Receiving a Notice of Default after the death of a primary borrower is a critical legal challenge for heirs and co-signers. This formal warning indicates that mortgage payments have ceased, potentially leading to foreclosure. Understanding your rights and communication obligations with lenders is essential to protecting the property estate. To assist your response, below are some ready to use template.

Image cover: Managing Mortgage Default Following the Death of a Borrower: Essential Templates and Legal Notices

Letter Samples List

- Primary Borrower Death Notification Letter

- Notice of Default Due to Death Letter

- Estate Representative Verification Letter

- Deceased Borrower Account Status Letter

- Successor in Interest Information Letter

- Mortgage Debt Acceleration Warning Letter

- Right to Cure Mortgage Default Letter

- Assumption of Mortgage Eligibility Letter

- Foreclosure Intent and Counseling Letter

- Outstanding Loan Balance Statement Letter

- Probate Court Documentation Request Letter

- Surviving Spouse Assumption Options Letter

- Notice of Foreclosure Proceedings Letter

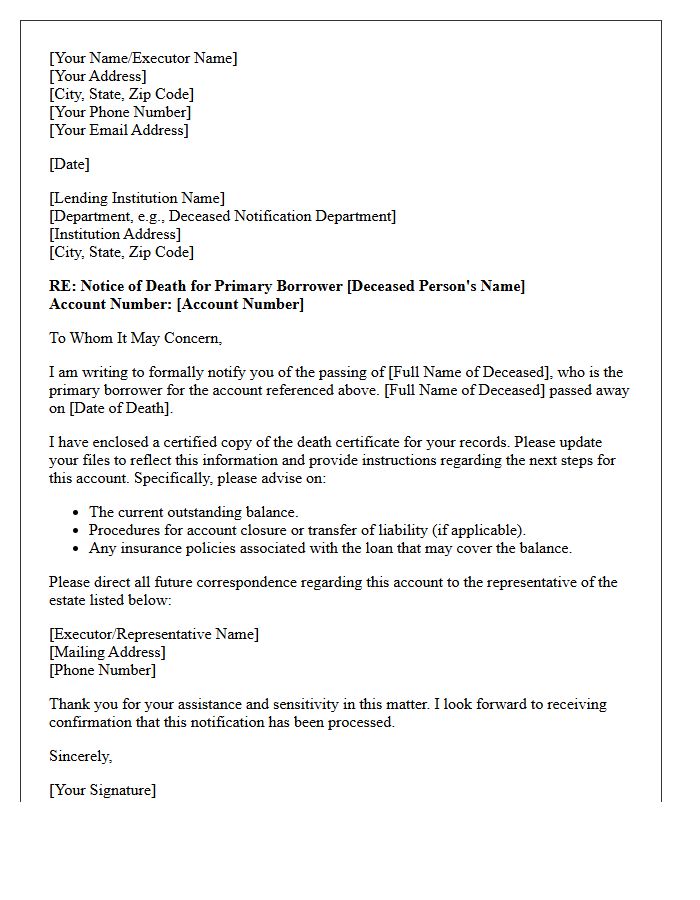

Primary Borrower Death Notification Letter

A Primary Borrower Death Notification Letter is a formal document sent to creditors and lenders to report a debtor's passing. It is crucial for preventing identity theft and initiating the estate settlement process. This notice typically includes the deceased's full name, social security number, and account details, accompanied by a certified copy of the death certificate. Timely notification ensures that interest accrual may be paused, late fees are avoided, and any credit life insurance or loan forgiveness clauses are activated to protect the surviving family's financial stability.

