Securing a New Construction Pre-Qualification Letter is the essential first step in building your dream home. This document proves to builders and lenders that you are financially prepared for the unique costs of ground-up development. It strengthens your negotiating position and ensures a smoother financing process. To help you get started, below are some ready to use template.

Image cover: Expert New Construction Pre-Qualification Letter Templates and Proven Samples

Letter Samples List

- Standard New Construction Pre-Qualification Letter

- Conventional New Construction Pre-Qualification Letter

- Federal Housing Administration New Construction Pre-Qualification Letter

- Veterans Affairs New Construction Pre-Qualification Letter

- Jumbo Loan New Construction Pre-Qualification Letter

- Construction-To-Permanent Pre-Qualification Letter

- One-Time Close Construction Pre-Qualification Letter

- Two-Time Close Construction Pre-Qualification Letter

- Builder Preferred Lender Pre-Qualification Letter

- Custom Home Build Pre-Qualification Letter

- Spec Home Purchase Pre-Qualification Letter

- Lot And Construction Loan Pre-Qualification Letter

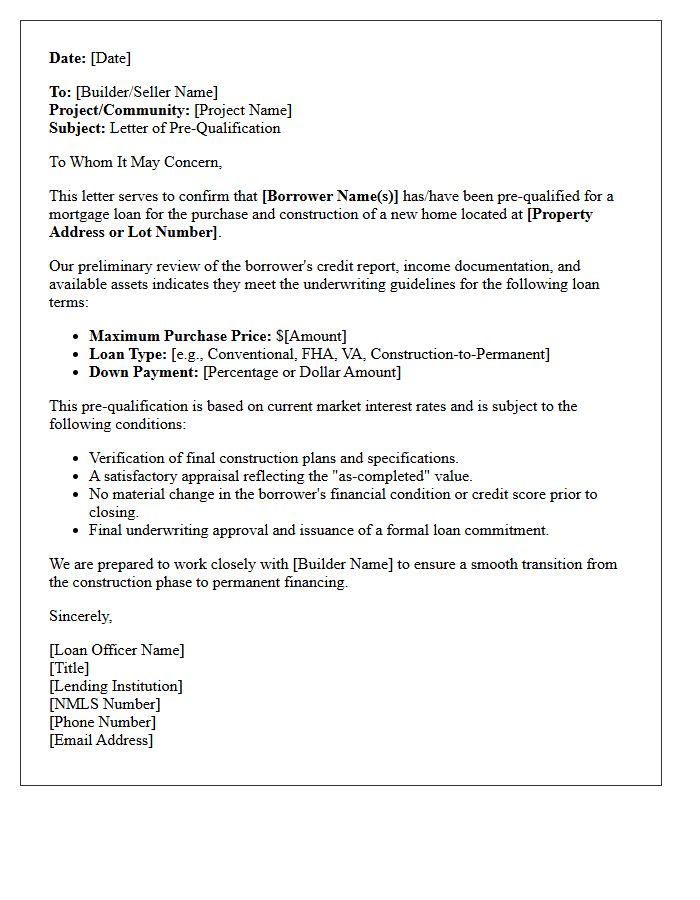

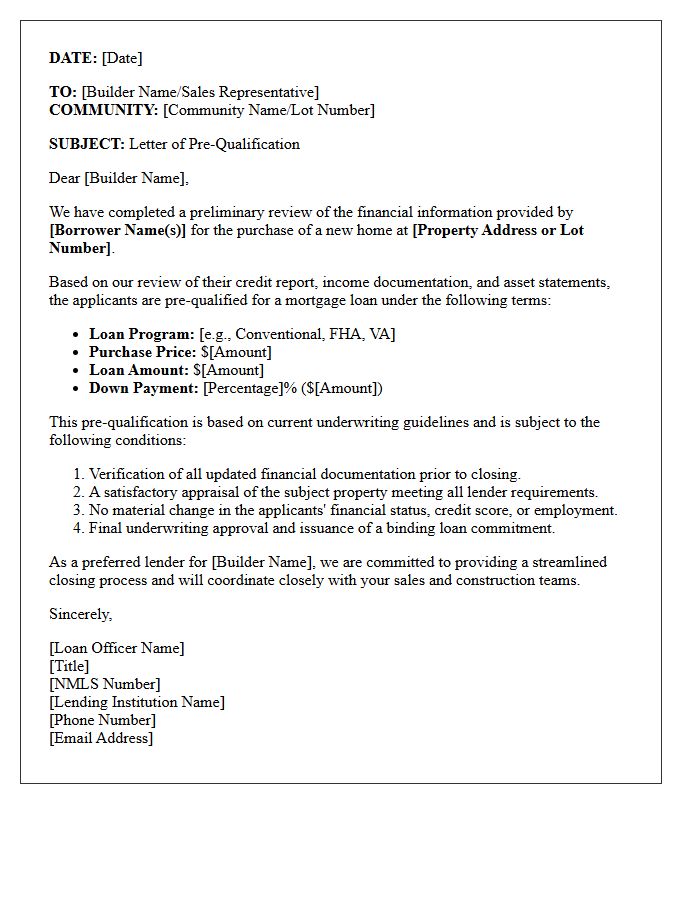

Standard New Construction Pre-Qualification Letter

