Receiving a Loan Modification Denial Notice can be stressful, but it is not the final word on your home's future. Understanding the specific reason for rejection is crucial for filing a successful appeal or exploring alternative foreclosure prevention options. Regain control of your mortgage situation by taking immediate action. To help you respond effectively, below are some ready to use template.

Image cover: Navigating Your Loan Modification Denial: Letter Samples and Response Templates

Letter Samples List

- Insufficient Income Loan Modification Denial Letter

- Incomplete Documentation Loan Modification Denial Letter

- Negative Net Present Value Loan Modification Denial Letter

- Maximum Allowable Modifications Reached Denial Letter

- Failure To Complete Trial Period Loan Modification Denial Letter

- Non-Owner Occupied Property Loan Modification Denial Letter

- Investor Guidelines Unmet Loan Modification Denial Letter

- Ineligible Mortgage Type Loan Modification Denial Letter

- Lack Of Verifiable Financial Hardship Loan Modification Denial Letter

- Excessive Debt To Income Ratio Loan Modification Denial Letter

- Unverified Employment Loan Modification Denial Letter

- Voluntary Application Withdrawal Loan Modification Denial Letter

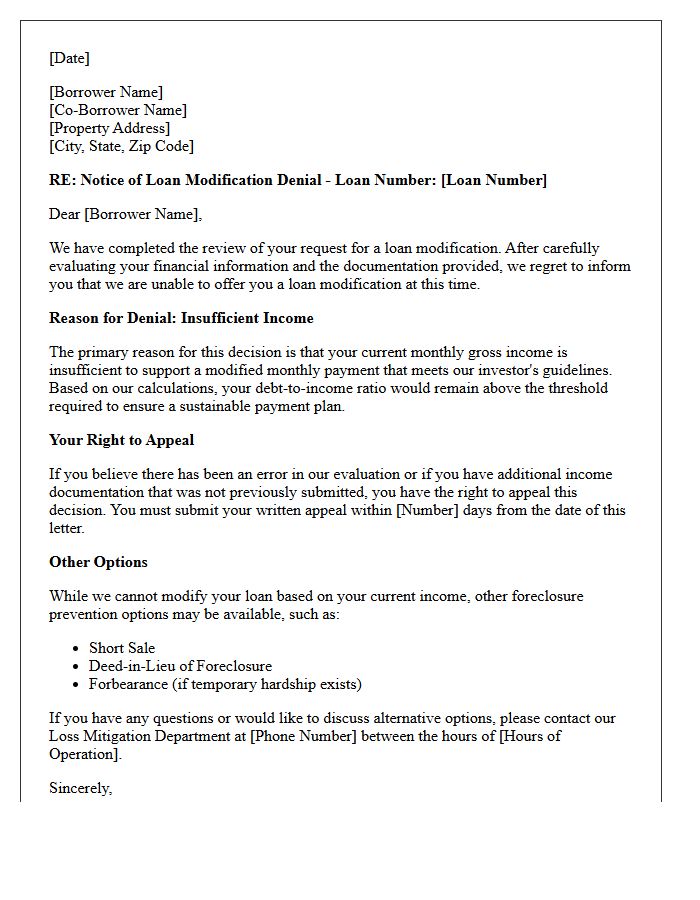

Insufficient Income Loan Modification Denial Letter

An Insufficient Income Loan Modification Denial Letter indicates that your financial documentation does not demonstrate enough stable cash flow to support even a reduced mortgage payment. Lenders use a debt-to-income ratio to evaluate eligibility; if your earnings are too low, they deem the modification unsustainable. To contest this, you should immediately review your financial statement for errors or omitted income sources, such as rental dividends or part-time wages. You have a limited appeals window to submit additional proof of income or explore alternatives like a deed-in-lieu or short sale to avoid foreclosure.