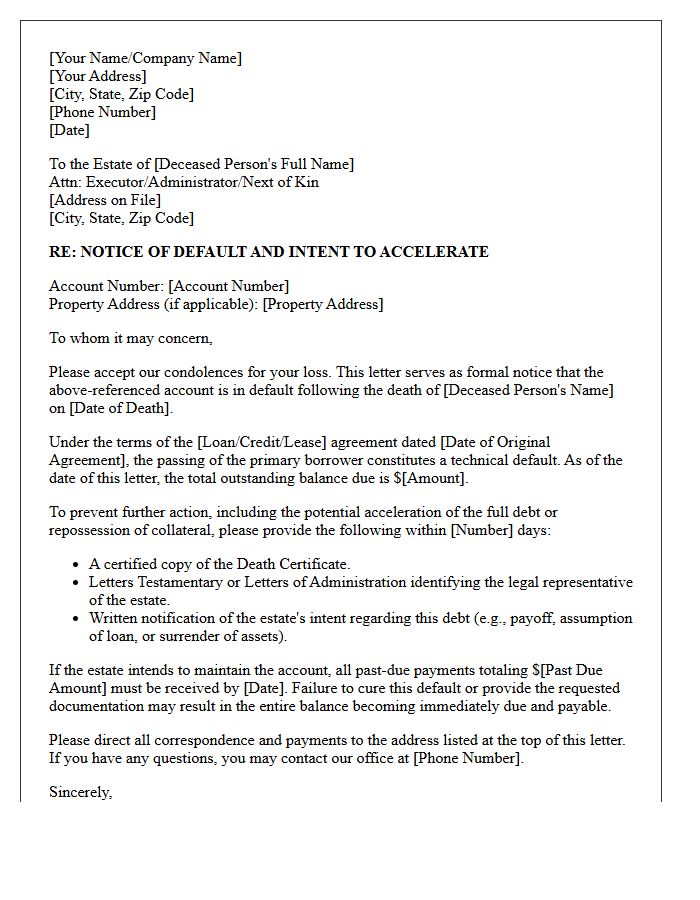

Notice of Default Due to Death Letter

A Notice of Default Due to Death is a legal formal alert issued by a lender when a mortgage borrower expires. Most loan agreements include a due-on-sale clause, which may trigger an immediate acceleration of the debt upon the owner's passing. Heirs must act quickly to prevent foreclosure by communicating with the loan servicer. Identifying successor in interest status is vital for survivors to gain legal rights to manage the account, assume the monthly payments, or negotiate a loan modification to retain the property title.

