A Non-QM Loan Pre-Qualification Letter demonstrates your eligibility for alternative financing based on bank statements or assets rather than traditional tax returns. This essential document signals to sellers that you are a serious buyer capable of securing specialized funding. Understanding the requirements helps streamline your homebuying journey. Below are some ready to use template.

Image cover: Non-QM Loan Pre-Qualification: Professional Templates and Samples for Borrowers

Letter Samples List

- Bank Statement Non-QM Loan Pre-Qualification Letter

- Debt Service Coverage Ratio Non-QM Pre-Qualification Letter

- Asset Depletion Mortgage Pre-Qualification Letter

- Foreign National Non-QM Pre-Qualification Letter

- Self-Employed Borrower Non-QM Pre-Qualification Letter

- Investor Cash Flow Non-QM Pre-Qualification Letter

- Jumbo Alternative Income Pre-Qualification Letter

- Recent Credit Event Non-QM Pre-Qualification Letter

- Independent Contractor Non-QM Pre-Qualification Letter

- Individual Taxpayer Identification Number Non-QM Pre-Qualification Letter

- No Ratio Investment Property Pre-Qualification Letter

- Interest Only Non-QM Mortgage Pre-Qualification Letter

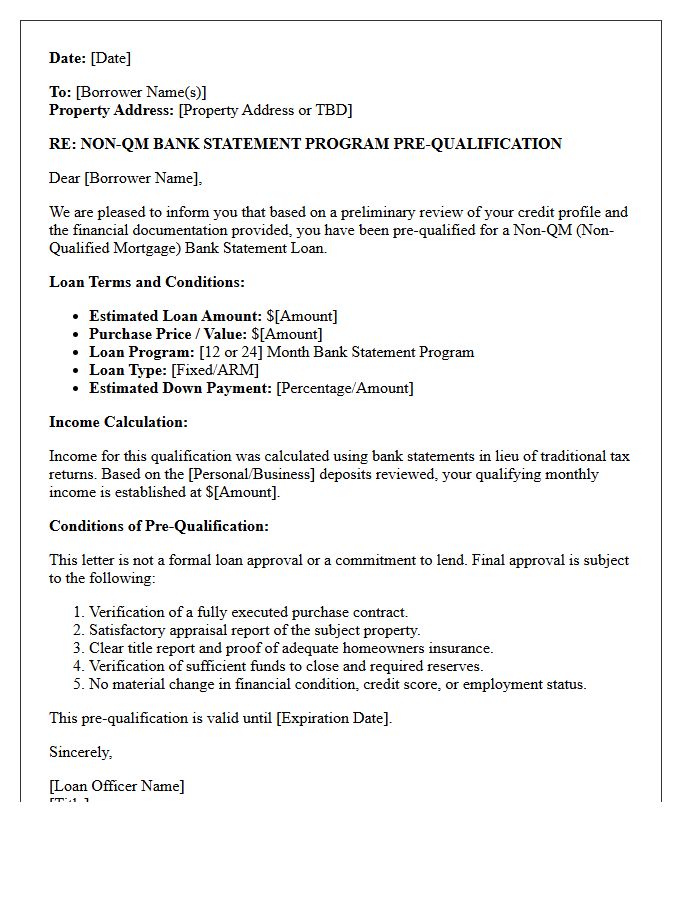

Bank Statement Non-QM Loan Pre-Qualification Letter

A Bank Statement Non-QM Loan Pre-Qualification Letter proves your buying power without traditional tax returns. It confirms that a lender has reviewed your cash flow from personal or business bank statements to determine eligibility. This document is essential for self-employed borrowers looking to secure a mortgage in a competitive market. It demonstrates financial credibility to sellers, showing you meet specific liquidity requirements and credit standards. Obtaining this letter is the first vital step toward financing a home using alternative documentation instead of standard W-2 forms.