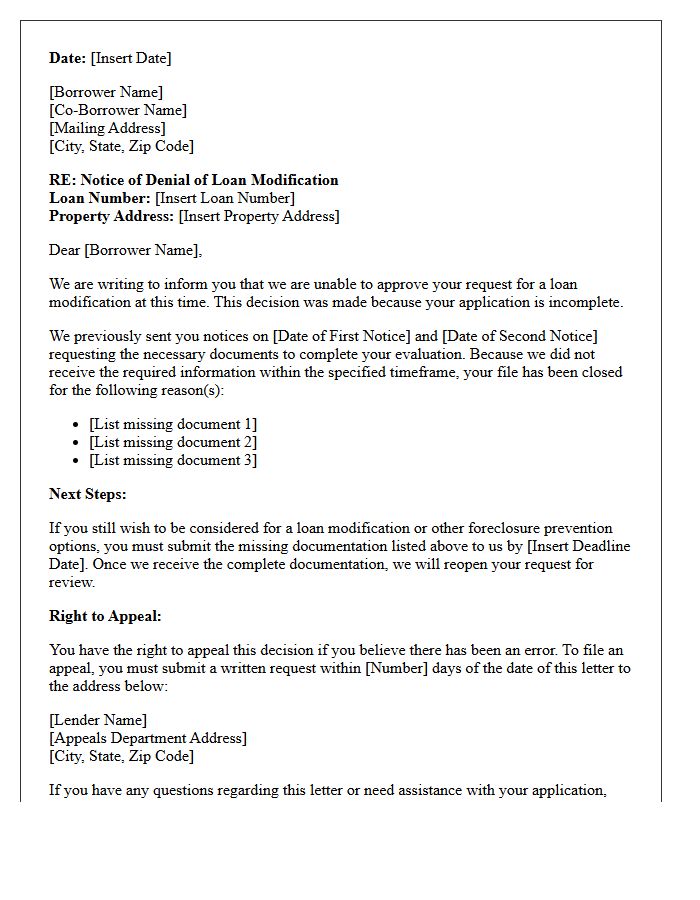

Incomplete Documentation Loan Modification Denial Letter

Receiving an Incomplete Documentation Loan Modification Denial Letter means the lender halted your application because specific financial records were missing or outdated. This is a procedural denial rather than a final rejection based on eligibility. To protect your home, you must act quickly to submit the requested tax returns, pay stubs, or bank statements within the specified appeal deadline. Carefully review the checklist provided in the letter to identify exactly what is missing, as providing a complete package is the only way to restart the loan workout process and avoid foreclosure.

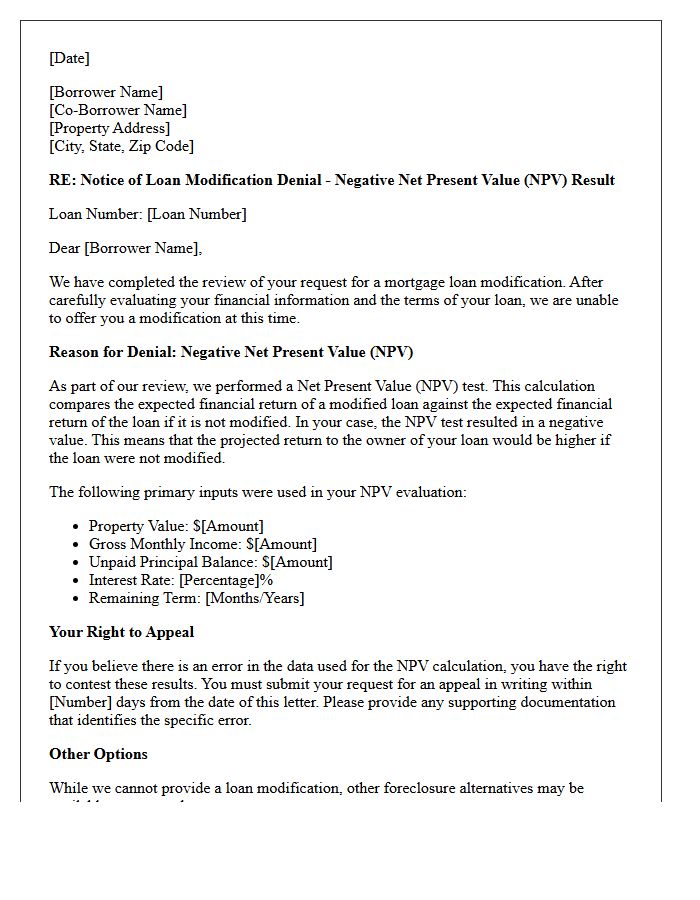

Negative Net Present Value Loan Modification Denial Letter

Receiving a Negative Net Present Value (NPV) denial letter means your loan modification was rejected because the investor would lose more money by modifying your mortgage than by proceeding with foreclosure. This calculation compares the expected cash flow of a modified loan against the recovery value of the property. It is crucial to review the input data, such as your income, property value, and credit score, for errors. Borrowers have a 30-day window to appeal the decision by proving that the financial data used in the NPV test was inaccurate.

