A Subsequent Events Representation Letter is a formal document provided by management to auditors, confirming that no significant events occurred after the balance sheet date that could materially affect the financial statements. This ensures reporting accuracy and transparency before finalizing audits. To help you draft this essential compliance document, below are some ready to use template.

Image cover: Best Practices for Drafting a Subsequent Events Representation Letter: Templates and Examples

Letter Samples List

- Standard Subsequent Events Representation Letter

- Management Subsequent Events Representation Letter

- Bring-Down Subsequent Events Representation Letter

- Updated Subsequent Events Representation Letter

- Audit Engagement Subsequent Events Representation Letter

- Review Engagement Subsequent Events Representation Letter

- Dual-Dated Subsequent Events Representation Letter

- Post-Balance Sheet Subsequent Events Representation Letter

- Interim Financial Subsequent Events Representation Letter

- Short-Form Subsequent Events Representation Letter

- Comprehensive Subsequent Events Representation Letter

- Final Audit Subsequent Events Representation Letter

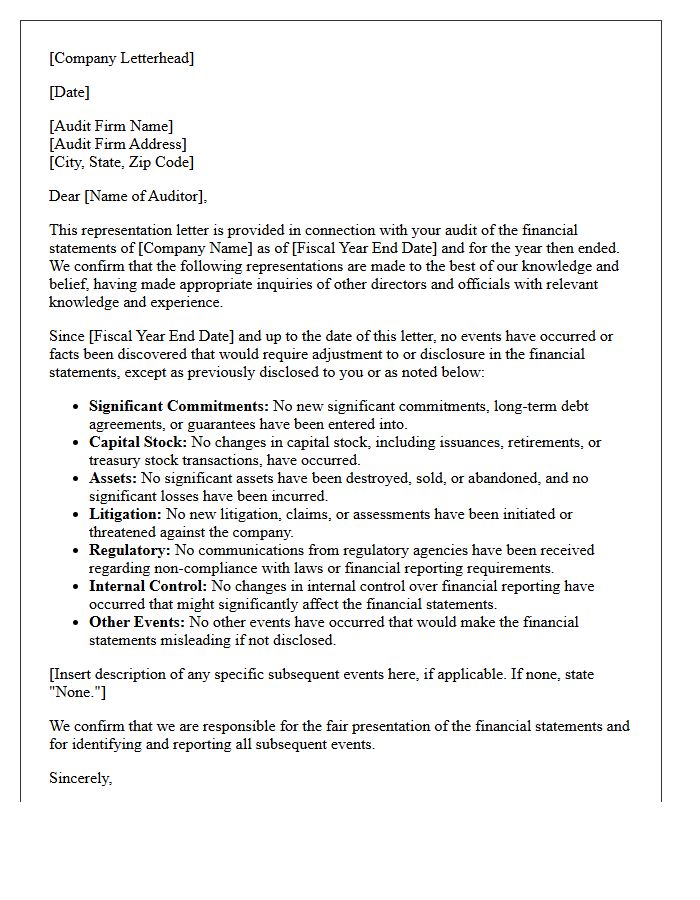

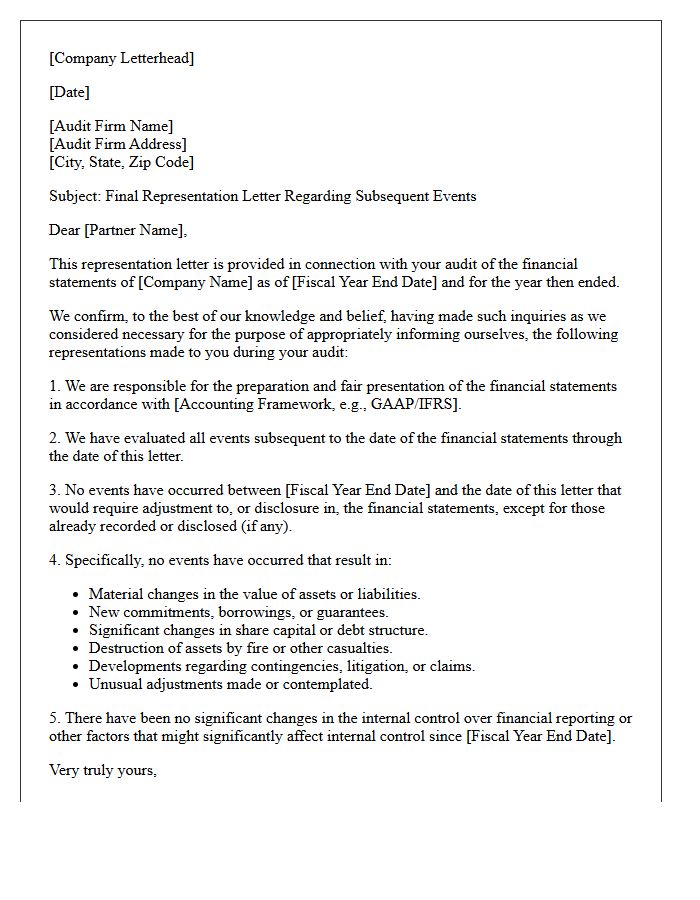

Standard Subsequent Events Representation Letter

