Homeowners facing financial hardship must understand the FHA Pre-Foreclosure Notice of Default. This formal notification marks the initial legal step in the recovery process, issued when mortgage payments are delinquent. Understanding your rights and timeline is essential to avoiding property loss and protecting your credit score. To help you respond effectively, below are some ready to use template options.

Image cover: Navigating FHA Pre-Foreclosure: Essential Notice of Default Templates and Samples

Letter Samples List

- Federal Housing Administration Pre-Foreclosure Notice of Default Letter

- Initial Federal Housing Administration Mortgage Default Warning Letter

- Federal Housing Administration Home Retention Options Information Letter

- Notice of Intent to Foreclose Federal Housing Administration Mortgage Letter

- Federal Housing Administration Loss Mitigation Application Request Letter

- Federal Housing Administration Pre-Foreclosure Sale Approval Letter

- Federal Housing Administration Special Forbearance Agreement Letter

- Federal Housing Administration Partial Claim Promissory Note Letter

- Federal Housing Administration Loan Modification Offer Letter

- Notice of Federal Housing Administration Default Counseling Requirement Letter

- Federal Housing Administration Deed in Lieu of Foreclosure Offer Letter

- Final Federal Housing Administration Pre-Foreclosure Warning Letter

- Federal Housing Administration Default Resolution Confirmation Letter

