Securing a Vacation Home Pre-Qualification Letter is the essential first step in financing your secondary residence. This document estimates your borrowing power based on initial financial data, helping you compete in popular vacation markets and proving your seriousness to sellers. Understanding the requirements ensures a smoother mortgage process. To help you get started, below are some ready to use template.

Image cover: Secure Your Getaway: Vacation Home Pre-Qualification Letter Samples and Templates

Letter Samples List

- Standard Vacation Home Pre-Qualification Letter

- Conditional Vacation Home Pre-Qualification Letter

- Luxury Vacation Home Pre-Qualification Letter

- Out-Of-State Vacation Home Pre-Qualification Letter

- Joint Applicant Vacation Home Pre-Qualification Letter

- Self-Employed Borrower Vacation Home Pre-Qualification Letter

- High Net Worth Vacation Home Pre-Qualification Letter

- Investment Property Vacation Home Pre-Qualification Letter

- Short-Term Rental Vacation Home Pre-Qualification Letter

- Waterfront Vacation Home Pre-Qualification Letter

- Condominium Vacation Home Pre-Qualification Letter

- Updated Vacation Home Pre-Qualification Letter

- Expired Vacation Home Pre-Qualification Letter

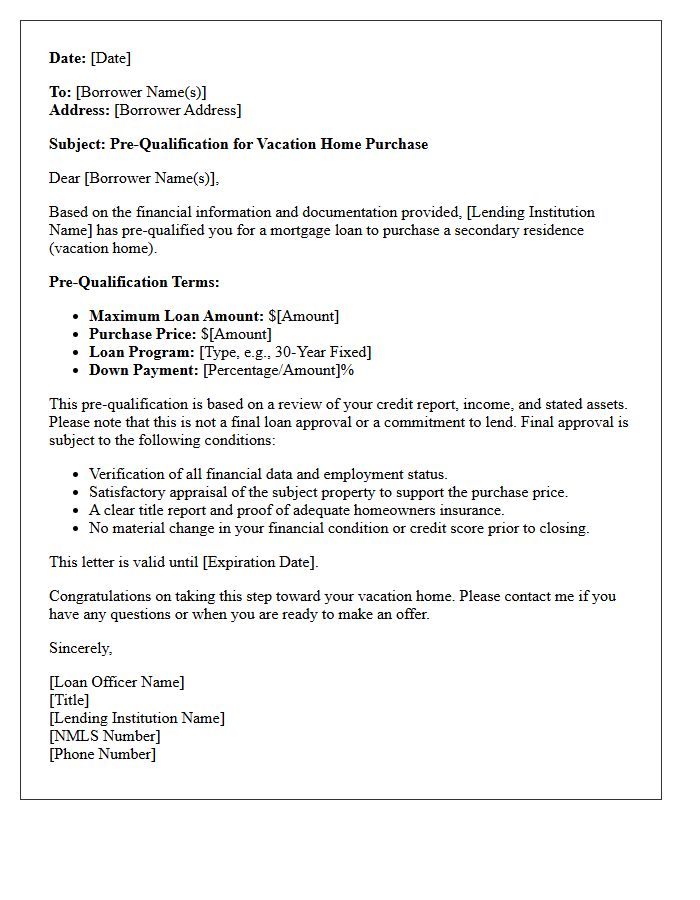

Standard Vacation Home Pre-Qualification Letter

A standard vacation home pre-qualification letter is an essential document proving a buyer's financial capacity to purchase secondary real estate. Unlike primary residences, lenders apply stricter debt-to-income ratios and higher credit score requirements for these properties. The letter confirms that a loan officer has reviewed your basic financial profile, including income and assets, to estimate a specific loan amount. Presenting this letter to sellers demonstrates serious intent and financial readiness, which is crucial for a competitive offer in popular vacation markets where high demand is common.

