A Pre-Approval Letter for Specific Property Address demonstrates to sellers that you have verified financing for their exact home. Unlike general letters, this property-specific document strengthens your offer by showing precise loan commitment and financial credibility for a particular listing. It gives you a competitive edge in fast-moving real estate markets. Below are some ready to use template.

Image cover: Property-Specific Pre-Approval Letter: Professional Templates and Examples

Letter Samples List

- Specific Property Mortgage Pre-Approval Letter

- Conditional Pre-Approval Letter for Specific Address

- Conventional Loan Specific Property Pre-Approval Letter

- Federal Housing Administration Specific Address Pre-Approval Letter

- Veterans Affairs Home Loan Property Specific Pre-Approval Letter

- Jumbo Mortgage Specific Property Pre-Approval Letter

- Underwriter Certified Specific Property Pre-Approval Letter

- Single Property Address Financing Pre-Approval Letter

- Seller Directed Specific Address Pre-Approval Letter

- Verified Assets and Income Property Specific Pre-Approval Letter

- Appraisal Contingent Specific Property Pre-Approval Letter

- United States Department of Agriculture Specific Property Pre-Approval Letter

Specific Property Mortgage Pre-Approval Letter

A Specific Property Mortgage Pre-Approval Letter is a lender's formal commitment to finance a particular home rather than a general price range. Unlike a standard pre-approval, this document accounts for property-specific costs like property taxes, insurance, and HOA fees. It demonstrates to sellers that you are a highly qualified buyer with verified financing tailored to their exact listing. Having this document makes your offer significantly more competitive in tight markets, as it reduces the risk of the loan failing during the final underwriting stage.

Conditional Pre-Approval Letter for Specific Address

A Conditional Pre-Approval Letter for a Specific Address is a document from a lender verifying that a buyer is qualified to purchase a particular property. Unlike a general pre-approval, it accounts for property-specific costs like taxes, insurance, and HOA fees. This letter strengthens an offer by demonstrating to sellers that the buyer's financing is tailored to their home's exact price and requirements. It provides a competitive advantage in bidding wars by confirming the lender has already vetted the property's financial feasibility for the borrower's specific loan profile.

Conventional Loan Specific Property Pre-Approval Letter

A Conventional Loan Specific Property Pre-Approval Letter is a formal document from a lender verifying a buyer's qualification for a particular home address. Unlike a general pre-approval, it reflects the specific property's taxes, HOA fees, and insurance costs to ensure the debt-to-income ratio remains acceptable. This letter demonstrates financial credibility to sellers, proving the buyer is fully vetted for that exact purchase price. It strengthens an offer by showing the lender has already accounted for property-specific expenses, reducing the risk of financing contingencies failing during the closing process.

Federal Housing Administration Specific Address Pre-Approval Letter

A Federal Housing Administration (FHA) Specific Address Pre-Approval Letter is a critical document confirming a lender has verified your financial profile for a particular property. Unlike a general pre-approval, this property-specific letter ensures the home meets FHA safety and value standards while matching your approved loan amount. It demonstrates to sellers that you are a serious buyer with verified financing tailored to their home. Obtaining this letter is an essential step in the mortgage process to strengthen your offer in competitive real estate markets.

