A Subject to Sale of Current Residence Pre-Approval Letter is a conditional financing statement issued by lenders. It confirms a buyer is qualified for a new mortgage, provided their existing home sells successfully. This document is essential for managing debt-to-income ratios during real estate transitions. To help you draft this professional document, below are some ready to use template.

Image cover: Home Purchase Contingent on Sale: Pre-Approval Letter Templates and Guide

Letter Samples List

- Standard Pre-Approval Letter Subject to Sale of Current Residence

- Contingent Home Sale Mortgage Pre-Approval Letter

- Subject to Sale Contingency Commitment Letter

- Verified Net Proceeds Subject to Sale Approval Letter

- Conditional Mortgage Pre-Approval Letter for Current Home Sale

- Outstanding Sale Contingency Pre-Approval Letter

- Underwriter Subject to Sale Clearance Letter

- Concurrent Closing Mortgage Pre-Approval Letter

- Pending Sale Contingent Mortgage Approval Letter

- Subject to Existing Property Sale Verification Letter

- Active Listing Subject to Sale Pre-Approval Letter

- Executed Contract Subject to Sale Approval Letter

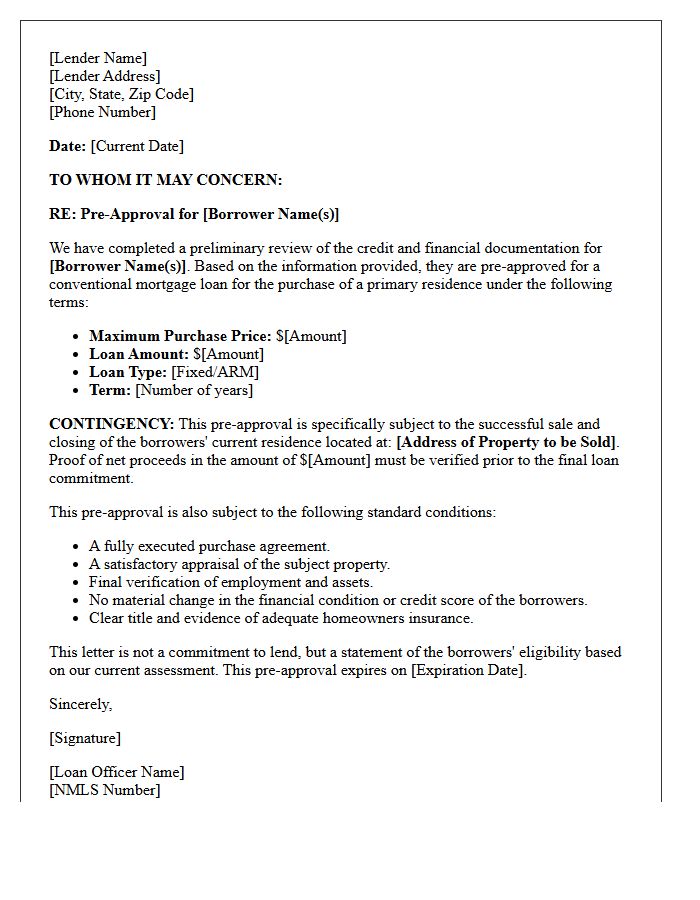

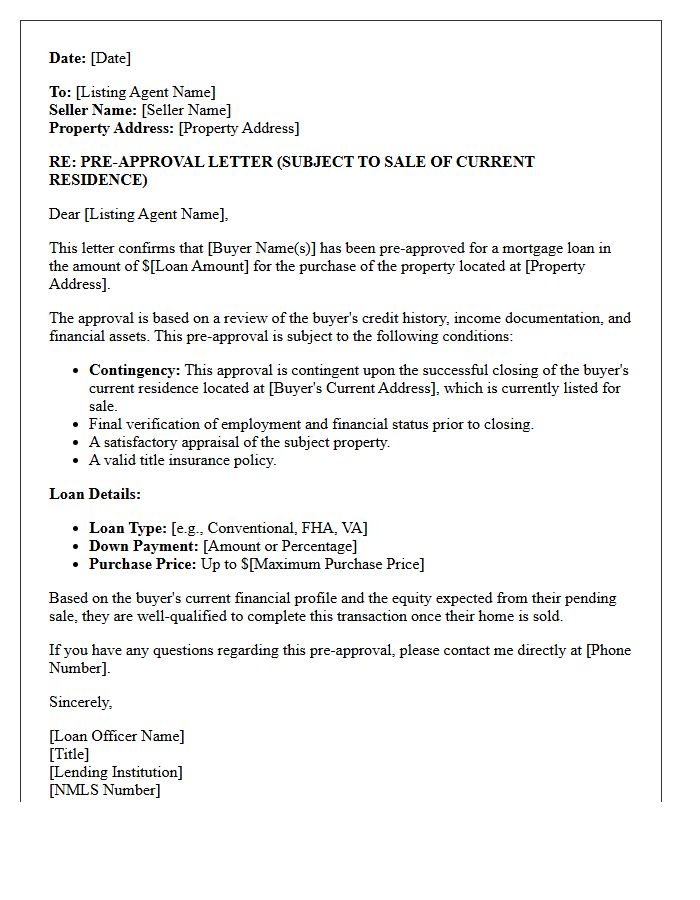

Standard Pre-Approval Letter Subject to Sale of Current Residence

A Standard Pre-Approval Letter Subject to Sale of Current Residence indicates a lender's conditional commitment to finance a new home. This contingency means the mortgage approval depends entirely on the successful liquidation of your existing property to secure necessary funds. While it confirms your creditworthiness, sellers often view these offers as higher risk because the deal relies on an outside transaction. To strengthen your position, ensure your current home is already under contract to minimize potential delays in the underwriting process.

