A Qualified Audit Opinion is issued when an auditor finds financial statements are fairly presented except for specific areas of non-compliance or scope limitations. It signals minor deviations from accounting standards without invalidating the entire report. Understanding this distinction is crucial for stakeholders assessing corporate transparency and financial health. To help you draft these reports, below are some ready to use template.

Image cover: Professional Templates and Examples for a Qualified Audit Opinion Letter

Letter Samples List

- Qualified Audit Opinion Letter Regarding Inventory Valuation Departure

- Qualified Audit Opinion Letter Due to Audit Scope Limitation

- Qualified Audit Opinion Letter Concerning Inadequate Financial Disclosures

- Qualified Audit Opinion Letter for Unverified Accounts Receivable Balances

- Qualified Audit Opinion Letter Addressing Improper Depreciation Methods

- Qualified Audit Opinion Letter Due to Missing Subsidiary Financial Records

- Qualified Audit Opinion Letter Regarding Unrecorded Corporate Liabilities

- Qualified Audit Opinion Letter Concerning Capitalization of Operating Expenses

- Qualified Audit Opinion Letter for Noncompliance With Revenue Recognition Standards

- Qualified Audit Opinion Letter Addressing Omitted Contingent Liabilities

- Qualified Audit Opinion Letter Due to Inability to Observe Physical Inventory

- Qualified Audit Opinion Letter Regarding Unjustified Changes in Accounting Principles

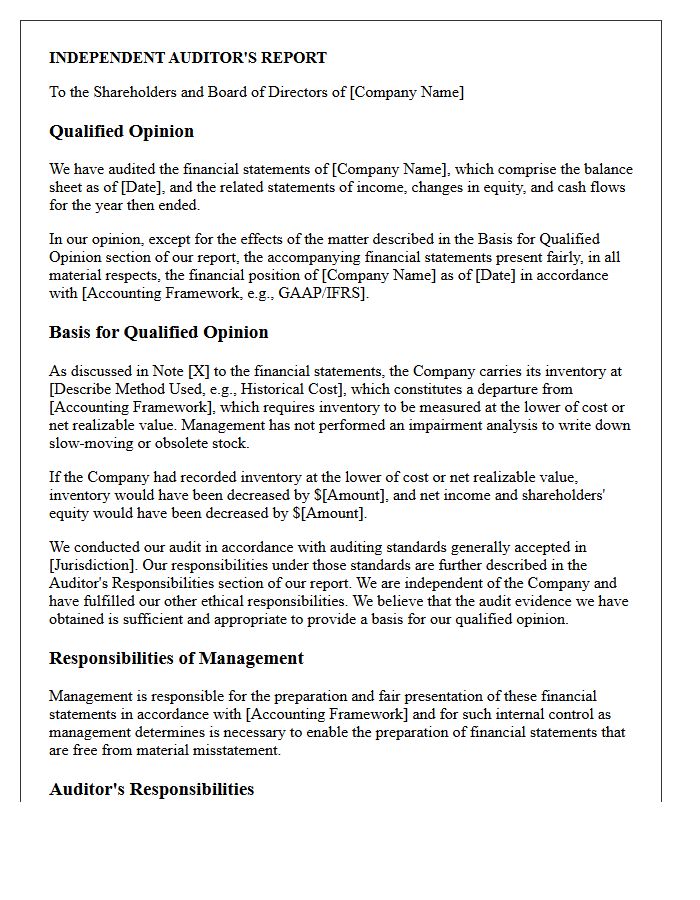

Qualified Audit Opinion Letter Regarding Inventory Valuation Departure

A qualified audit opinion indicates that a company's financial statements are fairly presented, except for a specific inventory valuation departure from accounting standards. This typically occurs when inventory is recorded at an incorrect cost or net realizable value, leading to potential misstatements in assets and cost of goods sold. While the overall report remains reliable, stakeholders must scrutinize the basis for qualified opinion section to understand the specific financial impact and risks associated with the non-compliance regarding physical counts or valuation methods used by the entity.

