Streamline your hiring process with an Independent Contractor Pre-Qualification Letter. This essential document ensures vendors meet your specific safety, insurance, and professional standards before work begins. Using a standardized vetting process minimizes legal risks and guarantees project quality. To help you get started quickly, below are some ready to use template options tailored for your business needs.

Image cover: Winning the Bid: Professional Independent Contractor Pre-Qualification Templates

Letter Samples List

- Standard Independent Contractor Pre-Qualification Letter

- Self-Employed 1099 Earner Pre-Qualification Letter

- Freelance Professional Mortgage Pre-Qualification Letter

- Sole Proprietorship Home Loan Pre-Qualification Letter

- Bank Statement Program Pre-Qualification Letter

- Gig Economy Worker Mortgage Pre-Qualification Letter

- Two-Year Income Average Pre-Qualification Letter

- Single-Year Tax Return Pre-Qualification Letter

- First-Time Homebuyer Independent Contractor Pre-Qualification Letter

- Jumbo Loan Independent Contractor Pre-Qualification Letter

- Joint Applicant Self-Employed Pre-Qualification Letter

- Non-Qualified Mortgage Independent Contractor Pre-Qualification Letter

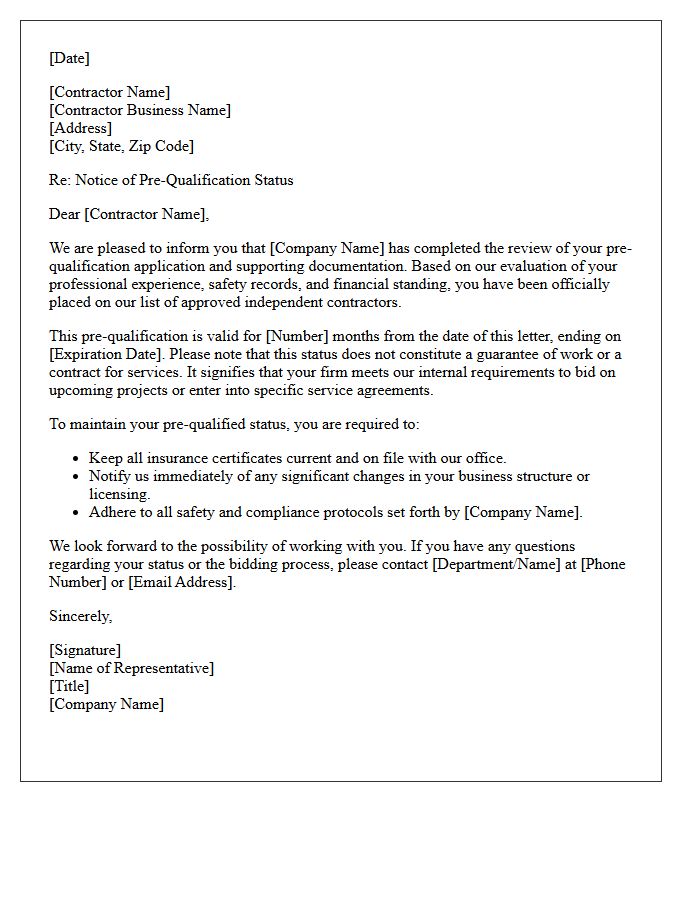

Standard Independent Contractor Pre-Qualification Letter

A Standard Independent Contractor Pre-Qualification Letter is a vital document used to verify the eligibility of external vendors. It ensures that a contractor possesses necessary liability insurance, valid business licenses, and tax documentation before beginning work. This due diligence process mitigates financial risk and confirms compliance with legal safety standards. By reviewing these credentials upfront, companies establish professional accountability and protect themselves from potential legal disputes. Always ensure the letter confirms the contractor's independent status to avoid misclassification issues with labor authorities and tax departments.

