Receiving a Notice of Default for Failure to Maintain Hazard Insurance signifies a serious breach of your mortgage agreement. Lenders require continuous coverage to protect the collateral. Failure to provide proof of insurance can lead to costly force-placed policies or potential foreclosure proceedings. Understanding your obligations is essential to protecting your home. To help you respond quickly, below are some ready to use templates.

Image cover: Formal Notice of Default: Failure to Maintain Required Hazard Insurance Templates

Letter Samples List

- First Warning Letter for Expired Hazard Insurance

- Second Notice Letter for Pending Lender Placed Insurance

- Final Demand Letter for Proof of Hazard Insurance Coverage

- Notice of Default Letter for Failure to Maintain Hazard Insurance

- Mortgage Covenant Breach Letter for Lapsed Hazard Insurance

- Lender Placed Hazard Insurance Activation Letter

- Escrow Account Adjustment Letter for Hazard Insurance Premium

- Loan Acceleration Letter Due to Hazard Insurance Default

- Intent to Foreclose Letter for Hazard Insurance Breach

- Grace Period Expiration Letter for Hazard Insurance Renewal

- Force Placed Hazard Insurance Cancellation Letter

- Default Cure and Reinstatement Letter for Hazard Insurance

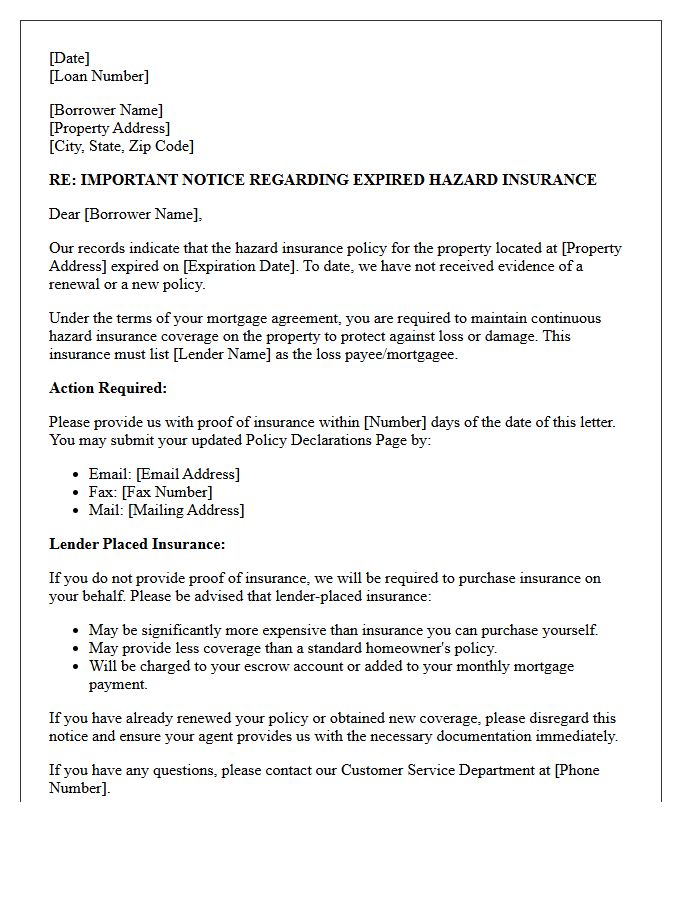

First Warning Letter for Expired Hazard Insurance

Receiving a First Warning Letter for expired hazard insurance indicates your mortgage lender has identified a lapse in coverage. Your loan agreement requires active protection to secure the collateral. If you do not provide proof of a current policy immediately, the lender may implement force-placed insurance. This substitute coverage is typically significantly more expensive and offers less protection for your personal property. To resolve this, contact your insurance agent to verify coverage or renew your policy, then submit the updated declarations page to your lender's compliance department to avoid additional fees.