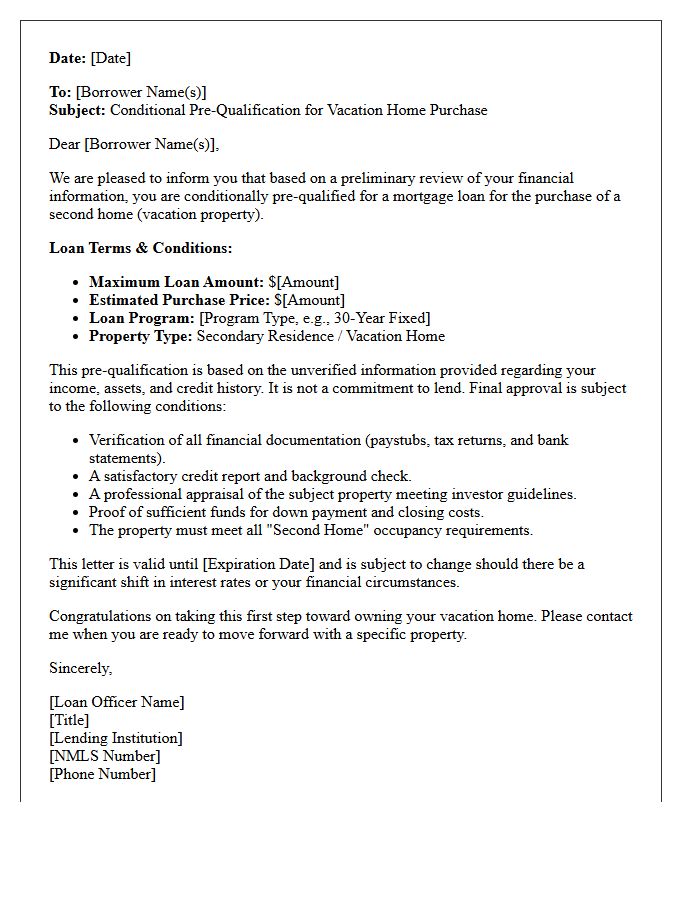

Conditional Vacation Home Pre-Qualification Letter

A Conditional Vacation Home Pre-Qualification Letter is a preliminary assessment by a lender indicating how much you can borrow for a secondary residence. Unlike primary homes, these loans often require higher credit scores and larger down payments. This document estimates your purchasing power based on unverified data, serving as a non-binding guide for your property search. It demonstrates to sellers that you are a serious buyer, but final approval depends on a full underwriting review of your actual financial documents, debts, and the specific property's eligibility.

