A Demand for Payment From Guarantor is a formal legal notice issued when a primary borrower defaults on their financial obligations. This request holds the co-signer accountable for the outstanding debt according to the signed guarantee agreement. Understanding the correct procedure ensures legal compliance and effective debt recovery. To help you draft a professional notice, below are some ready to use template.

Image cover: Professional Demand for Payment Templates for Guarantors

Letter Samples List

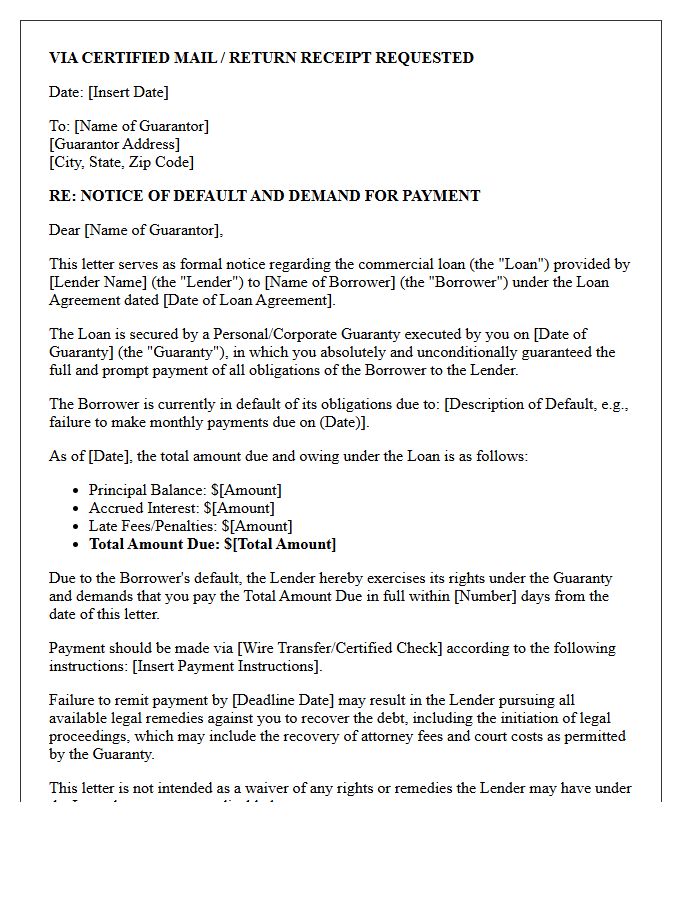

- Initial Commercial Loan Default Guarantor Demand Letter

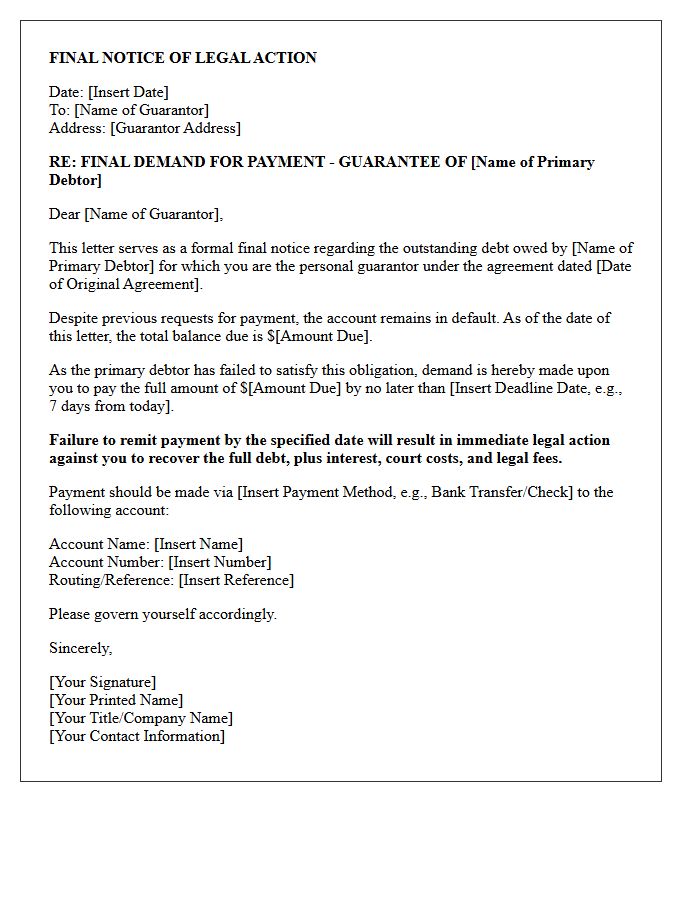

- Final Notice Of Legal Action Guarantor Payment Demand Letter

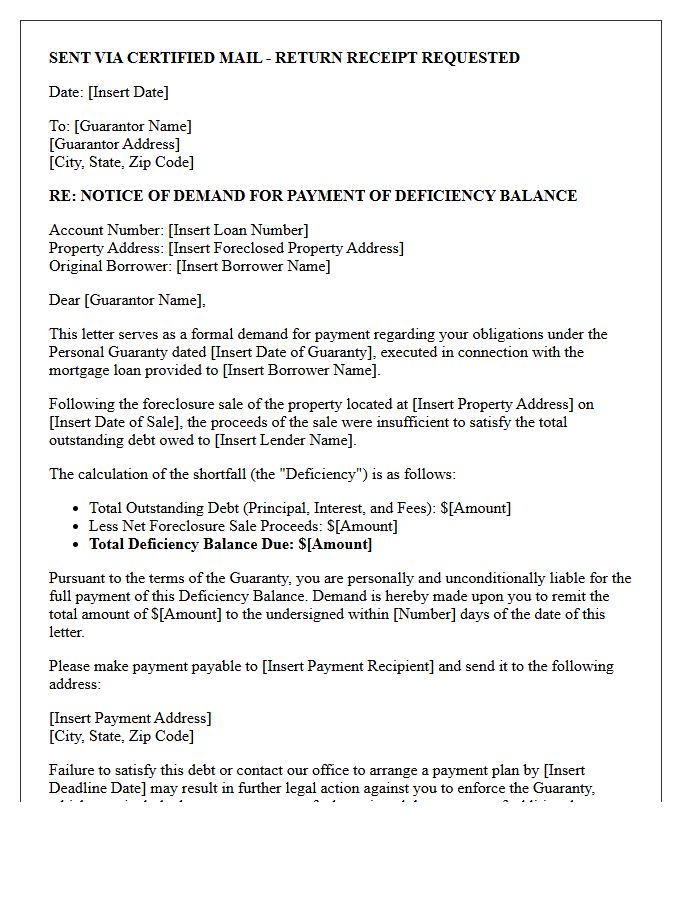

- Mortgage Foreclosure Shortfall Guarantor Demand Letter

- Corporate Overdraft Facility Guarantor Payment Demand Letter

- Principal Borrower Bankruptcy Guarantor Demand Letter

- Post-Liquidation Deficiency Guarantor Demand Letter

- Small Business Loan Default Guarantor Demand Letter

- Vehicle Repossession Balance Guarantor Demand Letter

- Unsecured Personal Loan Guarantor Payment Demand Letter

- Loan Acceleration And Guarantor Payment Demand Letter

- Syndicated Loan Default Guarantor Demand Letter

- Construction Loan Arrears Guarantor Demand Letter

Initial Commercial Loan Default Guarantor Demand Letter

An Initial Commercial Loan Default Guarantor Demand Letter is a critical legal notice issued when a borrower fails to meet repayment obligations. This formal document notifies the individual or entity providing the guaranty that they are now personally liable for the outstanding