Streamline your financial verification process with a professional Asset Management and Investment Holding Audit Confirmation Letter. These documents are essential for verifying portfolio valuations, ownership, and transaction accuracy during annual audits. Ensuring precise communication between auditors and fund managers maintains regulatory compliance and transparency. To simplify your workflow, below are some ready to use template options.

Image cover: Streamlined Audit Confirmation Templates for Asset Management and Investment Holdings

Letter Samples List

- Bank Account Balance Audit Confirmation Letter

- Investment Securities Holding Audit Confirmation Letter

- Collateral and Pledged Asset Audit Confirmation Letter

- Derivative Instrument and Forward Contract Audit Confirmation Letter

- Custodial Trust Account Audit Confirmation Letter

- Credit Facility and Outstanding Loan Audit Confirmation Letter

- Escrow Account Balance Audit Confirmation Letter

- Managed Portfolio Asset Audit Confirmation Letter

- Contingent Liability and Guarantee Audit Confirmation Letter

- Promissory Note and Commercial Paper Audit Confirmation Letter

- Dividend and Interest Income Audit Confirmation Letter

- Related Party Transaction Audit Confirmation Letter

- Mutual Fund Holding Audit Confirmation Letter

- Subordinated Debt Audit Confirmation Letter

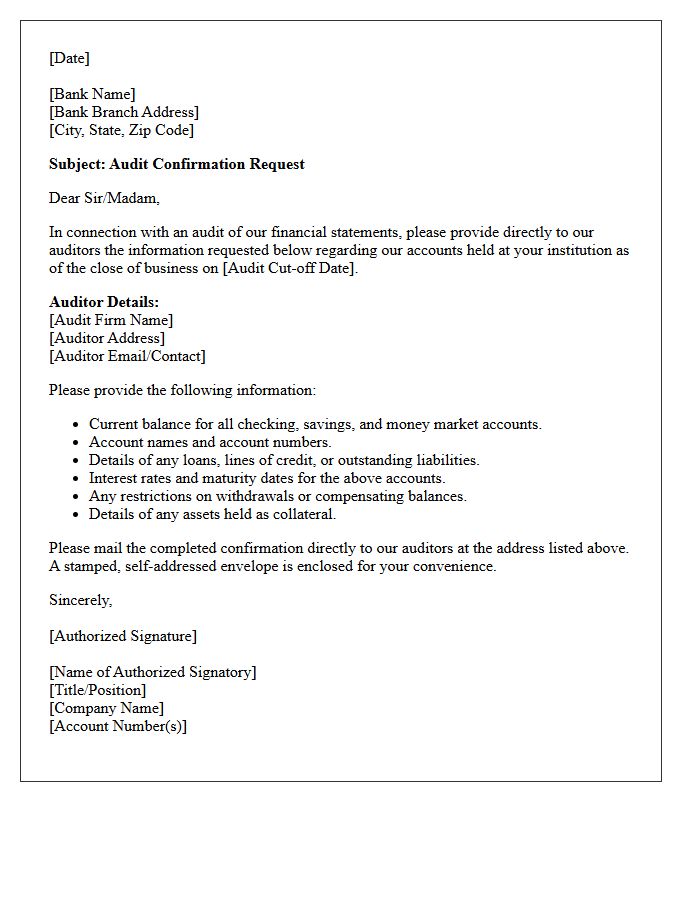

Bank Account Balance Audit Confirmation Letter

A Bank Account Balance Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify the accuracy of a company's financial records. This process is essential for independent verification of cash balances, loans, and contingent liabilities. It ensures that the assets reported on the balance sheet actually exist and are correctly valued. By mitigating risks of fraud or accounting errors, this document provides critical audit evidence necessary for issuing an accurate financial opinion on a business's fiscal health and transparency.

