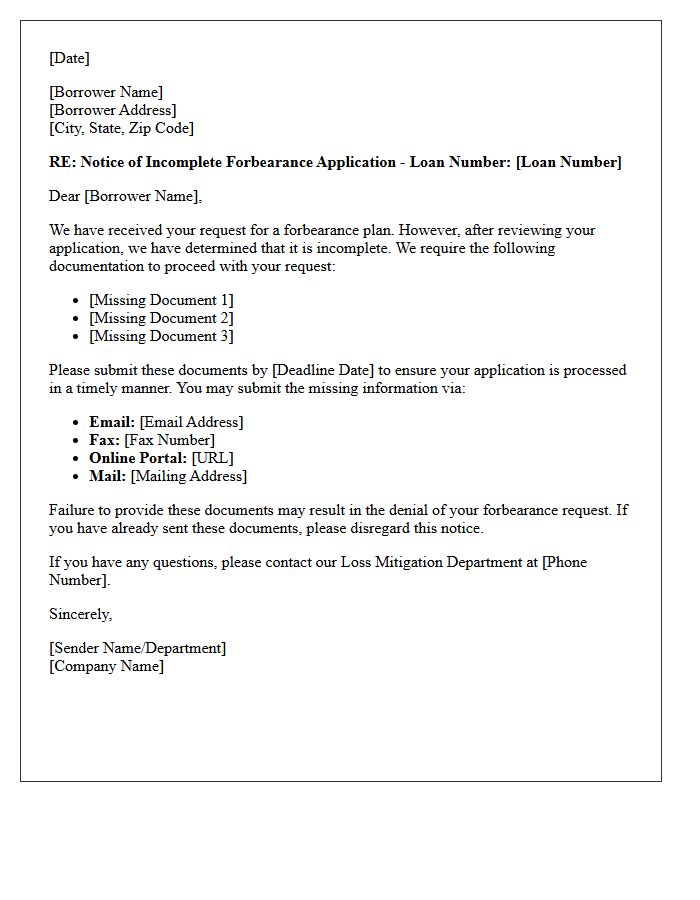

Notice of Missing Documentation for Forbearance Letter

A Notice of Missing Documentation for forbearance is a critical alert from your loan servicer. This letter indicates that your request is incomplete because specific financial records are absent. To prevent a denial of your relief plan, you must submit the requested items immediately. Key requirements often include proof of income, hardship statements, or tax returns. Act quickly to ensure your forbearance application remains active, as missing deadlines can lead to foreclosure proceedings or late penalties. Always verify receipt of documents to maintain your eligibility for payment suspension.

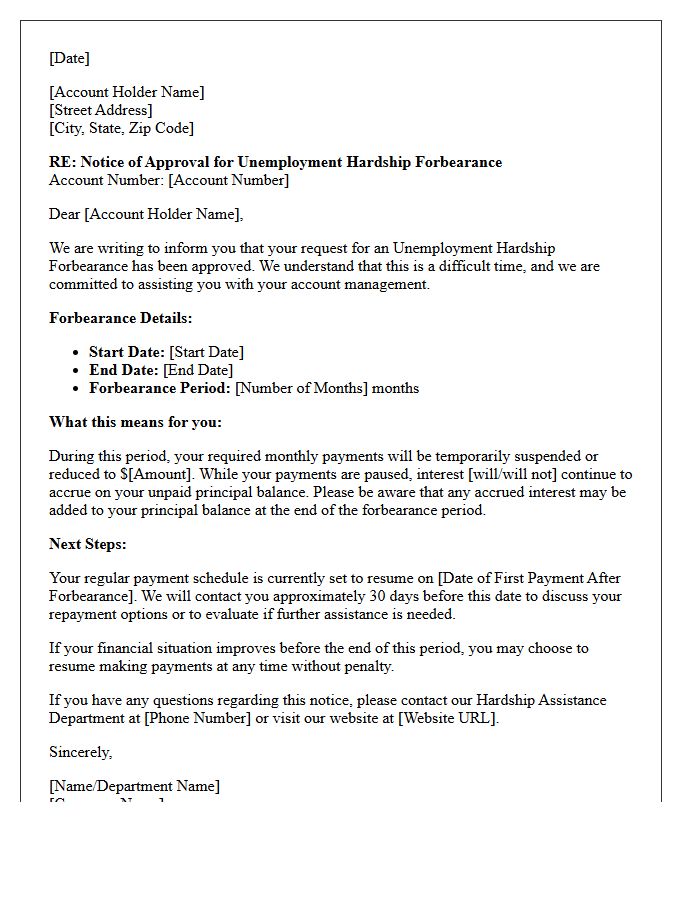

Unemployment Hardship Forbearance Approval Notice Letter

An Unemployment Hardship Forbearance Approval Notice Letter confirms your lender has granted a temporary suspension or reduction of monthly payments due to job loss. This official document outlines the specific start and end dates of the relief period. It is vital to understand that while payments pause, interest may still accrue and capitalize. Review the letter carefully to verify any required partial payments or reporting obligations. Always retain this notice for your records to ensure your credit score remains protected during this transitional financial period.