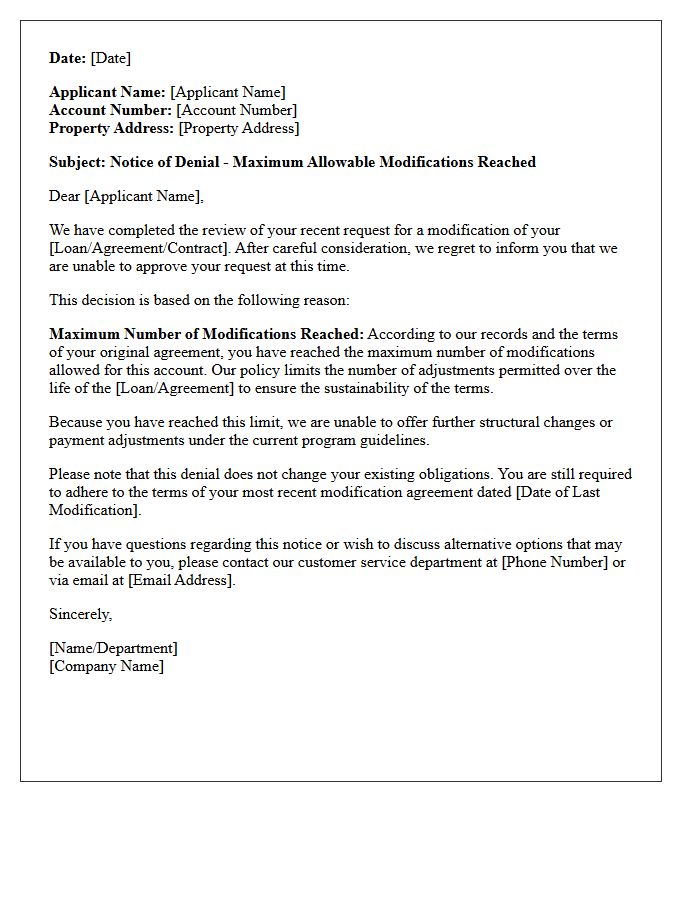

Maximum Allowable Modifications Reached Denial Letter

A Maximum Allowable Modifications Reached Denial Letter is a formal notice from a mortgage servicer stating your loan no longer qualifies for loss mitigation programs. This happens when you have reached the lifetime limit for restructuring your debt. Since you can no longer modify the terms to lower payments, you must explore alternatives like a short sale, deed-in-lieu, or repayment plan. Receiving this denial is critical because it often signals the final step before the lender proceeds with foreclosure actions against the property.