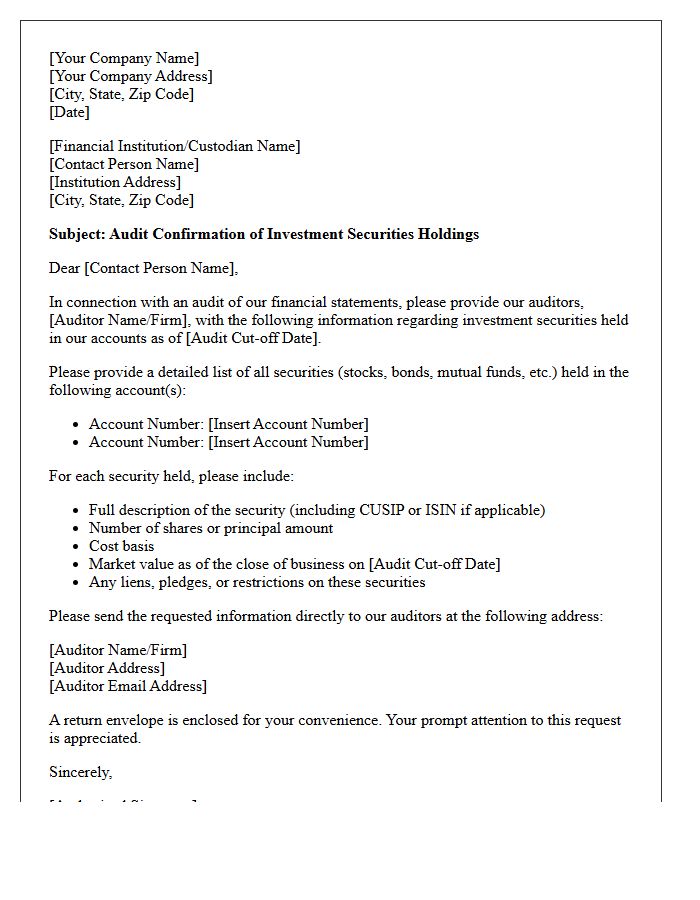

Investment Securities Holding Audit Confirmation Letter

An Investment Securities Holding Audit Confirmation Letter is a formal request sent by auditors to financial custodians to verify the existence and ownership of assets. This third-party verification is crucial for ensuring that the investment balances reported on a company's balance sheet are accurate and free from material misstatement. It confirms key details such as quantity, security type, and potential encumbrances. Providing this evidence maintains financial transparency and helps prevent fraud by reconciling internal records with external institutional data during the year-end audit process.

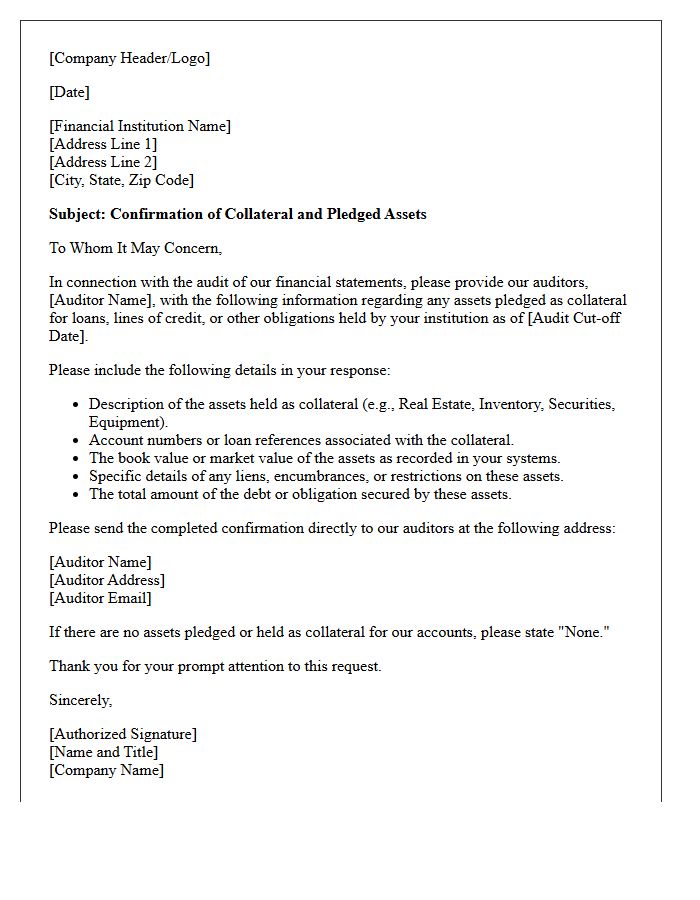

Collateral and Pledged Asset Audit Confirmation Letter

A collateral and pledged asset audit confirmation letter is a vital document used by auditors to verify the existence and valuation of assets securing a loan. It ensures that third-party custodians or lenders confirm the specific details of pledged securities, property, or cash. This process mitigates risks of fraud and reporting errors by validating that the assets are legally encumbered and accurately reflected on the financial statements. Timely responses are essential for maintaining audit integrity and ensuring compliance with financial transparency standards during the verification phase.