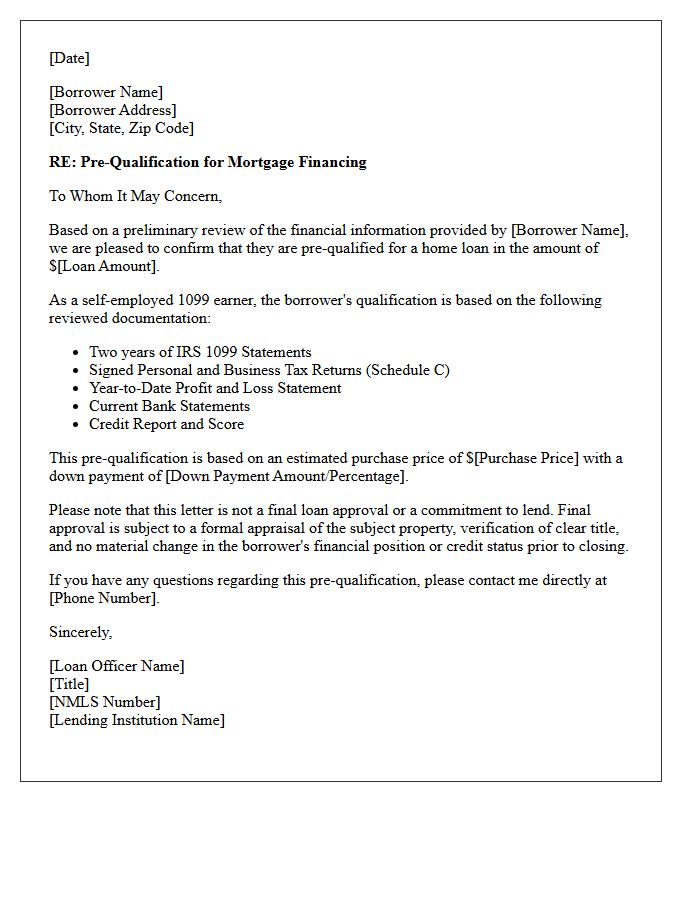

Self-Employed 1099 Earner Pre-Qualification Letter

A Self-Employed 1099 Earner Pre-Qualification Letter is a document from a lender estimating your borrowing power based on non-traditional income. Unlike W-2 employees, 1099 earners must provide bank statements or tax returns to verify cash flow stability. This letter is essential for proving financial credibility to home sellers. It demonstrates that a mortgage professional has reviewed your adjusted gross income and business write-offs to ensure you meet specific debt-to-income requirements. Securing this letter is the first critical step toward homeownership for independent contractors and freelancers seeking specialized loan programs.

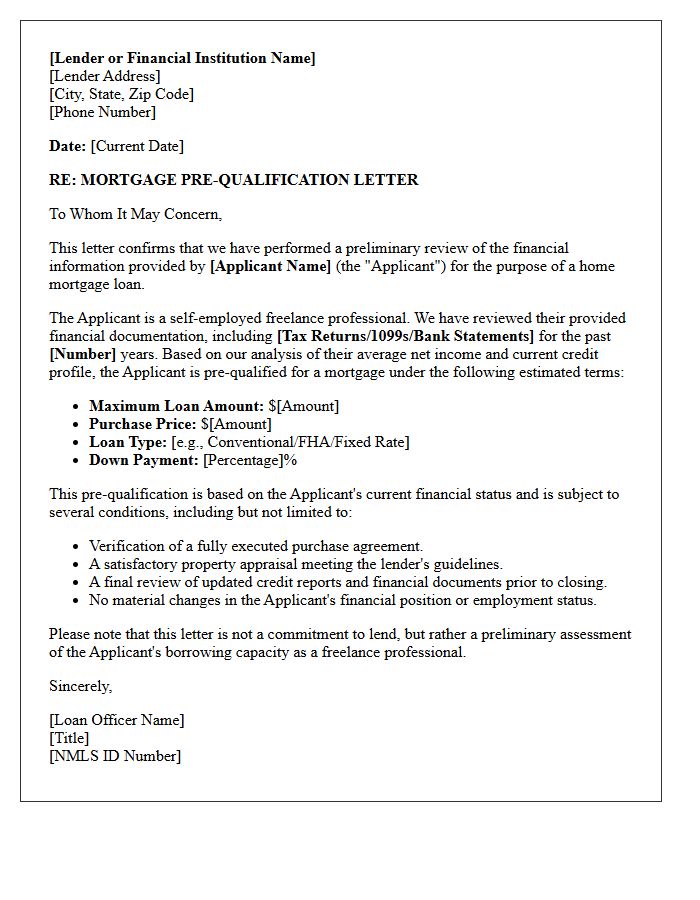

Freelance Professional Mortgage Pre-Qualification Letter

A Freelance Professional Mortgage Pre-Qualification Letter is an essential document that estimates your borrowing capacity based on self-employment income. Unlike traditional employees, freelancers must provide two years of tax returns and a profit and loss statement to verify earnings stability. This letter signals to sellers that a lender has reviewed your unique financial profile, including write-offs and 1099 history. Obtaining this initial assessment is a critical first step in the home-buying process, ensuring your freelance status meets specific lending criteria before you begin making formal offers on properties.