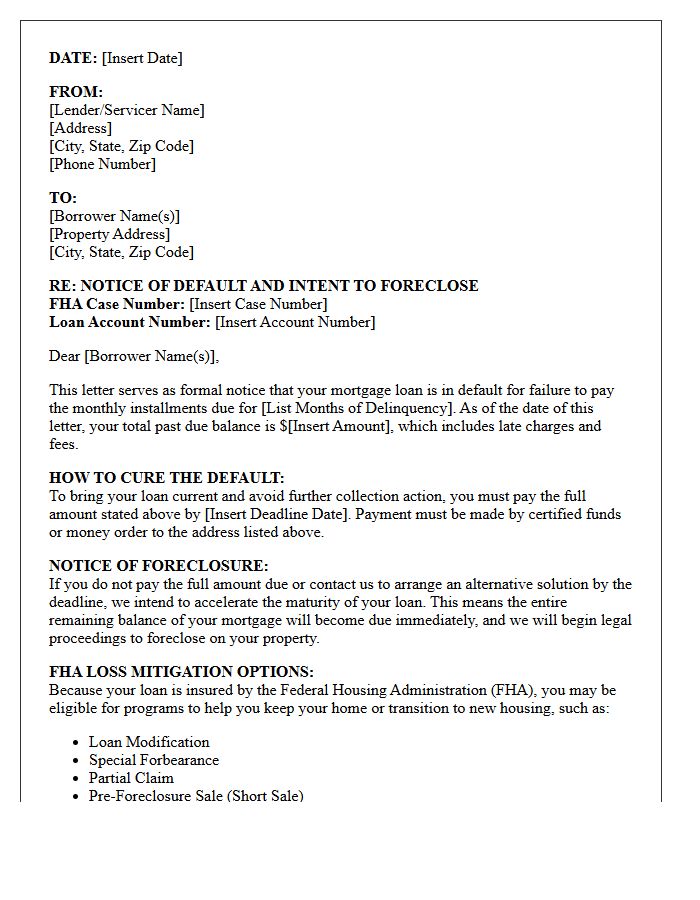

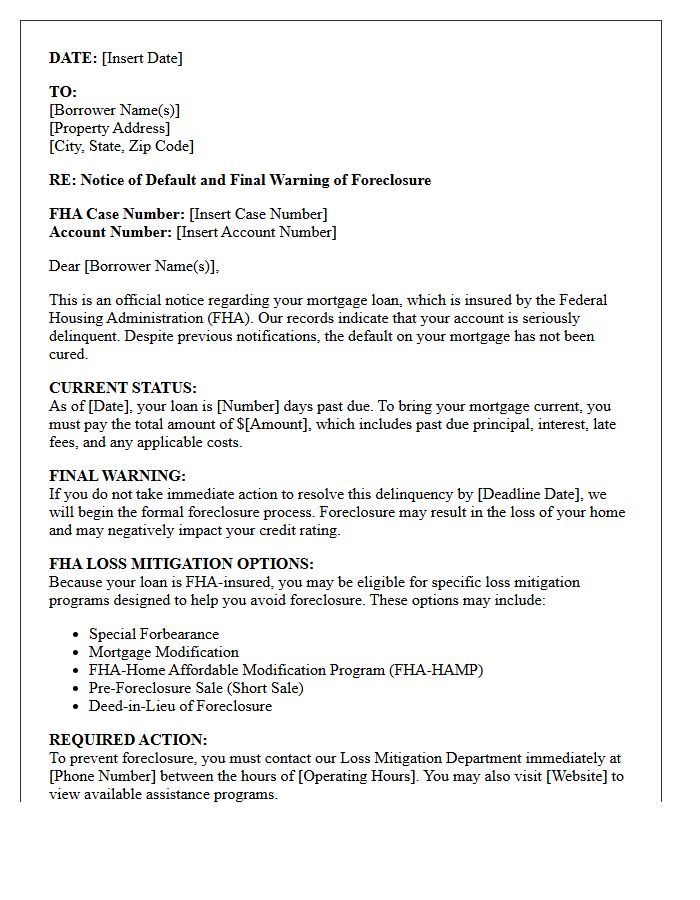

Federal Housing Administration Pre-Foreclosure Notice of Default Letter

The Federal Housing Administration (FHA) Pre-Foreclosure Notice of Default Letter is a critical legal document sent to borrowers who fall behind on mortgage payments. This notice serves as a formal warning that the lender intends to begin foreclosure proceedings unless the debt is resolved. Importantly, FHA guidelines require lenders to offer loss mitigation options, such as loan modifications or repayment plans, before seizing the property. Homeowners should act immediately upon receipt to explore reinstatement programs designed to prevent the loss of their home and protect their credit standing.

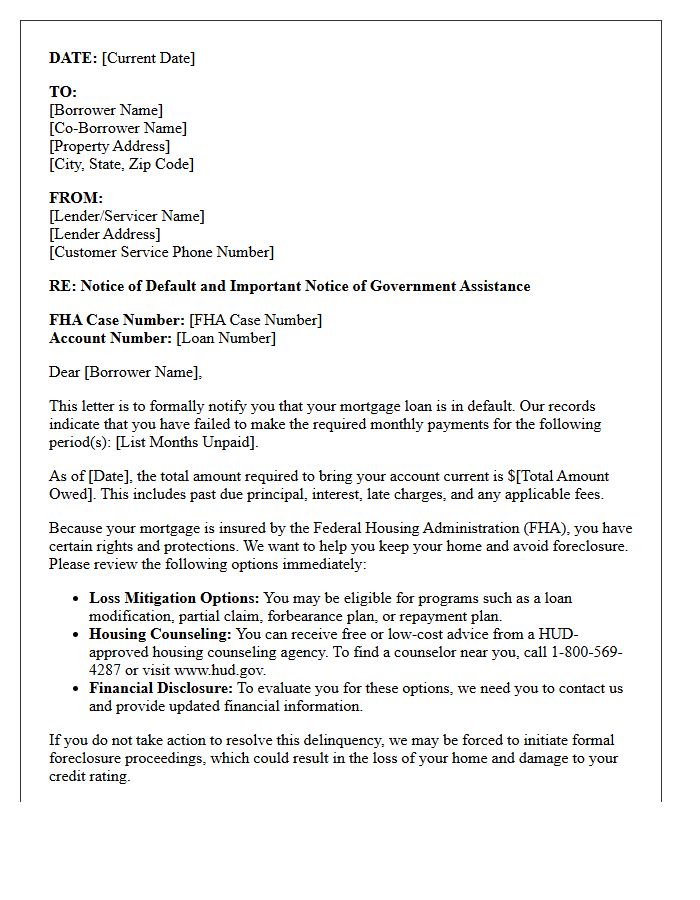

Initial Federal Housing Administration Mortgage Default Warning Letter

Receiving an Initial Federal Housing Administration Mortgage Default Warning Letter is a critical notification that your loan is delinquent. This formal document outlines that you have missed payments and are at risk of foreclosure. It serves as a legal requirement for lenders to inform borrowers of their rights and available assistance. To protect your home, you must contact your loan servicer immediately to discuss loss mitigation options, such as loan modification or forbearance. Taking prompt action is the most effective way to resolve the default and maintain your FHA-insured mortgage standing.