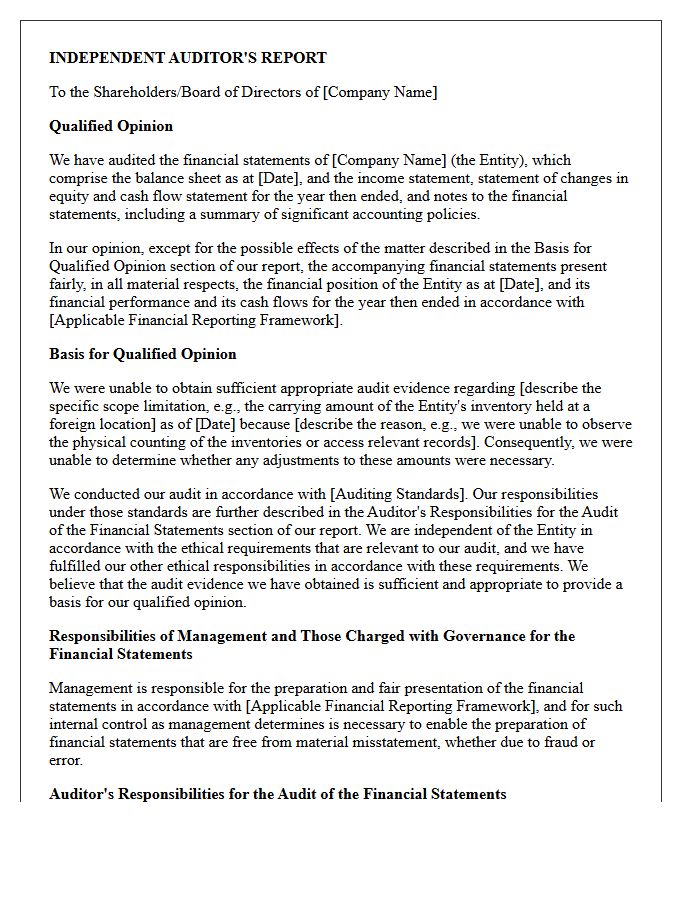

Qualified Audit Opinion Letter Due to Audit Scope Limitation

A qualified audit opinion is issued when auditors encounter an audit scope limitation, meaning they could not gather sufficient evidence for specific financial areas. This occurs due to restricted access, missing records, or timing issues. While the overall financial statements are generally reliable, the auditor must explicitly state the areas of uncertainty. This qualification signals to investors that certain balances remain unverified, potentially hiding inaccuracies. It serves as a critical warning that the limitation prevents a full assessment of the entity's complete financial health and transparency.