A Standard Subsequent Events Representation Letter is a formal document provided by management to auditors during a financial audit. It confirms that all material events occurring after the balance sheet date but before the report issuance have been disclosed. This letter ensures the integrity of financial reporting by identifying significant developments-such as lawsuits, mergers, or asset impairments-that could impact stakeholders' decisions. Providing this written assurance is a critical step in the audit verification process to ensure transparency and compliance with accounting standards.

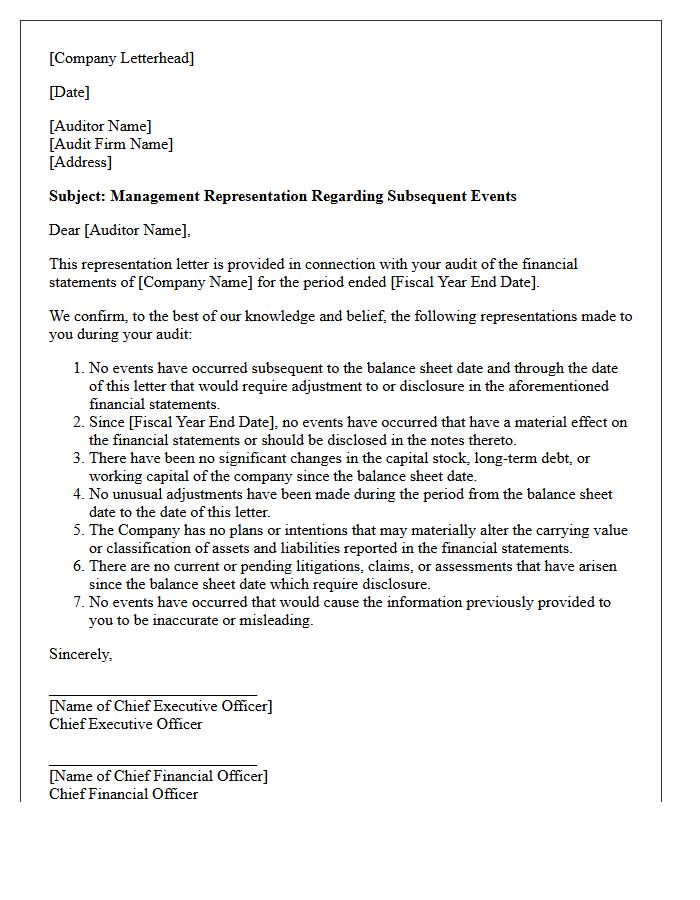

Management Subsequent Events Representation Letter

A Management Subsequent Events Representation Letter is a formal document provided to auditors to confirm that no material developments occurred between the balance sheet date and the audit report issuance. Management must disclose any significant contingent liabilities, changes in equity, or asset impairments that could impact financial statement accuracy. This letter ensures accountability, affirming that all adjustments or disclosures required by accounting frameworks are properly addressed. It serves as essential evidence that the financial health presented remains current and that no major unrecorded transactions jeopardize the audit's reliability.