A standard new construction pre-qualification letter is a document from a lender verifying a buyer's financial ability to secure a mortgage loan for a home build. Unlike typical resale letters, it specifically accounts for long-term interest rate fluctuations and construction-to-permanent financing requirements. Builders require this to ensure the buyer can afford the final purchase price upon completion. It demonstrates credibility, confirms the maximum loan amount, and highlights that the buyer has passed a preliminary credit and income analysis necessary to begin the building process with confidence.

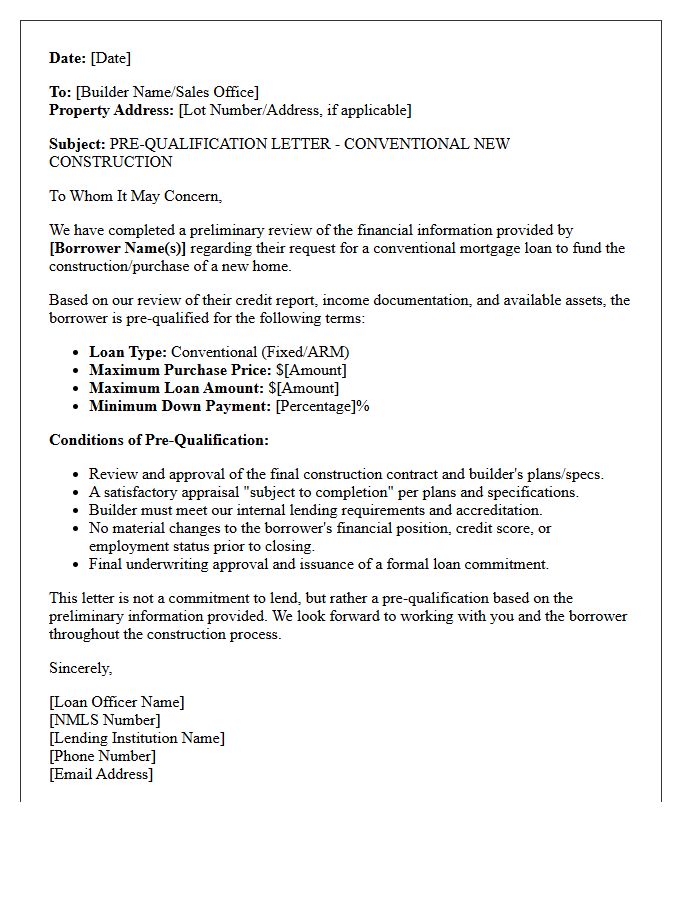

Conventional New Construction Pre-Qualification Letter

A Conventional New Construction Pre-Qualification Letter is a critical document proving a buyer's financial ability to fund a build-to-suit project. Unlike standard loans, lenders evaluate both the borrower's creditworthiness and the builder's viability. This letter ensures the builder that mortgage financing is secured before breaking ground. It typically requires a higher credit score and a stable debt-to-income ratio. Securing this commitment early protects your earnest money and streamlines the transition from a construction phase to a permanent mortgage upon home completion.