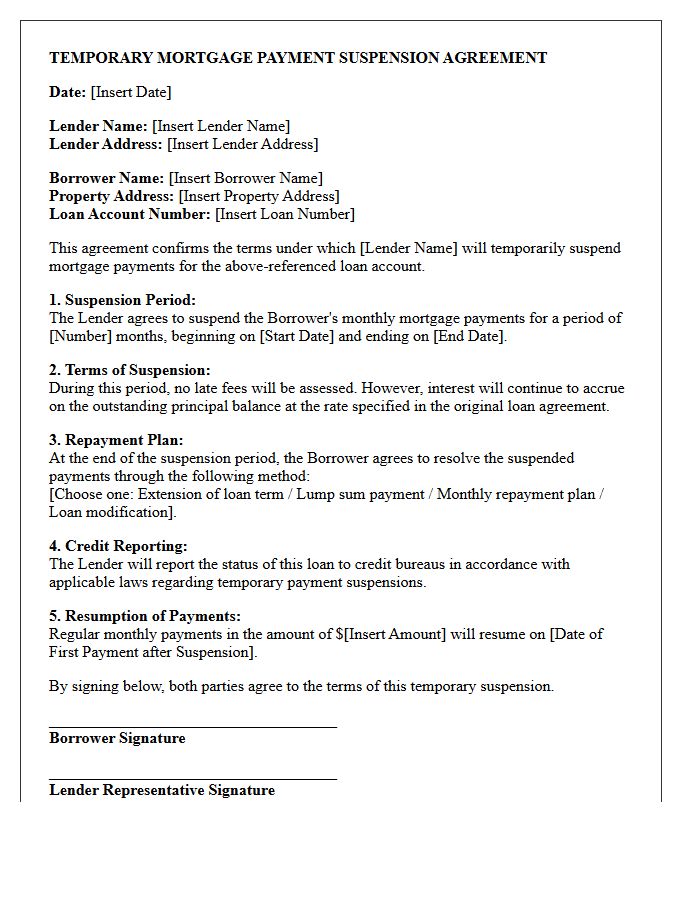

Temporary Mortgage Payment Suspension Agreement Letter

A Temporary Mortgage Payment Suspension Agreement Letter outlines a formal arrangement where a lender permits a borrower to pause or reduce monthly installments due to short-term financial hardship. This document is crucial because it defines the forbearance period, prevents immediate foreclosure actions, and specifies how missed payments must be repaid later. It serves as a legal safeguard, ensuring both parties agree on the terms of relief without permanently altering the original loan contract. Always review the letter to confirm if interest continues to accrue during the suspension period.

