Evaluate the financial viability of restructuring your home loan with a Mortgage Refinancing Feasibility Advisory Letter. This professional assessment analyzes current interest rates, closing costs, and break-even points to determine if switching lenders saves you money. It provides clear guidance for homeowners seeking to optimize their debt strategy and improve monthly cash flow. Below are some ready to use template.

Image cover: Strategic Mortgage Refinancing: Feasibility Advisory Templates and Professional Letter Samples

Letter Samples List

- Mortgage Refinancing Feasibility Advisory Letter

- Preliminary Refinancing Feasibility Assessment Letter

- Interest Rate Reduction Feasibility Advisory Letter

- Cash-Out Refinancing Feasibility Evaluation Letter

- Commercial Mortgage Refinancing Feasibility Letter

- Residential Mortgage Refinancing Advisory Letter

- Debt Consolidation Refinancing Feasibility Letter

- Home Equity Refinancing Feasibility Advisory Letter

- Refinancing Cost-Benefit Analysis Advisory Letter

- Adjustable Rate Mortgage Refinancing Advisory Letter

- Fixed Rate Mortgage Refinancing Feasibility Letter

- Credit Score Improvement Refinancing Advisory Letter

- Loan Term Modification Feasibility Advisory Letter

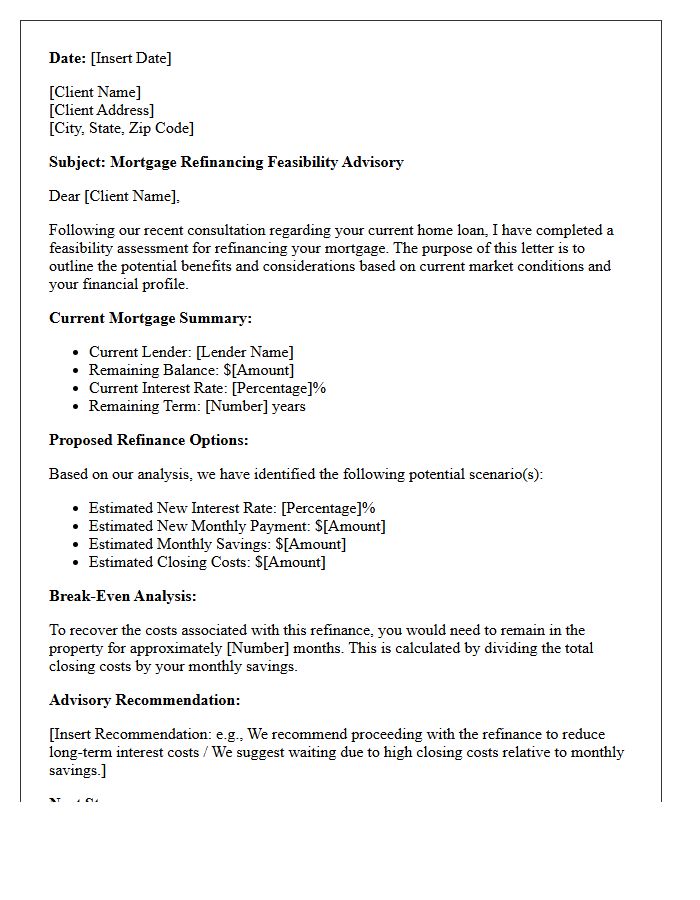

Mortgage Refinancing Feasibility Advisory Letter

A Mortgage Refinancing Feasibility Advisory Letter is a professional assessment determining if restructuring your home loan is financially viable. It analyzes current interest rates, closing costs, and your credit profile to calculate the break-even point. This document ensures that potential monthly savings outweigh the expenses of a new mortgage. By providing an objective feasibility study, the letter helps homeowners avoid unnecessary fees and confirms that refinancing aligns with their long-term financial strategy before committing to the process.