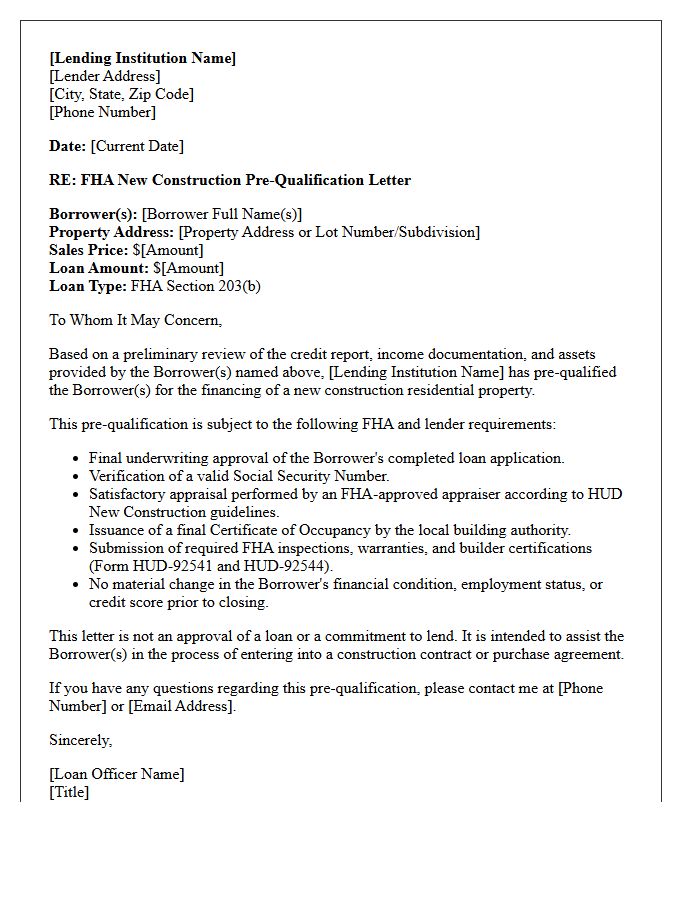

Federal Housing Administration New Construction Pre-Qualification Letter

A Federal Housing Administration (FHA) New Construction Pre-Qualification Letter is a crucial document for home buyers. It proves a lender has reviewed your finances and determined you meet the FHA loan requirements for a newly built home. This letter ensures builders that you have the necessary credit score and down payment capacity to secure mortgage financing. Unlike standard approvals, this pre-qualification specifically addresses FHA standards for inspections and builder certifications, making it a vital first step in the construction process to guarantee your financial eligibility before groundbreaking begins.