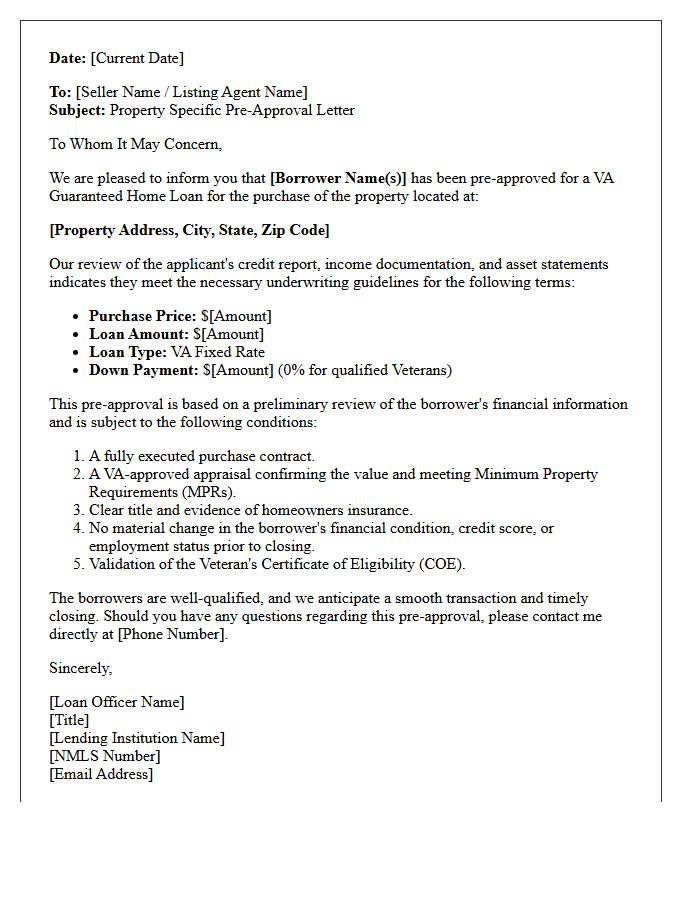

Veterans Affairs Home Loan Property Specific Pre-Approval Letter

A VA Property Specific Pre-Approval Letter is a formal document confirming a veteran's eligibility and creditworthiness for a specific home address. Unlike a general pre-approval, it verifies that both the veteran and the particular property meet Department of Veterans Affairs standards, including estimated taxes and insurance. This letter strengthens an offer by proving to sellers that the lender has already vetted the collateral, ensuring a faster closing process and higher certainty that the VA loan will be officially approved for that exact residence.

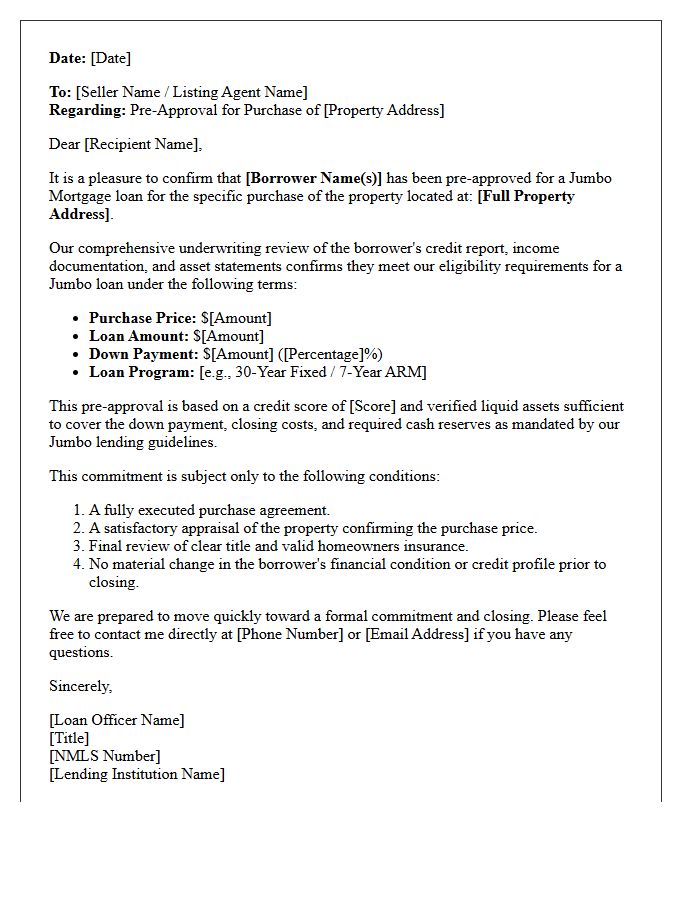

Jumbo Mortgage Specific Property Pre-Approval Letter

A Jumbo Mortgage Specific Property Pre-Approval Letter is a rigorous financial verification required for high-value real estate. Unlike general estimates, it confirms a lender's commitment to finance a defined luxury residence exceeding standard conforming loan limits. This document proves the buyer possesses the verified income, liquid reserves, and credit standing necessary for premium transactions. For sellers, it provides transactional security, ensuring the buyer can navigate the complex underwriting of a large-scale loan. Obtaining this specific letter is essential for making a competitive, credible offer in high-end housing markets.