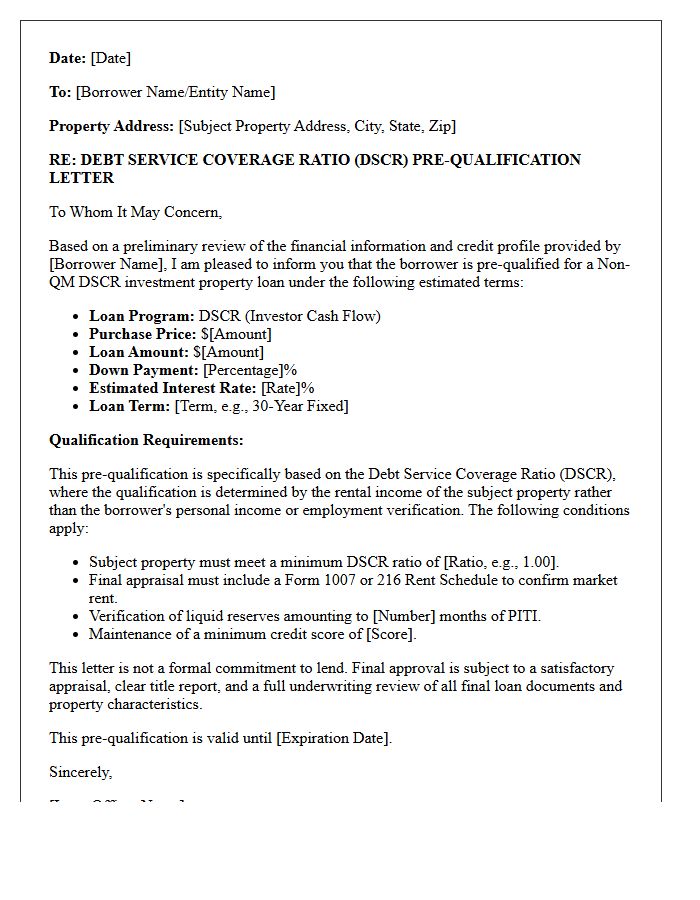

Debt Service Coverage Ratio Non-QM Pre-Qualification Letter

A DSCR Non-QM Pre-Qualification Letter proves a real estate investor's ability to secure financing based on a property's rental income rather than personal income. This document validates that the estimated cash flow covers the monthly debt obligations, including principal, interest, taxes, and insurance. Obtaining this letter is a critical first step in the mortgage approval process, signaling to sellers that the borrower is credible. It allows for faster closing times and competitive offers by confirming the Debt Service Coverage Ratio meets the lender's specific investment property guidelines without requiring traditional tax returns.