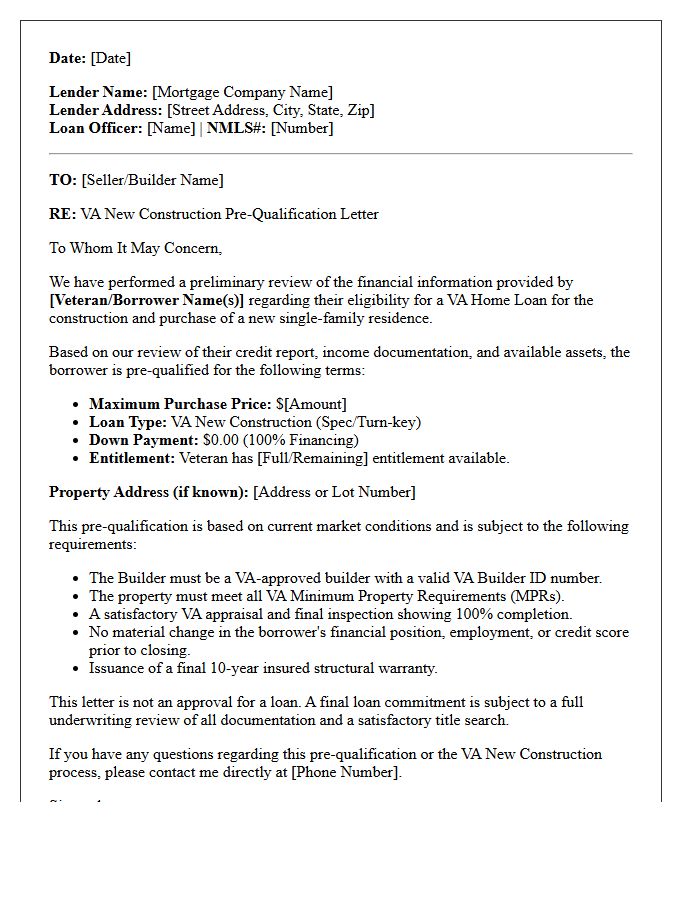

Veterans Affairs New Construction Pre-Qualification Letter

A Veterans Affairs New Construction Pre-Qualification Letter is a vital document confirming a lender's preliminary approval for a VA construction loan. This letter proves to builders that a veteran has the creditworthiness and entitlement necessary to fund both the land purchase and home building process. It outlines specific loan maximums and confirms that the lender specializes in the unique requirements of zero-down construction financing. Obtaining this letter is the first essential step to secure a building contract and ensure the project meets strict VA structural standards and inspection guidelines.

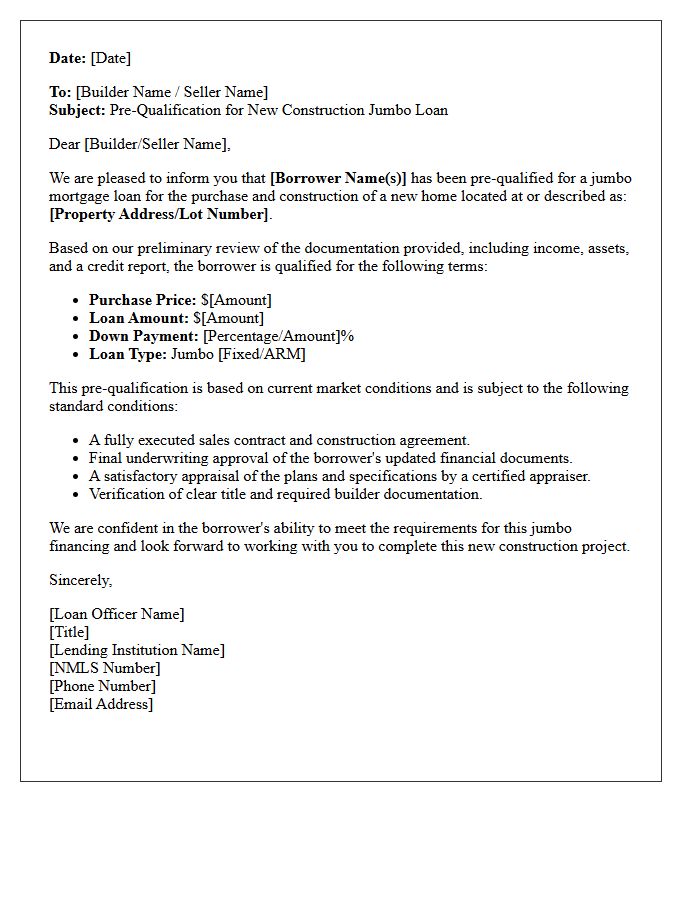

Jumbo Loan New Construction Pre-Qualification Letter

Securing a Jumbo Loan Pre-Qualification Letter for new construction is vital when borrowing amounts exceeding conforming limits. This document proves financial eligibility to builders, ensuring you can finance luxury upgrades and structural customizations. Unlike standard loans, these require higher credit scores, low debt-to-income ratios, and significant cash reserves. Obtaining this letter early streamlines the custom home-building process, giving you leverage during contract negotiations. It serves as a preliminary commitment from lenders, confirming you meet the rigorous capital requirements necessary to fund high-value residential projects from the ground up.