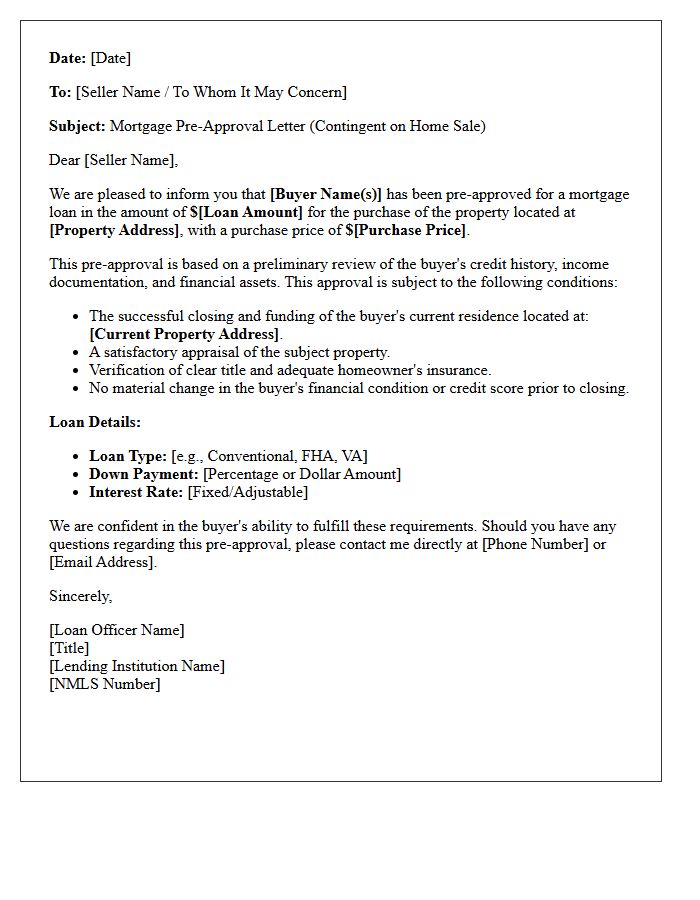

Contingent Home Sale Mortgage Pre-Approval Letter

A Contingent Home Sale Mortgage Pre-Approval is a conditional commitment from a lender, essential for buyers who must sell their current property to finance a new one. It verifies your creditworthiness while explicitly stating that final funding depends on the successful closing of your existing home. This document proves to sellers that you are financially prepared, though your offer carries higher risk. To strengthen your position, ensure your current residence is already under contract, as this reduces settlement uncertainty and makes your contingent bid more competitive in a crowded real estate market.

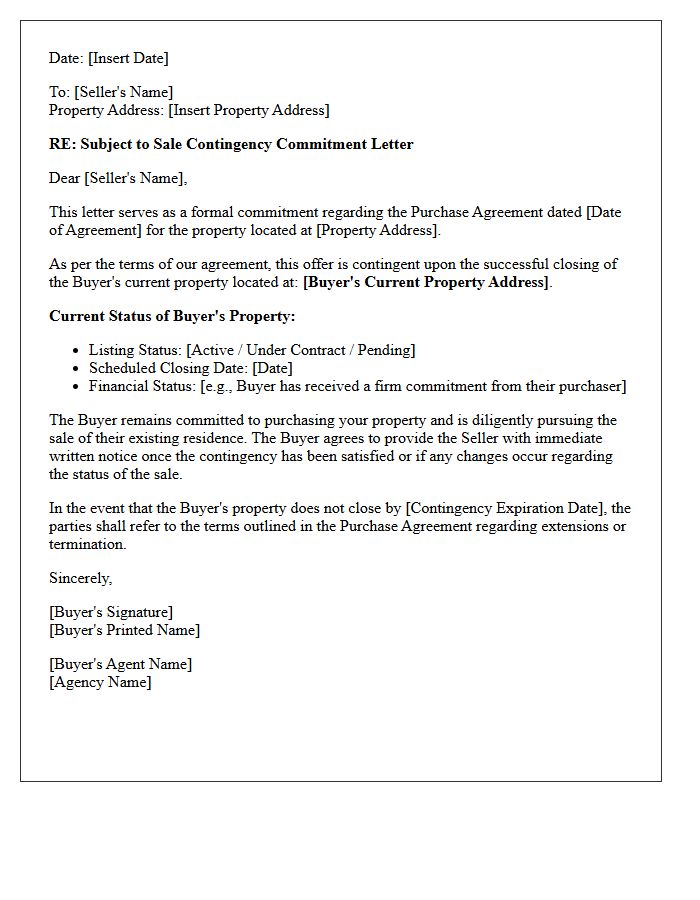

Subject to Sale Contingency Commitment Letter

A Subject to Sale Contingency Commitment Letter is a conditional mortgage approval issued when a buyer must sell their current residence to finance a new purchase. This document confirms the lender will provide financing only after the existing property is successfully sold and closed. It protects the lender's debt-to-income ratios while allowing buyers to bridge the gap between homes. Sellers often view this as a risk factor, as the transaction's success depends entirely on a third-party sale completing on schedule to satisfy the lender's final requirements.

