A Conditional Pre-Approval Letter Subject to Appraisal strengthens your offer by proving financial eligibility while noting that the loan depends on the property's market value. This document reassures sellers that financing is secure, provided the home's appraisal matches the purchase price. Understanding this requirement is essential for a smooth closing process. Below are some ready to use template.

Image cover: Conditional Pre-Approval Letters: Appraisal Contingency Templates and Samples

Letter Samples List

- Conditional Pre-Approval Letter Subject to Satisfactory Appraisal

- Mortgage Lender Conditional Pre-Approval Letter Contingent Upon Appraisal

- Subject to Appraisal Conditional Pre-Approval Letter for Homebuyers

- Conventional Loan Conditional Pre-Approval Letter Pending Appraisal Results

- FHA Mortgage Conditional Pre-Approval Letter Subject to Property Appraisal

- VA Loan Conditional Pre-Approval Letter With Appraisal Contingency

- Jumbo Mortgage Conditional Pre-Approval Letter Subject to Appraisal Valuation

- Primary Residence Conditional Pre-Approval Letter Pending Appraisal Review

- Investment Property Conditional Pre-Approval Letter Subject to Appraisal

- First-Time Buyer Conditional Pre-Approval Letter Contingent on Appraisal

- Refinance Conditional Pre-Approval Letter Subject to Home Appraisal

- Commercial Mortgage Conditional Pre-Approval Letter Pending Appraisal

- Portfolio Loan Conditional Pre-Approval Letter Subject to Final Appraisal

- High-Balance Conditional Pre-Approval Letter With Appraisal Requirement

- Multi-Family Home Conditional Pre-Approval Letter Subject to Appraisal

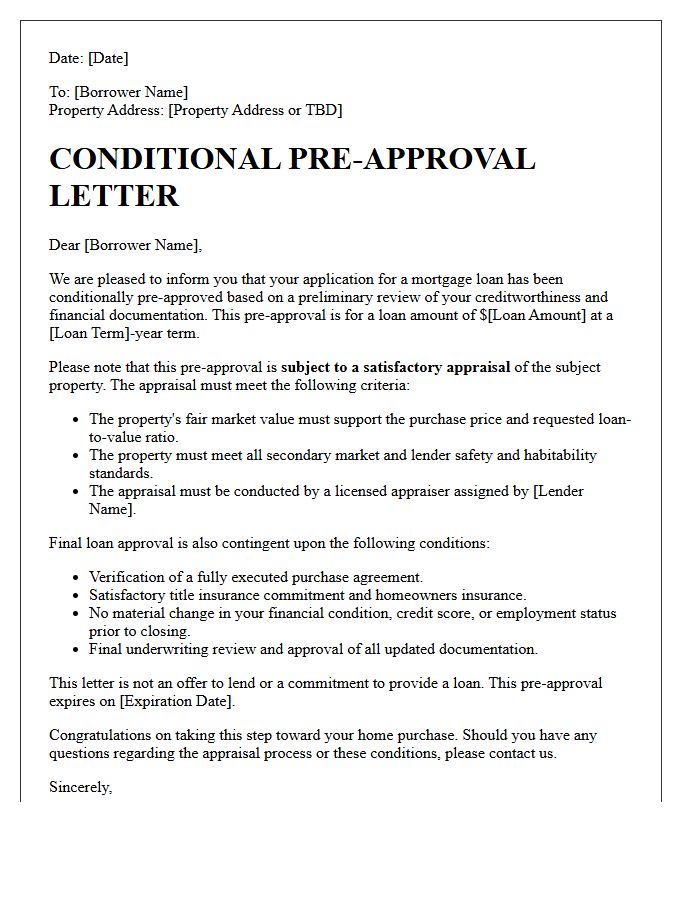

Conditional Pre-Approval Letter Subject to Satisfactory Appraisal

A conditional pre-approval letter subject to satisfactory appraisal signifies that a lender has verified your financial profile but requires a professional valuation of the property before final funding. The most critical factor is the home appraisal, which must meet or exceed the agreed purchase price to secure the loan amount. If the property value falls short, you may need to cover the appraisal gap or renegotiate terms. This document confirms creditworthiness while emphasizing that the collateral's worth is the ultimate security for the mortgage agreement.