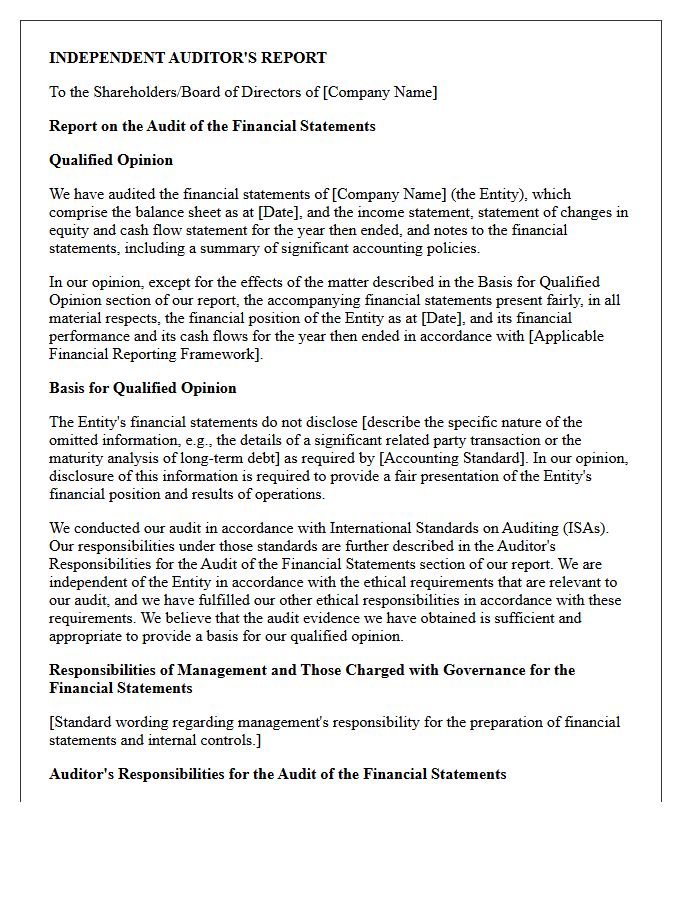

Qualified Audit Opinion Letter Concerning Inadequate Financial Disclosures

A Qualified Audit Opinion Letter regarding inadequate disclosures indicates that a company's financial statements are mostly accurate but fail to provide essential information required by accounting standards. This qualification serves as a formal warning to investors that specific details, such as pending litigation or debt obligations, are missing or obscured. While the overall data is reliable, the lack of transparency prevents a complete assessment of the entity's financial health. Stakeholders must carefully evaluate these omissions, as they represent a significant departure from standard reporting transparency and could hide potential fiscal risks.

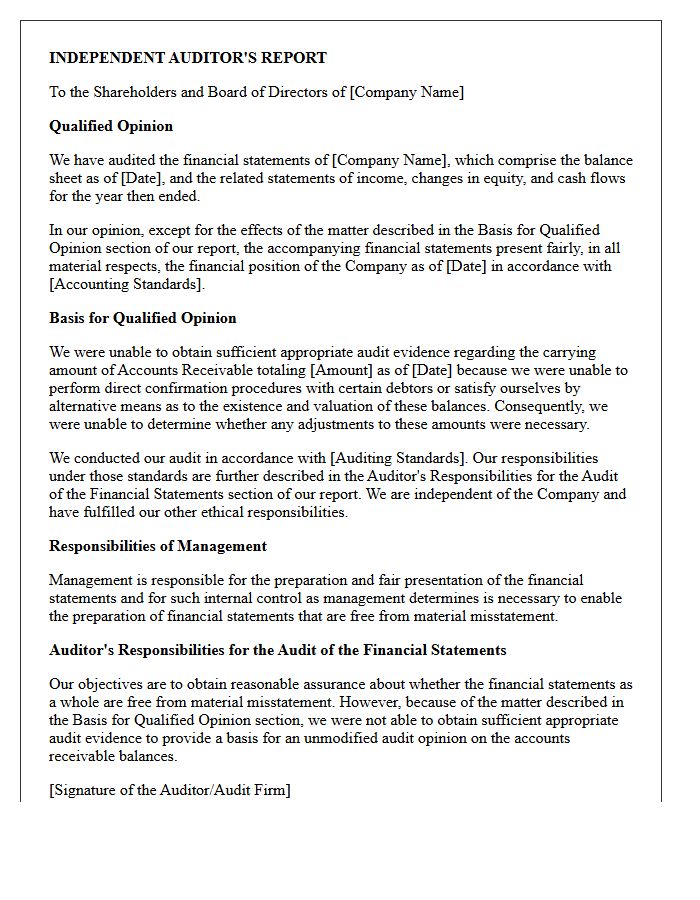

Qualified Audit Opinion Letter for Unverified Accounts Receivable Balances

A Qualified Audit Opinion is issued when auditors cannot verify specific Accounts Receivable balances due to scope limitations or missing documentation. This letter alerts stakeholders that while the financial statements are generally reliable, the unverified receivables could contain material misstatements. It signifies a "departure from standard reporting," indicating that auditors were unable to perform necessary testing, such as direct confirmations. Investors must view this as a red flag, as it suggests potential weaknesses in internal controls or uncertainty regarding the company's actual liquidity and asset valuation.