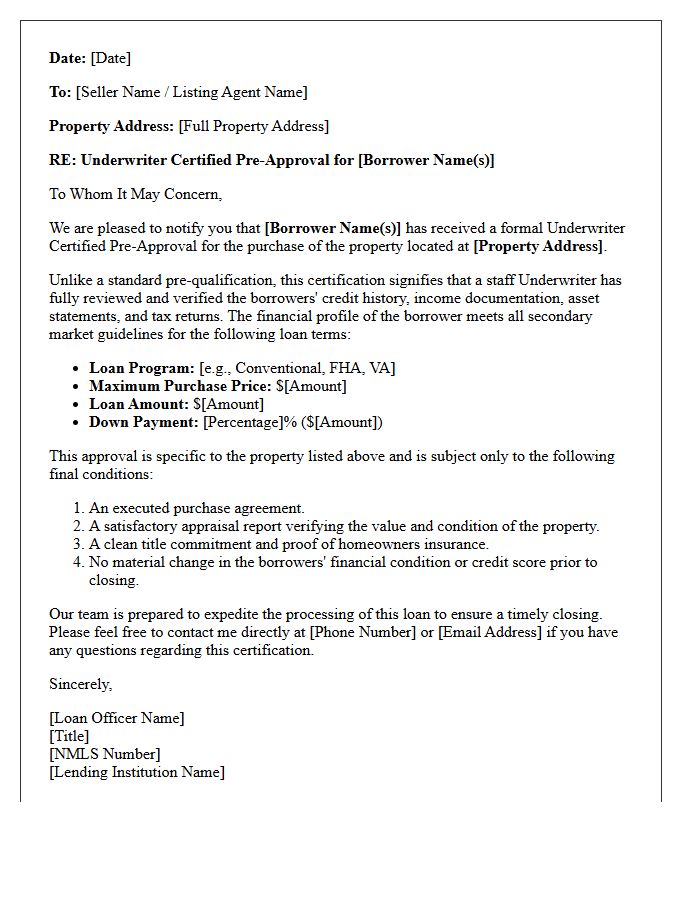

Underwriter Certified Specific Property Pre-Approval Letter

An Underwriter Certified Specific Property Pre-Approval Letter is the strongest form of financing commitment before a final loan approval. Unlike standard pre-approvals, a designated underwriter has already verified your income, assets, and credit. This document confirms you are fully cleared to purchase a particular address, making your offer nearly equivalent to cash. For sellers, it eliminates financing contingencies and minimizes risk, providing a competitive advantage in a crowded real estate market by ensuring the lender has already completed the rigorous mortgage underwriting process for that home.