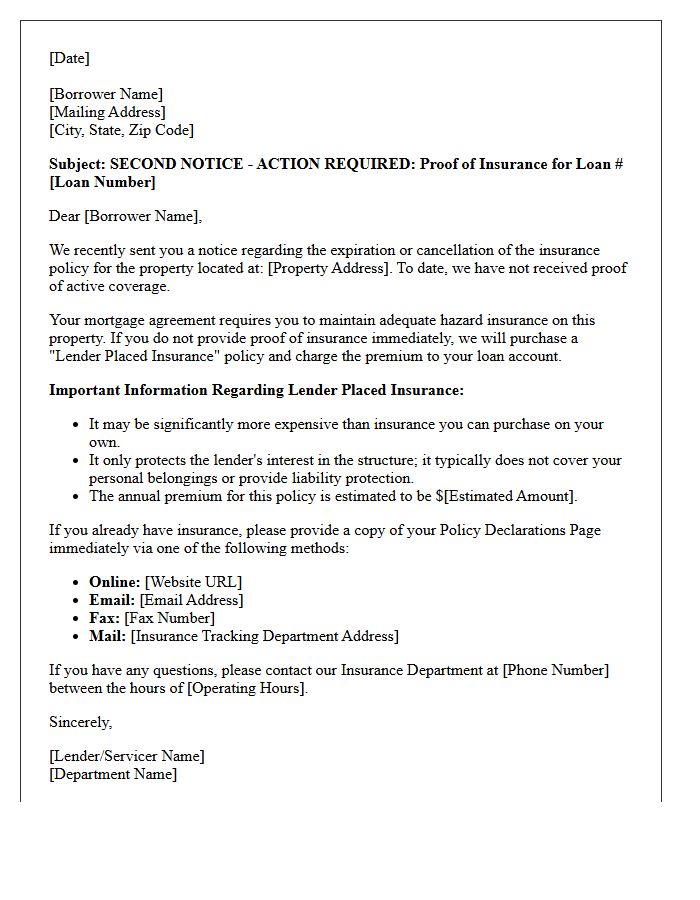

Second Notice Letter for Pending Lender Placed Insurance

A Second Notice Letter is a formal notification sent forty-five days after the first warning regarding a lapse in coverage. It informs you that your mortgage servicer will finalize Lender-Placed Insurance if proof of an active policy is not provided within fifteen days. This forced insurance is significantly more expensive and offers limited protection, typically excluding personal liability or belongings. To avoid these high costs and increased monthly payments, you must immediately submit your insurance declarations page to the lender to confirm adequate homeowners insurance exists.