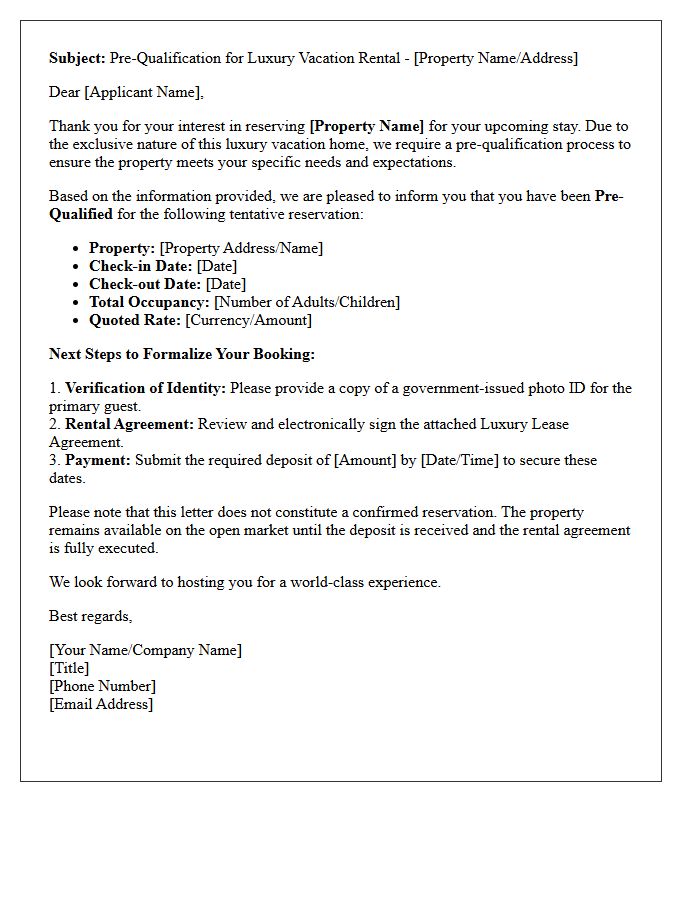

Luxury Vacation Home Pre-Qualification Letter

A luxury vacation home pre-qualification letter is an essential document that proves your financial credibility to sellers. It indicates that a lender has reviewed your basic income and assets to estimate your purchasing power. In the high-end market, most exclusive listings require this letter before granting property tours or considering offers. Obtaining one demonstrates you are a serious buyer capable of securing a jumbo loan or high-value mortgage, giving you a vital competitive edge when negotiating for premium real estate in sought-after destinations.

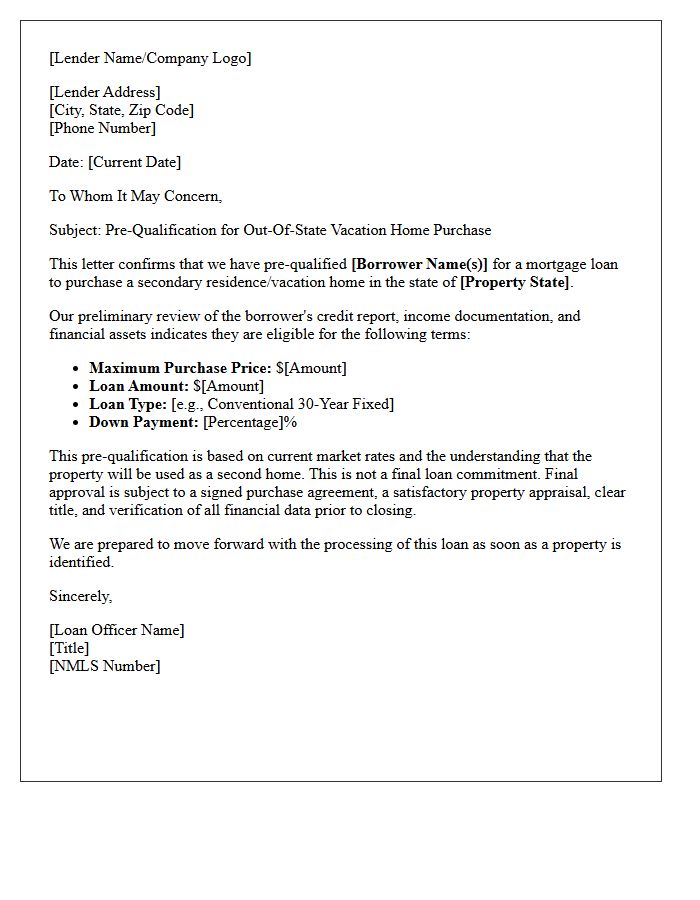

Out-Of-State Vacation Home Pre-Qualification Letter

Securing an out-of-state vacation home pre-qualification letter is the essential first step in your property search. Lenders evaluate your debt-to-income ratio differently for secondary residences compared to primary homes. It is vital to work with a lender licensed in the target state to ensure compliance with local regulations and tax laws. This document proves your financial credibility to sellers, giving you a competitive edge. Always confirm if your lender requires higher down payments or specific cash reserves for non-owner-occupied properties before making an offer on your getaway retreat.