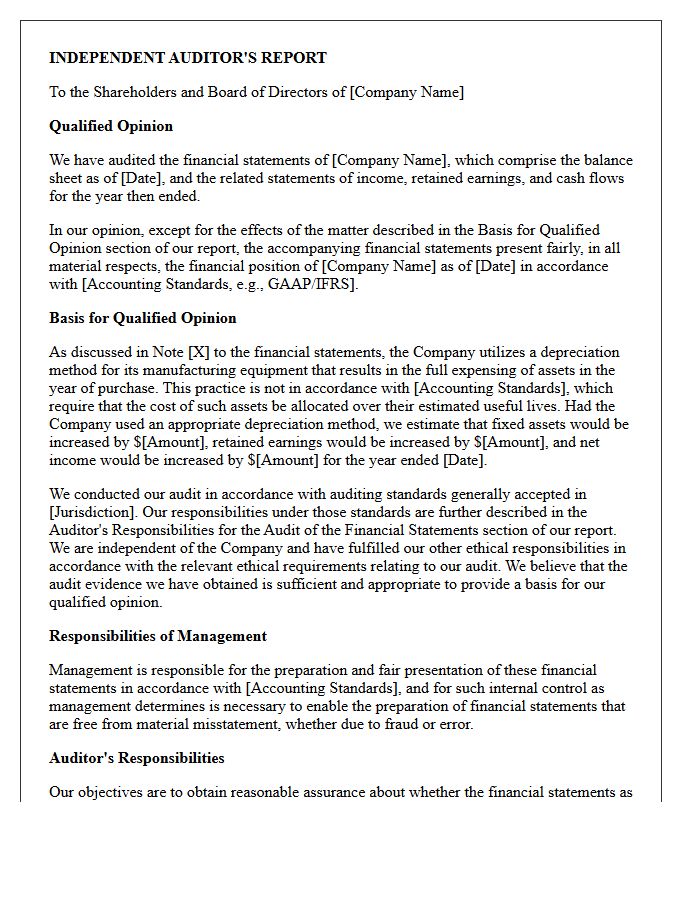

Qualified Audit Opinion Letter Addressing Improper Depreciation Methods

A Qualified Audit Opinion is issued when financial statements are fairly presented except for specific departures from accounting standards. When an auditor identifies improper depreciation methods, it indicates that the company's calculation of asset wear and tear violates GAAP or IFRS principles. This qualification warns stakeholders that reported net income and fixed asset values may be materially misstated. Understanding these discrepancies is crucial for assessing long-term profitability and true asset valuation, as incorrect depreciation schedules artificially inflate or deflate a firm's financial health and tax obligations.