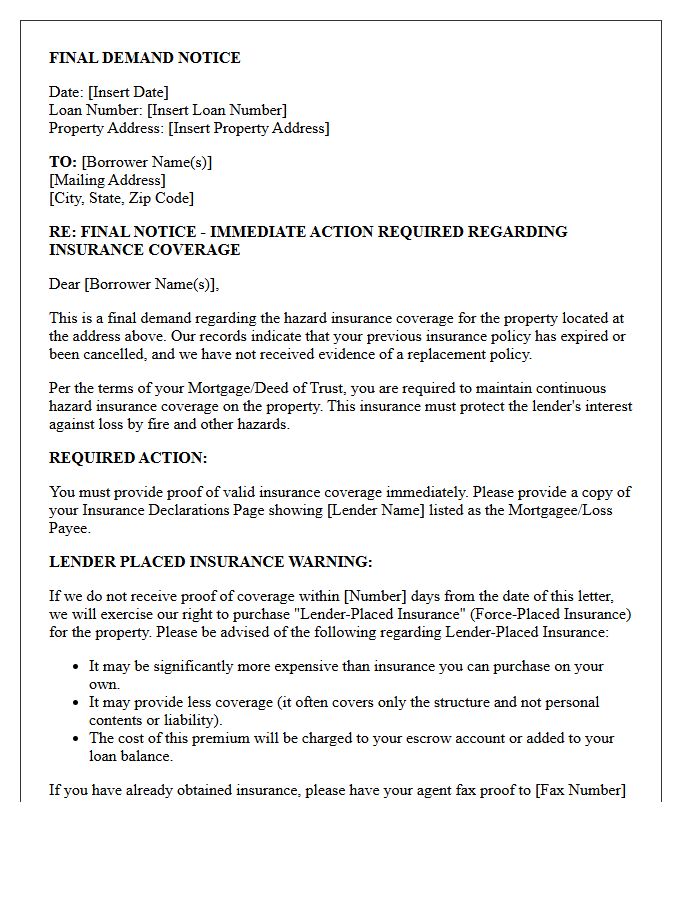

Final Demand Letter for Proof of Hazard Insurance Coverage

A final demand letter for proof of hazard insurance is a critical notice from your mortgage lender. It warns that if you do not provide evidence of coverage immediately, the lender will implement force-placed insurance. This lender-placed policy is typically much more expensive and offers less protection than private plans. To resolve this, you must quickly submit your current policy declarations page to the servicer. Maintaining active insurance is a mandatory requirement of your loan agreement to protect the property against physical damage or loss.

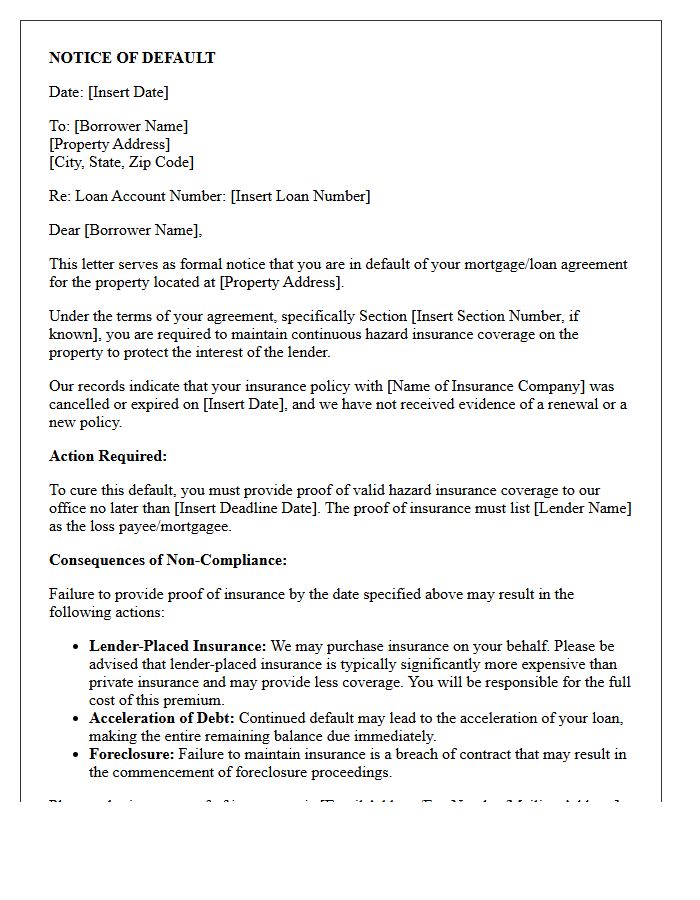

Notice of Default Letter for Failure to Maintain Hazard Insurance

A Notice of Default for failing to maintain hazard insurance is a formal warning from your lender. This document signifies a breach of the mortgage contract, as continuous property coverage is mandatory to protect the collateral. Failure to provide proof of insurance allows the lender to implement force-placed insurance, which is typically more expensive and offers less protection. If the deficiency is not corrected within the specified timeframe, the lender may initiate foreclosure proceedings to recover the loan balance. Promptly providing updated policy information is essential to resolve this default.