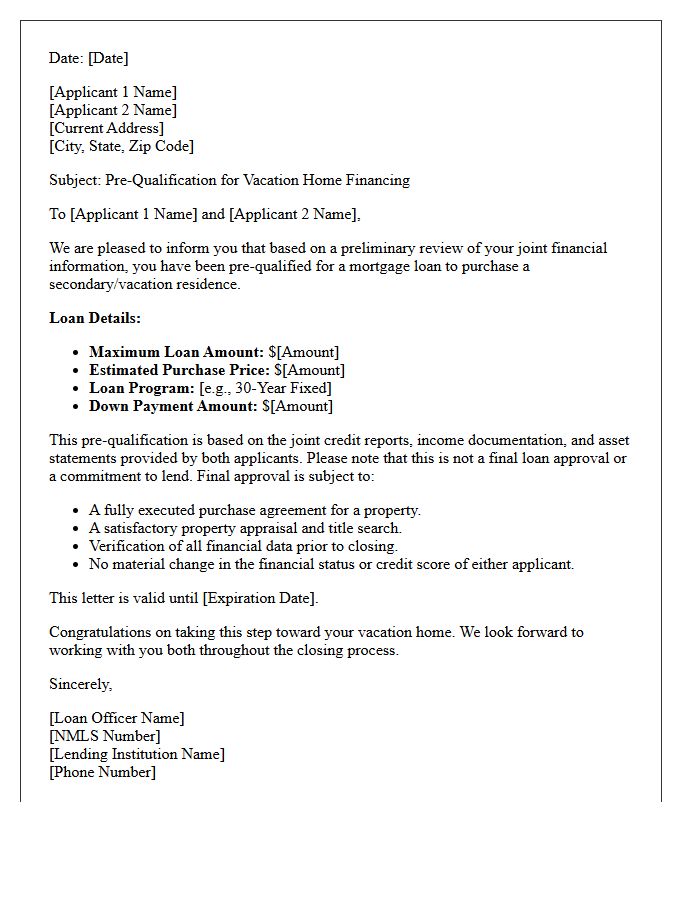

Joint Applicant Vacation Home Pre-Qualification Letter

A joint applicant vacation home pre-qualification letter estimates the combined borrowing power of two or more individuals seeking a secondary residence. Lenders evaluate the debt-to-income ratio and credit scores of all parties to determine loan eligibility. Since vacation homes often require higher down payments and stricter reserves, this document serves as financial proof for sellers. It demonstrates that the co-applicants meet specific lending criteria for non-primary properties, streamlining the negotiation process in competitive real estate markets while ensuring both borrowers are equally committed to the mortgage obligation.