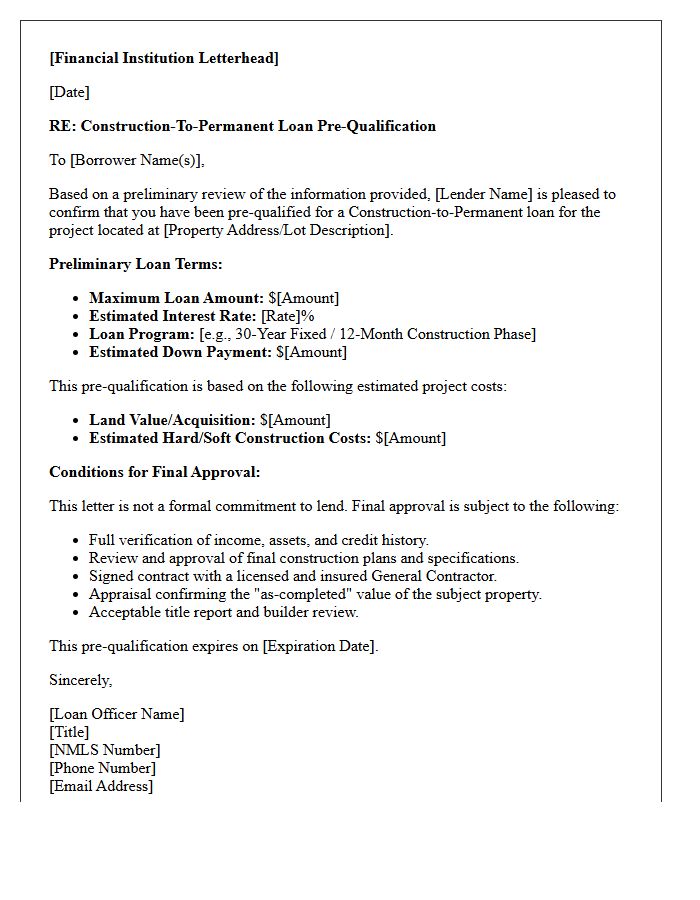

Construction-To-Permanent Pre-Qualification Letter

A Construction-To-Permanent Pre-Qualification Letter is a vital document confirming a lender's preliminary approval for a single-close loan. It evaluates your creditworthiness and financial capacity to fund both the building phase and the long-term mortgage. This letter is essential for securing a builder and starting the architectural process, as it proves you have the committed financing necessary to complete a custom home project. It outlines your maximum budget, ensuring the transition from interim construction financing to a fixed-rate permanent mortgage is seamless and financially viable from the outset.

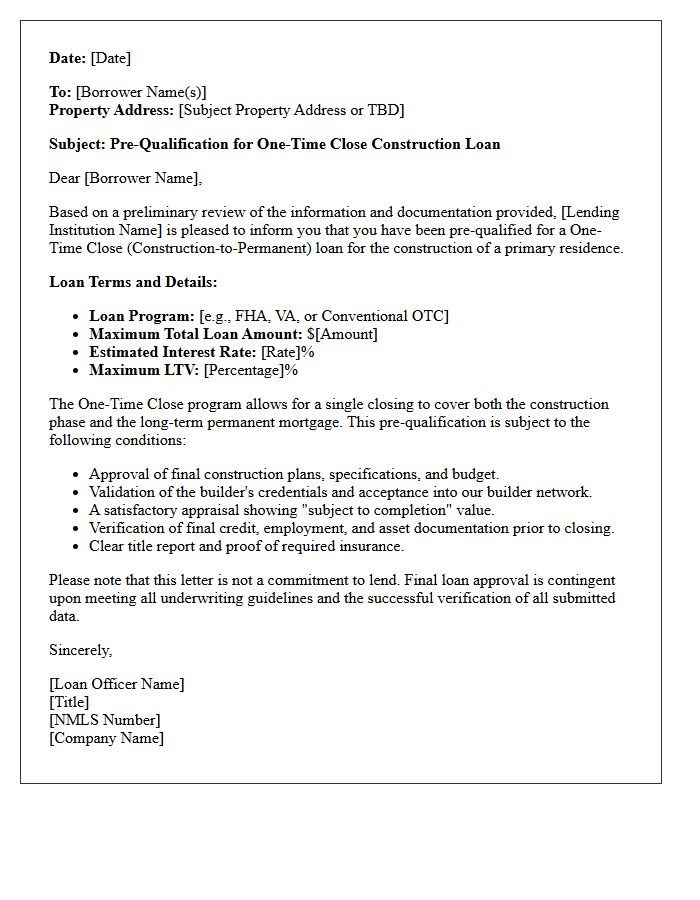

One-Time Close Construction Pre-Qualification Letter

A One-Time Close Construction Pre-Qualification Letter is a vital document confirming a borrower's initial eligibility for a single-close loan. This specialized financing combines construction costs and the permanent mortgage into one transaction with a single closing date. The letter proves to builders and lenders that you have the creditworthiness and financial capacity to fund both the build phase and the long-term debt. Securing this document early ensures your project starts smoothly, protects your interest rate, and simplifies the transition from breaking ground to moving into your new home.