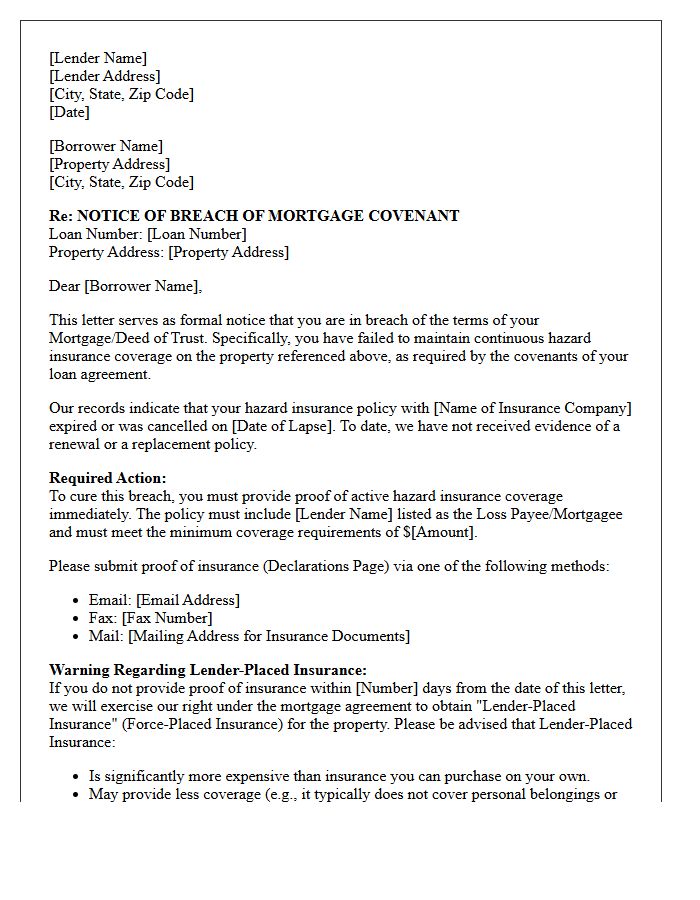

Mortgage Covenant Breach Letter for Lapsed Hazard Insurance

A mortgage covenant breach letter for lapsed hazard insurance is a formal notice stating you have violated your loan agreement by failing to maintain property coverage. Your lender requires hazard insurance to protect their financial interest in the asset. If you do not provide proof of a current policy, the servicer may implement force-placed insurance, which is significantly more expensive and offers less protection. To resolve this, immediately contact your insurer to reinstate coverage and submit the updated declarations page to your lender to avoid potential foreclosure proceedings.