Derivative Instrument and Forward Contract Audit Confirmation Letter

A derivative instrument audit confirmation is a vital control procedure used to verify the existence, terms, and valuation of financial contracts. Auditors send these requests to counterparties to validate notional amounts, expiration dates, and fair market values. For a forward contract, the letter specifically confirms the agreed-upon exchange price and delivery date for an underlying asset. This independent verification ensures financial statements accurately reflect potential liabilities and hedging activities, mitigating risks of material misstatement or undisclosed financial obligations during the year-end reporting process.

Custodial Trust Account Audit Confirmation Letter

A Custodial Trust Account Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify the existence, balance, and legal ownership of assets held in trust. This process ensures the accuracy of financial statements and confirms that the custodian is managing funds according to fiduciary responsibilities. It serves as a critical internal control to prevent fraud and unauthorized asset movement. Receiving a timely response is essential for completing a compliance audit and validating the integrity of trust account data for stakeholders and regulatory bodies.

Credit Facility and Outstanding Loan Audit Confirmation Letter

A credit facility audit confirmation is a formal document used to verify the accuracy of reported financial data. It ensures that the outstanding loan balance, interest rates, and repayment terms recorded in a company's books match the lender's records. This process is essential for financial transparency, helping auditors detect discrepancies or undisclosed liabilities. Companies must respond promptly to these requests to maintain regulatory compliance and provide stakeholders with a verified snapshot of their current debt obligations and overall credit availability.

Escrow Account Balance Audit Confirmation Letter

An Escrow Account Balance Audit Confirmation Letter is a formal request sent by auditors to verify the accuracy of funds held in trust. It ensures that the recorded balance matches the actual amount held by the financial institution. This process is critical for maintaining financial transparency and preventing fraud during real estate transactions or corporate mergers. The third-party verification provides independent evidence that escrow assets are properly managed and accounted for, protecting all stakeholders involved in the agreement from reporting errors or unauthorized fund disbursements.

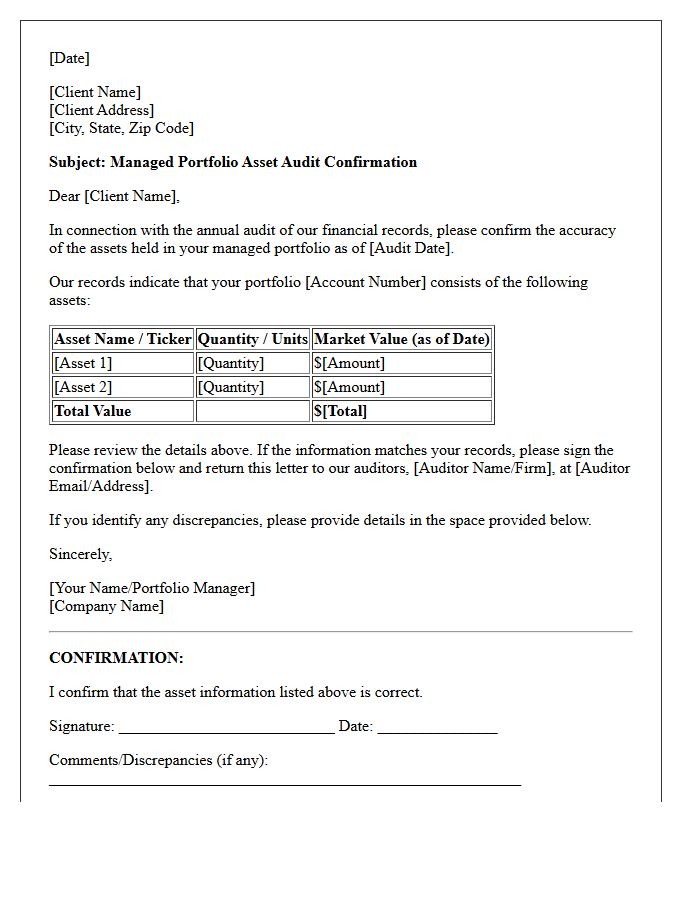

Managed Portfolio Asset Audit Confirmation Letter

A Managed Portfolio Asset Audit Confirmation Letter is a formal verification document used to validate the existence and value of investment holdings. Sent by independent auditors to financial custodians, it ensures that reported account balances and security positions are accurate. This process is essential for regulatory compliance and fraud prevention, providing investors with third-party assurance that their portfolio's financial statements are reliable. By confirming ownership and market valuations, these letters maintain transparency and fiduciary integrity within institutional and private wealth management frameworks.