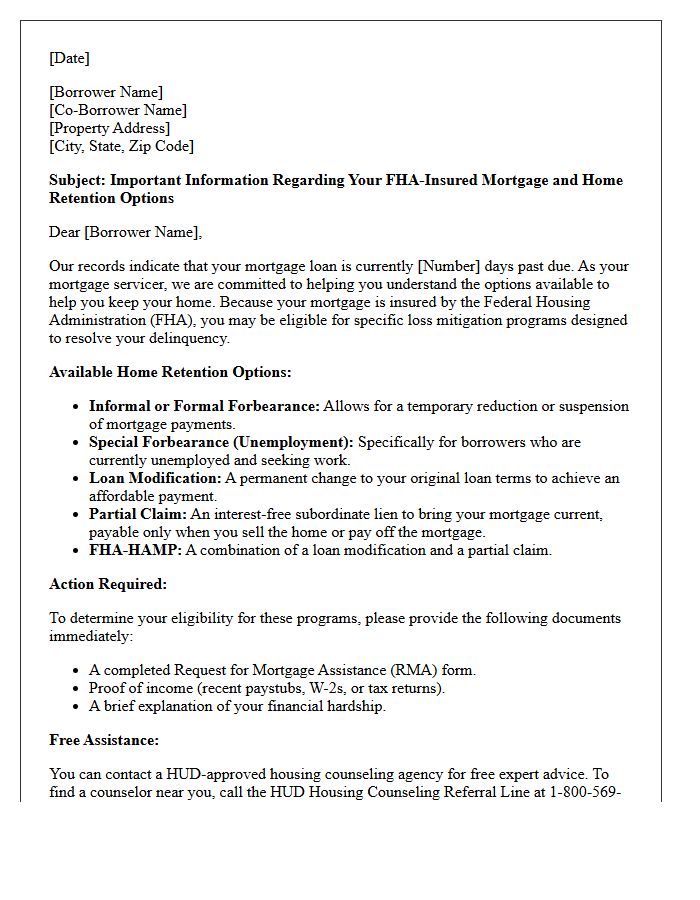

Federal Housing Administration Home Retention Options Information Letter

The FHA Home Retention Options Information Letter is a mandatory disclosure sent to struggling borrowers to prevent foreclosure. This critical document outlines available loss mitigation strategies, such as loan modifications, forbearance plans, and repayment options. It serves as a formal guide to help homeowners understand their rights and the specific steps required to achieve mortgage reinstatement. Homeowners should review this letter immediately to explore federally backed solutions designed to keep their housing secure during financial hardship.

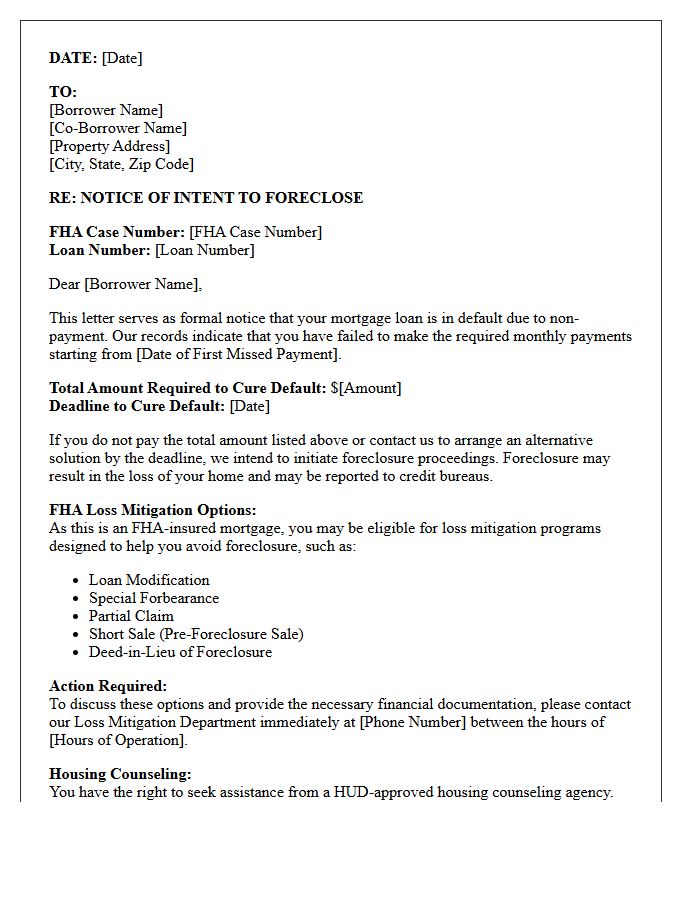

Notice of Intent to Foreclose Federal Housing Administration Mortgage Letter

A Notice of Intent to Foreclose is a formal legal warning sent to borrowers who are significantly delinquent on their Federal Housing Administration (FHA) mortgage payments. This document serves as the final step before the lender initiates official foreclosure proceedings. It outlines the specific amount needed to cure the default and provides a deadline for payment. Borrowers should immediately explore loss mitigation options, such as loan modifications or partial claims, which are unique protections offered by the FHA to help homeowners avoid losing their property during financial hardship.