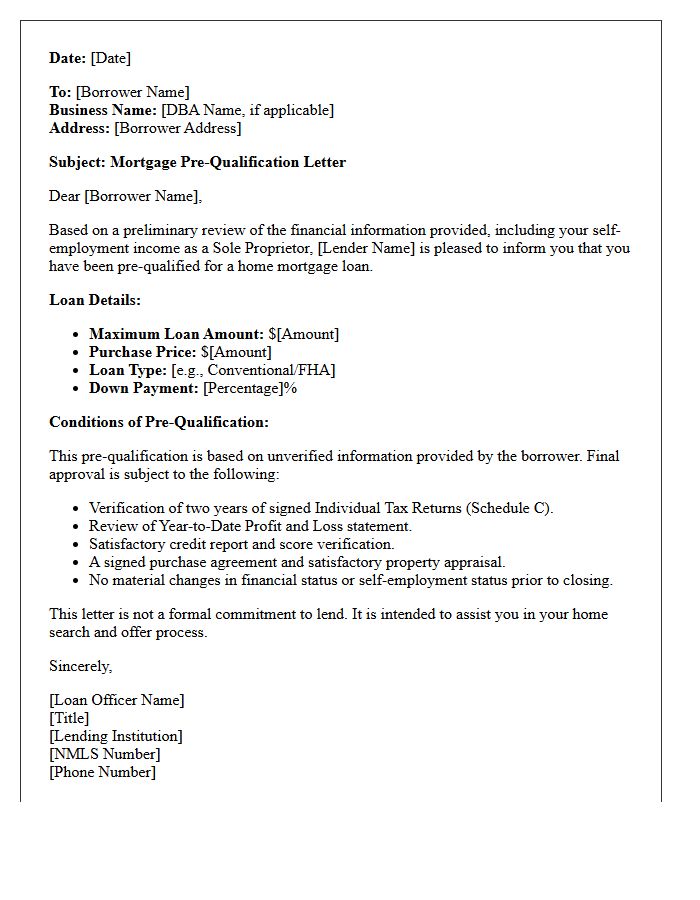

Sole Proprietorship Home Loan Pre-Qualification Letter

For a self-employed individual, a Sole Proprietorship Home Loan Pre-Qualification Letter is an essential document estimating your borrowing capacity based on self-reported financial data. Unlike W-2 employees, lenders focus heavily on your net profit rather than gross revenue. You must provide consistent tax returns (Schedule C) and bank statements to prove income stability. This letter serves as a preliminary eligibility indicator, signaling to sellers that you have the financial strength to secure a mortgage despite the complexities of independent business ownership and fluctuating cash flows.