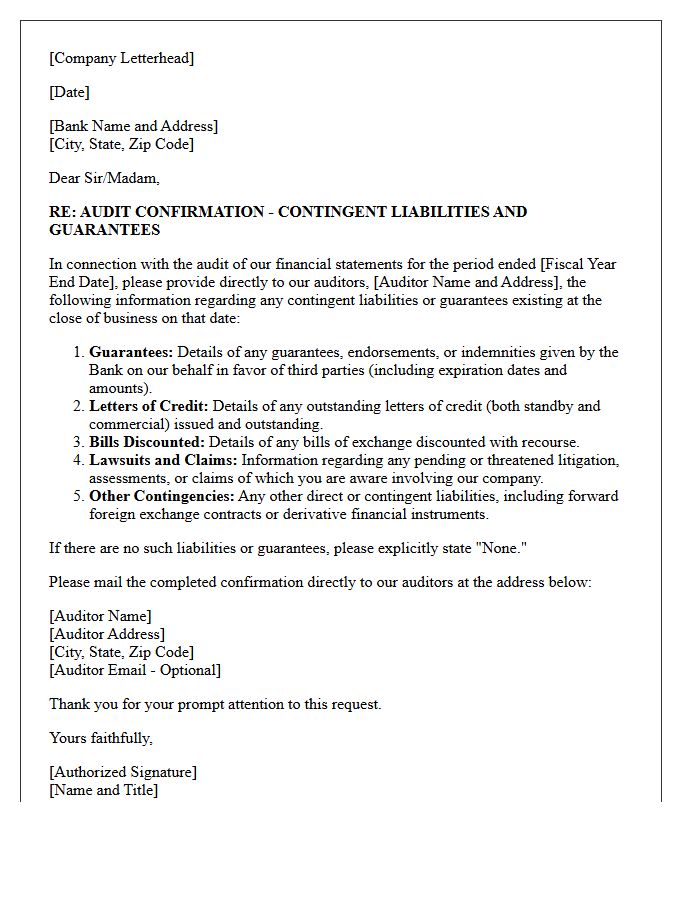

Contingent Liability and Guarantee Audit Confirmation Letter

A Contingent Liability and Guarantee Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify potential obligations. This document ensures the accuracy of reported off-balance sheet items, such as pending lawsuits or loan guarantees, which may become actual debts depending on future events. By confirming these contingent liabilities directly with third parties, auditors mitigate the risk of financial misstatement. It is a critical component of financial transparency, helping stakeholders understand the true scope of a company's financial exposure and risk management practices.