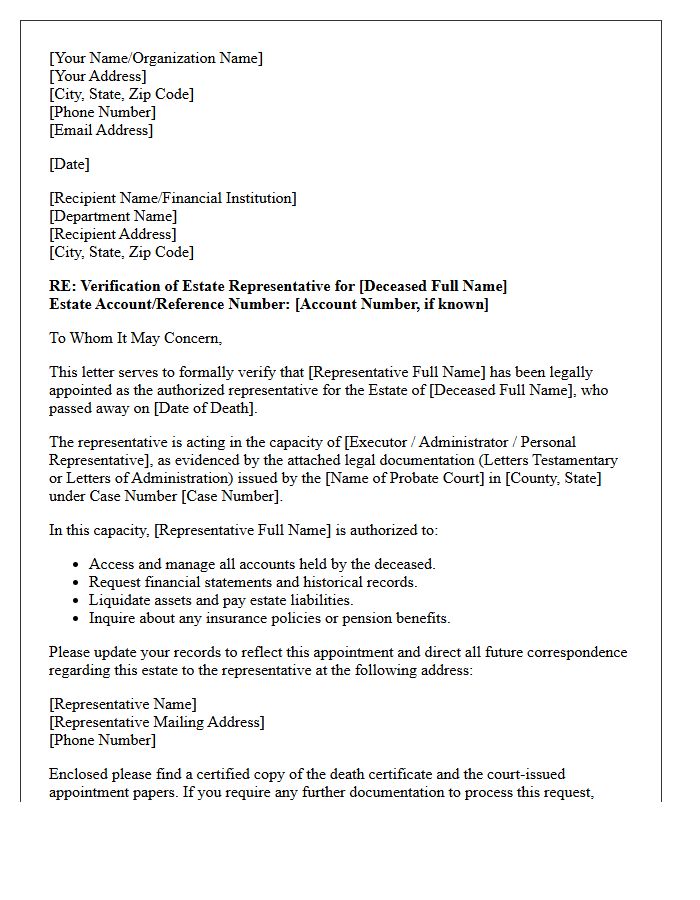

Estate Representative Verification Letter

An Estate Representative Verification Letter, often called Letters Testamentary or Letters of Administration, is a legal document issued by a probate court. This essential instrument officially confirms an individual's authority to manage a deceased person's assets. Financial institutions and government agencies require this verification to grant access to bank accounts, transfer property titles, and settle outstanding debts. It serves as formal proof that the designated executor or administrator has the fiduciary power to act on behalf of the estate during the settlement process.

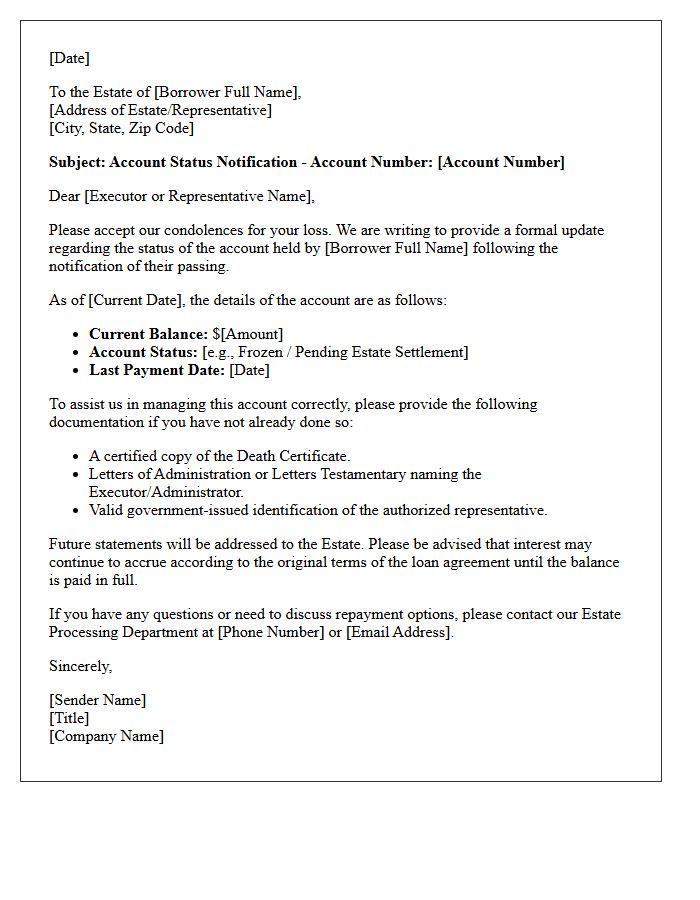

Deceased Borrower Account Status Letter

A Deceased Borrower Account Status Letter is a formal notification issued by lenders to confirm the outstanding balance and legal standing of a debt after a debtor passes away. This document is essential for estate executors and heirs to understand financial liabilities, such as mortgages or personal loans. It outlines repayment requirements, interest accrual, and potential foreclosure risks. Receiving this letter is a critical step in the probate process, allowing representatives to settle obligations or negotiate settlements before assets are distributed to beneficiaries according to the will or law.