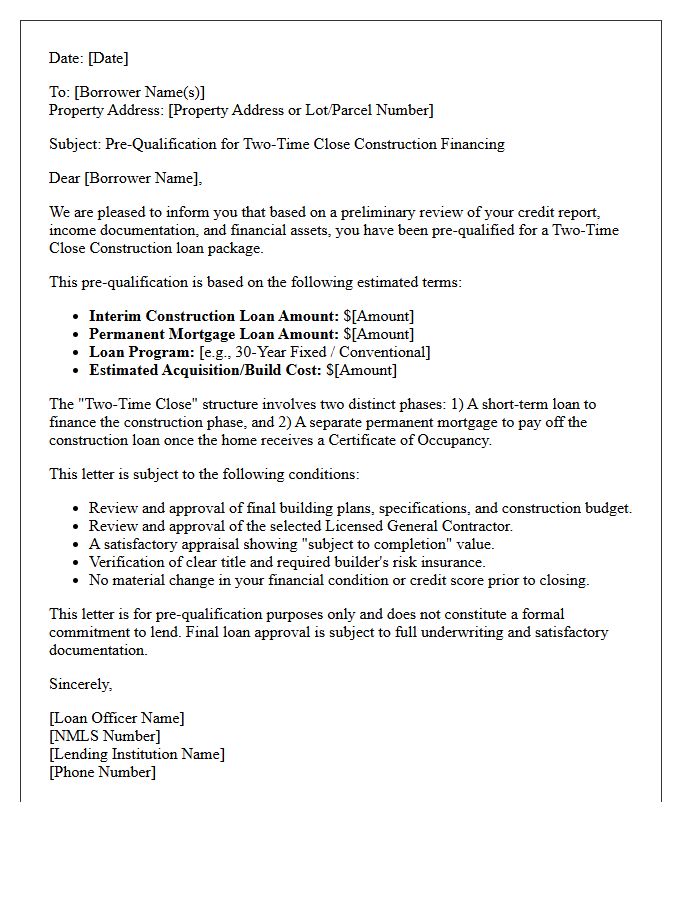

Two-Time Close Construction Pre-Qualification Letter

A Two-Time Close Construction Pre-Qualification Letter is a critical document confirming a borrower's initial eligibility for two separate loans: one for building and another for the permanent mortgage. Unlike single-close options, this path requires re-qualifying before the final conversion, meaning your credit and income must remain stable throughout the project. It offers flexibility in choosing different lenders for each phase but carries the risk of changing interest rates. Ensuring you meet debt-to-income requirements early is essential for securing financing from groundbreaking to move-in day.

Builder Preferred Lender Pre-Qualification Letter

A builder preferred lender pre-qualification letter is an essential document when purchasing new construction homes. Builders often require buyers to vet their finances through a specific affiliated lender to ensure closing reliability and financial stability. While you can often use any bank for your final mortgage, obtaining this specific letter is frequently mandatory to sign a contract or secure incentives like closing cost credits. This process confirms you meet the builder's unique criteria and helps prioritize your offer in competitive housing developments.