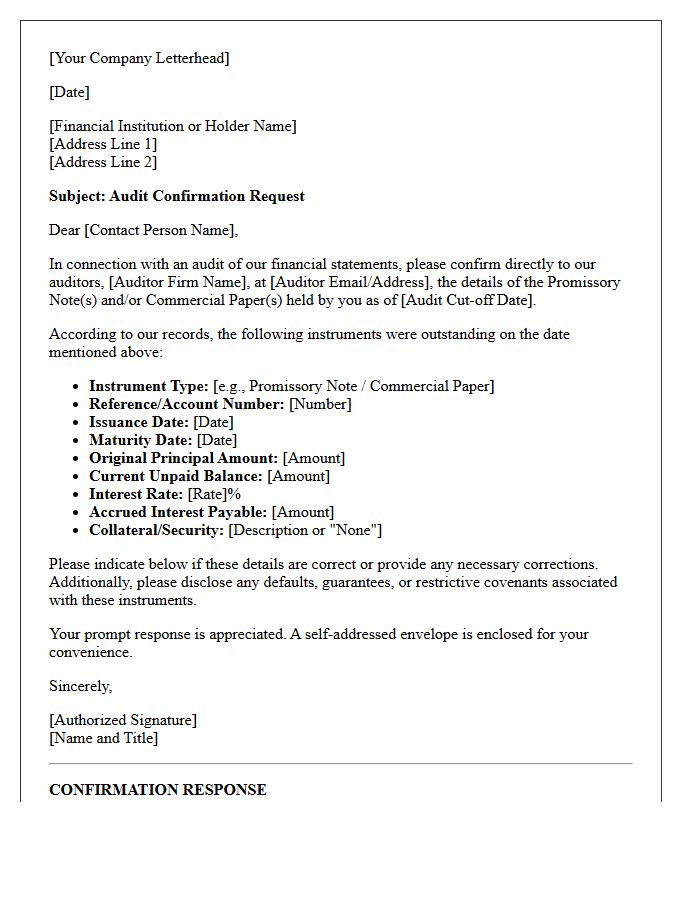

Promissory Note and Commercial Paper Audit Confirmation Letter

A Promissory Note and Commercial Paper Audit Confirmation Letter is a critical document used by auditors to verify the existence and accuracy of debt obligations. This formal inquiry ensures that reported balances, interest rates, and maturity dates align with the lender's records. By confirming these financial details directly with third parties, organizations provide independent evidence of their liabilities. This process is essential for maintaining transparent financial reporting, preventing fraud, and ensuring that all short-term debt instruments are recorded correctly on a company's balance sheet according to accounting standards.

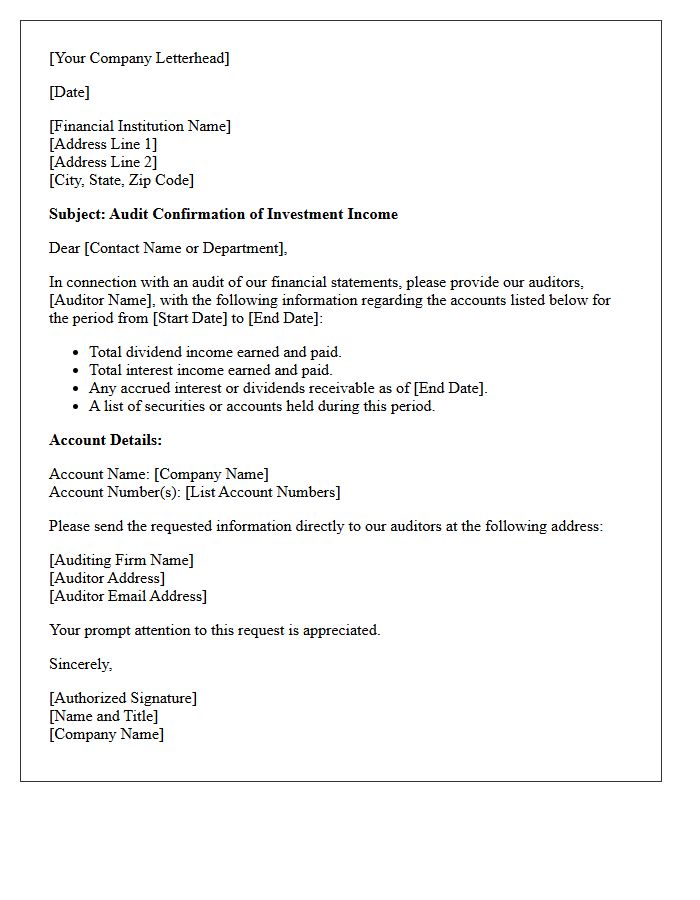

Dividend and Interest Income Audit Confirmation Letter

A Dividend and Interest Income Audit Confirmation Letter is a formal request sent by auditors to financial institutions to verify the accuracy of reported investment earnings. This process ensures that investment income recorded in financial statements matches the actual payments received. By validating yields, tax withholdings, and account balances, auditors mitigate risks of fraud or reporting errors. This third-party verification is a critical control measure used to confirm the existence and valuation of assets, providing stakeholders with assurance regarding the integrity of an organization's financial disclosures.