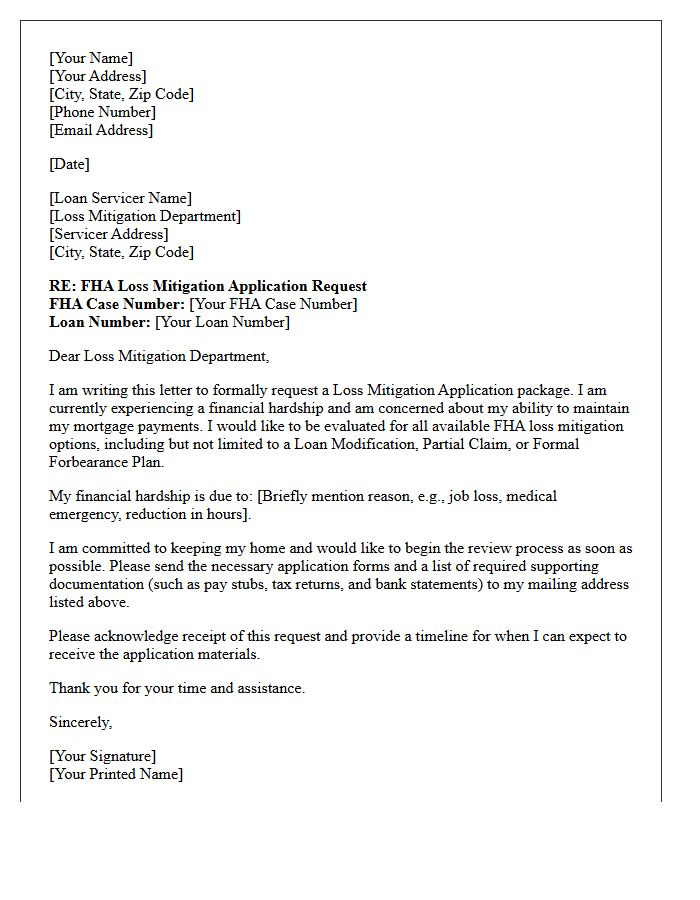

Federal Housing Administration Loss Mitigation Application Request Letter

A Federal Housing Administration (FHA) Loss Mitigation Application Request Letter is a formal document sent to your mortgage servicer to seek foreclosure alternatives. This letter initiates the review process for relief options, such as a loan modification, partial claim, or forbearance plan. To be effective, it must clearly explain your financial hardship and include updated documentation of income and expenses. Submitting this request is the critical first step in demonstrating a good faith effort to resolve delinquency and stabilize your housing situation under FHA loss mitigation guidelines.

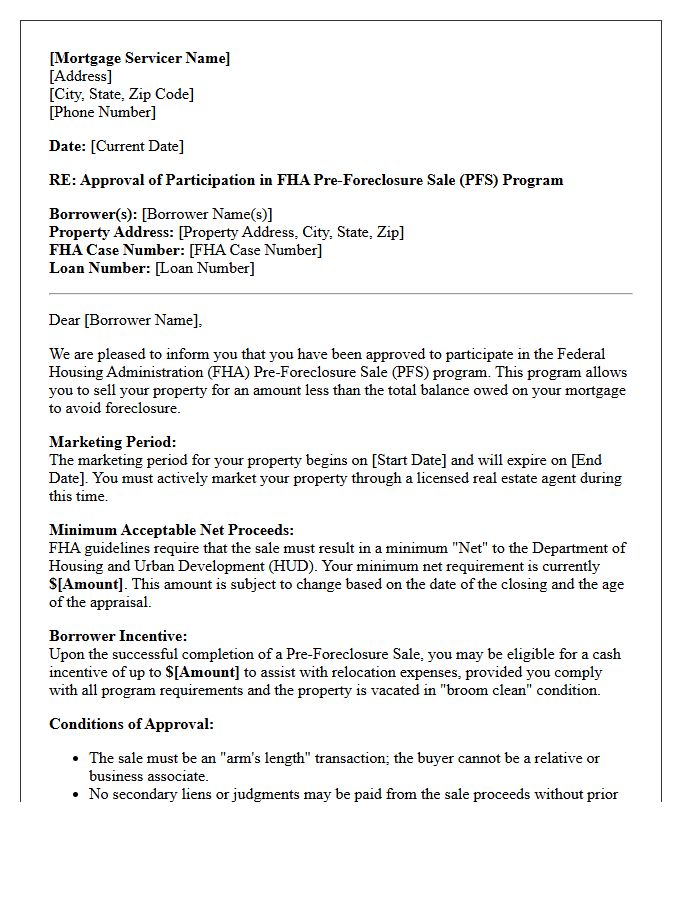

Federal Housing Administration Pre-Foreclosure Sale Approval Letter

A Federal Housing Administration (FHA) Pre-Foreclosure Sale Approval Letter is a formal document authorizing a short sale. This letter confirms that the Department of Housing and Urban Development (HUD) has reviewed the homeowner's financial hardship and approved the sale of the property for less than the remaining mortgage balance. It outlines the specific minimum net proceeds the lender will accept and establishes a strict expiration date for the transaction. Receiving this letter is a critical step for distressed borrowers to avoid formal foreclosure and mitigate damage to their credit scores.