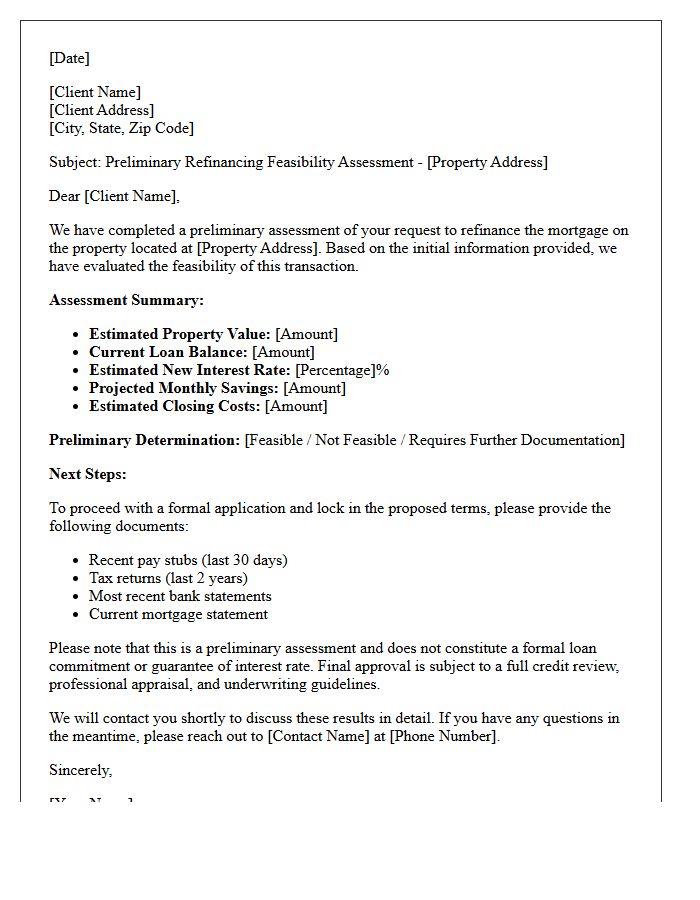

Preliminary Refinancing Feasibility Assessment Letter

A Preliminary Refinancing Feasibility Assessment Letter is a crucial document issued by lenders to evaluate if a borrower qualifies for new loan terms. It provides an early analysis of creditworthiness, property value, and debt-to-income ratios. This non-binding assessment outlines potential savings and updated interest rates, helping homeowners determine the financial viability of replacing an existing mortgage. It serves as a strategic roadmap for the formal application process, ensuring borrowers understand their eligibility and the specific benefits of restructuring their debt before committing to official appraisal costs or legal fees.