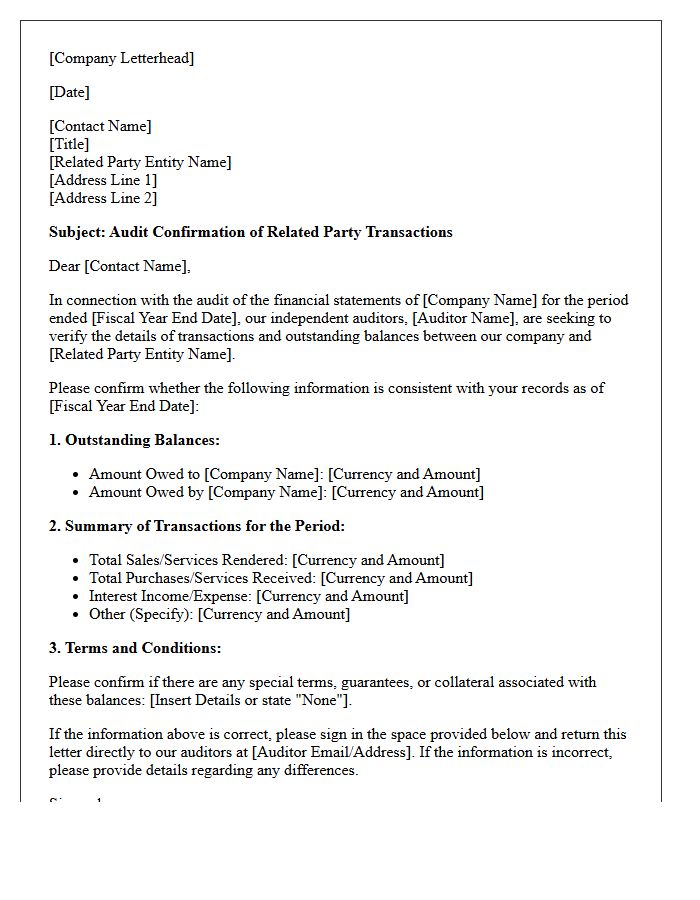

Related Party Transaction Audit Confirmation Letter

A Related Party Transaction Audit Confirmation Letter is a compliance document used by auditors to verify the accuracy and completeness of dealings between a company and its affiliates, directors, or major shareholders. This external verification helps identify potential conflicts of interest and ensures that financial reporting adheres to accounting standards. By confirming terms, balances, and the commercial substance of these interactions, the letter mitigates risks of fraud and material misstatement. Accurate disclosure is essential for maintaining transparency and protecting the interests of external stakeholders within the corporate governance framework.

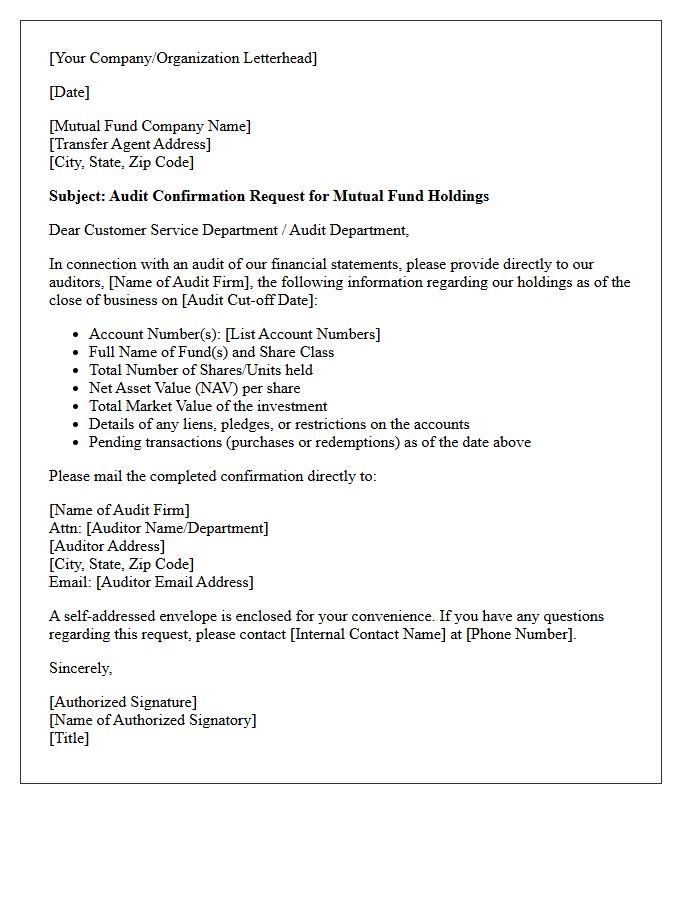

Mutual Fund Holding Audit Confirmation Letter

A Mutual Fund Holding Audit Confirmation Letter is a formal document used to verify the existence and accuracy of investment positions. Auditors send these requests to fund managers to independently confirm the asset balance, share count, and valuation as of a specific date. This process is a critical internal control that prevents financial misstatement and ensures transparency for stakeholders. By reconciling third-party data with internal records, the audit confirmation mitigates fraud risk and ensures the investment portfolio is reported at its true fair market value within financial statements.