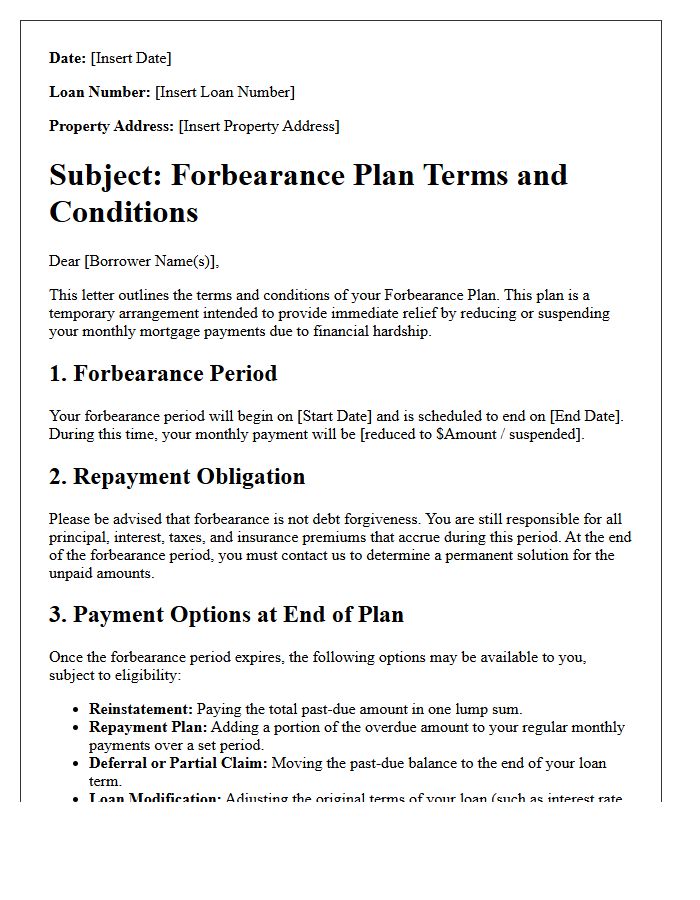

Forbearance Plan Terms and Conditions Letter

A Forbearance Plan Terms and Conditions Letter is a legally binding document outlining the temporary suspension or reduction of mortgage payments. It specifies the repayment structure required once the period ends, including options like deferrals or lump-sum payments. Homeowners must review the effective dates and impact on credit reporting. Signing this agreement confirms your commitment to the reinstatement terms to avoid foreclosure. Always verify if interest accrual continues during the pause to understand the total long-term cost of your debt relief plan.

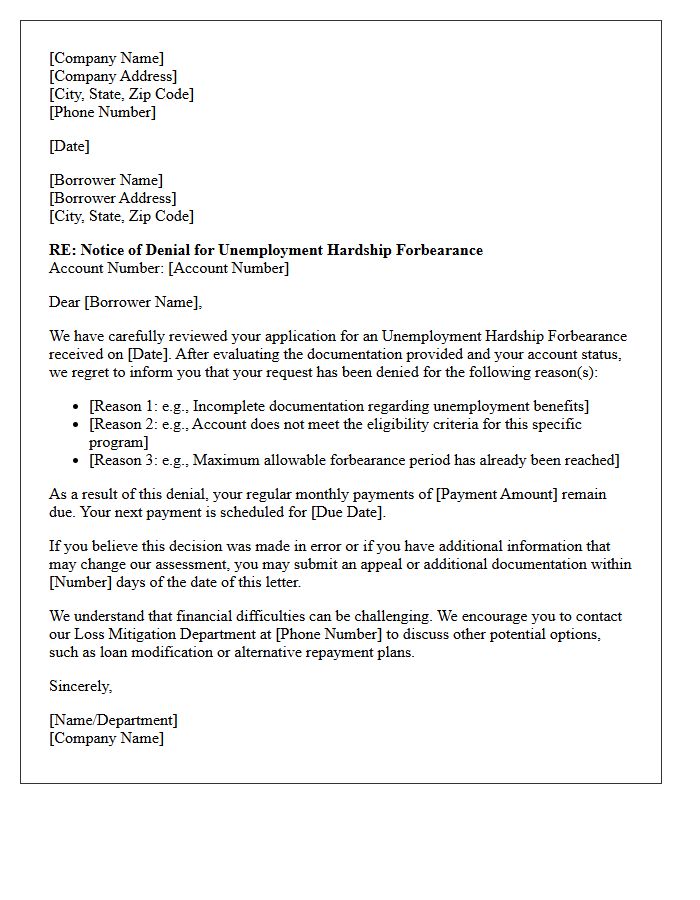

Unemployment Hardship Forbearance Denial Notice Letter

Receiving an Unemployment Hardship Forbearance Denial Notice Letter means your lender has rejected your request to pause or reduce loan payments. This denial often occurs due to missing documentation, failing to meet specific eligibility criteria, or being delinquent beyond the allowed limit. It is critical to review the specific reason provided in the letter immediately. You may have the right to appeal the decision, apply for alternative repayment plans, or seek loan modification to avoid default and protect your credit score during financial instability.

Request for Additional Hardship Evidence Letter

A Request for Additional Hardship Evidence Letter is a formal response to an RFE (Request for Evidence) from immigration or financial authorities. It requires you to provide documented proof of extreme financial, medical, or personal suffering that justifies your claim. To succeed, you must submit specific supporting documentation, such as medical records, bank statements, or expert evaluations, to bridge gaps in your initial application. This letter is critical for verifying claims and ensuring your case meets the legal standards for a hardship waiver or relief program.

Forbearance Period Midpoint Status Update Letter

The Forbearance Period Midpoint Status Update Letter is a critical communication sent to borrowers halfway through their repayment pause. Its primary purpose is to provide a status update regarding the remaining duration of financial relief. This document outlines available repayment options, such as extensions or loan modifications, ensuring borrowers can plan their transition back to regular payments. Reviewing this letter is essential for maintaining financial stability and avoiding unexpected delinquency once the temporary forbearance period concludes. It serves as a vital tool for proactive debt management and long-term fiscal health.