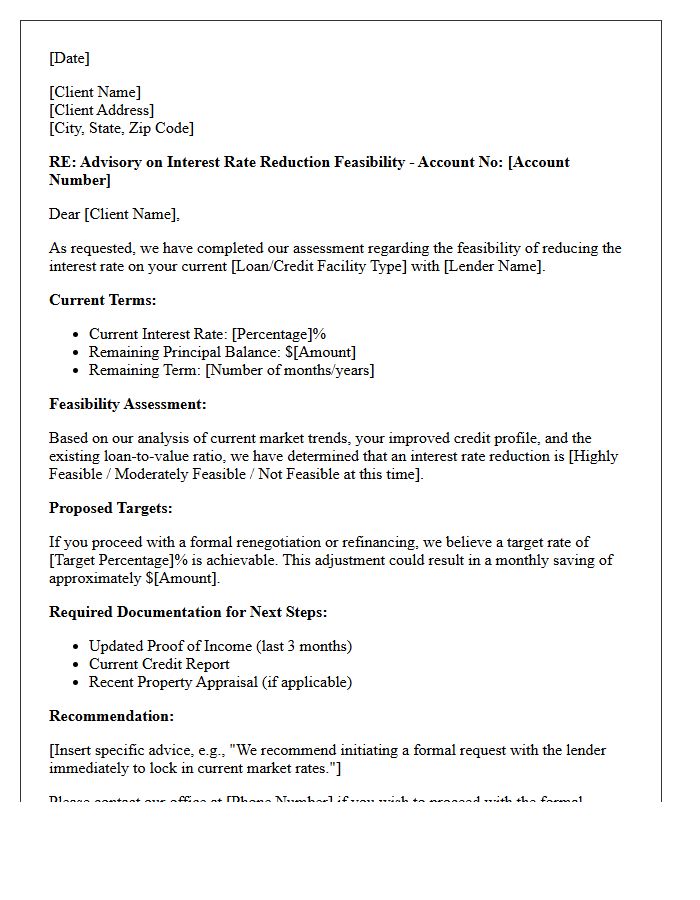

Interest Rate Reduction Feasibility Advisory Letter

An Interest Rate Reduction Feasibility Advisory Letter is a professional assessment used primarily in commercial real estate to determine if refinancing a loan is financially viable. This document analyzes current market trends against your existing debt terms to evaluate potential savings. It serves as a critical due diligence tool for borrowers, helping them decide whether to pursue a formal rate reduction application. By reviewing prepayment penalties and closing costs, the letter provides a clear cost-benefit analysis to ensure the new financing structure aligns with your long-term investment strategy.

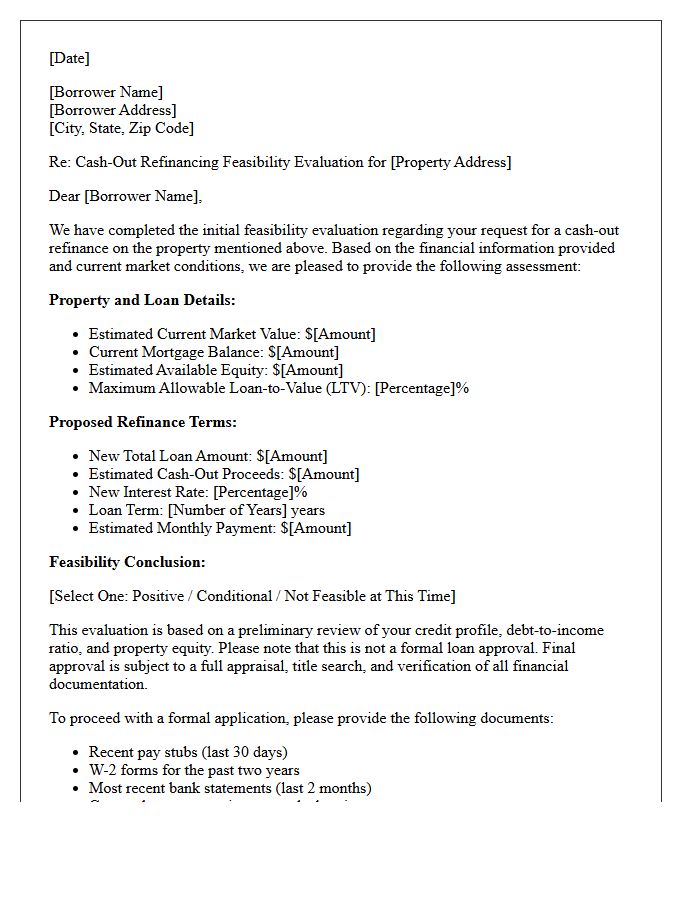

Cash-Out Refinancing Feasibility Evaluation Letter

A Cash-Out Refinancing Feasibility Evaluation Letter is a formal document used to determine if a borrower qualifies to replace their existing mortgage with a larger loan. This assessment analyzes the property's current equity, the borrower's creditworthiness, and debt-to-income ratios. It serves as a preliminary roadmap, outlining potential loan-to-value limits and estimated net proceeds. Obtaining this letter is essential for homeowners to confirm they meet specific lender criteria before committing to the full application process for accessing liquid capital from their home investment.