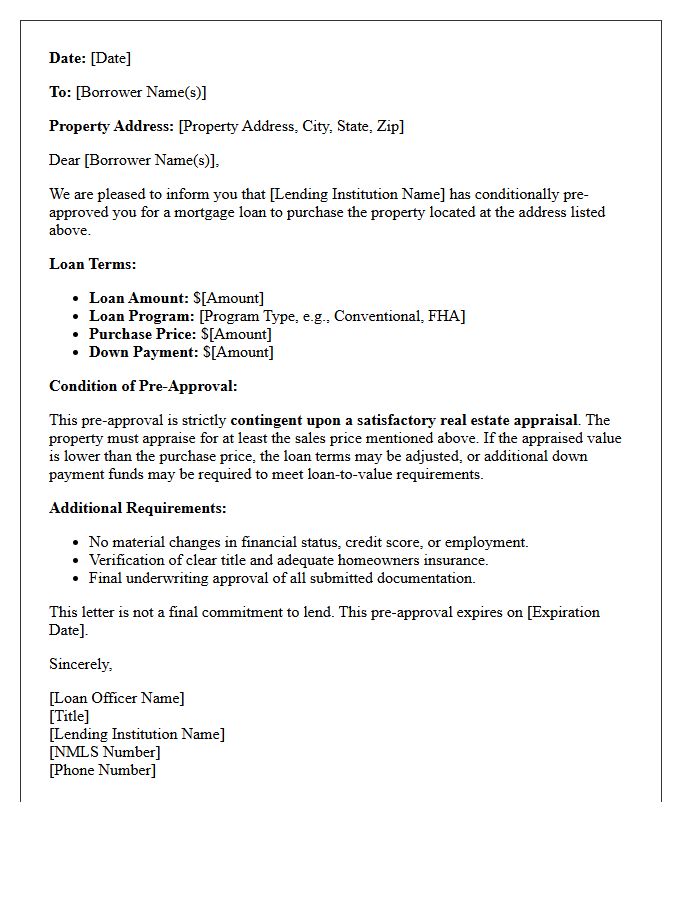

Mortgage Lender Conditional Pre-Approval Letter Contingent Upon Appraisal

A conditional pre-approval letter signifies a lender's intent to fund your loan, provided specific requirements are met. The most critical factor is the appraisal contingency, which ensures the property's market value supports the purchase price. If the professional valuation comes in lower than the agreed cost, the lender may reduce the loan amount or deny the application entirely. This document strengthens your offer but remains subject to a satisfactory property inspection and final underwriting verification to mitigate financial risk for the financial institution before closing the deal.