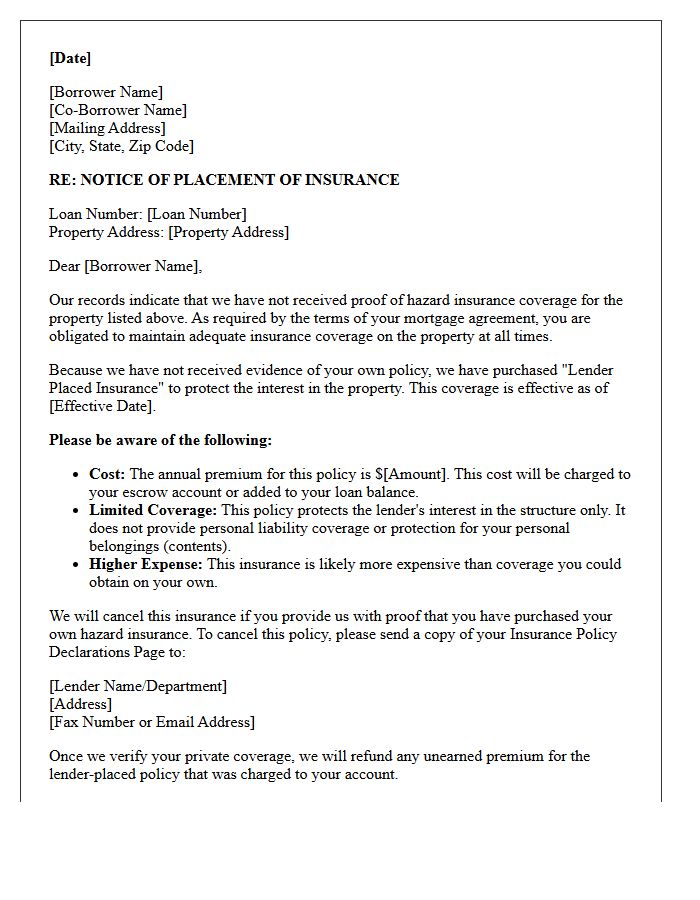

Lender Placed Hazard Insurance Activation Letter

A Lender Placed Hazard Insurance Activation Letter notifies homeowners that their mortgage servicer has purchased forced-placed coverage on their behalf. This occurs when your personal policy lapses or lacks sufficient protection. This insurance is typically much more expensive and provides limited coverage, often protecting only the lender's financial interest in the structure rather than your personal belongings or liability. To cancel this costly policy, you must immediately provide proof of continuous insurance to your lender to ensure your property remains adequately protected and to avoid unnecessary escrow charges.

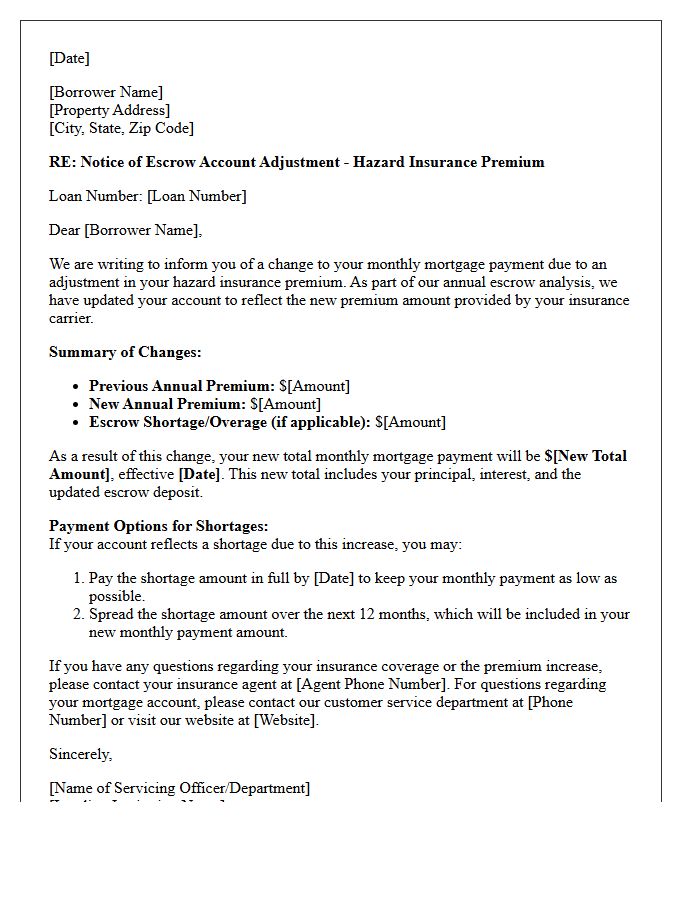

Escrow Account Adjustment Letter for Hazard Insurance Premium

An escrow account adjustment letter notifies homeowners of changes in their monthly mortgage payment due to updated hazard insurance premiums. When your insurer adjusts its rates, your lender recalculates your escrow analysis to cover the new cost. If the premium increases, it may result in an escrow shortage, requiring a one-time payment or increased monthly installments to maintain the minimum required balance. Reviewing this document is essential to verify that your coverage limits are accurate and to understand how insurance fluctuations directly impact your total mortgage obligation.