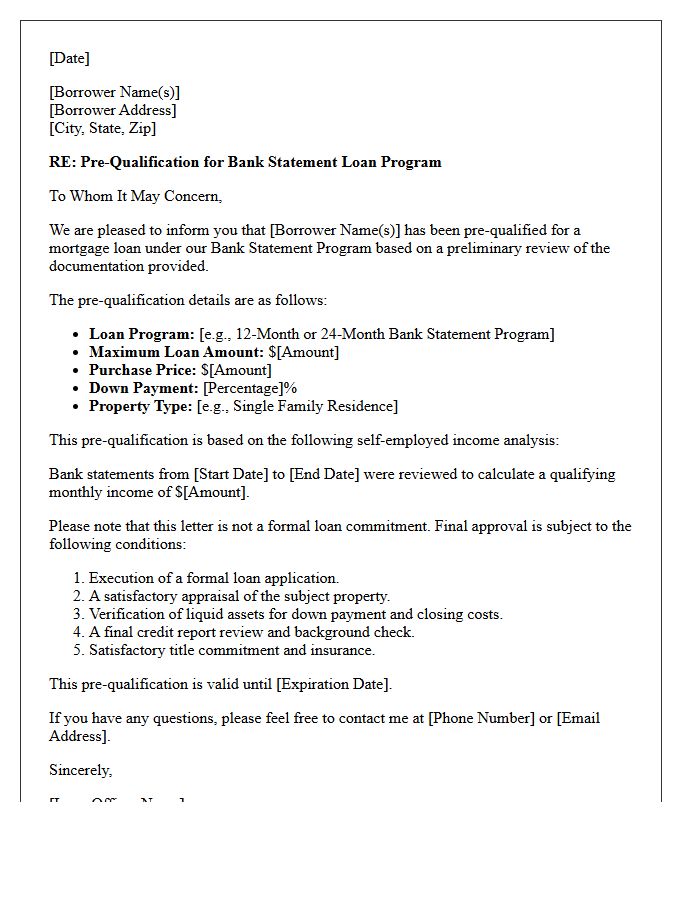

Bank Statement Program Pre-Qualification Letter

A Bank Statement Program Pre-Qualification Letter confirms that a self-employed borrower meets specific income requirements based on gross deposits rather than tax returns. This document serves as a preliminary approval, signaling to sellers that you have the necessary cash flow to secure a mortgage. To obtain one, lenders typically analyze 12 to 24 months of personal or business statements to calculate qualifying income. It is an essential tool for entrepreneurs looking to demonstrate creditworthiness and financial stability in a competitive real estate market without traditional documentation.

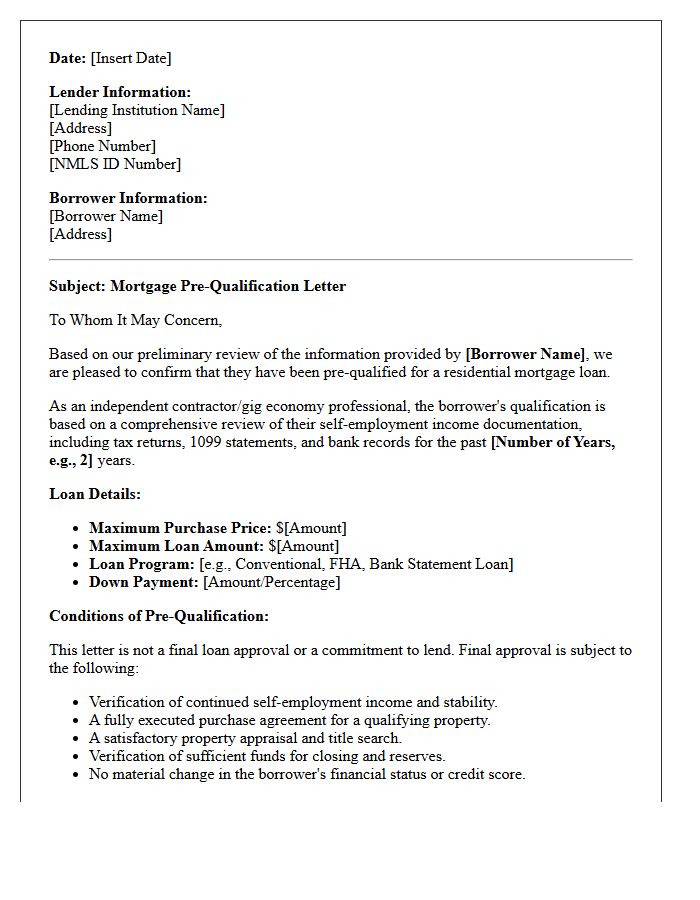

Gig Economy Worker Mortgage Pre-Qualification Letter

To secure a Gig Economy Worker Mortgage Pre-Qualification Letter, lenders prioritize stable income consistency over traditional employment contracts. Independent contractors should provide at least two years of tax returns (Form 1099s) and a current year-to-date profit and loss statement. High debt-to-income ratios can hinder approval, so minimizing personal liabilities is essential. Because freelance earnings fluctuate, underwriters focus on your net taxable income rather than gross revenue. Obtaining this letter early proves your financial credibility to sellers in a competitive real estate market.