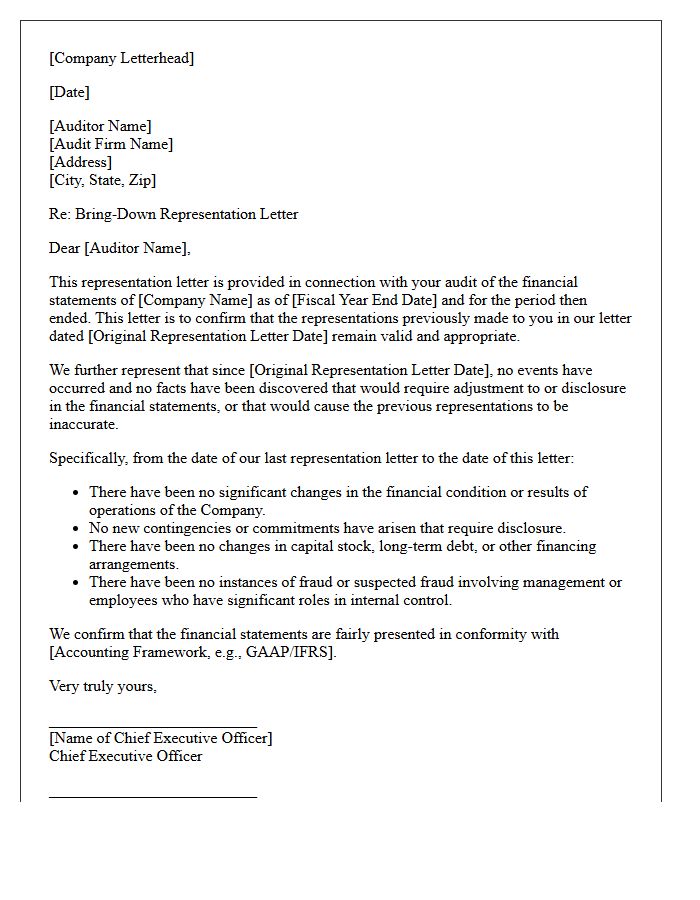

Bring-Down Subsequent Events Representation Letter

A Bring-Down Subsequent Events Representation Letter is a crucial legal document used in financial transactions to confirm that no material changes have occurred since the last audit or reporting period. It serves as an updated certification, ensuring that the financial statements remain accurate and that all relevant subsequent events have been disclosed. This letter provides essential assurance to underwriters or investors, bridging the gap between the initial audit and the closing date of a deal, thereby mitigating risks associated with undisclosed liabilities or significant operational shifts.

Updated Subsequent Events Representation Letter

An updated subsequent events representation letter is a critical audit document providing management's formal confirmation that no material occurrences happened between the balance sheet date and the audit report issuance. This letter of representation bridges the information gap during the final review phase, ensuring all significant financial changes, litigation, or market shifts are disclosed. It serves as essential legal and professional protection for auditors, verifying that the financial statements remain accurate and reflect the company's current standing before public release.

Audit Engagement Subsequent Events Representation Letter

An audit engagement requires a Subsequent Events Representation Letter to confirm significant occurrences between the balance sheet date and the audit report issuance. Management uses this document to formally disclose any material developments, such as litigation settlements, asset impairments, or new debt obligations, that could impact financial statements. This ensures the auditor has written evidence that all adjusting or disclosing events are accurately reflected. Timely identification of these events is essential for maintaining financial transparency and ensuring the integrity of the final audit opinion in compliance with professional standards.

Review Engagement Subsequent Events Representation Letter

The Subsequent Events Representation Letter is a critical document in a review engagement where management confirms no material changes occurred between the balance sheet date and the report issuance. It ensures that any significant financial fluctuations, legal developments, or business risks arising after year-end are properly disclosed. This letter provides written assurance to the practitioner, bridging the information gap during the reporting period. Understanding these events is vital for maintaining financial statement accuracy and ensuring all potential liabilities or assets are transparently communicated to stakeholders before final certification.