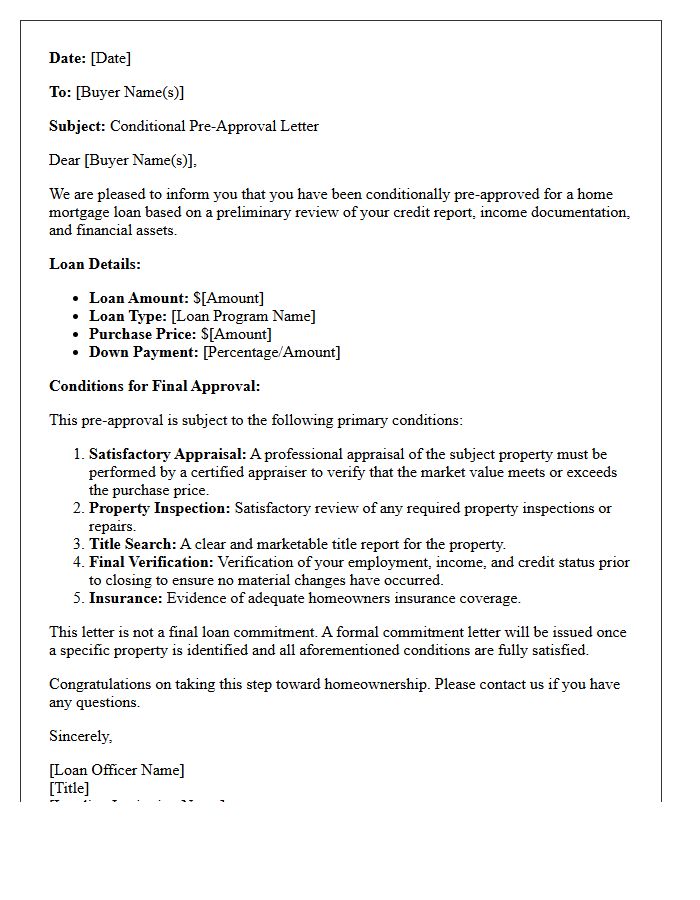

Subject to Appraisal Conditional Pre-Approval Letter for Homebuyers

A Subject to Appraisal conditional pre-approval letter indicates a lender's intent to finance your home purchase provided the property's market value meets or exceeds the sales price. While it confirms your creditworthiness, the final loan commitment remains contingent upon a professional appraisal report. If the home appraises lower than your offer, a valuation gap occurs, potentially requiring a larger down payment or price renegotiation. This document strengthens your offer but reminds sellers that the deal depends on the house being worth the investment amount.

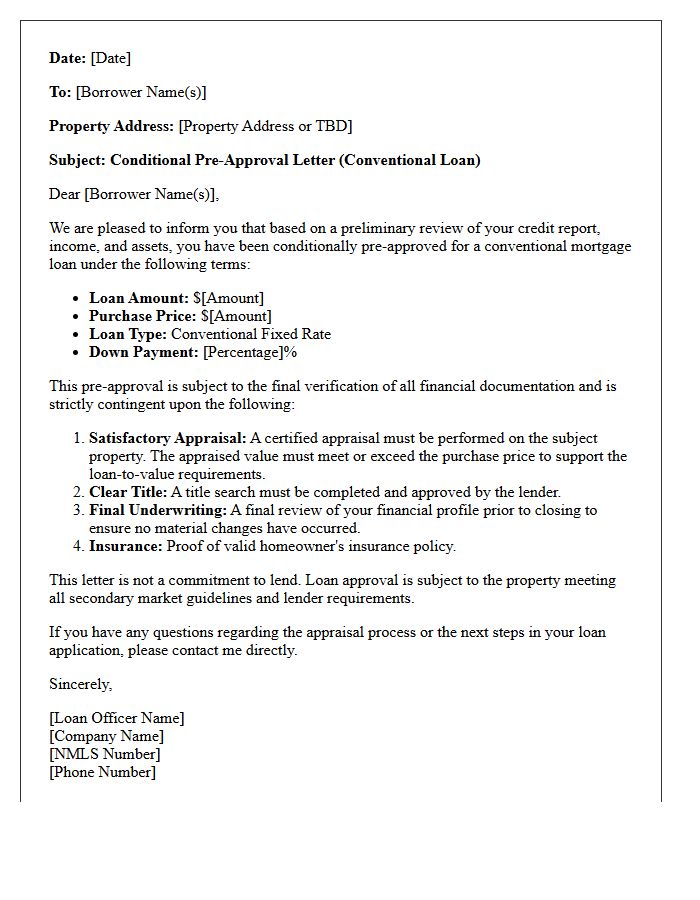

Conventional Loan Conditional Pre-Approval Letter Pending Appraisal Results

A Conditional Pre-Approval Letter for a conventional loan signifies that a lender has verified your financial documentation but final funding remains pending appraisal results. This crucial stage ensures the property's market value supports the loan amount. If the appraisal comes in lower than the purchase price, it may create a financing gap that requires negotiation or a larger down payment. Understanding this contingency is vital for buyers to protect their earnest money and ensure the collateral meets strict secondary market guidelines before closing the mortgage transaction.