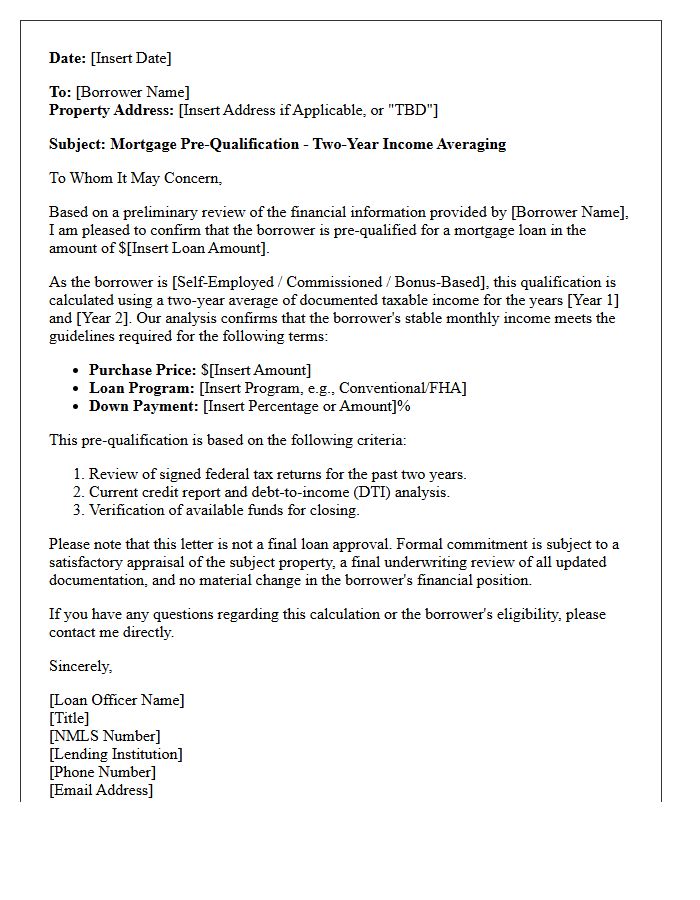

Two-Year Income Average Pre-Qualification Letter

A Two-Year Income Average Pre-Qualification Letter is essential for self-employed borrowers or those with variable pay like bonuses and commissions. Lenders analyze the mean earnings over a twenty-four-month period to ensure stable repayment capacity. This calculation offsets seasonal fluctuations, providing a more accurate reflection of your qualifying income. Maintaining consistent tax returns and documentation is vital, as significant declines in year-over-year earnings can negatively impact your maximum loan eligibility. This specialized letter confirms your financial readiness based on long-term historical performance rather than just current monthly gains.