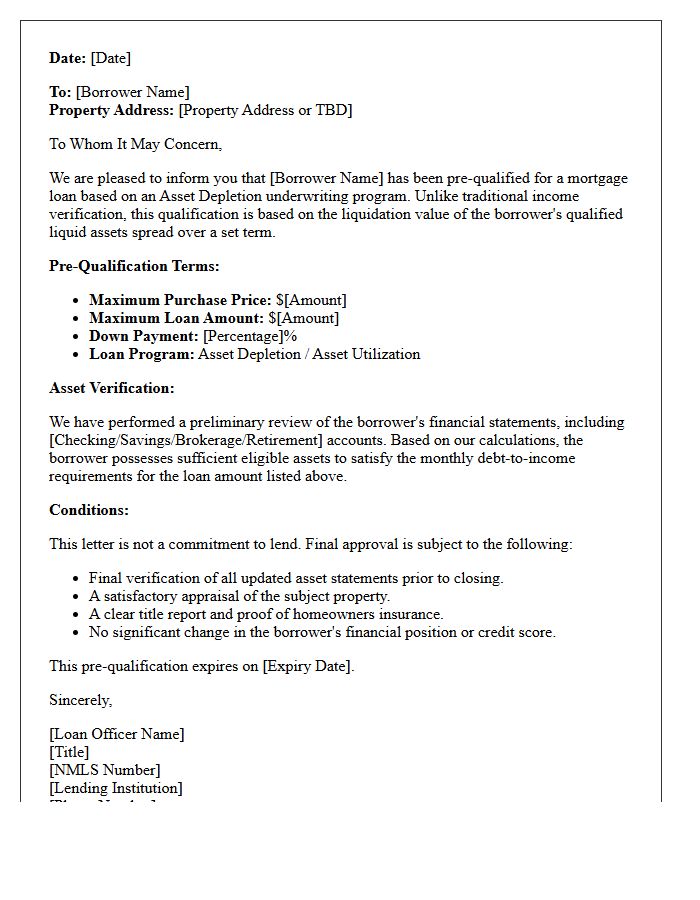

Asset Depletion Mortgage Pre-Qualification Letter

An Asset Depletion Mortgage Pre-Qualification Letter proves your borrowing power by converting liquid wealth into a monthly income stream. This document is essential for high-net-worth individuals with significant assets but limited traditional employment income. It confirms that a lender has calculated your "effective income" based on total portfolio value divided by a specific loan term. Having this letter demonstrates to sellers that you are a qualified buyer who can secure financing using asset-based underwriting rather than standard tax returns or paystubs.

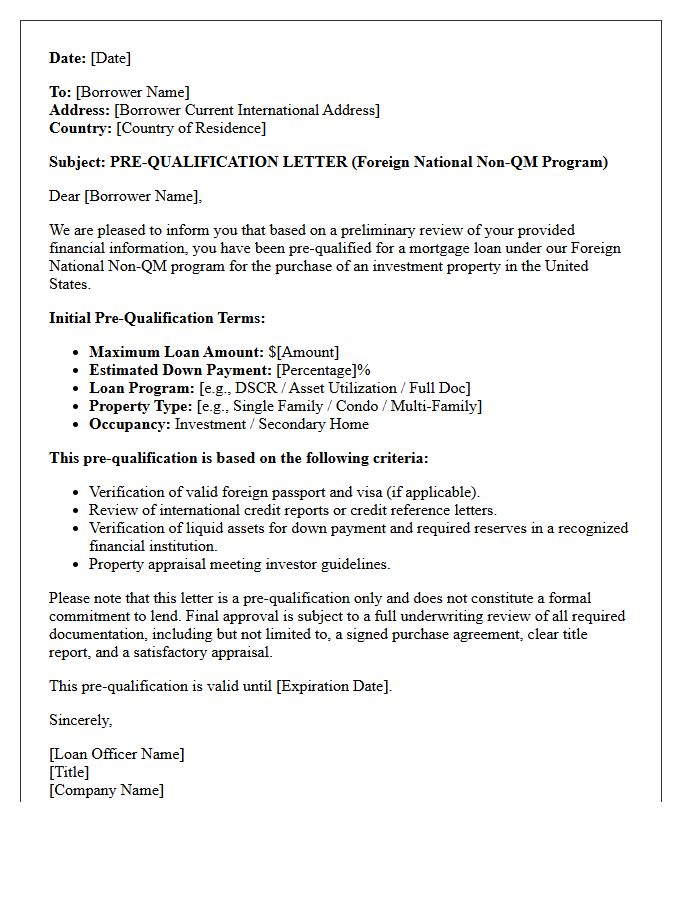

Foreign National Non-QM Pre-Qualification Letter

A Foreign National Non-QM Pre-Qualification Letter is a crucial document for non-resident investors seeking U.S. real estate. It proves creditworthiness and financial capacity without requiring a standard domestic credit score. These letters use alternative documentation, such as bank statements or DSCR ratios, to verify eligibility. Obtaining this letter is the vital first step in the mortgage process, signaling to sellers that you are a serious buyer capable of securing specialized non-QM financing despite your foreign status.