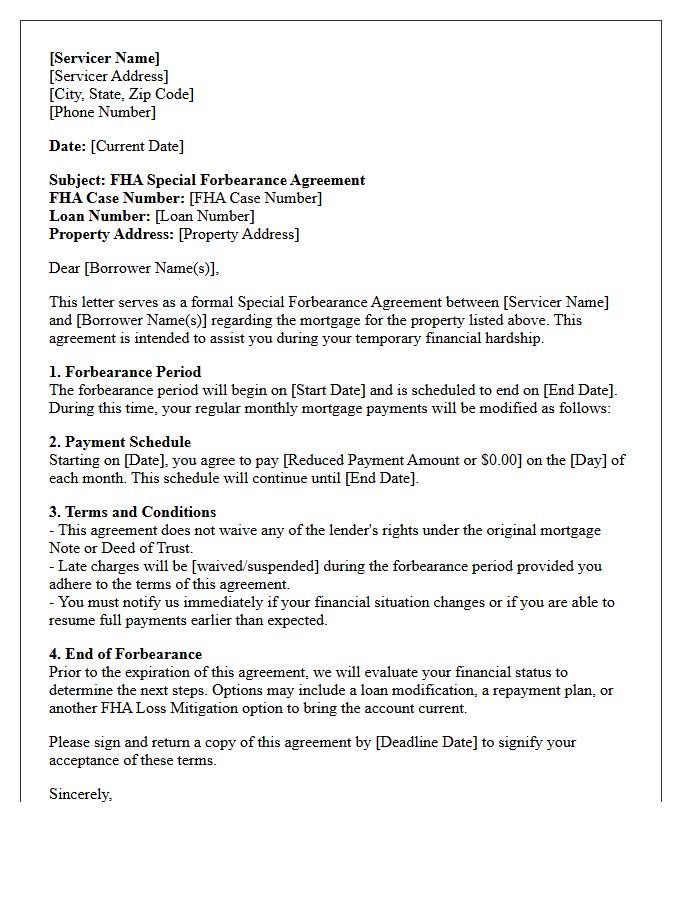

Federal Housing Administration Special Forbearance Agreement Letter

A Federal Housing Administration (FHA) Special Forbearance Agreement is a formal relief option designed for borrowers facing financial hardship, particularly unemployment. This written letter outlines a temporary arrangement where the servicer reduces or suspends mortgage payments for a specific period. It is crucial to understand that this is not a permanent loan modification; rather, it provides a grace period to regain financial stability. Homeowners must stay in contact with their mortgage servicer to finalize a long-term repayment plan once the forbearance period ends to avoid potential foreclosure actions.