debt. It serves as a mandatory precursor to litigation, outlining the specific default event, the total amount due, and a strict deadline for payment. Receiving this letter signifies that the lender is accelerating the debt, making it essential to seek legal counsel to protect personal assets from foreclosure or collection actions.

Final Notice Of Legal Action Guarantor Payment Demand Letter

A Final Notice of Legal Action is a critical formal demand issued to a guarantor after a primary borrower defaults. It serves as the last warning before a lawsuit is initiated to recover the outstanding debt. Recipients must understand that their personal assets are at risk due to the legally binding guarantee agreement. To avoid court costs, interest, and credit damage, immediate payment or a structured settlement is required. This document signifies that the creditor has exhausted informal collection methods and is prepared to pursue litigation to enforce payment obligations.

Mortgage Foreclosure Shortfall Guarantor Demand Letter

A Mortgage Foreclosure Shortfall Guarantor Demand Letter is a formal legal notice issued by a lender after a property sale fails to cover the total debt. This document targets the guarantor, demanding payment for the remaining balance, known as the deficiency. It outlines the specific shortfall amount, accrued interest, and legal fees owed under the guarantee agreement. Receiving this letter indicates that the lender is pursuing personal assets to satisfy the loan. Timely legal consultation is critical to negotiate a settlement or verify the deficiency judgment accuracy before further litigation begins.