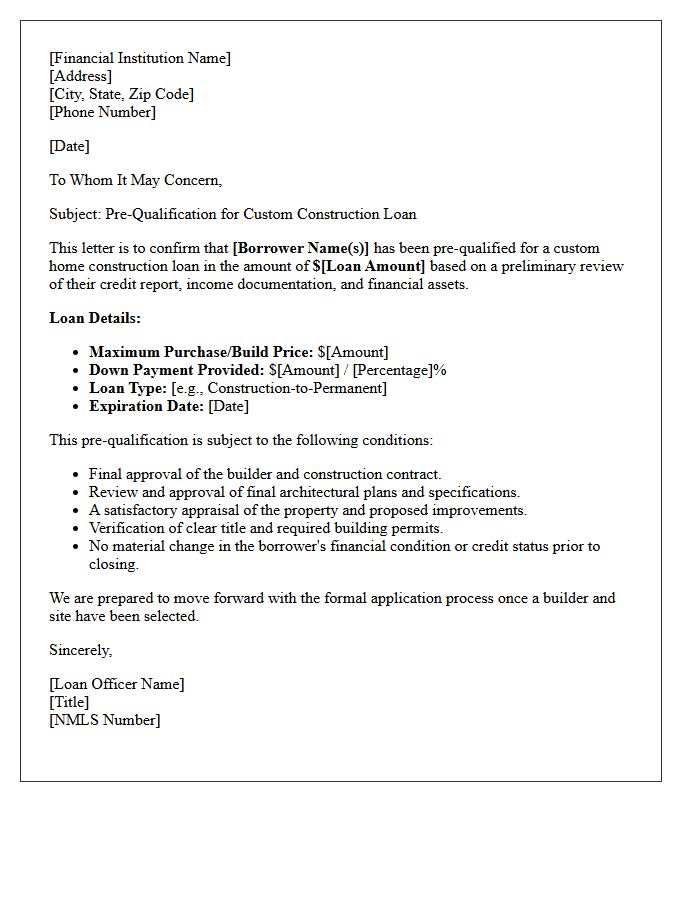

Custom Home Build Pre-Qualification Letter

A Custom Home Build Pre-Qualification Letter is a document from a lender estimating how much you can borrow for construction financing. Unlike a standard mortgage, it considers both the land value and projected building costs. This letter proves to builders and architects that you are a serious prospect with the financial capacity to fund a project. It is the essential first step in the home building process, helping you establish a realistic budget before investing in blueprints or land acquisitions to avoid costly overruns later.

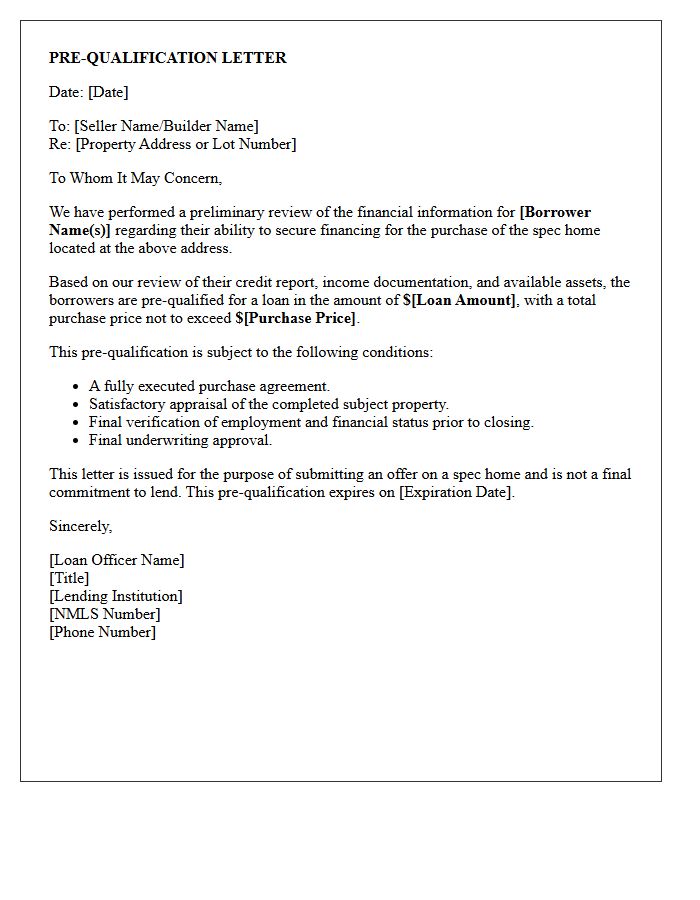

Spec Home Purchase Pre-Qualification Letter

A Spec Home Purchase Pre-Qualification Letter is a vital document confirming a buyer's financial ability to acquire a move-in-ready property. Builders require this proof of funding to ensure the mortgage approval aligns with the specific price point of the speculative construction. Unlike custom builds, these homes are already underway or finished, making a pre-qualification essential for securing a binding contract. It demonstrates credibility to the developer, confirming that the lender has verified the applicant's credit, income, and debt-to-income ratio before finalizing the sale of the newly built inventory.