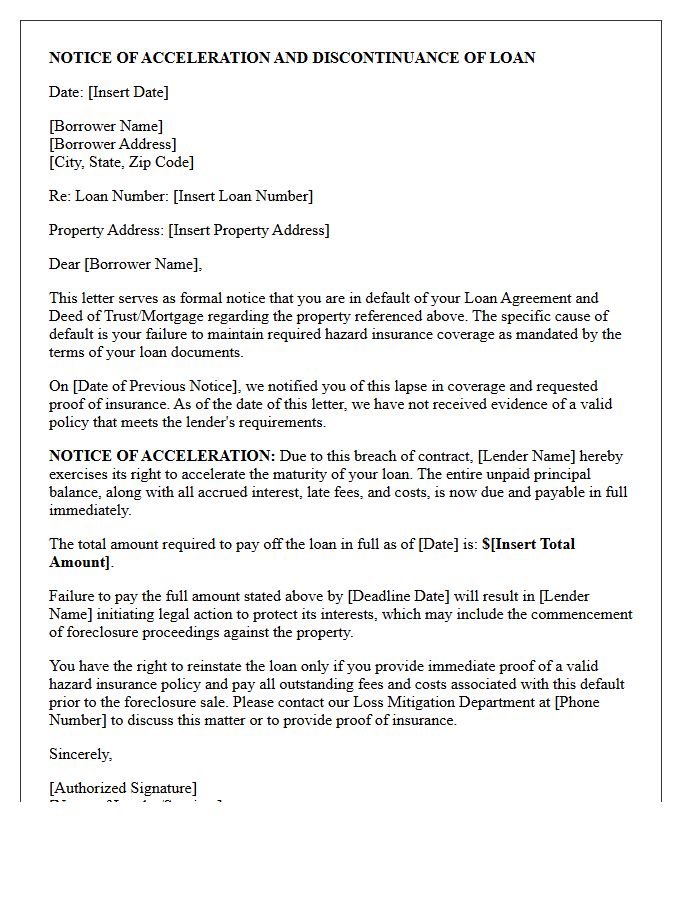

Loan Acceleration Letter Due to Hazard Insurance Default

A loan acceleration letter due to hazard insurance default is a formal notice stating that your lender is demanding immediate repayment of the entire mortgage balance. This occurs because maintaining valid property insurance is a mandatory contractual requirement. If coverage lapses, the lender considers the loan in default to protect their collateral. To resolve this urgent legal demand and prevent potential foreclosure, you must promptly provide proof of a current policy or pay the outstanding balance as specified in the acceleration notice.