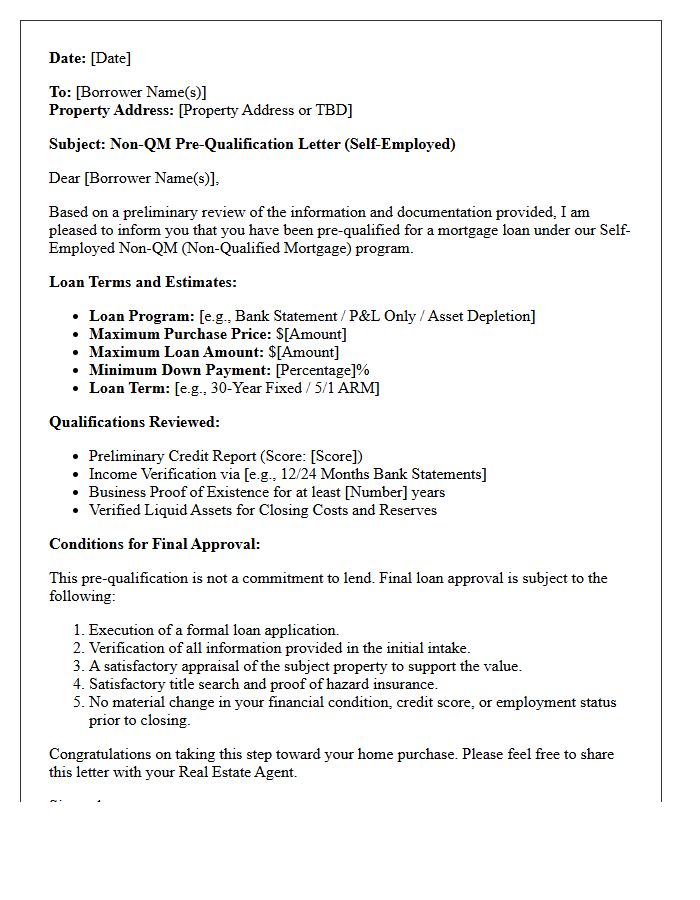

Self-Employed Borrower Non-QM Pre-Qualification Letter

A Self-Employed Borrower Non-QM Pre-Qualification Letter proves creditworthiness using alternative documentation. Unlike traditional loans, these Bank Statement Loans analyze cash flow rather than tax returns to determine income. This document signals to sellers that a lender has verified your liquid assets and credit score. It is essential for entrepreneurs with complex tax deductions who need to demonstrate purchasing power in a competitive market. Securing this letter ensures you meet specific non-agency guidelines, bridging the gap between non-traditional earnings and successful property acquisition.