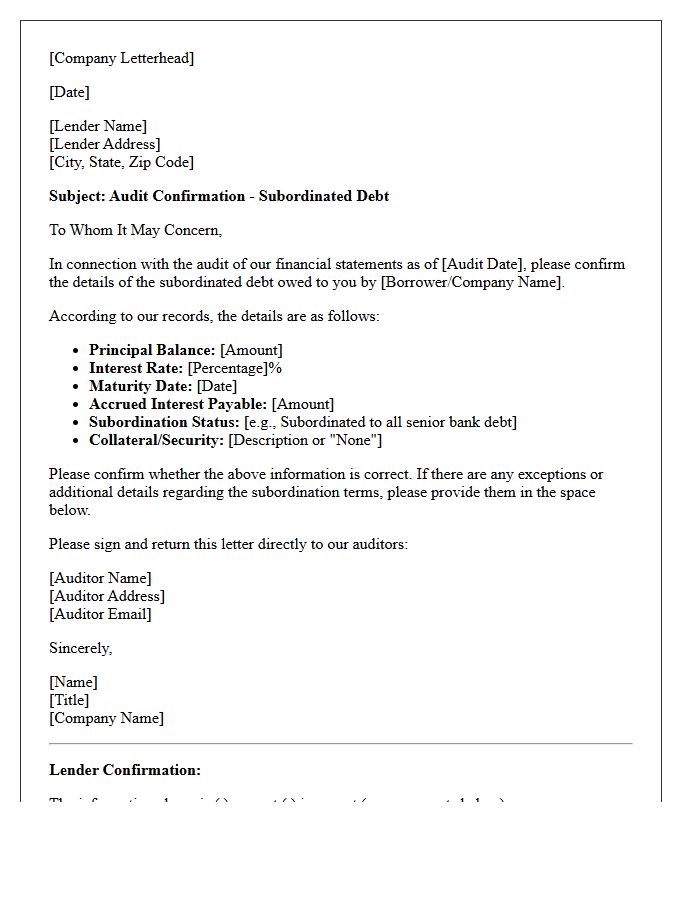

Subordinated Debt Audit Confirmation Letter

A Subordinated Debt Audit Confirmation Letter is a critical document used by auditors to verify the existence, terms, and balance of junior debt obligations. It confirms that the lender agrees to be paid only after senior creditors are satisfied. This process ensures financial statements accurately reflect liabilities and compliance with debt seniority agreements. Auditors use this third-party verification to mitigate financial risk, detect reporting errors, and confirm that the company maintains required capital ratios. Accurate confirmation is essential for transparency in complex corporate financing and regulatory audits.

What is an audit confirmation letter for asset management and investment holdings?

An audit confirmation letter is a formal request sent by an external auditor to a financial institution or investment manager to verify the existence, ownership, and valuation of assets held under management as of a specific reporting date.

Which specific details are verified in an investment holding confirmation?

The confirmation typically verifies account balances, quantity of shares or units held, asset valuations, pending trades, accrued interest, dividend income, and any encumbrances or liens against the investment portfolio.

Why are third-party confirmations essential for asset management audits?

Third-party confirmations provide high-quality, independent evidence that mitigates the risk of material misstatement, ensuring that the assets reported on the balance sheet actually exist and are accurately valued according to market standards.

How are "alternative investments" like private equity or hedge funds confirmed?

For alternative investments where public market prices may not be available, the confirmation focuses on the capital commitment, total contributions, distributions, and the Net Asset Value (NAV) provided by the fund manager or administrator.

What is the difference between a positive and negative audit confirmation in this context?

A positive confirmation requires the investment holder to respond whether they agree or disagree with the stated balance, whereas a negative confirmation only requires a response if the recipient disagrees with the provided account information.

Comments