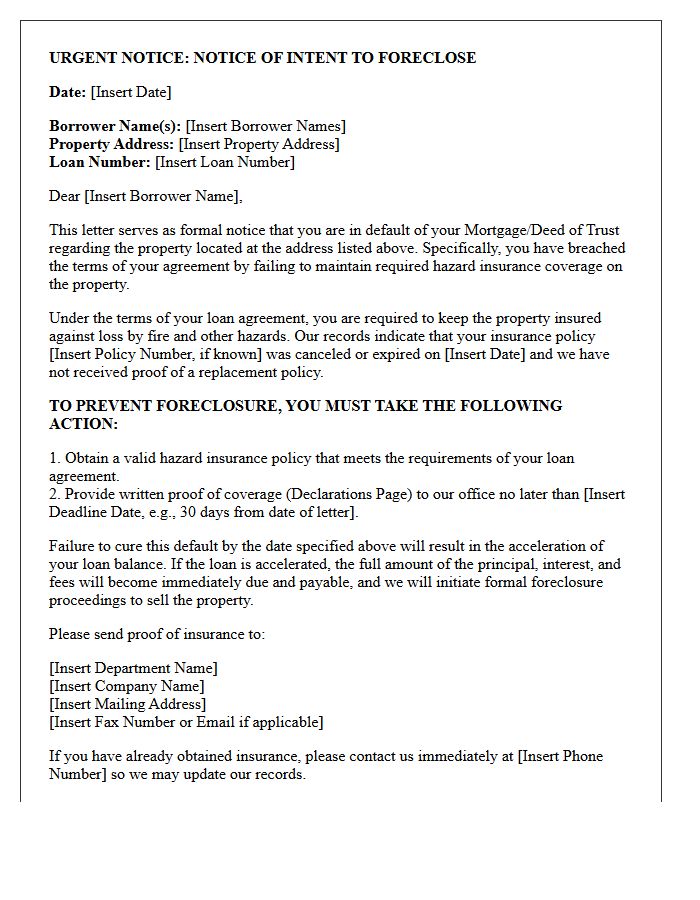

Intent to Foreclose Letter for Hazard Insurance Breach

An Intent to Foreclose Letter for a hazard insurance breach is a formal notice issued when a homeowner fails to maintain required property coverage. Lenders require continuous insurance to protect their collateral. If you receive this, your mortgage contract is in default. To avoid legal action, you must immediately provide proof of a valid policy or pay for force-placed insurance, which is often more expensive. Ignoring this letter allows the lender to initiate foreclosure proceedings to recover the loan balance due to the increased financial risk of an uninsured property.

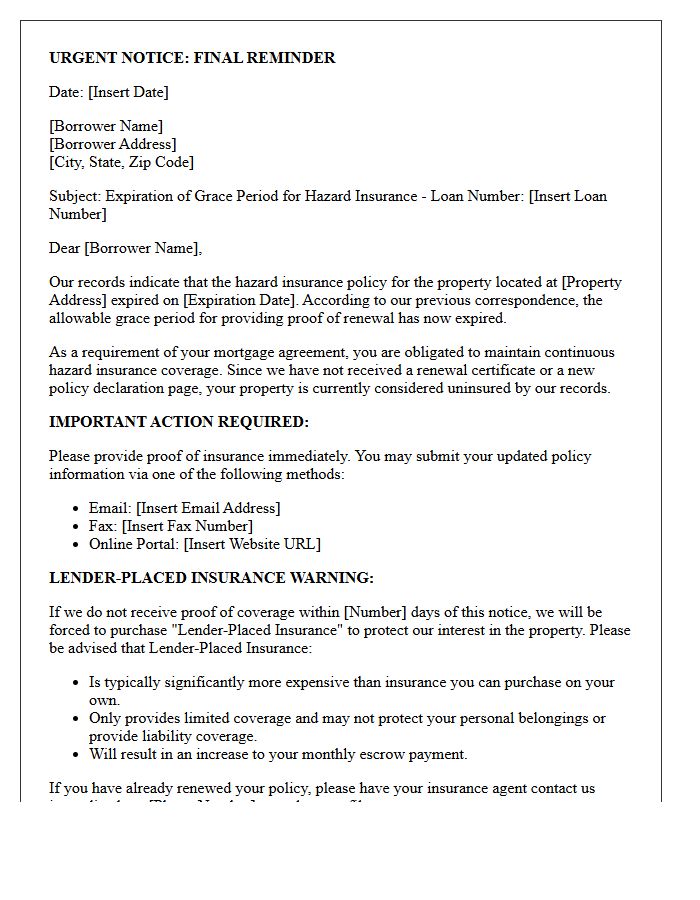

Grace Period Expiration Letter for Hazard Insurance Renewal

A Grace Period Expiration Letter is a critical notice from your mortgage lender warning that your hazard insurance policy has lapsed. If you do not provide proof of coverage renewal immediately, the lender will implement force-placed insurance. This substitute policy is typically more expensive and offers less protection than private plans. To avoid financial loss, contact your agent to confirm payment and send the updated declarations page to your loan servicer before the specified deadline to maintain continuous property protection.