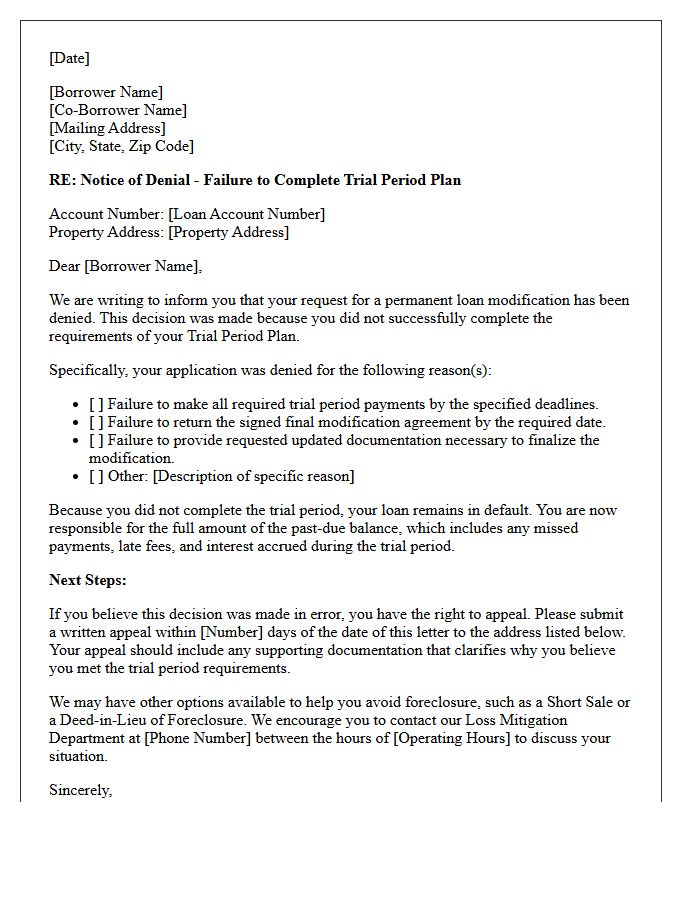

Failure To Complete Trial Period Loan Modification Denial Letter

Receiving a Failure to Complete Trial Period Plan notice means your permanent loan modification was denied because the servicer claims you missed payments or breached agreement terms. This denial letter is critical because it triggers the end of foreclosure protection. You must immediately review your payment records for errors and submit a written appeal within the required 30-day window. If the servicer made a mistake, providing proof of timely payments can reverse the decision and secure your permanent modification to keep your home.

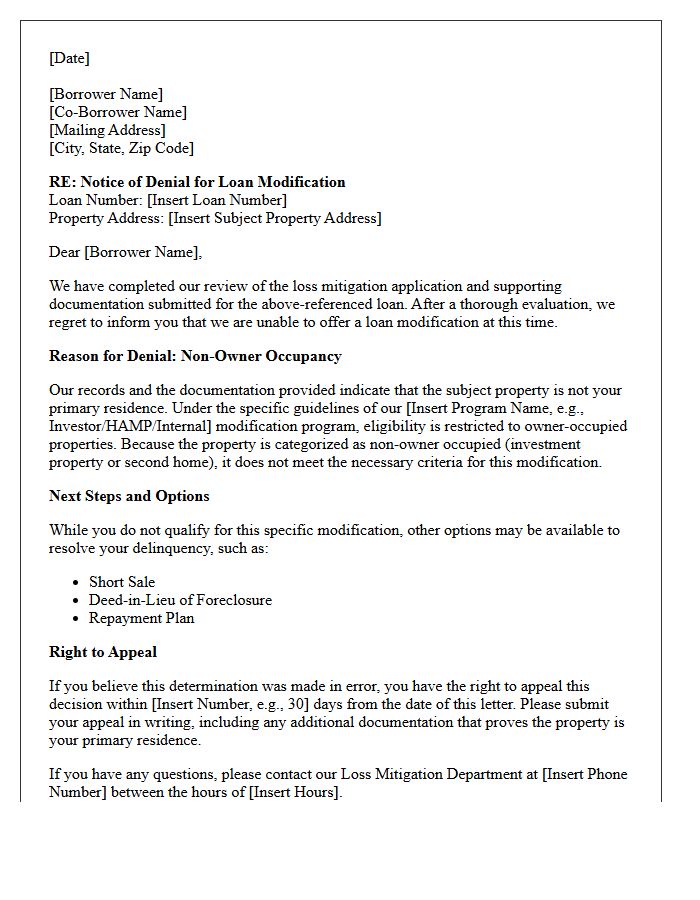

Non-Owner Occupied Property Loan Modification Denial Letter

A Non-Owner Occupied Property Loan Modification Denial Letter formally notifies a borrower that their request to restructure a mortgage on an investment property has been rejected. Lenders often prioritize primary residences, making eligibility criteria for rentals much stricter. Common reasons for denial include insufficient debt-to-income ratios, negative net present value (NPV) results, or missing documentation. Understanding the specific reason cited is crucial for filing an appeal or exploring alternative loss mitigation options, such as a short sale or deed-in-lieu, to avoid potential foreclosure proceedings on the asset.