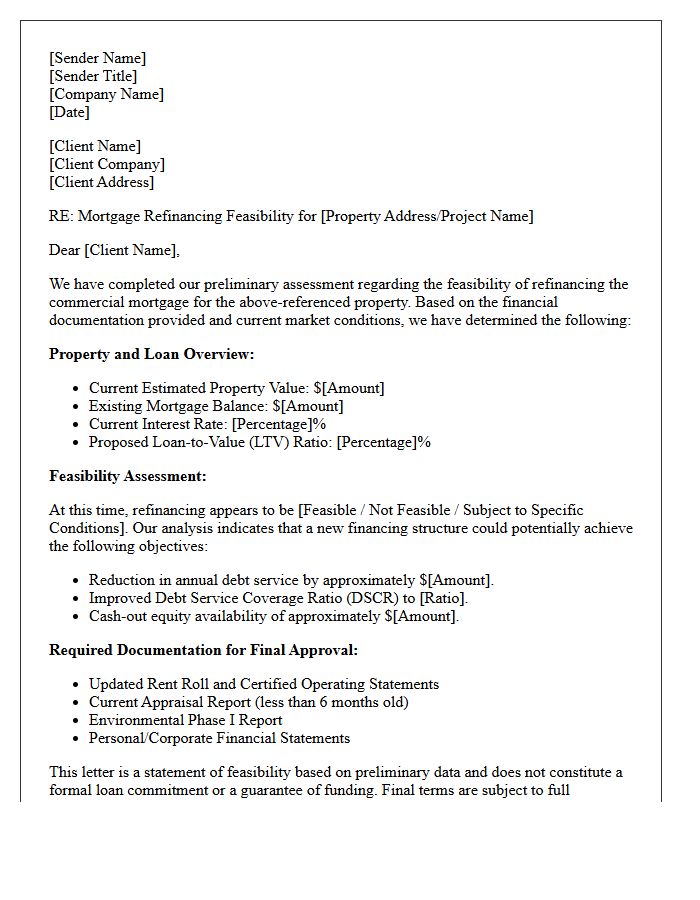

Commercial Mortgage Refinancing Feasibility Letter

A Commercial Mortgage Refinancing Feasibility Letter is a preliminary assessment issued by a lender to evaluate the viability of a new loan. It outlines potential terms, interest rates, and loan-to-value ratios based on the property's current financial performance. This document acts as a non-binding roadmap, helping investors determine if restructuring existing debt is profitable before committing to formal application fees. Understanding the net operating income and debt service coverage ratio highlighted in this letter is essential for securing favorable long-term financing strategies.