Dual-Dated Subsequent Events Representation Letter

A Dual-Dated Subsequent Events Representation Letter is a specific audit document used when a significant event occurs after the original audit report date but before its issuance. This limited re-examination requires auditors to extend their procedures only to that specific item. By using dual-dating, auditors effectively restrict their legal liability for subsequent events to the original date for most financial aspects, while specifically updating the date for the newly disclosed transaction. This ensures financial statements remain accurate without necessitating a full-scope re-audit of the entire reporting period.

Post-Balance Sheet Subsequent Events Representation Letter

The Post-Balance Sheet Subsequent Events Representation Letter is a formal document provided by management to auditors. It confirms that all material events occurring between the balance sheet date and the audit report issuance have been disclosed. This letter ensures the financial statements reflect significant occurrences, such as litigation settlements, asset impairments, or business combinations, that could impact a user's interpretation. By signing this document, management accepts responsibility for the completeness of subsequent event disclosures, providing critical assurance for the integrity of financial reporting and audit accuracy.

Interim Financial Subsequent Events Representation Letter

An Interim Financial Subsequent Events Representation Letter is a formal document issued by management to auditors during a review. It confirms that all material occurrences between the balance sheet date and the report issuance have been disclosed. This letter ensures the integrity of financial statements by accounting for significant developments, such as litigation or asset fluctuations, that might impact investor decisions. It serves as a vital compliance tool, providing legal assurance that the interim data remains accurate, complete, and transparently reflects the company's current fiscal health before final publication.

Short-Form Subsequent Events Representation Letter

A Short-Form Subsequent Events Representation Letter is a legal certification issued by management to auditors or underwriters. It confirms that no material changes have occurred in a company's financial position between the audit report date and the effective date of a registration statement. This document ensures full disclosure of significant events like mergers, litigation, or market shifts. By providing this update, leadership maintains financial transparency and protects stakeholders from outdated information, ensuring the accuracy of all public filings and compliance with accounting standards during securities offerings.

Comprehensive Subsequent Events Representation Letter

A Comprehensive Subsequent Events Representation Letter is a formal document provided by management to auditors during a financial audit. It confirms that all material occurrences between the balance sheet date and the audit report issuance have been disclosed. This letter ensures that significant financial changes, such as lawsuits or asset impairments, are transparently reported to stakeholders. By signing this, management accepts responsibility for the integrity and accuracy of the financial statements, safeguarding the audit process and ensuring compliance with accounting standards regarding events that could impact the company's valuation.

Final Audit Subsequent Events Representation Letter

A Final Audit Subsequent Events Representation Letter is a formal confirmation provided by management to auditors. It ensures that no material events occurred between the balance sheet date and the audit report issuance that could impact financial statements. This document is legally binding, affirming that all significant developments, such as lawsuits or acquisitions, have been disclosed. It provides auditors with essential assurance, bridging the information gap during the final review phase to maintain reporting accuracy and compliance with professional auditing standards.

What is a Subsequent Events Representation Letter?

A Subsequent Events Representation Letter is a formal document provided by management to external auditors confirming whether any significant events occurred between the date of the financial statements and the date of the auditor's report that would require adjustment or disclosure.

Why do auditors require a management representation letter for subsequent events?

Auditors require this letter to obtain written evidence that management has fulfilled its responsibility to identify and disclose all material events occurring after the balance sheet date, ensuring the financial statements are not misleading.

What are the two types of subsequent events covered in the representation letter?

The letter covers Type I events, which provide additional evidence about conditions existing at the balance sheet date (requiring adjustment), and Type II events, which concern conditions that arose after the balance sheet date (requiring disclosure only).

When should the Subsequent Events Representation Letter be signed?

The letter should be signed and dated as close as possible to, but no earlier than, the date of the auditor's report to ensure all events up to the completion of the audit are officially accounted for.

What happens if management refuses to sign the subsequent events representation?

A refusal to provide the requested representations constitutes a scope limitation, which typically prevents the auditor from issuing an unqualified opinion and may result in a disclaimer of opinion or withdrawal from the engagement.

Comments