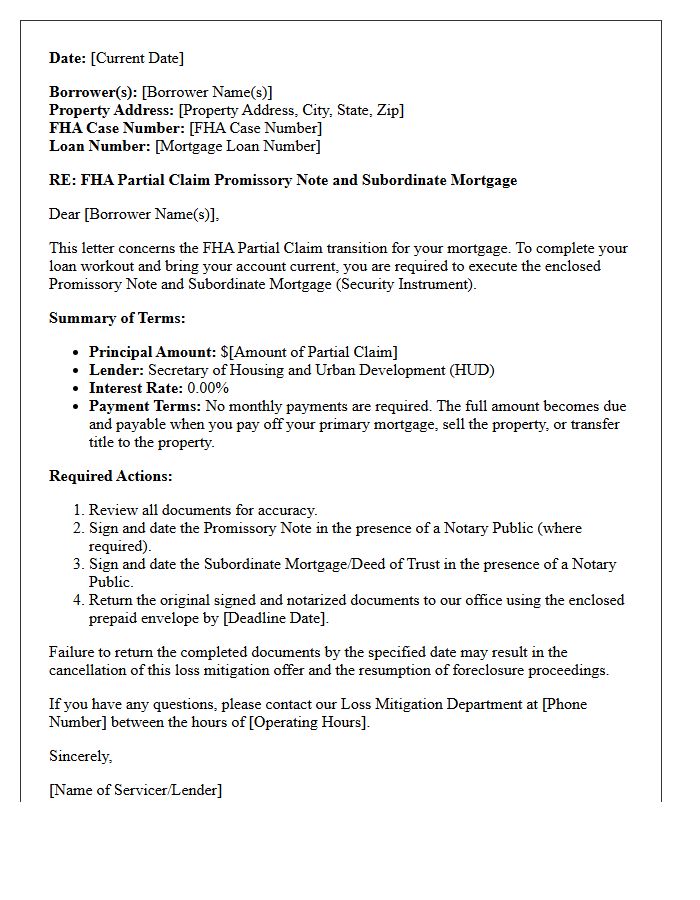

Federal Housing Administration Partial Claim Promissory Note Letter

The FHA Partial Claim is a zero-interest subordinate lien used to resolve mortgage delinquencies. When a homeowner falls behind, the Department of Housing and Urban Development pays the past-due amount to the lender on their behalf. In exchange, the borrower signs a Promissory Note, agreeing to repay this interest-free loan only when the property is sold, the mortgage is refinanced, or the primary loan reaches maturity. It is a critical loss mitigation tool designed to prevent foreclosure and allow homeowners to resume regular monthly payments without an immediate lump-sum requirement.

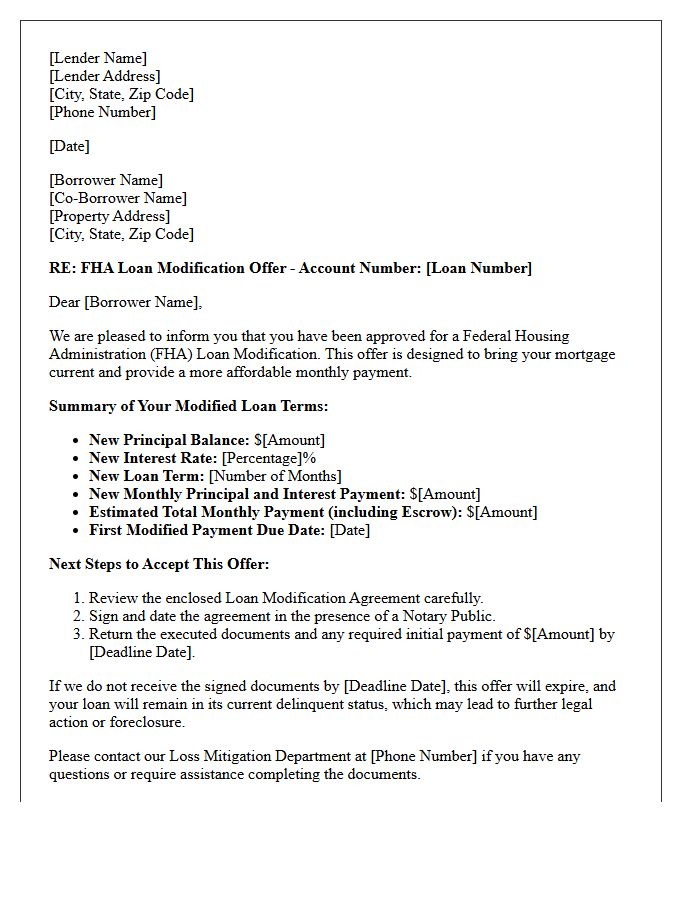

Federal Housing Administration Loan Modification Offer Letter

A Federal Housing Administration (FHA) loan modification offer letter is a formal proposal to permanently restructure your mortgage terms to prevent foreclosure. This document typically outlines a new, lower monthly payment, an extended loan term, or a reduced interest rate. It is crucial to review the trial period plan requirements and specific deadlines mentioned. Once you successfully complete the trial payments and sign the final modification agreement, your loan is considered reinstated. Always verify the sender to avoid scams and ensure the offer aligns with official HUD guidelines for financial recovery.