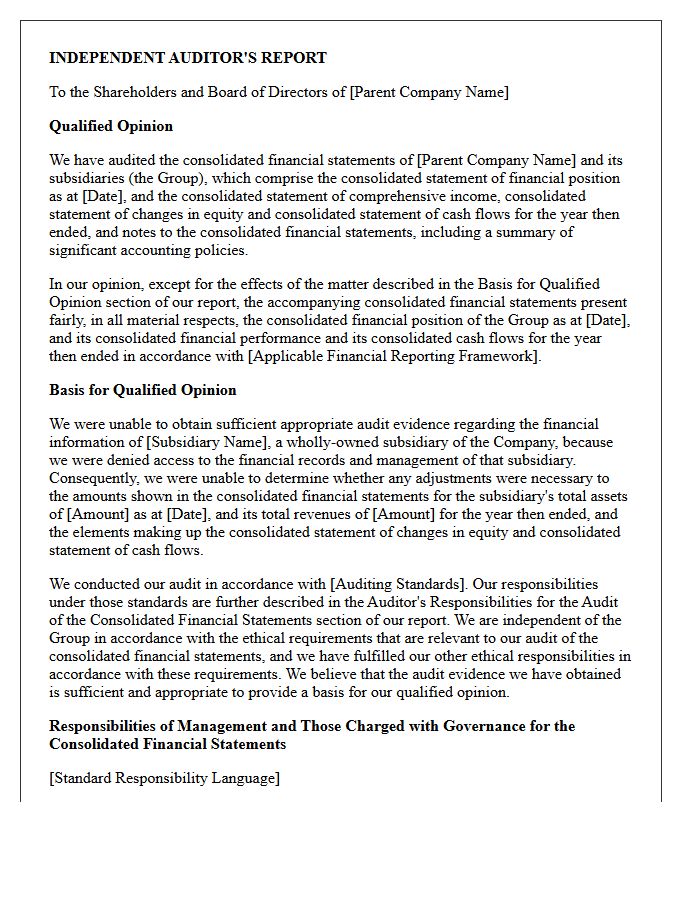

Qualified Audit Opinion Letter Due to Missing Subsidiary Financial Records

A qualified audit opinion issued due to missing subsidiary records indicates a "scope limitation." This means auditors could not obtain sufficient evidence regarding a specific business unit's financial data. While the overall report is mostly accurate, the missing records prevent a clean certification. Stakeholders must be cautious, as these information gaps can hide potential liabilities or inaccuracies within the consolidated statements. This qualification signals financial transparency risks, suggesting that the company lacks complete control over its subsidiary's accounting documentation, which may impact investor confidence and regulatory compliance.

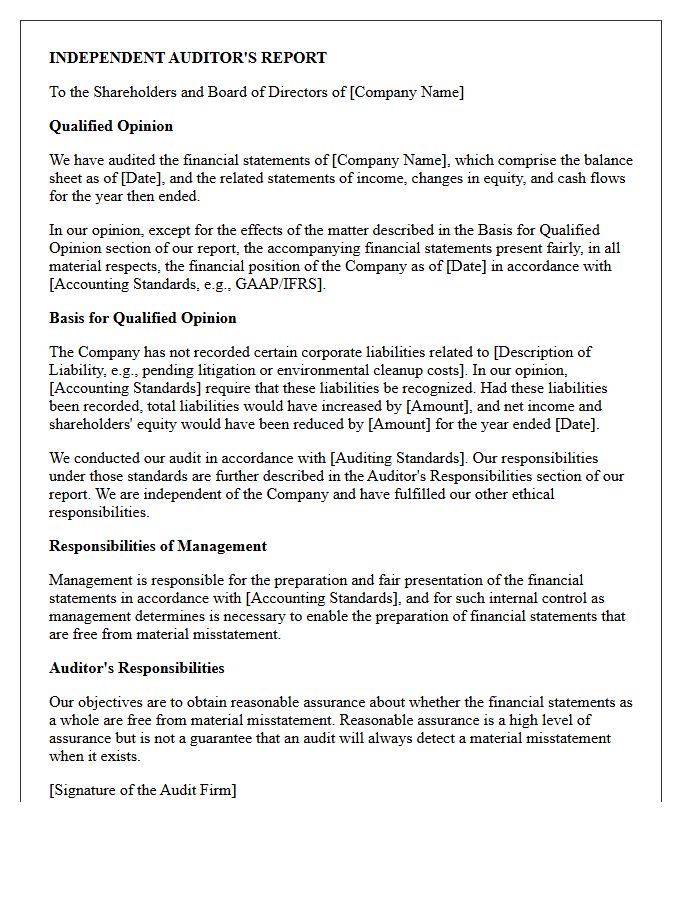

Qualified Audit Opinion Letter Regarding Unrecorded Corporate Liabilities

A Qualified Audit Opinion signals that a company's financial statements are fairly presented except for specific areas of concern. When auditors identify unrecorded corporate liabilities, it indicates that the firm failed to disclose certain debts or obligations. This qualification warns investors that reported figures may understate total debt, potentially impacting solvency and risk assessments. This letter serves as a crucial red flag, highlighting a material departure from accounting standards and suggesting that the financial health of the organization might be less stable than the primary balance sheet figures initially suggest.