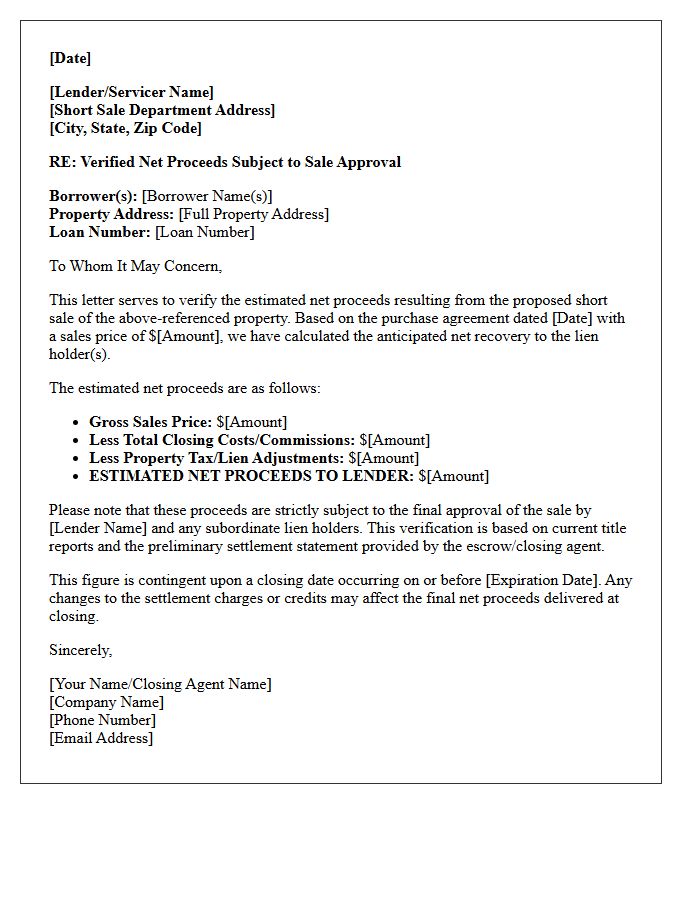

Verified Net Proceeds Subject to Sale Approval Letter

A Verified Net Proceeds Subject to Sale Approval Letter is a critical document in real estate transactions, confirming that a lender has reviewed and verified the estimated final payout to the seller. It ensures that all closing costs, liens, and mortgage balances are accounted for before finalizing a deal. This letter is vital for short sales, providing assurance to all parties that the transaction meets the lender's financial requirements for closing approval. Without this verification, the sale cannot legally proceed to the transfer of title.

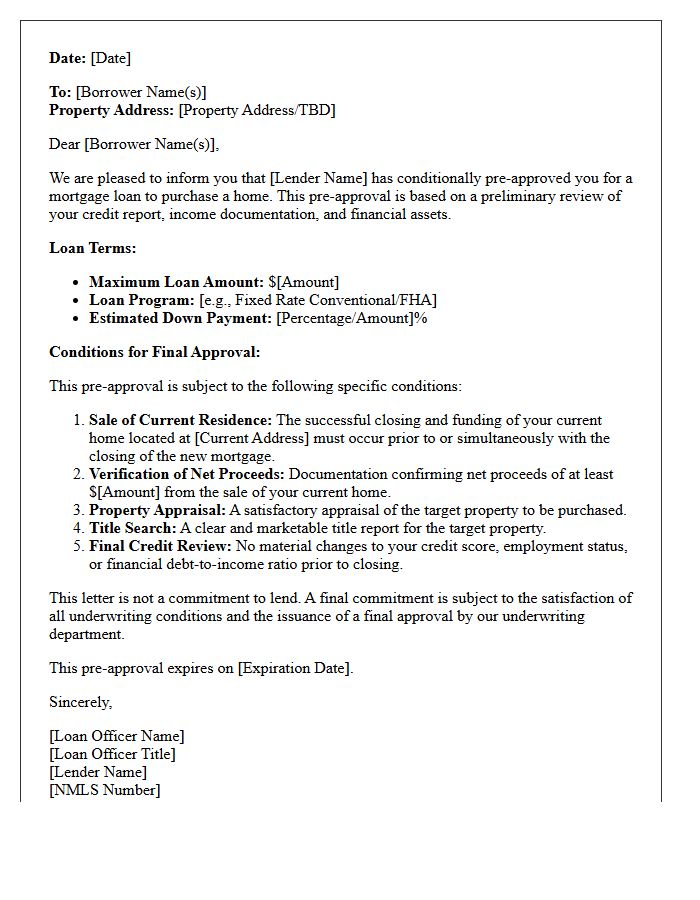

Conditional Mortgage Pre-Approval Letter for Current Home Sale

A conditional mortgage pre-approval is a critical document for buyers who must sell their existing property to finance a new purchase. This letter specifies that the lender's commitment depends on the successful closing of your current home sale. It provides sellers with assurance that your financing is solid, provided your equity is liquidated. Understanding this contingency is essential, as it impacts your negotiating power and ensures all parties are aware of the required timeline for a seamless real estate transition between two properties.