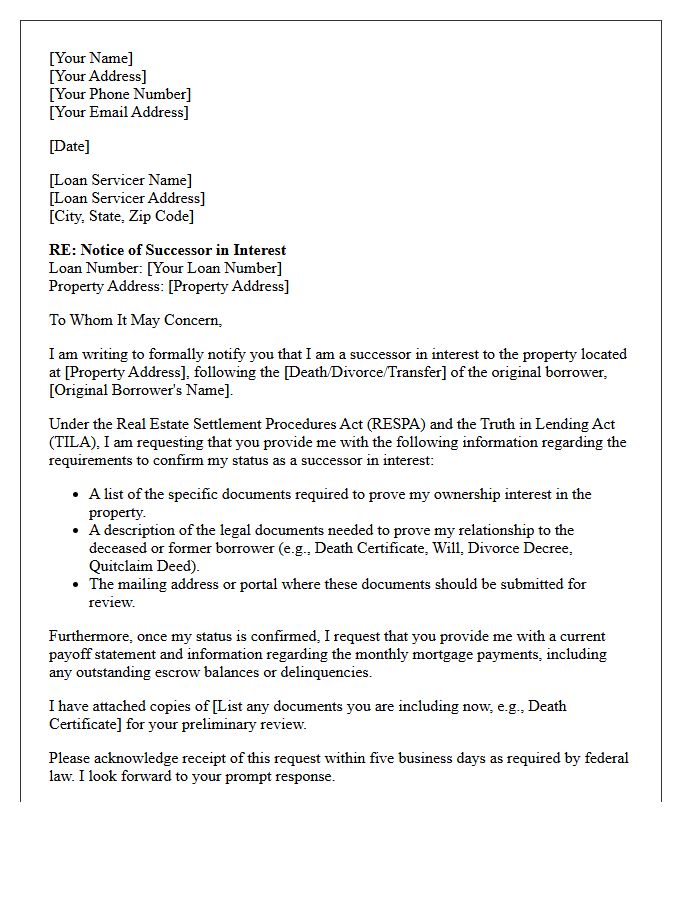

Successor in Interest Information Letter

A Successor in Interest Information Letter is a legal document sent by a mortgage servicer to individuals who have inherited property or acquired ownership through legal transfers. It outlines the legal requirements and documentation needed to confirm your identity as the lawful successor. Once confirmed, you gain specific rights under federal law, allowing you to access loan information, receive statements, and pursue loss mitigation options. Providing the requested proof promptly is essential to protect your property ownership and manage the existing mortgage debt effectively after a homeowner's death or transfer.