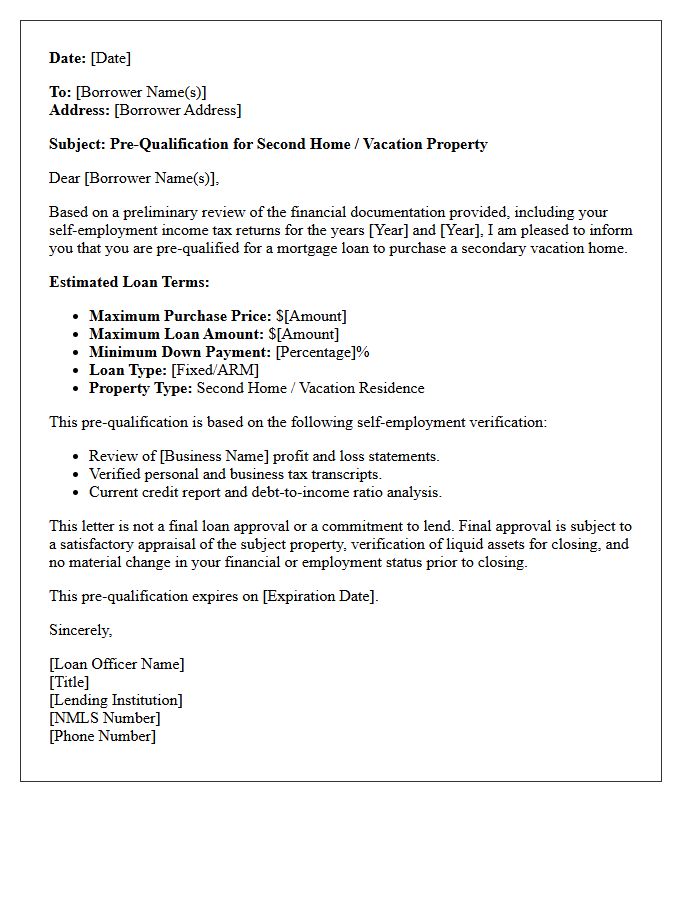

Self-Employed Borrower Vacation Home Pre-Qualification Letter

To secure a pre-qualification letter for a vacation home, self-employed borrowers must demonstrate stable income through two years of tax returns. Lenders scrutinize debt-to-income ratios carefully, as second homes often require higher credit scores and larger down payments than primary residences. Ensuring your Schedule C or corporate filings accurately reflect your net cash flow is essential for proving repayment ability. This document provides a competitive edge in real estate negotiations, signaling to sellers that your complex financial profile has been professionally vetted and meets specific mortgage underwriting criteria.

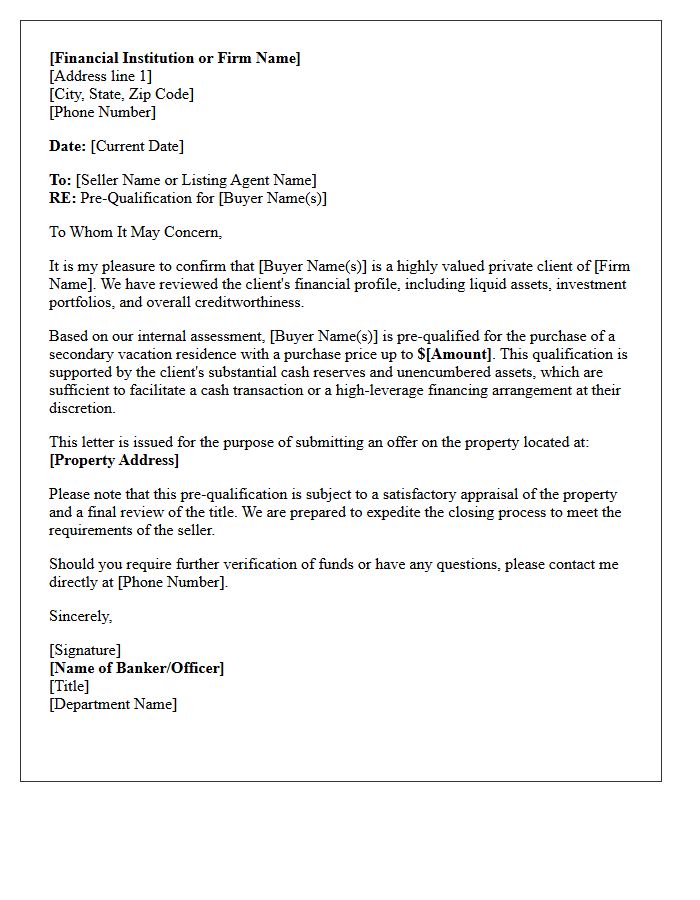

High Net Worth Vacation Home Pre-Qualification Letter

A high net worth vacation home pre-qualification letter serves as financial proof of your capability to acquire luxury real estate. Unlike standard approvals, this document validates liquidity and asset strength rather than just monthly income. It streamlines the buying process by assuring sellers of your credibility in competitive markets. Obtaining this letter requires a specialized lender who understands complex tax returns and portfolio-based underwriting. Having this documentation ready allows you to secure exclusive properties quickly, ensuring your purchasing power is recognized by elite real estate agents and sophisticated sellers alike.