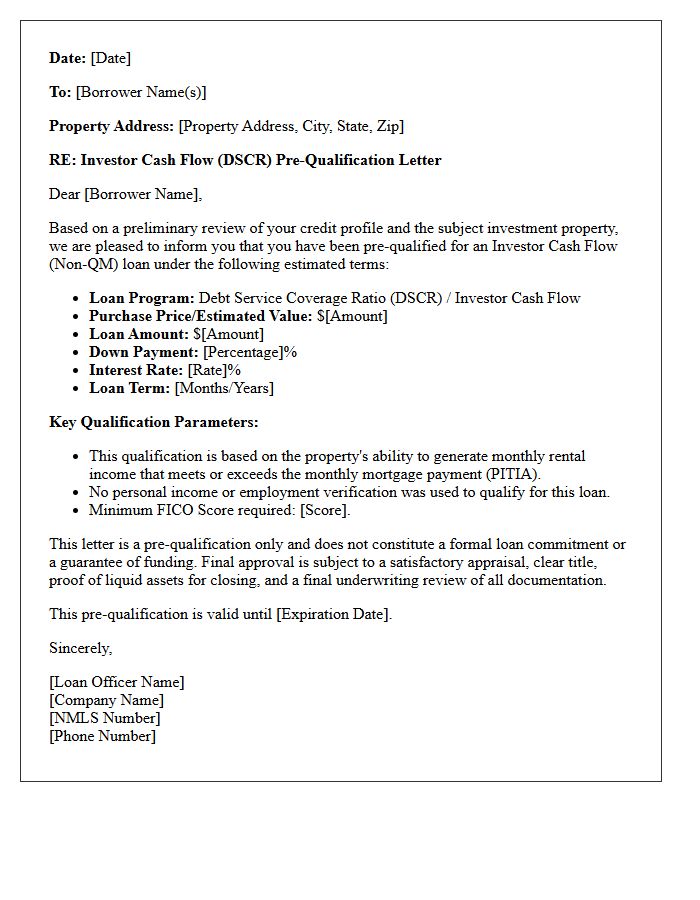

Investor Cash Flow Non-QM Pre-Qualification Letter

An Investor Cash Flow Non-QM Pre-Qualification Letter confirms eligibility for a DSCR loan, focusing on the property's rental income rather than personal finances. This document is essential for real estate investors seeking to leverage debt without providing traditional tax returns or employment verification. It proves to sellers that the investment property generates sufficient cash flow to cover mortgage obligations. Obtaining this letter is the critical first step in securing alternative financing, allowing for faster closings and more flexible underwriting standards compared to conventional mortgage products.

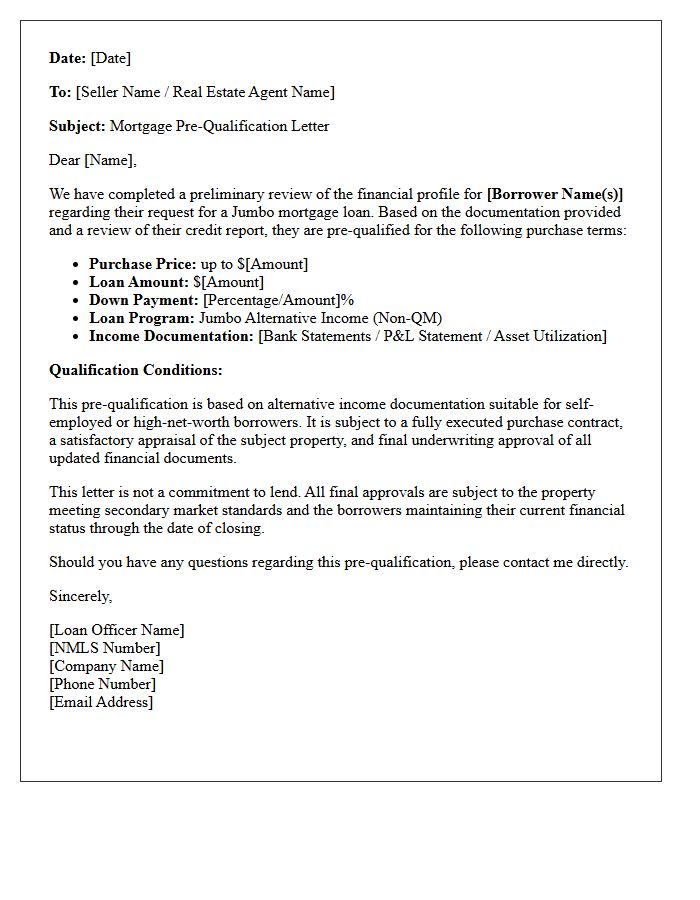

Jumbo Alternative Income Pre-Qualification Letter

A Jumbo Alternative Income Pre-Qualification Letter proves a borrower's creditworthiness using non-traditional documentation, such as bank statements or asset depletion, rather than standard tax returns. This essential document signals to sellers that a high-net-worth buyer qualifies for a large loan amount despite having complex self-employment income or unique financial structures. Obtaining this letter is the critical first step in securing luxury real estate, as it validates purchasing power in competitive markets where traditional underwriting guidelines are often too restrictive for sophisticated investors.