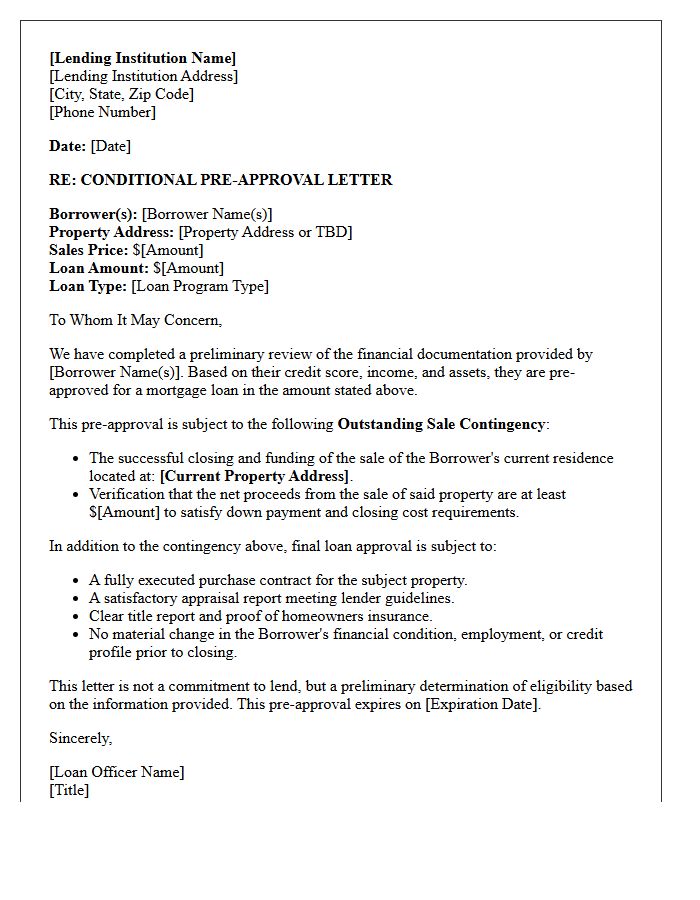

Outstanding Sale Contingency Pre-Approval Letter

An Outstanding Sale Contingency Pre-Approval Letter is a conditional financing commitment issued when a buyer must sell their current home before closing on a new one. It signals to sellers that the lender has verified the buyer's credit and income, but the final loan approval depends on the successful equity release from the pending sale. This document is essential for managing transactional timing and risk, though it may be viewed as less competitive than a non-contingent offer in fast-moving real estate markets.