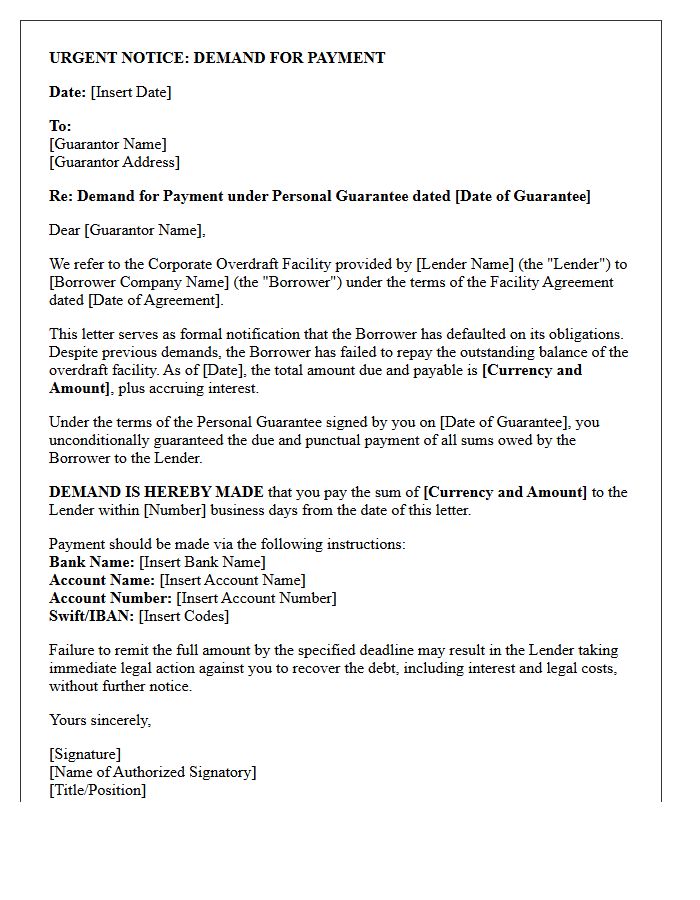

Corporate Overdraft Facility Guarantor Payment Demand Letter

A corporate overdraft facility guarantor payment demand letter is a formal legal notice issued by a lender to a guarantor. This document serves as a final demand for immediate repayment when a business fails to clear its debt. It signifies that the primary borrower has defaulted and the bank is now exercising its right to recover funds from the individual's assets. Receiving this letter is a critical legal trigger that may lead to litigation or asset seizure if the outstanding balance is not settled within the specified timeframe.

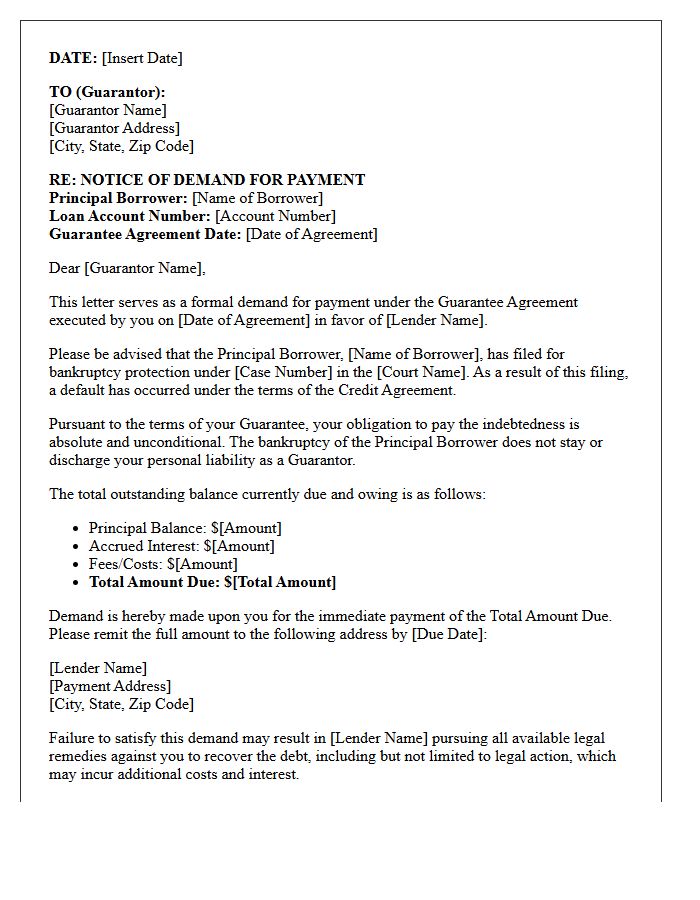

Principal Borrower Bankruptcy Guarantor Demand Letter

A Principal Borrower Bankruptcy Guarantor Demand Letter is a formal legal notice issued when a primary debtor declares insolvency. It informs the guarantor that their secondary liability has become an immediate obligation. Even if the borrower is protected by a bankruptcy stay, the lender may still pursue the guarantor for the full outstanding balance. Understanding the acceleration clause is vital, as it often requires total repayment within a strict timeframe. This document serves as a final prerequisite before initiating legal action or litigation against the guarantor's personal assets.