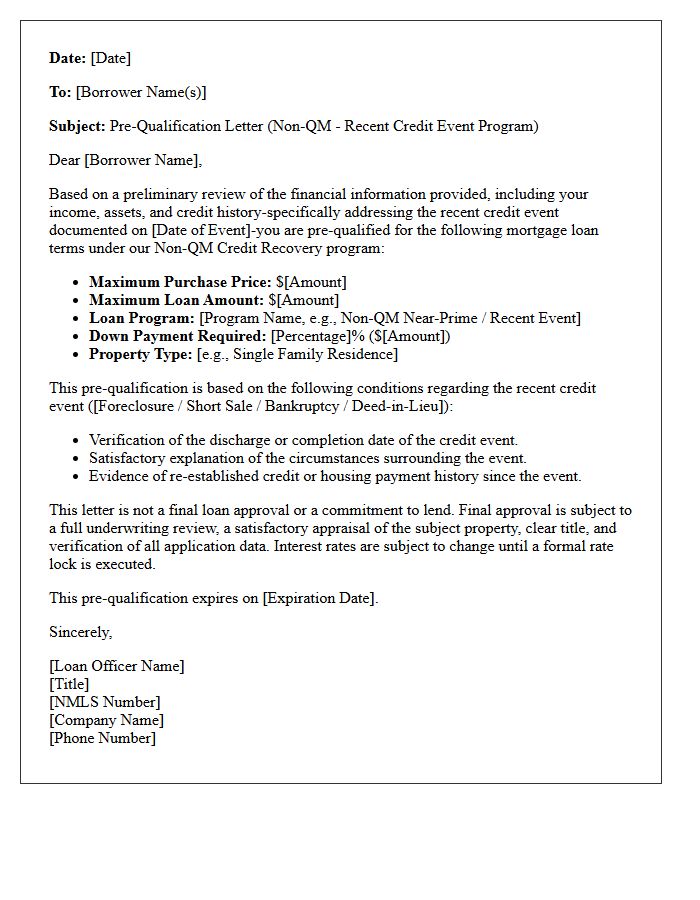

Recent Credit Event Non-QM Pre-Qualification Letter

A Recent Credit Event Non-QM Pre-Qualification Letter is a vital document for borrowers recovering from financial setbacks such as bankruptcy, foreclosure, or short sales. Unlike traditional loans, Non-QM lending focuses on overall repayment ability rather than strict waiting periods. This letter proves a lender has reviewed your alternative documentation, such as bank statements, to verify eligibility despite past credit issues. It serves as a competitive advantage in real estate transactions, signaling to sellers that you are a qualified buyer capable of securing specialized financing outside of conventional mortgage guidelines.