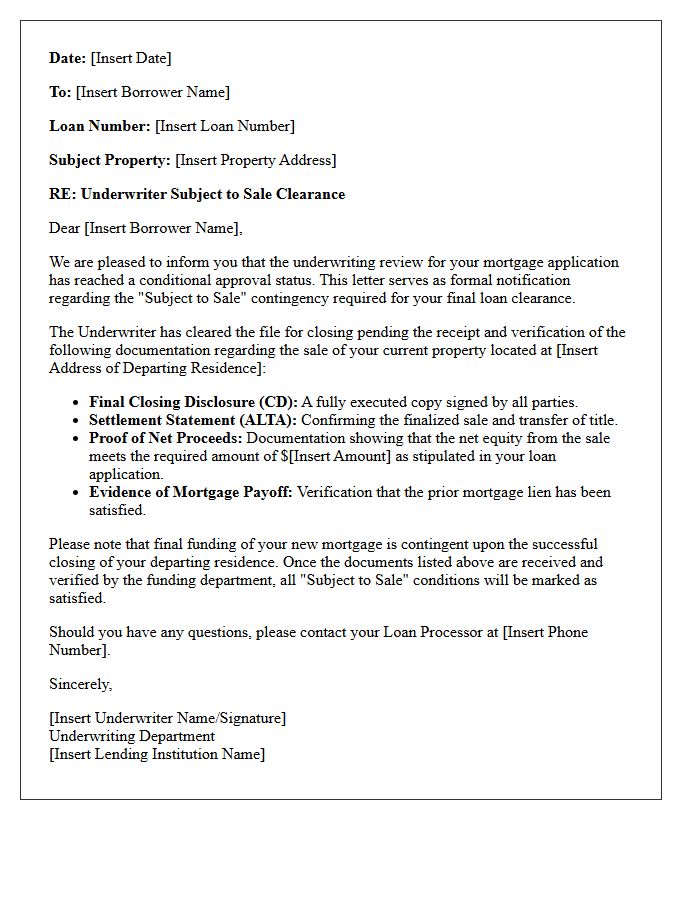

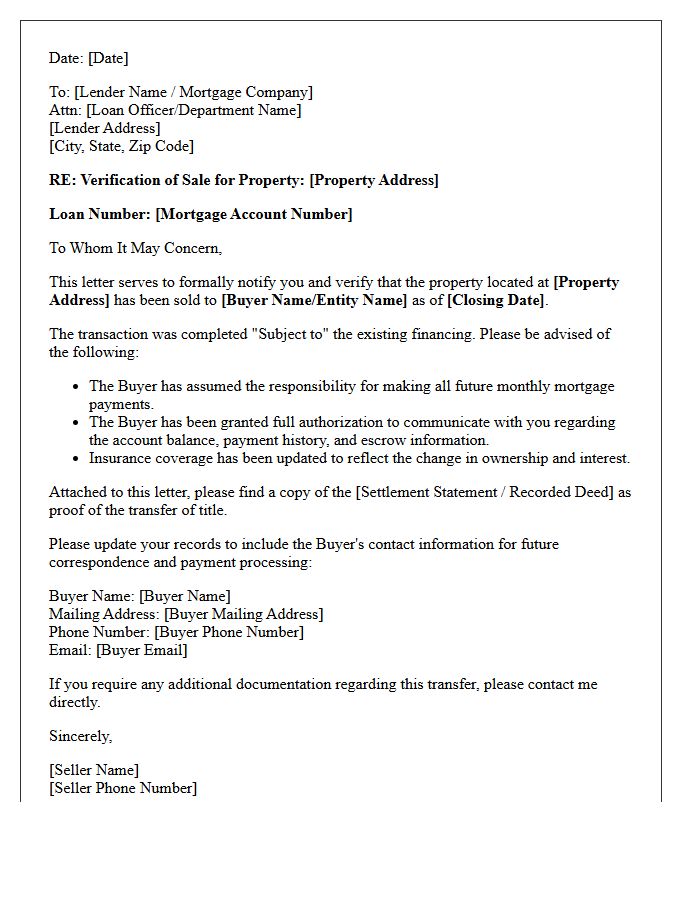

Underwriter Subject to Sale Clearance Letter

An Underwriter Subject to Sale Clearance Letter is a critical document confirming that a borrower's current property has been successfully sold and closed. Lenders issue this to verify that the net proceeds from the sale are available for the new purchase and that the previous mortgage debt is legally extinguished. This clearance is essential for meeting specific loan conditions, ensuring the borrower maintains the required debt-to-income ratio and sufficient liquidity to finalize the new mortgage transaction without financial contingency risks.