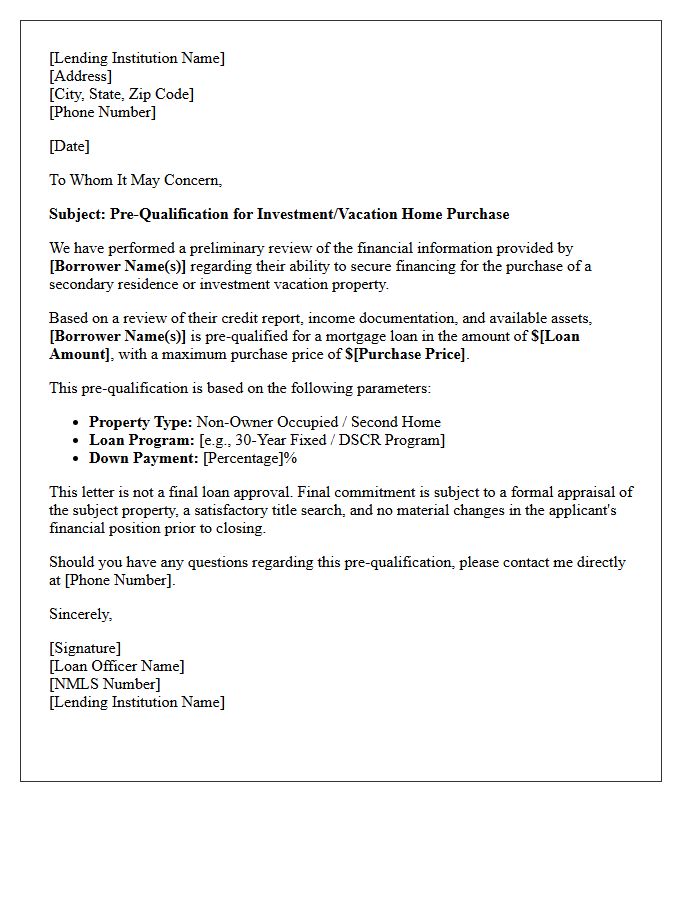

Investment Property Vacation Home Pre-Qualification Letter

Securing an Investment Property Vacation Home Pre-Qualification Letter is the essential first step in your real estate journey. This document confirms a lender's preliminary assessment of your creditworthiness and borrowing capacity based on unverified data. It demonstrates to sellers that you are a serious buyer capable of financing a secondary residence. Unlike a primary home, lenders may require higher credit scores and larger down payments. Obtaining this letter helps you establish a realistic budget, strengthening your negotiating position when making competitive offers in popular vacation markets.