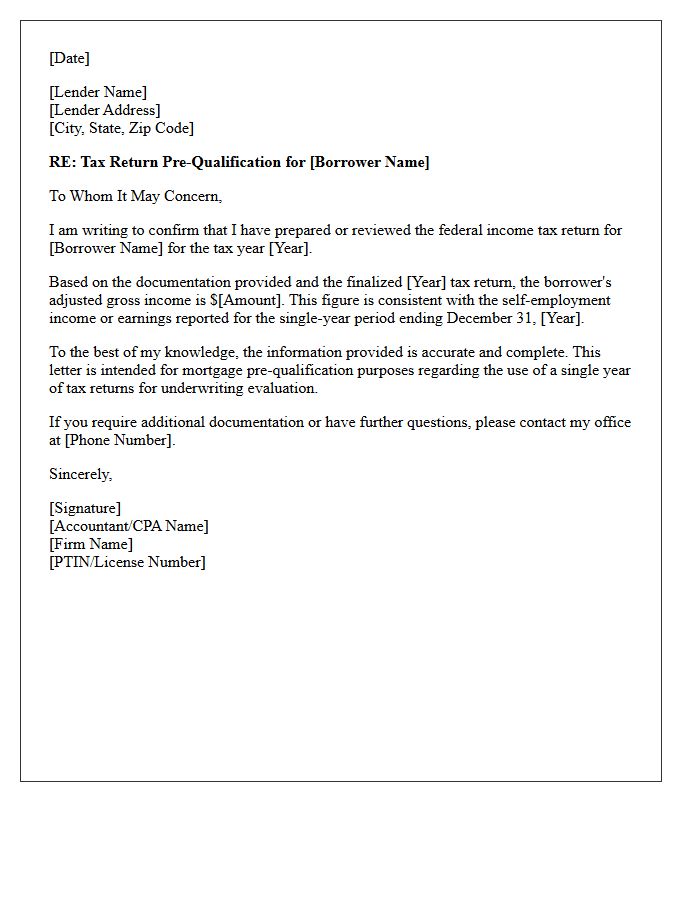

Single-Year Tax Return Pre-Qualification Letter

A Single-Year Tax Return Pre-Qualification Letter is a specialized document used by self-employed borrowers to secure mortgage financing. Unlike traditional loans requiring two years of history, this streamlined underwriting process evaluates income based solely on the most recent federal filing. It is essential for business owners who experienced a significant revenue increase or recently transitioned to self-employment. This letter confirms that a lender has verified your taxable income, providing a competitive edge when bidding on a home by demonstrating immediate financial stability and borrowing capacity.

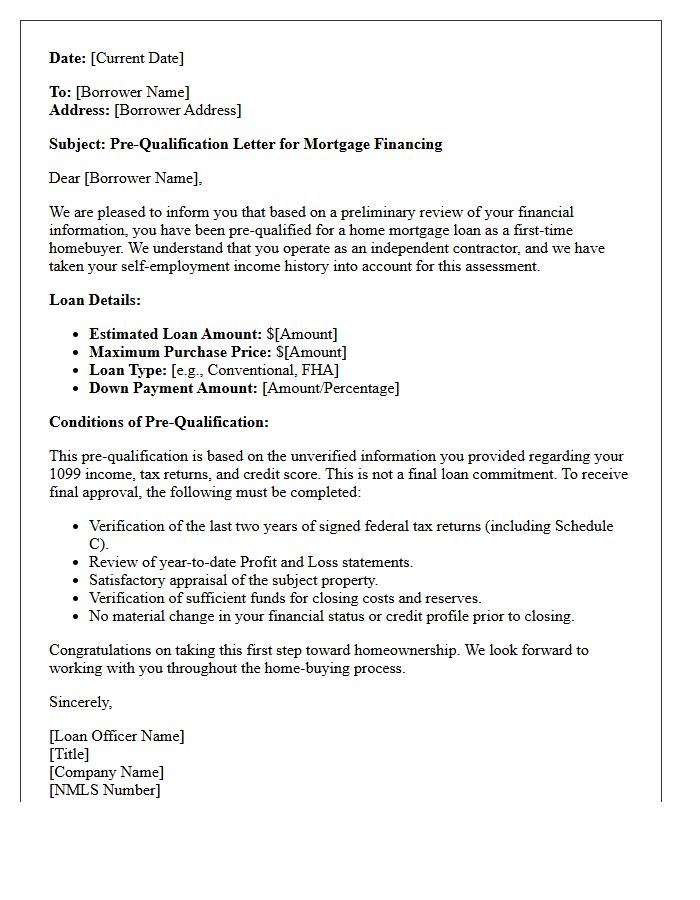

First-Time Homebuyer Independent Contractor Pre-Qualification Letter

Independent contractors seeking a pre-qualification letter must provide two years of consistent self-employment income documented via tax returns. Lenders calculate your qualifying earnings using your net profit after business expenses, not gross revenue. It is vital to minimize deductions in the years preceding your application to maximize your borrowing power. Additionally, maintaining a low debt-to-income ratio and a stable credit score is essential for first-time homebuyers. Consistent 1099 history or a steady Profit and Loss statement proves financial reliability to mortgage underwriters during the verification process.