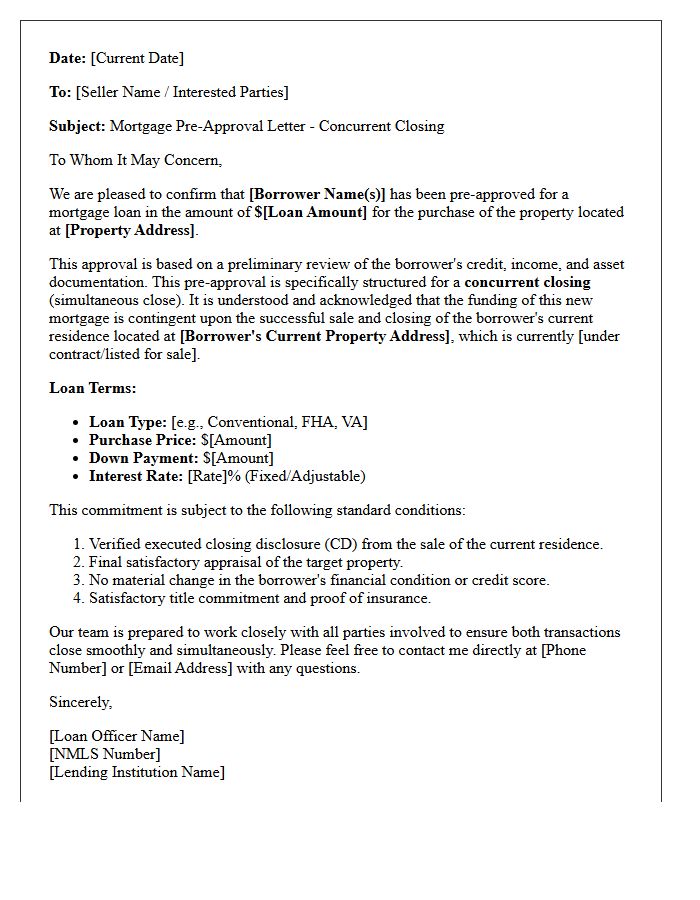

Concurrent Closing Mortgage Pre-Approval Letter

A concurrent closing mortgage pre-approval letter is a specialized document used when a buyer must sell their current home to finance a new purchase. It signifies that the lender has verified the borrower's financials, contingent upon the simultaneous settlement of both properties. This letter is crucial for sellers to evaluate risk, as it confirms the buyer's ability to perform depends on a successful linked transaction. Having this specific pre-approval strengthens your offer by demonstrating a clear, coordinated path to funding and closing coordination between both real estate deals.