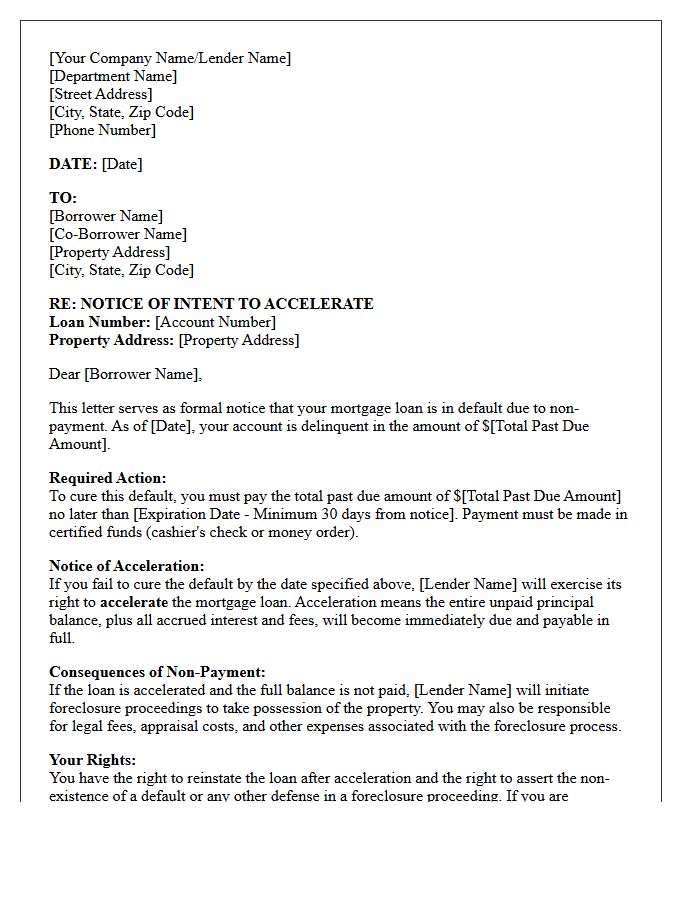

Mortgage Debt Acceleration Warning Letter

A Mortgage Debt Acceleration Warning Letter is a critical notice from your lender indicating that your loan is in default. This formal communication warns that the entire remaining balance may become due immediately if the delinquency is not resolved. Receiving this document is the final step before the legal foreclosure process begins. To protect your home, you must act quickly to pay the specified arrears or contact your servicer to discuss loss mitigation options. Ignoring this letter often leads to the loss of your property through a trustee sale.

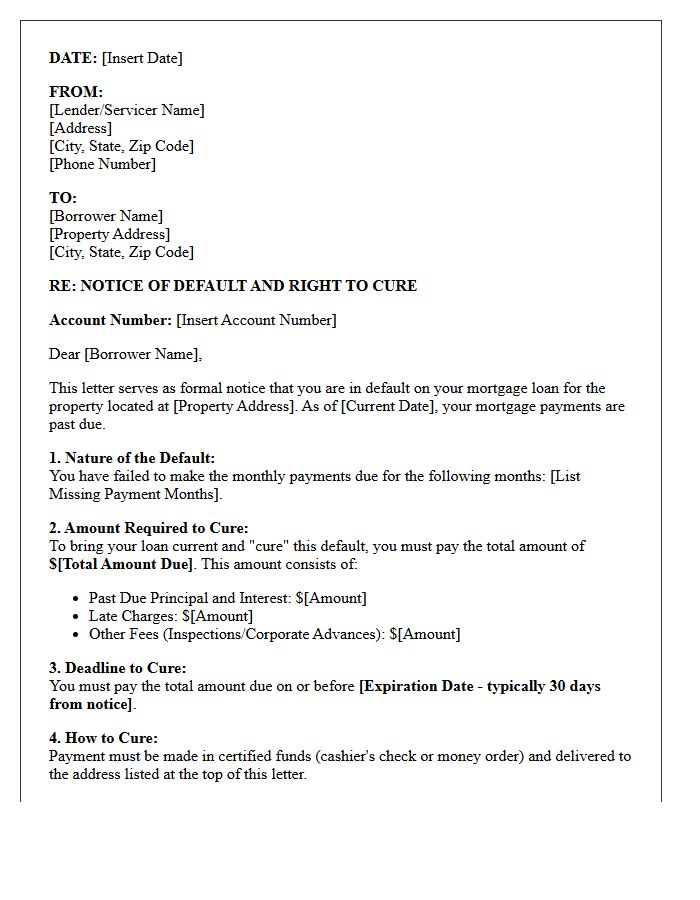

Right to Cure Mortgage Default Letter

A Right to Cure notice is a formal legal document sent by mortgage lenders before initiating foreclosure. It informs homeowners that they are in default due to missed payments and specifies the exact amount required to reinstate the loan. This letter provides a strictly defined grace period, typically 30 to 90 days, to pay the arrears and late fees. Acting promptly during this window is essential to stop legal proceedings, as it represents your final opportunity to resolve the delinquency and protect your homeownership rights before the foreclosure process officially begins.

Assumption of Mortgage Eligibility Letter

An Assumption of Mortgage Eligibility Letter is a formal document issued by a lender verifying that a potential buyer meets specific financial criteria to take over a seller's existing loan. This process allows the buyer to inherit the original interest rate and terms. To qualify, applicants must undergo a rigorous credit underwriting review, providing proof of income and assets. Obtaining this letter is the critical first step in a loan assumption, ensuring the lender approves the transfer of debt liability from the original borrower to the new homeowner.

Foreclosure Intent and Counseling Letter

A Foreclosure Intent and Counseling Letter is a formal legal notice sent by mortgage servicers to homeowners in default. This crucial document warns that the lender intends to initiate legal proceedings to seize the property. Importantly, it provides a list of housing counseling agencies approved by HUD to help borrowers explore loss mitigation options. Receiving this letter marks the final opportunity to seek professional guidance and negotiate a loan modification or repayment plan to stop the foreclosure process before it officially begins in court.