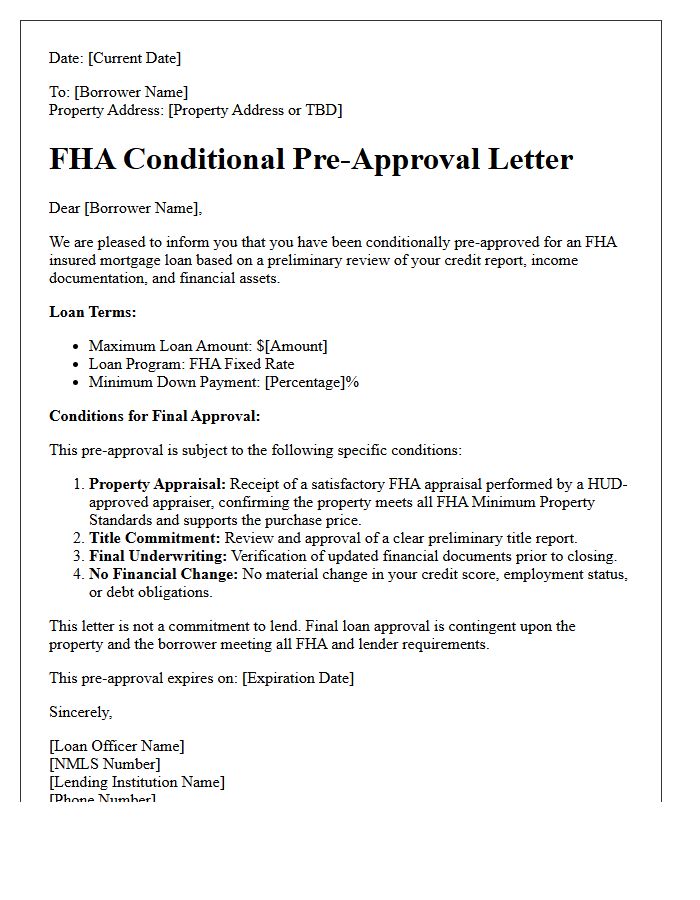

FHA Mortgage Conditional Pre-Approval Letter Subject to Property Appraisal

An FHA mortgage conditional pre-approval indicates a lender has verified your income, credit, and assets, but final funding remains subject to property appraisal. This stage is crucial because the home must meet specific HUD safety standards and value requirements. If the appraisal comes in lower than the purchase price or identifies structural issues, the loan amount may be adjusted or denied. This letter proves your buying power to sellers while highlighting that the property itself must still pass a rigorous federal inspection to secure the mortgage.

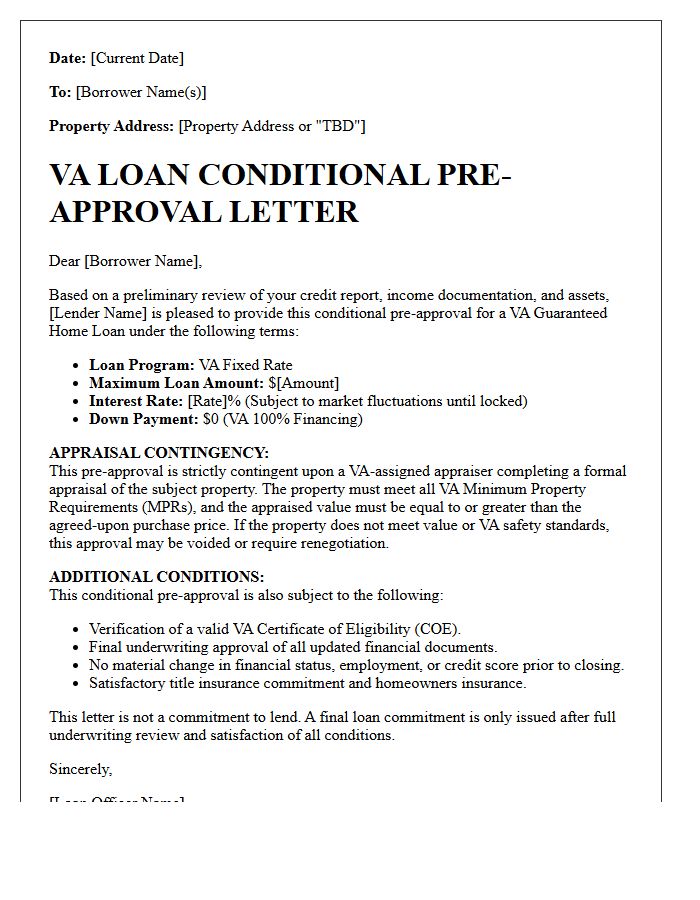

VA Loan Conditional Pre-Approval Letter With Appraisal Contingency

A VA loan conditional pre-approval letter signifies a lender's preliminary intent to fund your mortgage based on verified income and credit. However, the appraisal contingency is a vital safeguard. It ensures the Department of Veterans Affairs verifies the property's Market Value and confirms it meets strict Minimum Property Requirements (MPRs) for safety and habitability. If the home fails to appraise at the purchase price or meet VA standards, the buyer can typically cancel the contract without penalty. This letter proves you are a qualified buyer while protecting your investment from overpaying for a substandard property.