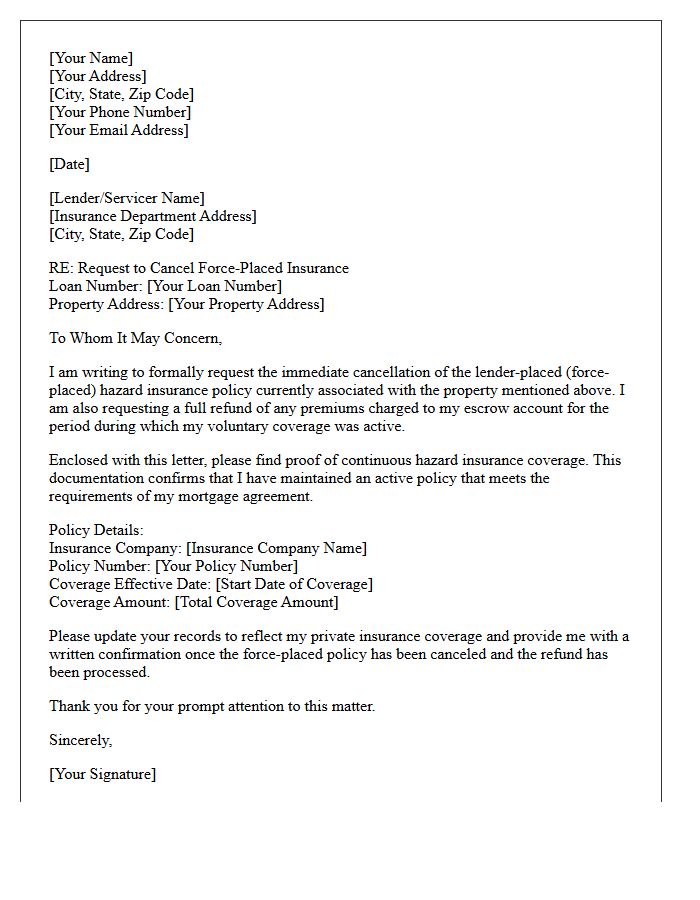

Force Placed Hazard Insurance Cancellation Letter

A Force Placed Hazard Insurance Cancellation Letter is a formal request sent to your mortgage lender to remove expensive, lender-placed coverage. To succeed, you must provide proof of private insurance, such as a declarations page, showing your policy meets the lender's minimum requirements and has no coverage gaps. Once verified, the lender is legally required to cancel the forced policy and refund any overlapping premiums charged during the period of dual coverage. Timely submission ensures you regain control over your escrow payments and protect your financial interests.

Default Cure and Reinstatement Letter for Hazard Insurance

A Default Cure and Reinstatement Letter is a formal notice sent by mortgage servicers when hazard insurance coverage lapses. This document warns homeowners that failing to maintain active insurance violates their loan agreement. It specifies the deadline to provide proof of coverage and the required steps to resolve the default. If the policy is not reinstated, the lender will implement expensive force-placed insurance to protect their collateral. Timely action is essential to avoid increased monthly payments, potential foreclosure proceedings, and the higher costs associated with lender-procured policies.

What is a Notice of Default for Failure to Maintain Hazard Insurance?

A Notice of Default for Failure to Maintain Hazard Insurance is a formal legal notification sent by a mortgage lender to a borrower when the required property insurance policy has lapsed or been cancelled. This notice warns the homeowner that they are in violation of their loan agreement and must provide proof of coverage to avoid further legal action or foreclosure.

Can a lender foreclose if I fail to maintain hazard insurance?

Yes, failure to maintain hazard insurance is considered a technical default under most mortgage contracts. If the homeowner does not cure the default by obtaining a valid insurance policy and providing proof to the lender within the specified timeframe, the lender has the legal right to accelerate the loan and initiate foreclosure proceedings.

What is "Force-Placed Insurance" in a Notice of Default?

Force-placed insurance, also known as lender-placed insurance, is a policy the lender purchases on your behalf if you fail to provide proof of hazard insurance. This coverage is typically significantly more expensive than private insurance and only protects the lender's interest in the structure, not your personal belongings or liability.

How do I resolve a Notice of Default for insurance non-compliance?

To resolve the default, you must immediately reinstate your insurance policy or purchase a new hazard insurance policy that meets your lender's minimum requirements. Once obtained, you must send the "Declarations Page" or a certificate of insurance to your lender's loss draft department to prove the property is protected.

What happens if I have insurance but still received a Notice of Default?

If you have active coverage, the notice was likely triggered by a communication gap between your insurance provider and the lender. You should immediately contact your insurance agent to ensure the lender is listed as the "Loss Payee" with the correct address and provide the lender with your policy number to clear the default status from your account.

Comments