Notice of Approaching Forbearance Expiration Letter

A Notice of Approaching Forbearance Expiration Letter is a critical legal notification sent by your loan servicer. It informs borrowers that their temporary payment relief period is ending soon. This document outlines your repayment options, such as loan modification, deferral, or a repayment plan, to avoid potential default. It is essential to act immediately upon receipt to evaluate your financial situation and contact your lender. Proactive communication ensures you maintain housing stability and transition smoothly back to regular monthly payments before the deadline expires.

Unemployment Hardship Forbearance Extension Request Letter

An Unemployment Hardship Forbearance Extension Request Letter is a formal document sent to lenders to prolong temporary payment relief. When initial assistance ends but your job search continues, this letter must demonstrate your continued financial instability and intent to resume payments. Clearly state your original loan details, current employment status, and provide updated documentation of your situation. Sending this request proactively is essential to protect your credit score and avoid default while navigating prolonged job loss. Always include a specific timeframe for the requested extension to ensure a clear formal agreement.

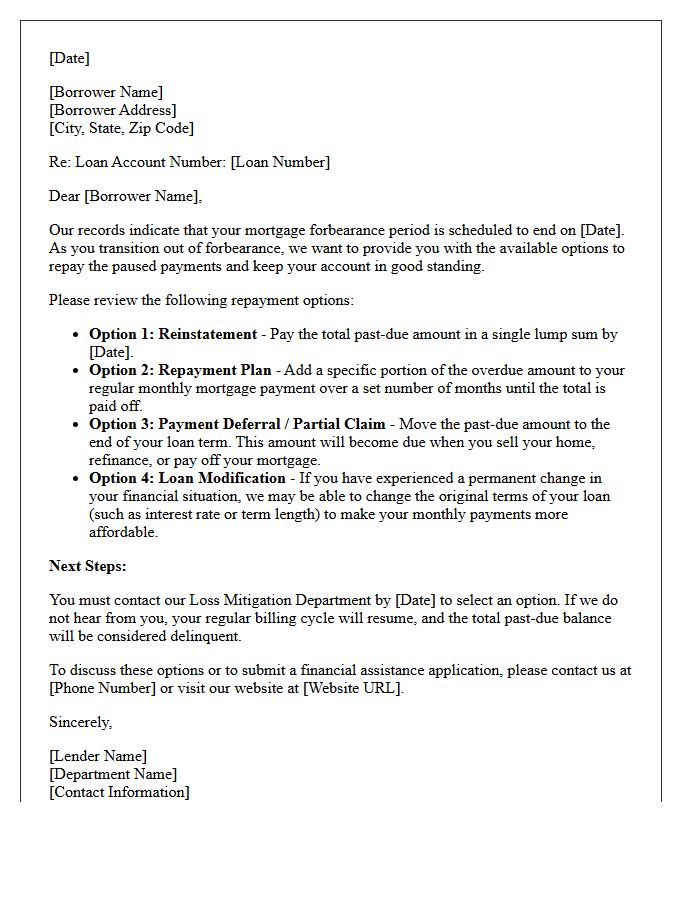

Post-Forbearance Repayment Plan Options Letter

A Post-Forbearance Repayment Plan Options Letter is a critical document from your mortgage servicer outlining reinstatement strategies after a pause in payments. It details specific repayment plan terms, allowing you to catch up on missed installments by adding a portion of the past-due amount to your monthly bill. This formal notice helps borrowers avoid default by establishing a structured timeline to restore loan normalcy. Reviewing this letter promptly ensures you understand your eligibility for loss mitigation and helps maintain your long-term homeownership stability.

What is an Unemployment Hardship Forbearance?

An Unemployment Hardship Forbearance is a temporary agreement that allows borrowers to pause or reduce their monthly loan payments if they have lost their job or experienced a significant involuntary loss of income.

How do I qualify for an Unemployment Hardship Forbearance?

To qualify, you must typically provide proof of eligibility for unemployment benefits or a formal termination notice from your previous employer, and demonstrate that your current financial situation prevents you from meeting your payment obligations.

Will interest continue to accrue during the forbearance period?

Yes, in most cases, interest continues to accrue on the outstanding principal balance during an Unemployment Hardship Forbearance and may be capitalized (added to the loan balance) at the end of the period.

How long does an Unemployment Hardship Forbearance last?

The duration varies by lender but is typically granted in 3 to 6-month increments, with a maximum lifetime limit often capped at 12 to 36 months depending on the specific loan type and servicer policies.

How does entering forbearance affect my credit score?

While the forbearance itself may be noted on your credit report, it is generally less damaging than missing payments; however, it may impact your ability to refinance or take out new loans until the account returns to regular repayment status.

Comments