Outstanding Loan Balance Statement Letter

An Outstanding Loan Balance Statement Letter is an official document providing a real-time snapshot of your remaining debt. It specifies the exact principal amount, accrued interest, and applicable fees required to satisfy the obligation. This formal record is essential for financial planning, refinancing, or verifying repayment progress. It serves as legal evidence of your current liability, helping borrowers track their amortization schedule and ensure all payments are accurately credited by the lender to maintain financial transparency.

Probate Court Documentation Request Letter

A Probate Court Documentation Request Letter is a formal written inquiry used to obtain official case records, such as wills, letters of testamentary, or inventory filings. When drafting this request, you must include the specific case number and the full legal name of the deceased to ensure accuracy. Clearly state whether you require simple photocopies or certified copies, as these are often necessary for legal asset transfers. Providing a self-addressed stamped envelope and the required research fee will expedite the court clerk's processing of your vital information request.

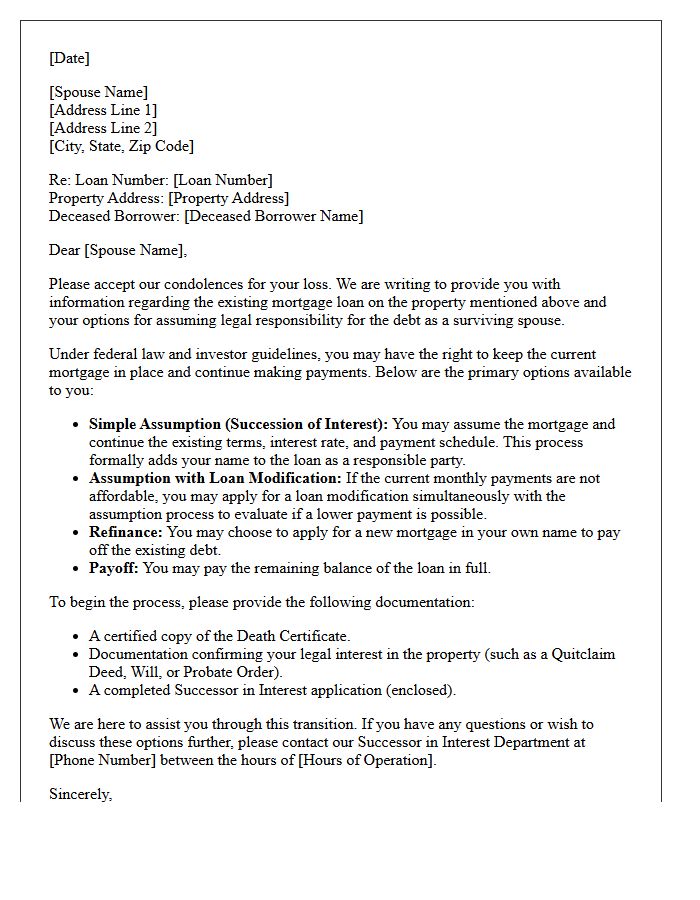

Surviving Spouse Assumption Options Letter

The Surviving Spouse Assumption Options Letter is a critical document sent by mortgage servicers after a homeowner's death. It outlines legal rights for the widow or widower to formally assume the mortgage debt. This process allows the survivor to maintain the existing interest rate and payment terms without a full credit re-evaluation. Understanding these options is essential for ensuring home retention and preventing foreclosure. Survivors must promptly review the deadline for returning required documentation to establish their status as a successor in interest and protect their equity.