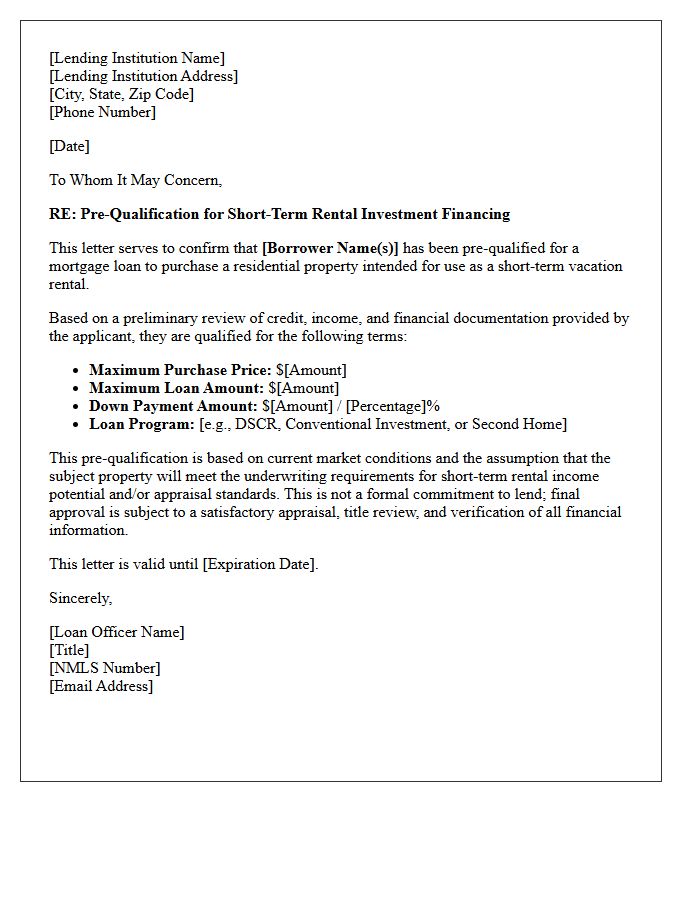

Short-Term Rental Vacation Home Pre-Qualification Letter

A short-term rental pre-qualification letter is a critical document proving a buyer's financial capability to purchase an investment property. Unlike standard home loans, this letter confirms that a lender has reviewed your credit, debt-to-income ratio, and potential rental income projections. Obtaining this document early streamlines the offer process, signaling to sellers that you are a serious investor. It ensures you understand your borrowing limit and specific loan terms tailored for vacation homes, which often require higher down payments and unique underwriting criteria compared to primary residences.

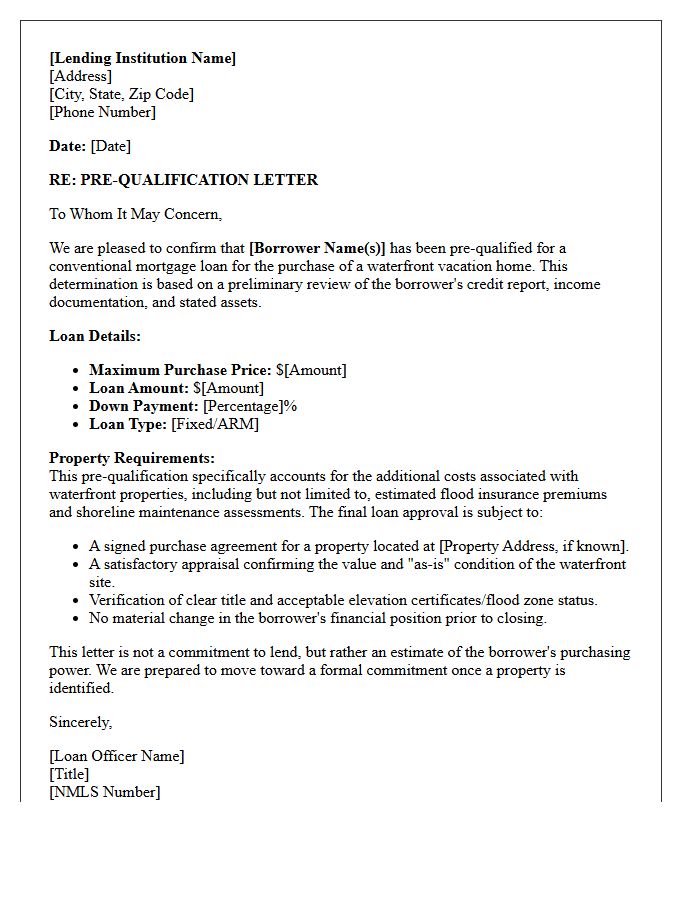

Waterfront Vacation Home Pre-Qualification Letter

A Waterfront Vacation Home Pre-Qualification Letter is an essential document from a lender estimating your borrowing capacity based on basic financial data. In the competitive coastal market, having this letter shows sellers you are a serious buyer with the necessary funding to close. It helps you focus on properties within your budget while strengthening your offer against competitors. Since waterfront financing often involves unique insurance and jumbo loan requirements, obtaining this initial assessment is the first step toward a successful shoreline investment.