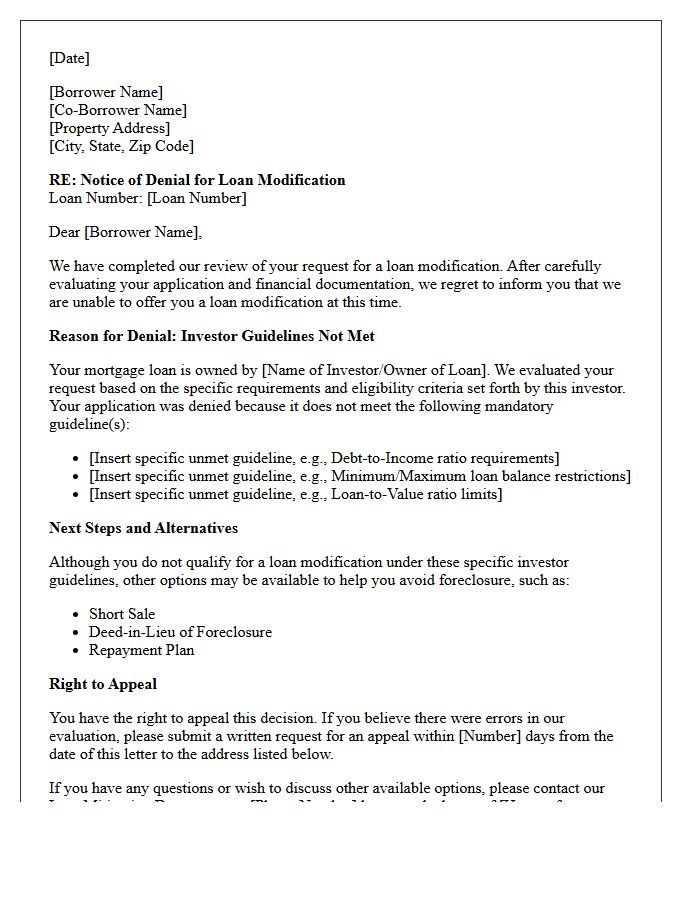

Investor Guidelines Unmet Loan Modification Denial Letter

An Investor Guidelines Unmet denial letter means your mortgage servicer cannot approve a loan modification because your application failed to satisfy specific criteria set by the loan's owner. These requirements often involve strict debt-to-income ratios, minimum credit scores, or specific net present value results. Since the servicer must follow these contractual mandates, they lack the authority to grant exceptions. If you receive this notice, review the listed requirements immediately to identify discrepancies, as you may need to appeal the decision or explore alternative options like short sales or deeds-in-lieu.

Ineligible Mortgage Type Loan Modification Denial Letter

Receiving an ineligible mortgage type denial letter means your specific loan structure does not qualify for traditional modification programs. This often occurs with private investors, portfolio loans, or non-conforming products that lack government backing like FHA or Fannie Mae. To contest this, review your original loan documents to verify your loan classification. Since some lenders offer internal proprietary modifications, you should immediately request an alternative loss mitigation review or explore options like a short sale or deed-in-lieu to avoid foreclosure proceedings.

Lack Of Verifiable Financial Hardship Loan Modification Denial Letter

Receiving a Lack of Verifiable Financial Hardship denial letter means your mortgage servicer determined your current income or expenses do not justify a loan modification. To overturn this decision, you must provide documented evidence of a legitimate financial crisis, such as job loss, medical bills, or divorce. Lenders require specific proof that your situation is involuntary and persistent. If your application was rejected, immediately request a detailed appeal and submit updated pay stubs, bank statements, or tax returns to verify your inability to maintain standard monthly payments.

Excessive Debt To Income Ratio Loan Modification Denial Letter

Receiving an Excessive Debt To Income Ratio loan modification denial means your monthly obligations remain too high relative to your gross income, even with adjusted terms. Lenders use the DTI ratio to determine if a borrower can realistically sustain modified payments. To overturn this decision, you should document additional income sources or pay down existing balances. Review your denial letter immediately to verify the financial data used, as correcting reporting errors or providing updated proof of income are common ways to appeal and secure an approval.