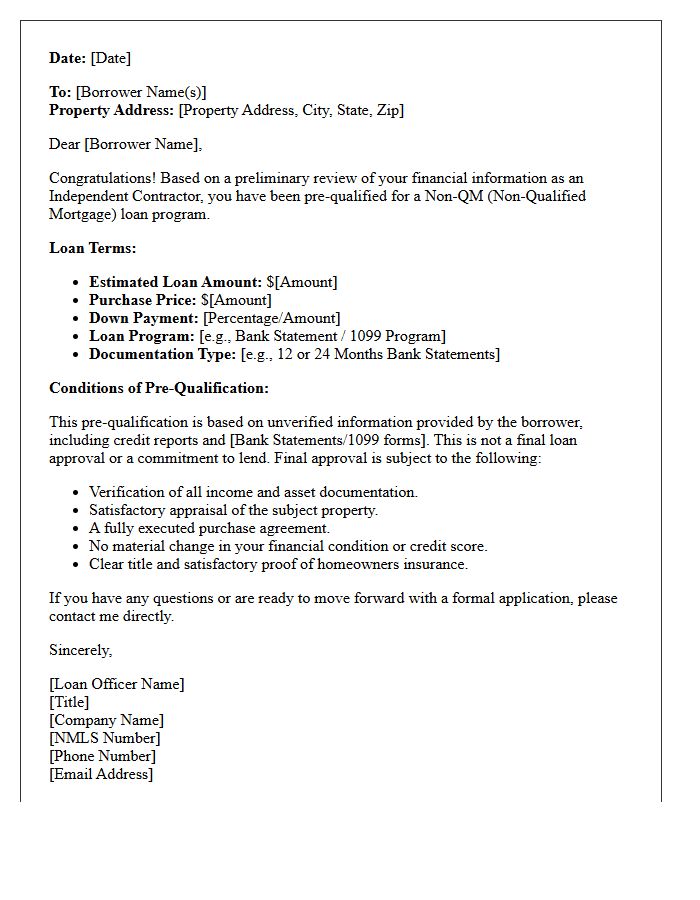

Independent Contractor Non-QM Pre-Qualification Letter

An Independent Contractor Non-QM Pre-Qualification Letter proves creditworthiness for 1099 workers using alternative documentation like bank statements instead of tax returns. This document confirms a lender has reviewed your cash flow and credit profile to estimate a maximum loan amount. It is essential for gig economy professionals to demonstrate buying power to sellers when traditional W-2 income is unavailable. Securing this letter ensures you meet specific Non-Qualified Mortgage criteria, bridging the gap between self-employment flexibility and homeownership eligibility in a competitive real estate market.

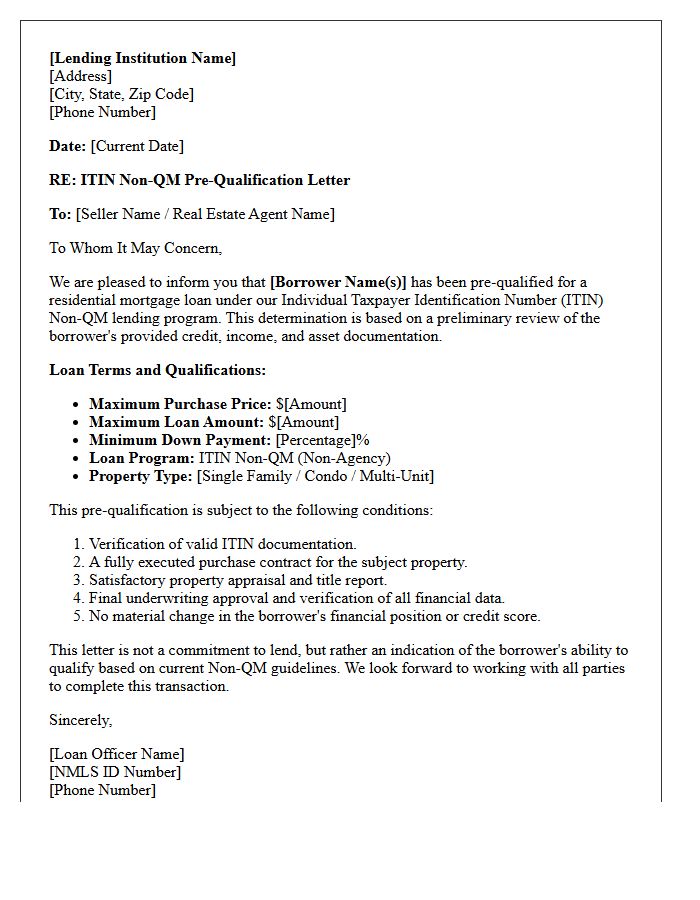

Individual Taxpayer Identification Number Non-QM Pre-Qualification Letter

An ITIN Non-QM Pre-Qualification Letter is a vital document for foreign nationals or residents without a Social Security Number seeking alternative mortgage financing. It proves that a lender has verified your creditworthiness and income potential under Non-Qualified Mortgage guidelines. This letter strengthens your home-buying offer by demonstrating financial readiness to sellers. To obtain one, you must provide your Individual Taxpayer Identification Number and documentation showing stable repayment capacity. It serves as an essential first step for non-traditional borrowers to access the United States real estate market securely.