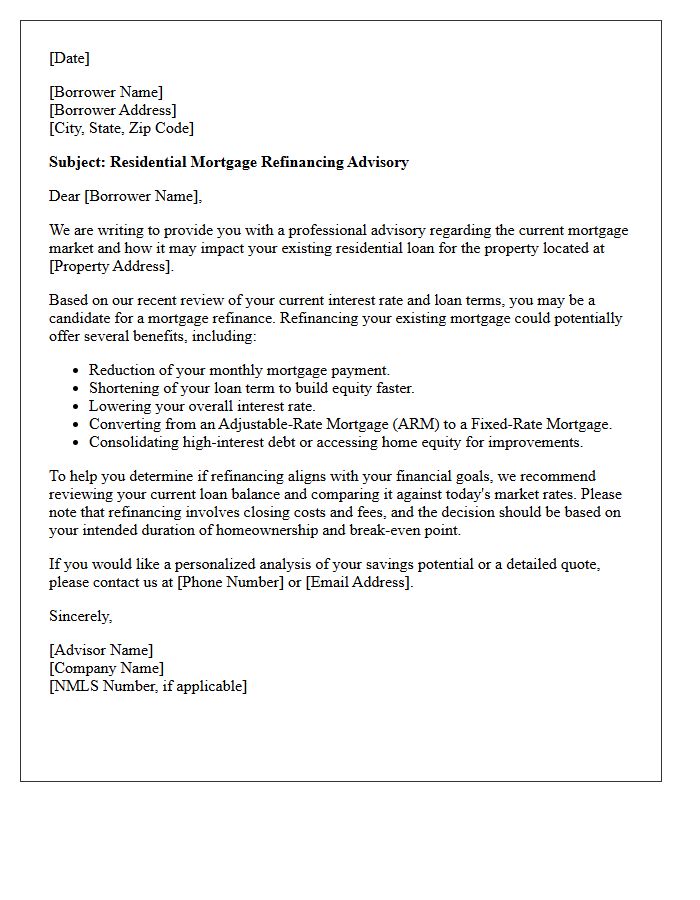

Residential Mortgage Refinancing Advisory Letter

A Residential Mortgage Refinancing Advisory Letter provides strategic financial guidance to homeowners seeking better loan terms. This document typically analyzes your current debt structure against current market interest rates to determine potential savings. It highlights essential factors like closing costs, break-even points, and equity requirements. Understanding this letter is crucial for making an informed decision on whether to replace an existing mortgage with a new loan agreement to reduce monthly payments or shorten the repayment period effectively.

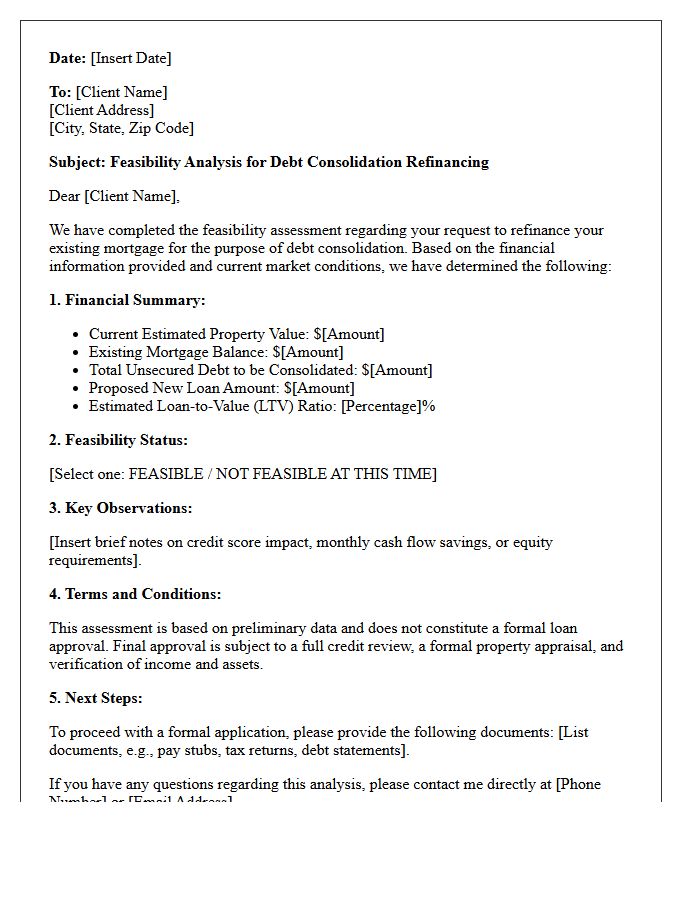

Debt Consolidation Refinancing Feasibility Letter

A Debt Consolidation Refinancing Feasibility Letter is a formal document used to assess whether restructuring multiple liabilities into a single mortgage loan is viable. It evaluates your creditworthiness, current equity, and debt-to-income ratio to determine potential interest savings. Lenders use this analysis to verify if the new loan provides a net tangible benefit to the borrower. Obtaining this letter is a critical preliminary step to ensure that refinancing will effectively lower monthly payments and improve overall financial stability before committing to the process.

Home Equity Refinancing Feasibility Advisory Letter

A Home Equity Refinancing Feasibility Advisory Letter is a critical document used to evaluate your financial eligibility for restructuring mortgage debt. This professional assessment analyzes current loan-to-value ratios, creditworthiness, and prevailing market rates to determine if tapping into property equity is a viable strategy. It serves as a formal roadmap for homeowners seeking to consolidate debt or secure liquid capital. By reviewing this advisory, borrowers can make informed decisions regarding equity extraction while ensuring long-term fiscal stability and understanding the potential risks or benefits associated with new refinancing terms.