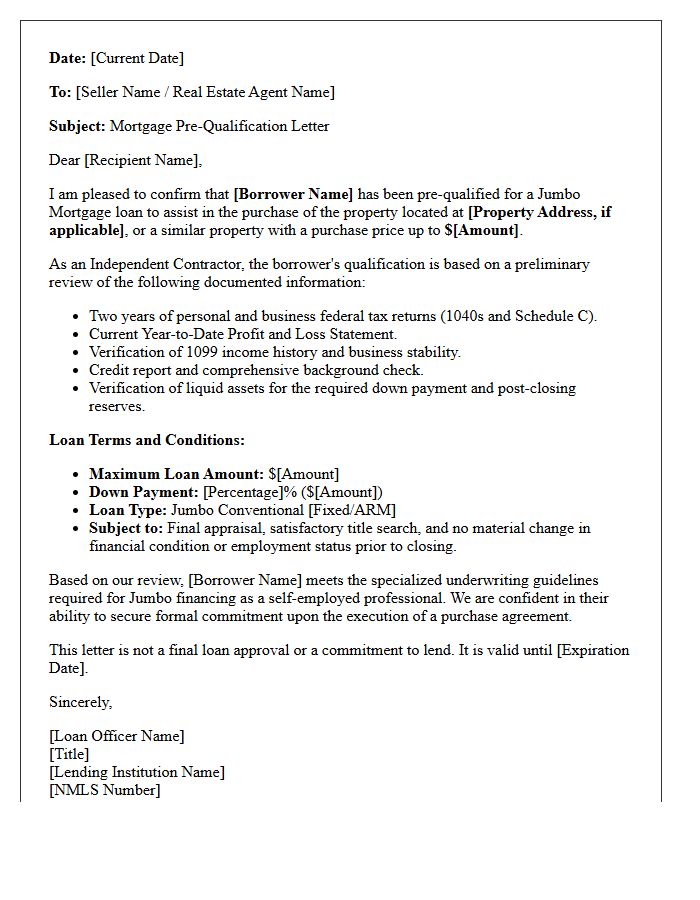

Jumbo Loan Independent Contractor Pre-Qualification Letter

To secure a Jumbo Loan as an independent contractor, obtaining a specialized Pre-Qualification Letter is essential. Lenders evaluate high-balance financing using two years of tax returns to calculate your qualifying income. Unlike standard mortgages, jumbo programs require meticulous asset verification and higher credit scores. This letter demonstrates your financial credibility to sellers, proving your business stability and cash reserves meet non-conforming loan standards. Ensure your documentation reflects consistent earnings to satisfy strict underwriting guidelines for luxury property investments.

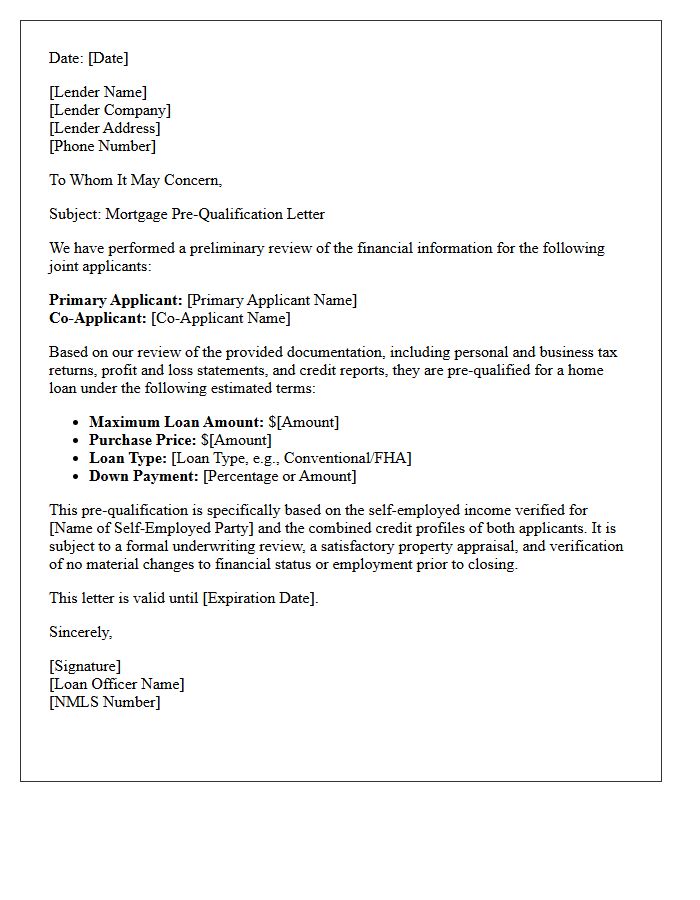

Joint Applicant Self-Employed Pre-Qualification Letter

When applying for a mortgage, a Joint Applicant Self-Employed Pre-Qualification Letter proves that combined incomes meet lending standards. Lenders rigorously verify net profit from tax returns rather than gross turnover for self-employed individuals. Both parties must provide comprehensive financial statements and 1099 forms to establish stability. This document is essential because it demonstrates mortgage affordability to sellers, confirming that the self-employed status and joint creditworthiness satisfy specific underwriting criteria for a successful home loan approval in a competitive real estate market.