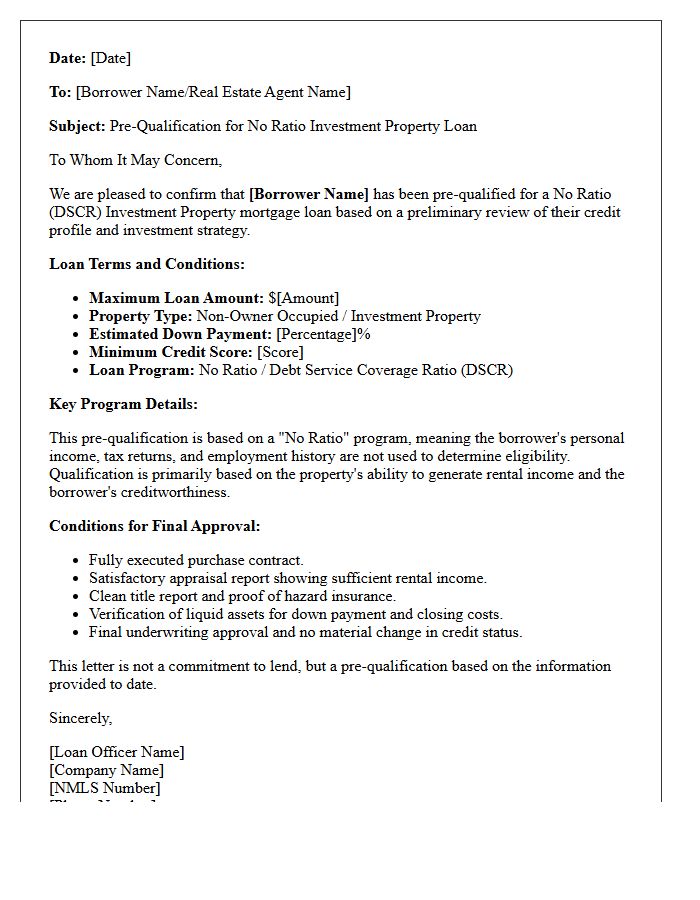

No Ratio Investment Property Pre-Qualification Letter

A No Ratio Investment Property Pre-Qualification Letter proves a borrower's eligibility for financing based solely on the property's potential income rather than personal debt-to-income ratios. This document confirms that the Debt Service Coverage Ratio (DSCR) or rental revenue meets lender requirements. It allows real estate investors to move quickly on offers without disclosing personal tax returns or employment history. Securing this letter demonstrates financial readiness to sellers, highlighting that the investment asset itself generates sufficient cash flow to secure the mortgage independently of the investor's individual income profile.

Interest Only Non-QM Mortgage Pre-Qualification Letter

An Interest Only Non-QM Mortgage Pre-Qualification Letter demonstrates a borrower's ability to secure financing without standard income documentation. This document confirms that a lender has reviewed your alternative financial data, such as bank statements or asset verification, to support lower initial monthly payments. It is a vital tool for real estate investors and self-employed individuals to prove purchasing power in competitive markets. Obtaining this letter ensures you meet specific credit and liquidity requirements before making a formal offer on a property.

What is a Non-QM loan pre-qualification letter?

A Non-QM loan pre-qualification letter is a document from a lender indicating that a borrower is likely to be approved for a non-qualified mortgage based on an initial review of their alternative financial documentation, such as bank statements or asset portfolios.

How do I qualify for a Non-QM mortgage pre-qualification?

To obtain a pre-qualification letter, you must provide a lender with basic financial data, including credit scores and proof of income through non-traditional means like 12 to 24 months of bank statements, P&L statements, or investment property cash flow (DSCR) details.

How long does it take to get a Non-QM pre-qualification letter?

Most lenders can issue a Non-QM pre-qualification letter within 24 to 48 hours after receiving your initial financial documents, as the process relies on an automated or manual review of your credit profile and liquid assets.

Does a Non-QM pre-qualification letter guarantee loan approval?

No, a pre-qualification letter is not a binding commitment to lend; it is an estimate of borrowing power. Final loan approval is subject to full underwriting, a formal property appraisal, and verification of all submitted financial data.

What is the difference between a standard pre-qualification and a Non-QM pre-qualification?

A standard pre-qualification focuses on W-2 income and tax returns, while a Non-QM pre-qualification is specifically designed for self-employed individuals, investors, or foreign nationals who use alternative documentation to verify their ability to repay the loan.

Comments