Unverified Employment Loan Modification Denial Letter

An Unverified Employment Loan Modification Denial Letter indicates your lender could not confirm your current income or job status. This rejection often occurs due to outdated paystubs, unresponsive employers, or discrepancies in tax documentation. To resolve this, you must quickly provide valid proof of income, such as recent W-2s or bank statements, to file an appeal. Failure to verify employment prevents the servicer from calculating your debt-to-income ratio, which is essential for determining eligibility for a loan workout plan and avoiding potential foreclosure actions.

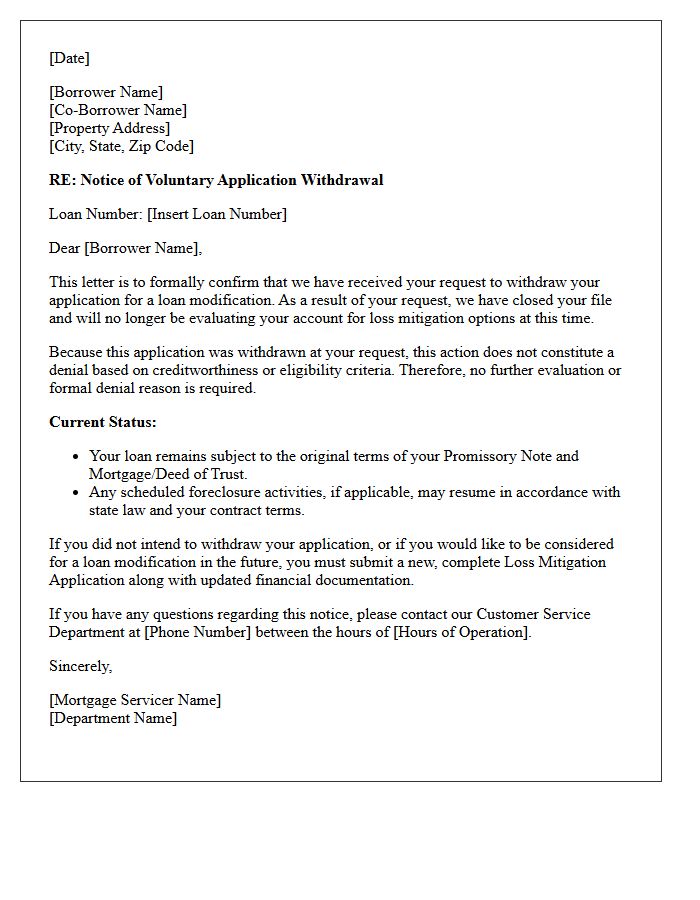

Voluntary Application Withdrawal Loan Modification Denial Letter

A voluntary application withdrawal occurs when a borrower chooses to stop the loan modification process before a final decision is reached. Receiving a denial letter for this reason means the lender closed your file because you requested its removal or failed to provide required documentation by the deadline. It is crucial to understand that this is not a credit-based rejection. To resume, you must often submit a new application or reapply with updated financial records to demonstrate your current eligibility for foreclosure prevention options.

What should I do first after receiving a Loan Modification Denial Notice?

Read the entire denial letter carefully to identify the specific reason for the decision. You typically have 30 days from the date of the notice to file an appeal or request a meeting with your loan servicer to contest the findings.

What are the most common reasons for a loan modification denial?

Common reasons include incomplete documentation, failure to meet the "Net Present Value" (NPV) test, an unsustainable debt-to-income ratio, or the lender determining that your financial hardship is not documented sufficiently to qualify for their specific programs.

Can I appeal a loan modification denial from my mortgage servicer?

Yes, most federal guidelines and bank policies allow for an administrative appeal. You must submit a formal written request providing new evidence or pointing out specific errors in the lender's initial calculation, such as incorrect income data or property valuation.

How does a "Net Present Value" (NPV) failure affect my denial?

An NPV failure means the lender's mathematical model determined that foreclosing on the home would be more profitable for the investor than modifying the loan. You can challenge this by verifying if the servicer used accurate data regarding your income, taxes, and the current market value of your home.

What are my alternatives if my loan modification appeal is rejected?

If your appeal is denied, you can explore other loss mitigation options such as a short sale, a deed-in-lieu of foreclosure, or a Chapter 13 bankruptcy filing, which may allow you to cure the default through a court-ordered repayment plan.

Comments