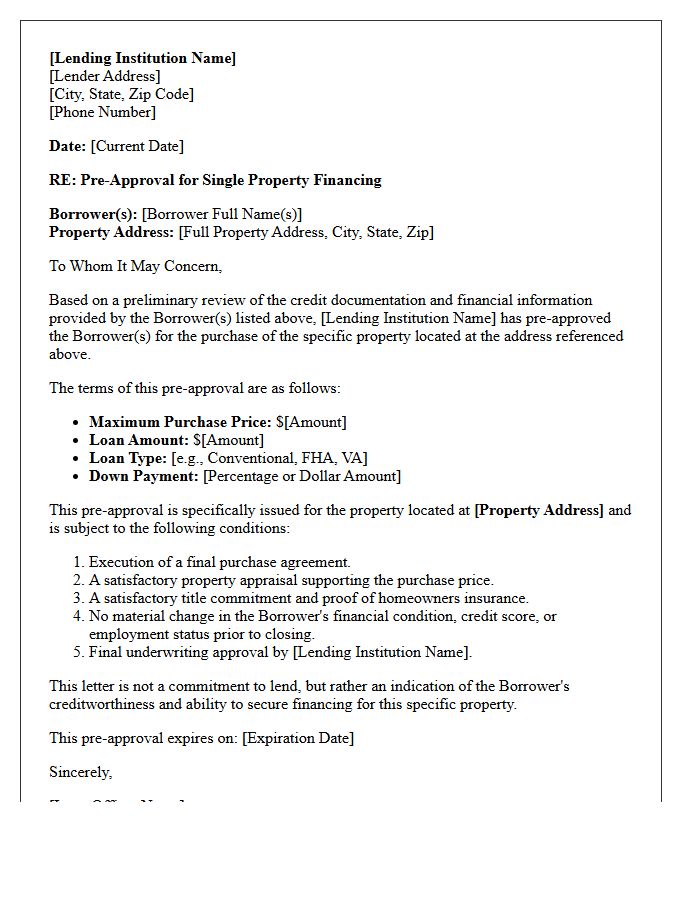

Single Property Address Financing Pre-Approval Letter

A Single Property Address Financing Pre-Approval Letter is a formal document issued by a lender verifying a buyer's eligibility to purchase a specific residence. Unlike a general pre-approval, this letter is property-specific, detailing the exact purchase price, loan amount, and address. This specificity demonstrates to sellers that the buyer has undergone rigorous financial underwriting for that particular home. It strengthens an offer in competitive markets by proving funding reliability and ensuring the mortgage terms align perfectly with the property's value and tax profile, minimizing the risk of closing delays.

Seller Directed Specific Address Pre-Approval Letter

A Seller Directed Specific Address Pre-Approval Letter is a specialized document issued by a lender for a single property. Unlike a general pre-approval, it matches the exact purchase price and address, demonstrating to the seller that the buyer is vetted specifically for their home. This targeted approach strengthens the offer in competitive markets by proving financial viability for that specific transaction. It prevents the seller from seeing the buyer's maximum budget, maintaining negotiation leverage while providing the necessary assurance to close the deal efficiently.

Verified Assets and Income Property Specific Pre-Approval Letter

A Verified Assets and Income Property Specific Pre-Approval Letter is a rigorous mortgage document that confirms a lender has fully vetted your financial documents. Unlike a basic pre-qualification, this letter signifies that your tax returns, pay stubs, and bank statements have undergone underwriter review. By detailing a specific property address, it demonstrates to sellers that you are a qualified buyer with guaranteed financing capacity for that exact purchase price. This provides a competitive advantage in real estate negotiations by ensuring financial credibility and a faster, more reliable closing process.

Appraisal Contingent Specific Property Pre-Approval Letter

An Appraisal Contingent Specific Property Pre-Approval Letter is a conditional financing guarantee tied to a unique address. Unlike general letters, it confirms a lender has verified your financial profile but includes a mandatory valuation requirement. This means the mortgage approval depends entirely on the home's appraised value meeting or exceeding the purchase price. If the property underperforms during the appraisal process, the loan amount may be reduced, requiring the buyer to cover the valuation gap or renegotiate terms to successfully close the real estate transaction.

United States Department of Agriculture Specific Property Pre-Approval Letter

A United States Department of Agriculture (USDA) Specific Property Pre-Approval Letter verifies that both the borrower and a particular address meet strict eligibility requirements. Unlike a general pre-qualification, this document confirms the home is located in a designated rural area and complies with safety standards. It provides sellers with certainty that the USDA loan underwriting process is nearly complete for that specific residence. Obtaining this letter is a critical final step to ensure the property qualifies for zero down payment financing before closing the real estate transaction.

Can I get a pre-approval letter for a specific property address?

Yes, lenders can issue a property-specific pre-approval letter. This document is often preferred by sellers because it demonstrates that the lender has vetted your finances specifically for the purchase price, taxes, and insurance costs associated with that exact home.

What details are included in a property-specific pre-approval letter?

A property-specific letter typically includes the exact property address, the specific offer price, the loan amount, the down payment percentage, and the expiration date of the credit approval. It shows the seller that you are qualified for their specific listing rather than a general price range.

Do I need a new pre-approval letter for every house I bid on?

While a general pre-approval letter works for many, most real estate agents recommend requesting a new, address-specific letter for each offer. This prevents the seller from knowing your maximum budget and ensures the figures align perfectly with your offer price.

How long does it take to get a pre-approval letter for a specific address?

If you are already pre-approved by your lender, generating an address-specific letter usually takes only a few minutes to a few hours. Most loan officers can quickly update your existing file with the property's tax and insurance data to provide the updated document.

Why do sellers prefer property-specific pre-approval letters?

Sellers prefer these letters because they prove the buyer's debt-to-income ratio has been calculated using the specific property's real estate taxes and HOA fees. It reduces the risk of the financing falling through due to high carrying costs unique to that home.

Comments