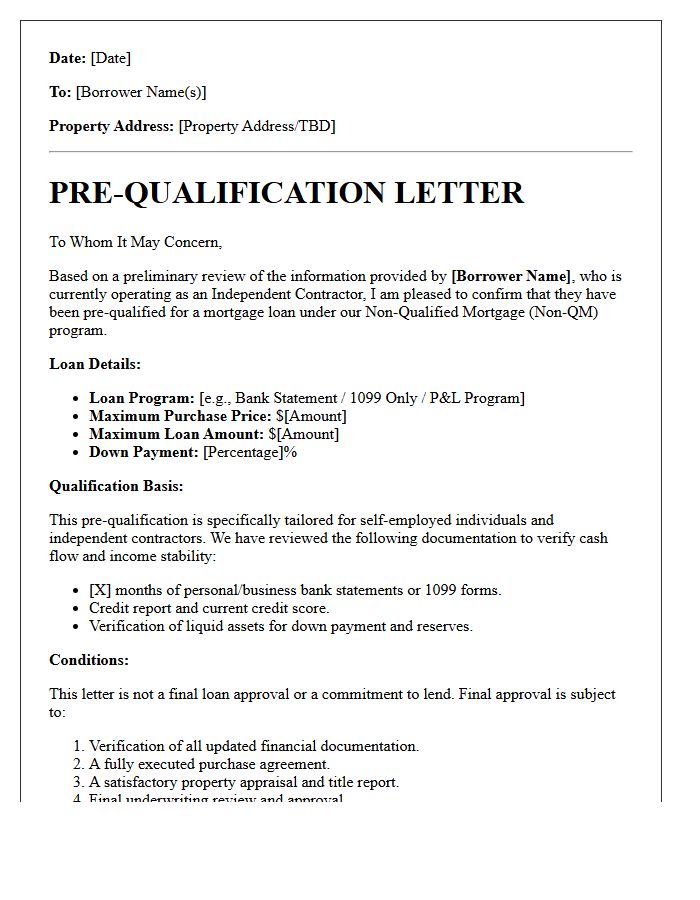

Non-Qualified Mortgage Independent Contractor Pre-Qualification Letter

A Non-Qualified Mortgage (Non-QM) Independent Contractor Pre-Qualification Letter verifies a self-employed borrower's borrowing power using alternative documentation. Unlike traditional loans, these Non-QM programs analyze bank statements or 1099 forms rather than tax returns to calculate qualifying income. This letter proves to sellers that a freelancer or contractor meets specific credit and liquidity requirements despite irregular pay cycles. It is a critical tool for independent workers to demonstrate financial credibility and secure a home loan in a competitive real estate market without standard W-2 employment verification.

What is an Independent Contractor Pre-Qualification Letter?

An Independent Contractor Pre-Qualification Letter is a formal document issued by a client or agency confirming that a contractor has met specific preliminary requirements-such as insurance coverage, tax compliance, and professional licensing-to perform work for a project.

Why do I need a pre-qualification letter as a freelancer?

This letter serves as a professional credential that verifies your business legitimacy. It streamlines the onboarding process, reduces liability risks for hiring entities, and demonstrates that you are prepared to meet contractual obligations before a formal agreement is signed.

What key information is included in a contractor pre-qualification document?

A standard letter typically includes the contractor's legal business name, Taxpayer Identification Number (TIN), proof of General Liability and Workers' Compensation insurance, professional certifications, and a statement of financial or operational capacity.

How does a pre-qualification letter differ from a signed contract?

A pre-qualification letter is a non-binding preliminary assessment of a contractor's eligibility to bid or be hired, whereas a signed contract is a legally binding agreement that outlines specific project scopes, payment terms, and delivery timelines.

Does a pre-qualification letter guarantee project approval?

No, receiving a pre-qualification letter indicates that you have passed the initial vetting process and meet the minimum safety and compliance standards, but it does not guarantee the awarding of a specific project or contract.

Comments