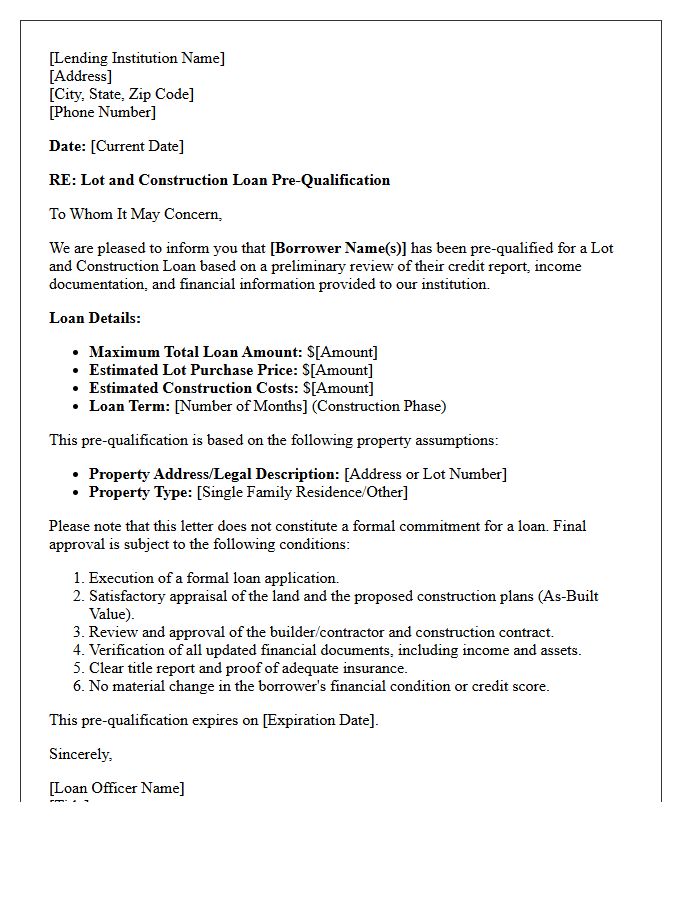

Lot And Construction Loan Pre-Qualification Letter

A Lot and Construction Loan Pre-Qualification Letter is an essential document that estimates your borrowing capacity for purchasing land and building a home. It signals to sellers and builders that you are a credible buyer with a verified financial profile. To obtain one, lenders evaluate your credit score, income, and debt-to-income ratio. This preliminary approval is not a final commitment but provides a realistic budget for your project. Having this letter in hand streamlines the process, allowing you to secure the ideal lot and initiate construction plans with confidence.

What is a New Construction Pre-Qualification Letter?

A new construction pre-qualification letter is a document from a mortgage lender indicating that a homebuyer is tentatively approved for a loan specifically to build a new home. It estimates the loan amount based on a preliminary review of the buyer's credit, income, and assets.

How does a pre-qualification letter differ from a pre-approval for new construction?

A pre-qualification is based on self-reported data and a soft credit check, providing a ballpark estimate of borrowing power. A pre-approval involves a rigorous verification of financial documents and a hard credit pull, making it a stronger commitment often required by builders before signing a construction contract.

Why do builders require a pre-qualification letter before starting a project?

Builders require this letter to ensure the buyer has the financial capacity to secure a construction-to-permanent loan. It minimizes the risk of the project stalling due to funding issues and confirms that the buyer can afford both the base price of the home and potential upgrades.

What financial information is needed to get a new construction pre-qualification?

To obtain the letter, you typically need to provide your social security number for a credit check, recent pay stubs, bank statements, and tax returns. The lender will evaluate your debt-to-income (DTI) ratio to determine if you can support the costs of land acquisition and home construction.

How long is a new construction pre-qualification letter valid?

Most pre-qualification letters are valid for 60 to 90 days. Because new construction projects can take several months or even years to complete, buyers must often renew their qualification or transition to a formal loan commitment as the build progresses and interest rates fluctuate.

Comments