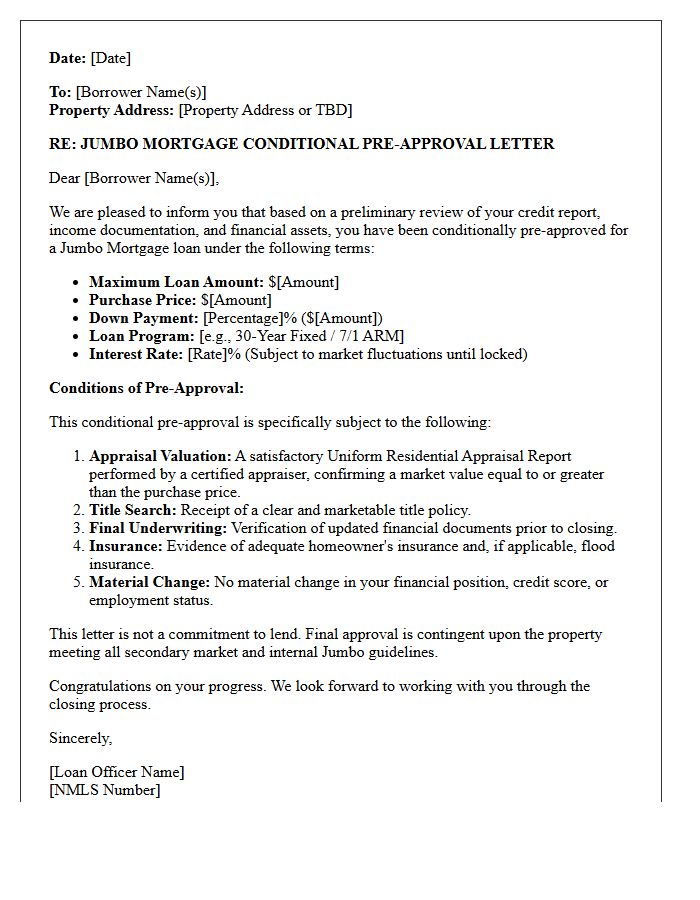

Jumbo Mortgage Conditional Pre-Approval Letter Subject to Appraisal Valuation

A Jumbo Mortgage Conditional Pre-Approval indicates a lender has verified your high-balance income and credit, yet the loan remains subject to appraisal valuation. Because jumbo loans exceed standard conforming limits, lenders require strict collateral confirmation. If the professional appraisal identifies a value lower than the purchase price, your financing may be denied or require a larger down payment. This document proves purchasing power but reminds buyers that final funding depends entirely on the home's market value meeting specific loan-to-value requirements during the underwriting process.

Primary Residence Conditional Pre-Approval Letter Pending Appraisal Review

A Primary Residence Conditional Pre-Approval Letter indicates a lender is willing to finance your home, provided specific conditions are met. The most critical contingency is the Pending Appraisal Review, which confirms the property's market value supports the loan amount. If the appraisal comes in lower than the purchase price, you may need to increase your down payment or renegotiate the deal. This document strengthens your offer but remains subject to a final collateral assessment and a comprehensive underwriting verification of your financial stability before closing.

Investment Property Conditional Pre-Approval Letter Subject to Appraisal

An investment property conditional pre-approval letter signifies a lender's preliminary commitment based on your creditworthiness. However, being subject to appraisal means the final loan amount depends on a professional valuation of the real estate. Since investment loans often require higher equity, the property must meet specific loan-to-value ratios and market rent estimates to secure funding. This document proves your buying power to sellers while highlighting that the deal remains contingent on the asset's verified market value and physical condition before closing.

First-Time Buyer Conditional Pre-Approval Letter Contingent on Appraisal

A conditional pre-approval letter for first-time buyers signifies a lender's preliminary commitment based on credit and income. However, it remains contingent on an appraisal, meaning the final loan amount depends on a professional valuation of the property. If the home's appraised value is lower than the agreed purchase price, a funding gap occurs. Buyers must then negotiate a lower price, pay the difference in cash, or risk loan denial. Understanding this valuation requirement is essential to protecting your earnest money deposit during the home-buying process.