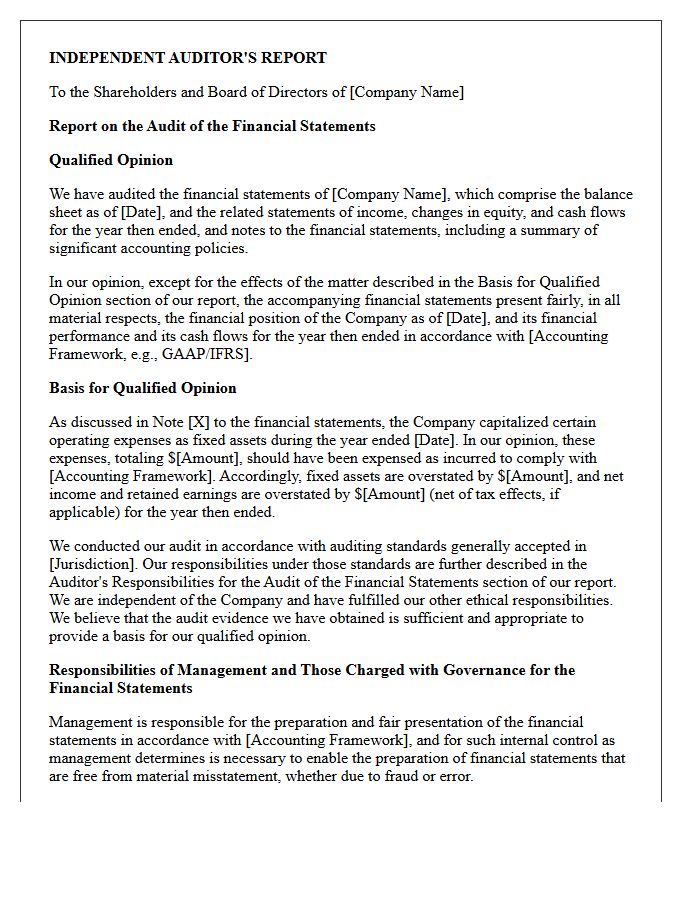

Qualified Audit Opinion Letter Concerning Capitalization of Operating Expenses

A qualified audit opinion regarding capitalized operating expenses indicates that a company's financial statements are mostly accurate, except for a specific departure from GAAP. In this context, the auditor has identified that operating expenses were improperly recorded as capital assets. This practice artificially inflates net income and overstates total assets on the balance sheet. Investors should view this as a red flag, as it suggests aggressive accounting maneuvers or internal control weaknesses that distort the firm's true profitability and long-term financial health.

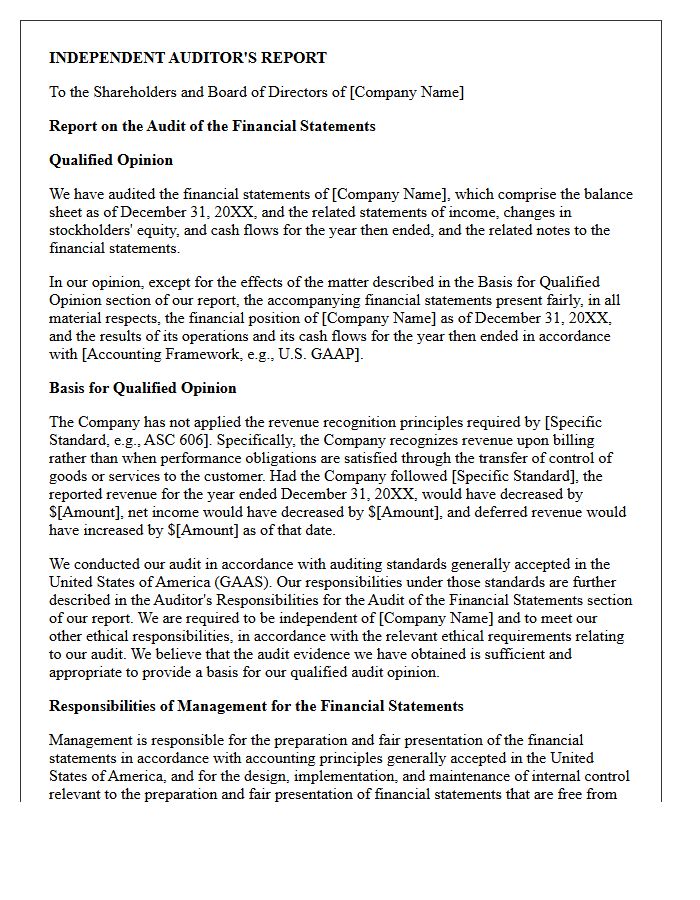

Qualified Audit Opinion Letter for Noncompliance With Revenue Recognition Standards