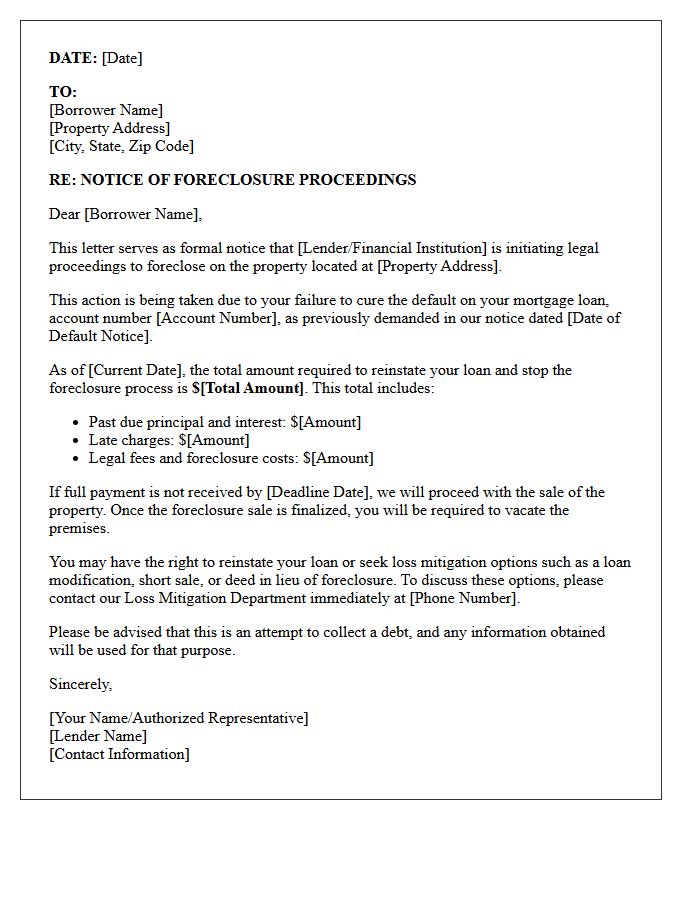

Notice of Foreclosure Proceedings Letter

A Notice of Foreclosure Proceedings is a formal legal document signaling that a lender has initiated a lawsuit to seize a property due to mortgage default. Receiving this letter is the final warning before a judicial sale occurs. It outlines the total debt owed, legal grounds for the action, and a specific deadline to respond. Homeowners must act immediately to explore loss mitigation options, such as loan modification or short sales, to prevent losing their equity and home ownership through the court system.

What is a Notice of Default due to the death of a primary borrower?

A Notice of Default (NOD) is a formal legal notification sent by a mortgage lender to inform heirs or surviving co-borrowers that the mortgage loan is in arrears following the primary borrower's passing. It signifies the beginning of the foreclosure process because monthly payments have been missed during the transition of the estate.

Can a lender foreclose immediately after the death of the primary borrower?

While the death of a borrower does not cancel the debt, federal laws such as the Garn-St. Germain Act protect certain heirs and family members from immediate foreclosure. Lenders typically cannot trigger an "acceleration clause" solely due to death, provided a qualified successor continues making timely mortgage payments and communicates with the servicer.

What should heirs do upon receiving a Notice of Default?

Heirs should immediately contact the mortgage servicer to provide a death certificate and proof of heirship to be recognized as a "successor in interest." To stop the foreclosure process, heirs must resolve the delinquency through a reinstatement payment, a loan modification, or by selling the property to satisfy the outstanding balance.

Does the "Due-on-Sale" clause apply when a primary borrower dies?

In most residential cases involving family members, the "Due-on-Sale" clause cannot be enforced to demand immediate full payment upon the death of the borrower. Federal regulations allow relatives who inherit the home to take over the existing mortgage terms and continue payments without needing to refinance immediately, provided they occupy the property.

How can I stop a foreclosure if the primary borrower died without a will?

If the borrower died intestate (without a will), you may need to open a probate case to be legally appointed as the personal representative or executor of the estate. This legal standing allows you to negotiate with the lender, apply for loss mitigation options, or authorize the sale of the home to prevent the foreclosure from finalizing.

Comments