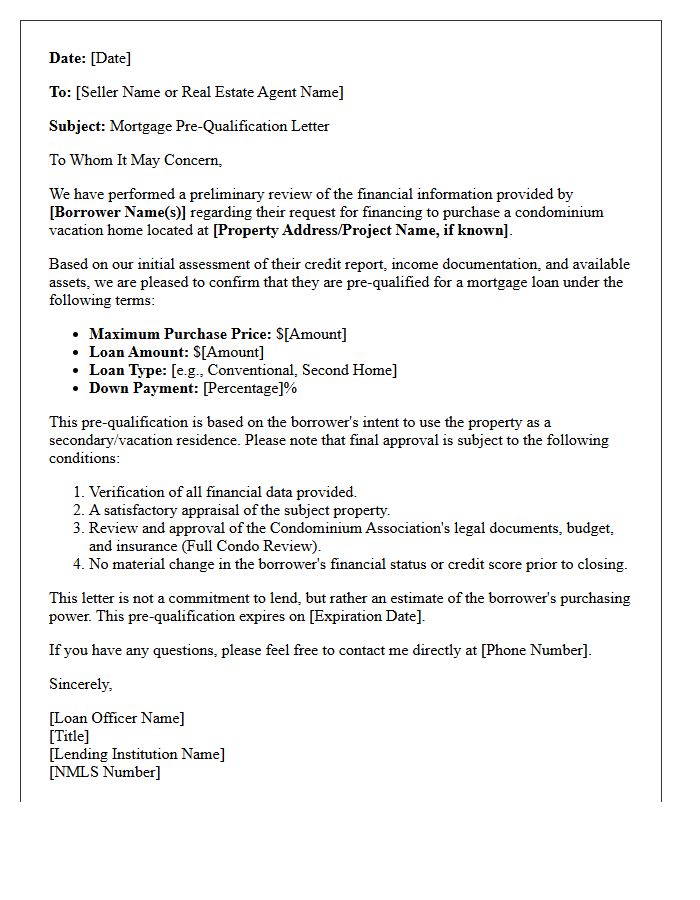

Condominium Vacation Home Pre-Qualification Letter

A Condominium Vacation Home Pre-Qualification Letter is an essential document from a lender confirming your eligibility to finance a secondary property. Unlike standard home loans, condotel financing often involves stricter guidelines regarding building warrants, rental pools, and down payment requirements. Obtaining this letter proves to sellers that you are a serious buyer who understands the specific lending criteria for non-warrantable units. It ensures your budget aligns with the unique homeowners association (HOA) fees and insurance costs associated with resort-style investments, streamlining the purchasing process in competitive markets.

Updated Vacation Home Pre-Qualification Letter

An updated vacation home pre-qualification letter is essential for proving your current financial credibility to sellers in a volatile market. Unlike standard approvals, this document confirms you meet specific secondary residence criteria, including higher credit score requirements and debt-to-income ratios. Because mortgage rates and lending guidelines fluctuate, having a recent letter ensures your purchasing power is accurately represented. Presenting a timely verification of your loan eligibility strengthens your offer, demonstrating that you are a serious buyer ready to secure a seasonal property or investment retreat immediately.

Expired Vacation Home Pre-Qualification Letter

An expired vacation home pre-qualification letter means your documented purchasing power is no longer valid. Mortgage rates and financial statuses change rapidly, requiring a current assessment of your debt-to-income ratio. To secure a secondary property, you must update your financial profile with a lender to reflect today's market conditions. Sellers will not accept offers backed by outdated documents, as they fail to prove your present ability to finance a non-primary residence. Always ensure your pre-qualification is active before submitting a competitive bid on a vacation property.

What is a vacation home pre-qualification letter?

A vacation home pre-qualification letter is a document from a lender estimating how much you can afford to borrow for a secondary residence based on an informal review of your credit, income, and assets.

How does a pre-qualification for a second home differ from a primary residence?

While the process is similar, lenders often require higher credit scores and larger down payments (typically 10-20%) for vacation home pre-qualification because secondary properties represent a higher risk than primary homes.

What information is needed to get a vacation home pre-qualification letter?

To receive a letter, you must provide your estimated annual income, total monthly debt obligations, available down payment funds, and permission for a soft credit pull to evaluate your debt-to-income ratio.

Does a pre-qualification letter guarantee I will get a vacation home loan?

No, a pre-qualification is an initial estimate. Final loan approval depends on a full underwriting process, including income verification, a hard credit check, and a professional appraisal of the specific vacation property.

How long is a vacation home pre-qualification letter valid?

Most vacation home pre-qualification letters are valid for 60 to 90 days. If your financial situation or market interest rates change significantly during this time, you may need to request an updated letter from your lender.

Comments