A Qualified Audit Opinion is issued when a company's financial statements deviate from GAAP, specifically regarding revenue recognition standards. This letter indicates that while most records are accurate, the reported income contains material misstatements. Investors must scrutinize these findings, as noncompliance suggests revenue may be prematurely recorded or overstated. Such qualifications signal potential risks in financial integrity and internal controls, making it essential to understand the specific accounting departures identified by the auditor to assess the company's true fiscal health and future performance.

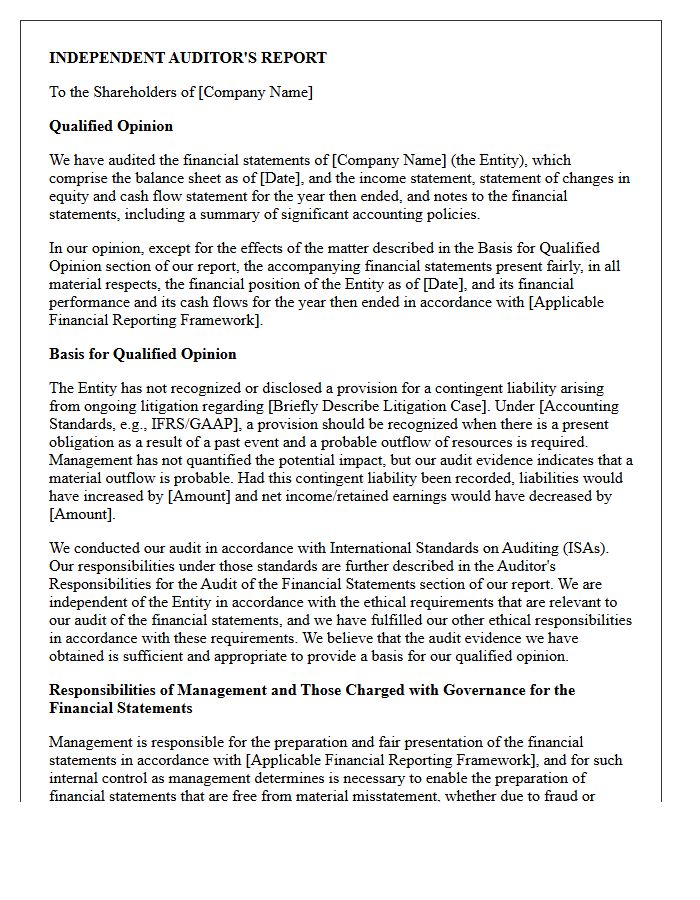

Qualified Audit Opinion Letter Addressing Omitted Contingent Liabilities

A Qualified Audit Opinion serves as a formal warning that a company's financial statements are not entirely compliant with GAAP. When an auditor issues this due to omitted contingent liabilities, it signifies that potential future debts-such as pending lawsuits or environmental fines-have been hidden from the balance sheet. This lack of transparency obscures the firm's true financial risk. Investors must treat this as a significant red flag, as undisclosed obligations can lead to sudden, material losses and diminish the overall reliability of the reported financial health.