Refinancing Cost-Benefit Analysis Advisory Letter

A Refinancing Cost-Benefit Analysis Advisory Letter is a critical document used to evaluate the financial viability of replacing an existing loan. It provides a quantitative comparison between current debt obligations and proposed terms, accounting for closing costs, break-even points, and interest rate differentials. This professional assessment ensures borrowers understand if the long-term savings outweigh the upfront expenses. By analyzing the net present value of the transaction, the letter acts as a strategic guide for informed decision-making, helping to mitigate financial risk and maximize liquidity during the mortgage or loan restructuring process.

Adjustable Rate Mortgage Refinancing Advisory Letter

An Adjustable Rate Mortgage Refinancing Advisory Letter is a formal notification sent by lenders to inform borrowers of upcoming changes to their loan terms. This document details your new interest rate, updated monthly payment amounts, and the specific effective date of these adjustments. Understanding this letter is vital for financial planning, as it helps you decide whether to maintain your current loan or pursue refinancing to secure a stable fixed-rate mortgage. Reviewing these updates promptly ensures you avoid payment shocks and maintain long-term housing affordability.

Fixed Rate Mortgage Refinancing Feasibility Letter

A Fixed Rate Mortgage Refinancing Feasibility Letter is a formal document used to determine if replacing your current loan is financially beneficial. It analyzes your existing interest rate against current market trends to calculate potential long-term savings. Lenders provide this assessment to verify that the net tangible benefit justifies the closing costs. Understanding this letter helps homeowners decide if switching to a new fixed-rate term will effectively lower monthly payments or reduce total debt. It serves as a crucial financial viability check before proceeding with the formal application process.

Credit Score Improvement Refinancing Advisory Letter

A Credit Score Improvement Refinancing Advisory Letter provides a strategic roadmap for borrowers to enhance their creditworthiness before finalizing a loan. This document highlights specific actions, such as debt consolidation and timely payments, to boost ratings. By following these professional recommendations, homeowners can secure lower interest rates and better terms during the refinancing process. Understanding these guidelines is essential for maximizing long-term financial savings and ensuring a successful application outcome.

Loan Term Modification Feasibility Advisory Letter

A Loan Term Modification Feasibility Advisory Letter is a professional assessment evaluating if a borrower qualifies for restructured mortgage terms. This document analyzes financial stability, hardship documentation, and debt-to-income ratios to determine the likelihood of lender approval. It serves as a strategic roadmap for homeowners seeking to lower interest rates or extend repayment periods. By providing a formal feasibility analysis, the letter helps borrowers understand their eligibility before entering formal negotiations, ensuring they present a compelling case to mitigate the risk of foreclosure and improve long-term affordability.

What is a Mortgage Refinancing Feasibility Advisory Letter?

A Mortgage Refinancing Feasibility Advisory Letter is a professional assessment issued by a financial advisor or lending specialist that evaluates whether replacing your current mortgage with a new loan is financially viable based on current market rates, closing costs, and your long-term financial goals.

How does a feasibility advisory letter help in the refinancing process?

This letter provides a detailed break-even analysis, comparing your current monthly payments and total interest costs against the projected terms of a new loan. It helps borrowers determine if the potential savings outweigh the upfront costs associated with refinancing, such as appraisal fees and title insurance.

What key metrics are included in a refinancing feasibility report?

The advisory letter typically highlights the Net Present Value (NPV) of the refinance, the monthly cash flow impact, the total interest savings over the life of the loan, and the "break-even point"-the specific month where the accumulated savings surpass the initial closing costs.

When should a homeowner request a refinancing feasibility advisory letter?

Homeowners should request this advisory letter when market interest rates drop significantly, when their credit score improves, or when they wish to change their loan structure, such as switching from an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Mortgage.

Is a feasibility advisory letter a guarantee of loan approval?

No, a feasibility advisory letter is an analytical tool used for decision-making and planning purposes. While it demonstrates the logic behind a refinance, the borrower must still undergo a formal underwriting process, including income verification and property appraisal, to secure final loan approval.

Comments