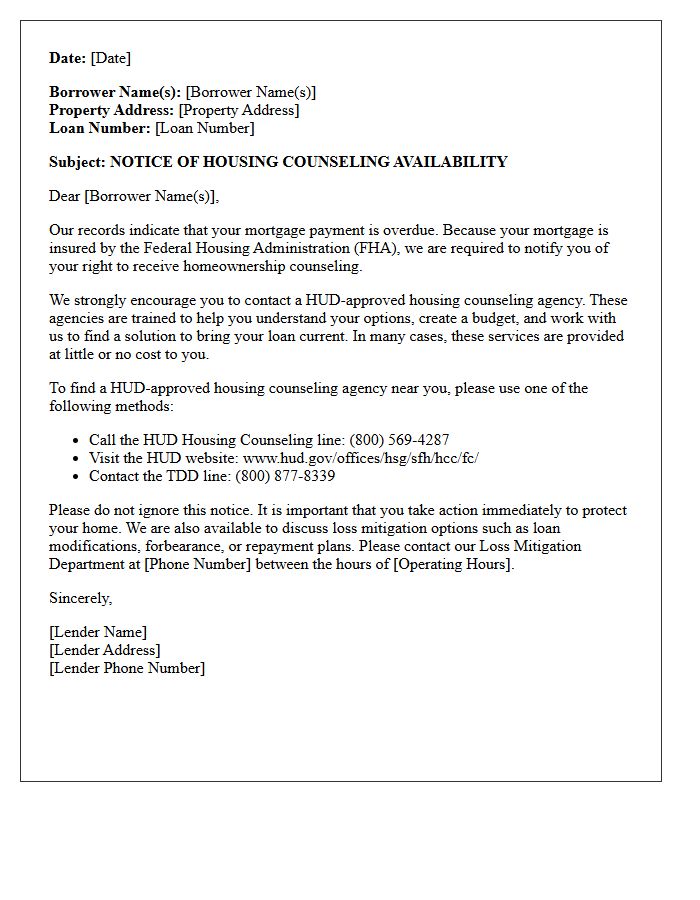

Notice of Federal Housing Administration Default Counseling Requirement Letter

Receiving a Notice of Federal Housing Administration Default Counseling Requirement Letter means your FHA-insured mortgage is delinquent. This mandatory document informs homeowners of their right to access free foreclosure avoidance counseling. To protect your home, you must contact a HUD-approved agency immediately. These counselors provide professional guidance to help you navigate repayment plans or loan modifications. Ignoring this notice accelerates the legal process, so taking proactive communication with your servicer and a counselor is the most critical step to preventing a permanent loss of your property.

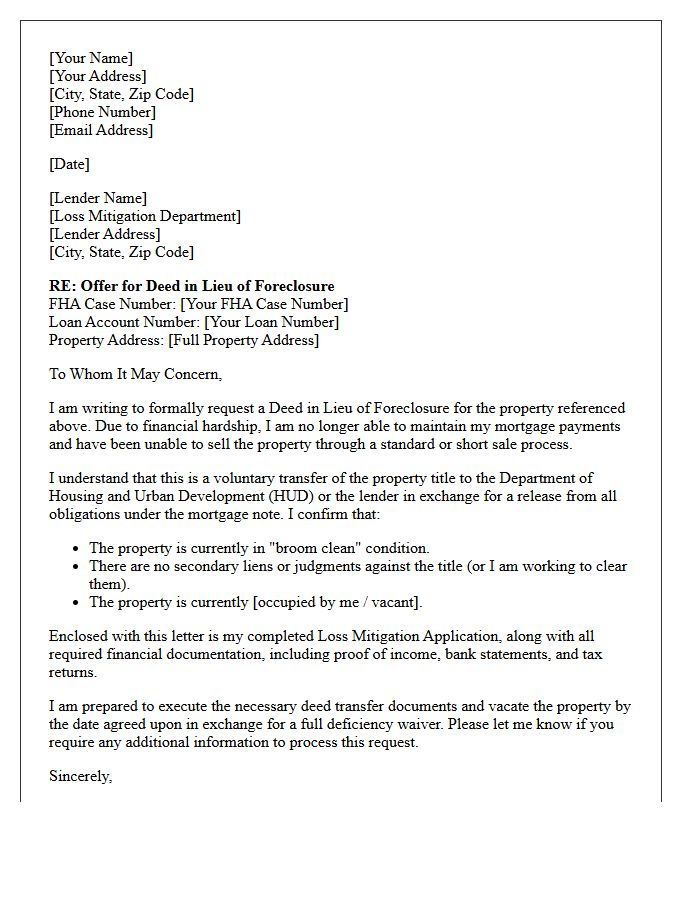

Federal Housing Administration Deed in Lieu of Foreclosure Offer Letter

A Federal Housing Administration (FHA) Deed in Lieu of Foreclosure Offer Letter is a formal proposal allowing homeowners to voluntarily transfer property ownership to the lender to avoid legal proceedings. This loss mitigation strategy helps borrowers satisfy their mortgage debt when a loan modification or short sale is not feasible. To qualify, you must demonstrate financial hardship and meet specific HUD requirements. If accepted, this process can minimize credit damage compared to a standard foreclosure and may include financial assistance to help the occupant transition to new housing.