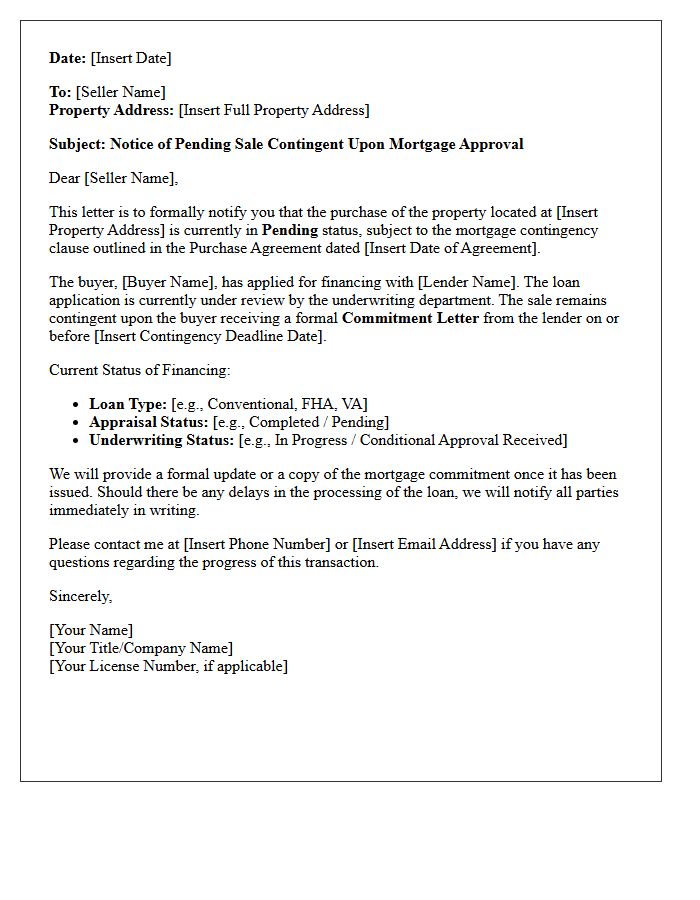

Pending Sale Contingent Mortgage Approval Letter

A pending sale contingent on mortgage approval indicates a seller has accepted an offer, but the transaction relies on the buyer securing a formal loan commitment. While a pre-approval starts the process, the final sale requires a mortgage approval letter issued after rigorous underwriting of the buyer's finances and the property's appraisal. If the lender denies the loan, the contingency clause allows the buyer to withdraw without penalty and recover their earnest money. This stage is a critical transition between an initial agreement and a legally binding closing.

Subject to Existing Property Sale Verification Letter

A Subject to Existing Property Sale Verification Letter is a crucial document used in real estate to confirm that a buyer has a pending sale on their current home. This letter provides financial certainty to sellers by verifying that the necessary equity for the new purchase is under contract. It typically outlines the closing date and contingency status of the previous property. Lenders require this verification to ensure the buyer can realistically manage the new mortgage, making it a vital component for transaction security in contingent offers.

Active Listing Subject to Sale Pre-Approval Letter

An active listing subject to sale with a pre-approval letter indicates the seller has accepted an offer contingent on the buyer selling their current home. The property remains active because the seller can still accept backup offers. For new buyers, providing a strong pre-approval letter is essential to demonstrate financial readiness if the initial contingency fails. This status offers a unique opportunity for secondary buyers to secure a home if the primary contingent contract collapses due to financing or sale issues, making it a critical window for competitive positioning.

Executed Contract Subject to Sale Approval Letter

An Executed Contract Subject to Sale Approval Letter is a legally binding agreement where the finalization depends on a third party's consent. This is most common in short sales or estate settlements where a lender or court must authorize the purchase price. While both buyer and seller have signed, the deal remains contingent until formal validation is received. Understanding this timeline is crucial, as the approval process can introduce significant delays, meaning the contract is not fully enforceable until the specific approval letter is issued and delivered to all parties.

What is a "Subject to Sale of Current Residence" pre-approval letter?

This is a conditional mortgage pre-approval issued to a homebuyer who needs the net proceeds from the sale of their existing home to qualify for a new mortgage. It confirms that the lender will provide financing once the borrower's current residence is successfully sold and closed.

How does a subject to sale contingency affect my home offer?

Including this letter with an offer informs the seller that your purchase depends on your current home selling first. While it demonstrates financial readiness, it is considered a "contingency," meaning the seller may view your offer as higher risk compared to non-contingent buyers.

Can I get pre-approved if my current home isn't on the market yet?

Yes, lenders can issue a preliminary pre-approval letter based on your projected home equity. However, most sellers will require the letter to state that your current home is at least listed on the MLS or currently under contract before they will accept a contingent offer.

Do I need a subject to sale letter if I have enough income for two mortgages?

If your Debt-to-Income (DTI) ratio allows you to carry both your current mortgage and the new mortgage simultaneously, you do not need a subject to sale pre-approval. In this case, you can obtain a standard pre-approval and buy your new home before selling the old one.

What happens if my current home fails to sell by the closing date?

If your pre-approval is strictly subject to the sale of your residence and the sale falls through, the lender will not fund the new loan. This usually allows you to exit the purchase contract via the financing or sale contingency, provided the agreement was structured correctly by your real estate agent.

Comments