Refinance Conditional Pre-Approval Letter Subject to Home Appraisal

A refinance conditional pre-approval letter signifies that a lender has reviewed your financial profile and is willing to lend, provided specific requirements are met. The most critical factor is the home appraisal, which determines the property's current market value. This step ensures the loan-to-value ratio aligns with underwriting guidelines. Since the approval is contingent on the valuation, the final loan amount or interest rate may change if the appraisal comes in lower than expected. Always verify all conditions early to ensure a smooth closing process.

Commercial Mortgage Conditional Pre-Approval Letter Pending Appraisal

A commercial mortgage conditional pre-approval letter serves as a lender's commitment to provide financing based on your current financial profile. However, the most critical contingency is the pending appraisal. This means final loan authorization depends on a professional valuation confirming the property's worth supports the loan-to-value ratio. Even with a pre-approval, the deal remains conditional until the collateral is verified. Buyers should ensure the property's condition and market data align with the purchase price to prevent funding gaps during the final underwriting stage.

Portfolio Loan Conditional Pre-Approval Letter Subject to Final Appraisal

A portfolio loan conditional pre-approval indicates a lender is prepared to finance your property using their private funds. The most critical factor is the Final Appraisal, as the lender must verify the asset's value matches the purchase price before closing. Unlike standard loans, these programs offer flexible underwriting tailored to unique financial situations. However, the commitment remains non-binding until the appraisal confirms the Collateral Value meets internal risk standards. Receiving this letter is a strong signal of intent, provided the property condition and valuation satisfy the final underwriting review.

High-Balance Conditional Pre-Approval Letter With Appraisal Requirement

A high-balance conditional pre-approval letter signifies a lender's preliminary commitment to finance a loan exceeding standard conforming limits. The most critical factor is the underwriting contingency, which remains subject to final verification. Because these loans involve significant capital, the appraisal requirement is mandatory to ensure the property's market value supports the high loan amount. Borrowers must provide comprehensive financial documentation, but final funding is only guaranteed once a professional appraiser confirms the asset's worth, mitigating risk for the financial institution before closing the transaction.

Multi-Family Home Conditional Pre-Approval Letter Subject to Appraisal

A multi-family home conditional pre-approval letter indicates a lender's intent to fund your purchase based on verified credit and income. However, the commitment is strictly subject to appraisal, meaning the property's fair market value must meet or exceed the sale price. For multi-family units, appraisers evaluate rental income potential alongside comparable sales. If the valuation comes in low, the loan amount may decrease, requiring a larger down payment. This letter strengthens your offer but remains contingent on the final professional valuation report of the specific investment property.

What is a conditional pre-approval letter subject to appraisal?

A conditional pre-approval letter subject to appraisal is a document from a lender stating you are qualified for a loan, provided the home's market value meets or exceeds the purchase price. This means the final loan commitment depends on a professional appraiser verifying the property's worth as collateral.

Why do lenders include an appraisal contingency in a pre-approval letter?

Lenders include this condition to protect their investment and ensure the Loan-to-Value (LTV) ratio remains within acceptable limits. Since the house serves as collateral, the lender will not finance an amount significantly higher than what the property is worth according to a formal valuation.

Does a conditional pre-approval guarantee I will get the mortgage?

No, it is not a final guarantee. While it shows you are creditworthy, the "subject to appraisal" clause means the deal can still fail if the home appraises for less than the offer price, or if other conditions-such as a final credit check or employment verification-are not met before closing.

What happens if the appraisal comes in lower than the pre-approved amount?

If the appraisal is lower than the purchase price, a "shortfall" occurs. You may need to cover the difference in cash, negotiate a lower price with the seller, or request a rebuttal of the appraisal. If neither party budges, the lender may decline the loan based on the appraisal condition.

How long is a conditional pre-approval letter subject to appraisal valid?

Typically, these letters are valid for 60 to 90 days. The timeframe is limited because your financial situation (credit score, debt-to-income ratio) and market interest rates can change, which may affect your eligibility even before the appraisal phase begins.

Comments