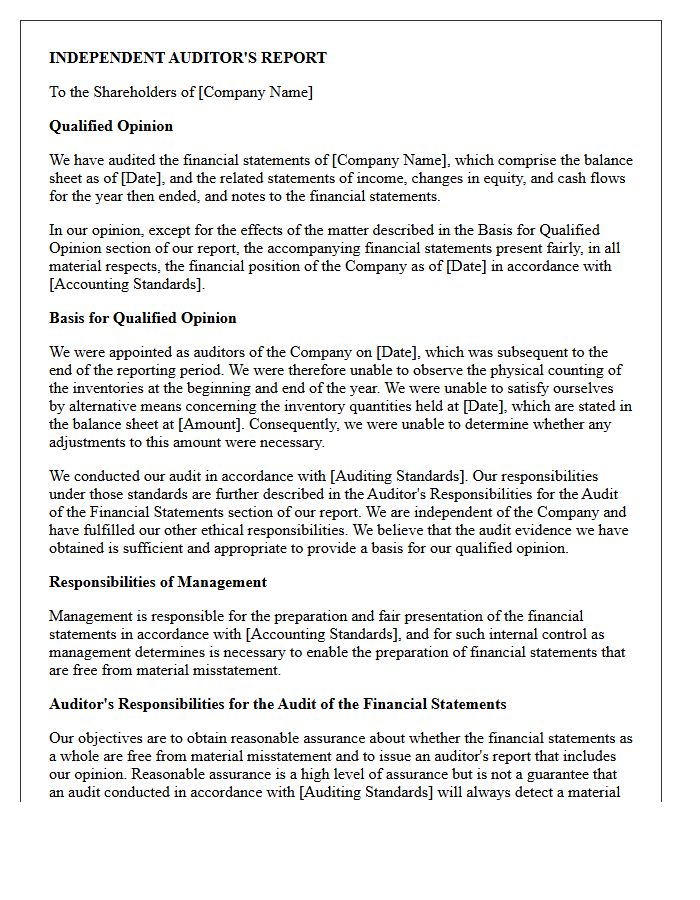

Qualified Audit Opinion Letter Due to Inability to Observe Physical Inventory

A Qualified Audit Opinion is issued when auditors cannot verify physical inventory quantities, often due to late appointment or inaccessible locations. This limitation prevents the auditor from gathering sufficient evidence regarding a material portion of the balance sheet. While the financial statements are generally reliable, this specific scope limitation signals a disclaimer of assurance over stock valuation. Investors should recognize this as a warning that inventory accuracy cannot be guaranteed, potentially affecting the integrity of reported assets and cost of goods sold without implying overall financial fraud.

Qualified Audit Opinion Letter Regarding Unjustified Changes in Accounting Principles

A qualified audit opinion is issued when an auditor identifies unjustified changes in accounting principles that deviate from established frameworks like GAAP. This specific qualification signals that the financial statements are "fair except for" the effects of these inconsistent methods. It warns stakeholders that the company's financial performance may be artificially inflated or distorted, lacking comparability over time. Such a letter serves as a critical red flag for investors, indicating potential financial reporting risks and a lack of transparency in the entity's management of accounting policies.

What is a qualified audit opinion letter?

A qualified audit opinion letter is a report issued by an independent auditor stating that a company's financial statements are fairly presented in all material respects, except for a specific area or account that does not conform to Generally Accepted Accounting Principles (GAAP) or lacks sufficient evidence.

What are the primary reasons an auditor issues a qualified opinion?

Auditors typically issue a qualified opinion due to a scope limitation, where they cannot obtain sufficient appropriate audit evidence, or because of a material departure from the applicable financial reporting framework that is not pervasive enough to warrant an adverse opinion.

How does a qualified audit opinion differ from an unqualified opinion?

An unqualified opinion is a "clean" report indicating that financial statements are free from material misstatements. In contrast, a qualified opinion includes an "except for" clause, highlighting a specific deficiency or uncertainty while asserting that the rest of the financial report is reliable.

What is the impact of a qualified audit opinion on a business?

A qualified audit opinion can negatively affect a company's credibility, potentially leading to difficulties in securing loans, higher interest rates from lenders, or decreased investor confidence due to the identified accounting discrepancies or lack of transparency.

Can a company rectify a qualified audit opinion?

Yes, a company can resolve a qualified opinion by addressing the specific issues raised by the auditor, such as providing missing documentation, adjusting accounting treatments to meet GAAP standards, or improving internal controls before the next audit cycle.

Comments