Final Federal Housing Administration Pre-Foreclosure Warning Letter

The Final FHA Pre-Foreclosure Warning Letter is a critical formal notice sent to borrowers who are at least 60 days delinquent on their mortgage. This document serves as a final notification before the servicer initiates legal foreclosure proceedings. It outlines specific loss mitigation options, such as loan modifications or repayment plans, to help homeowners retain their property. Receiving this letter indicates that immediate action is required to avoid losing the home. Borrowers should contact their lender or a HUD-approved counselor instantly to discuss foreclosure alternatives and resolve the default status.

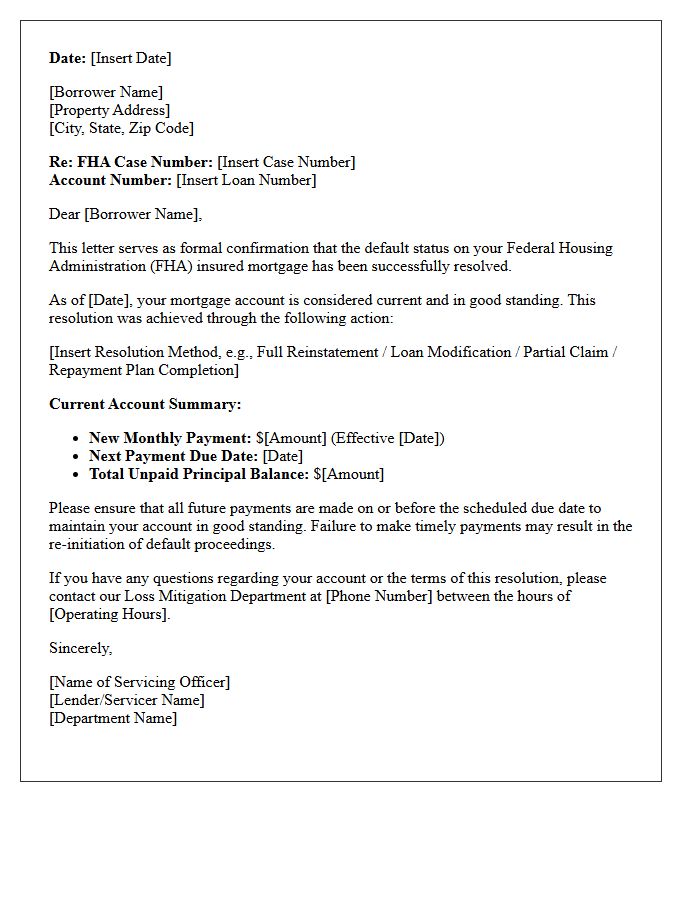

Federal Housing Administration Default Resolution Confirmation Letter

An FHA Default Resolution Confirmation Letter is an official document verifying that a homeowner has successfully resolved a mortgage delinquency. This letter confirms the completion of a loss mitigation intervention, such as a loan modification or repayment plan. It serves as essential proof that the default status has been cleared, restoring the loan to good standing. Borrowers should retain this document to protect their credit reputation and ensure the Department of Housing and Urban Development records accurately reflect the account's current resolution and updated payment terms.

What is an FHA Pre-Foreclosure Notice of Default?

An FHA Pre-Foreclosure Notice of Default is a formal legal notification sent by a mortgage servicer to a borrower who has fallen behind on their FHA-insured loan payments. It serves as an official warning that the lender intends to begin the foreclosure process unless the delinquency is resolved within a specific timeframe.

What should I do if I receive a Notice of Default on my FHA loan?

Upon receiving the notice, you should immediately contact your mortgage servicer to discuss loss mitigation options. Because FHA loans are government-insured, lenders are required to explore alternatives such as loan modifications, partial claims, or special forbearance plans before proceeding with a foreclosure sale.

How many missed payments trigger an FHA Pre-Foreclosure Notice?

Under HUD guidelines, a lender typically issues a Notice of Default after a borrower has missed at least three monthly payments (90 days delinquent). However, federal law generally prohibits a servicer from making the first official judicial or non-judicial foreclosure filing until the borrower is more than 120 days delinquent.

Can I stop a foreclosure after receiving an FHA Notice of Default?

Yes, you can stop the process by "curing" the default, which involves paying the total past-due amount plus late fees. If you cannot afford a lump sum, you may qualify for FHA-specific programs like the Home Affordable Modification Program (HAMP) or a Pre-Foreclosure Sale (Short Sale) to avoid a final foreclosure judgment.

Does an FHA Notice of Default affect my credit score?

Yes, receiving a Notice of Default significantly impacts your credit score because it indicates a serious delinquency and the initiation of public legal proceedings. While the notice itself is a major derogatory mark, completing a loan workout or modification can help prevent the even greater long-term damage of a completed foreclosure sale.

Comments