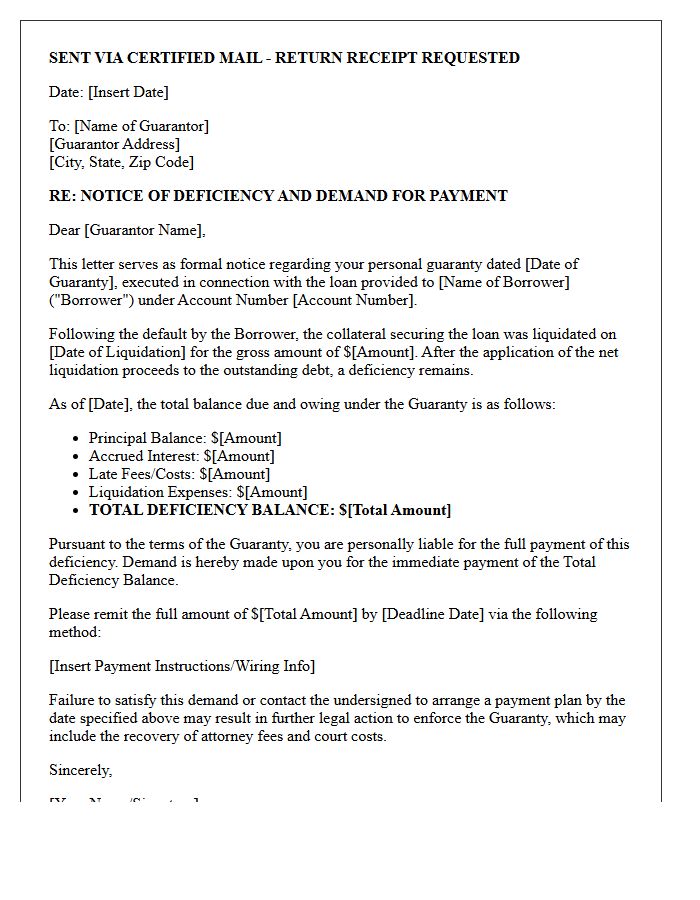

Post-Liquidation Deficiency Guarantor Demand Letter

A Post-Liquidation Deficiency Guarantor Demand Letter is a formal legal notice issued after collateral liquidation fails to cover the total debt. It informs the guarantor that a remaining balance exists and demands immediate payment. This document is critical because it establishes the legal basis for recovery actions against personal assets. Receving this letter marks the final opportunity to settle the deficiency or negotiate a workout before the lender initiates formal litigation or collection proceedings to satisfy the outstanding financial obligation.

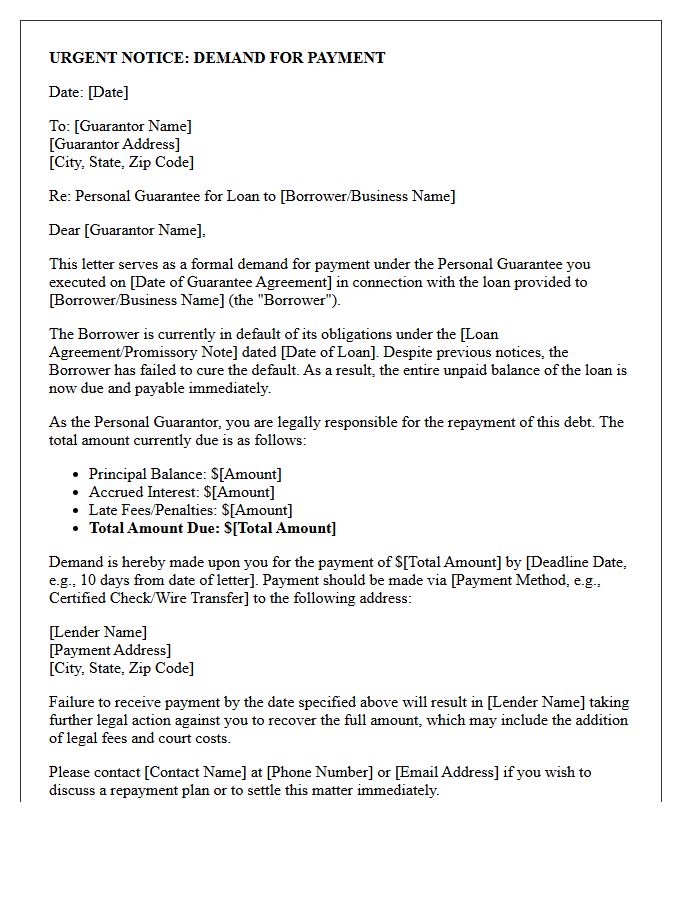

Small Business Loan Default Guarantor Demand Letter

A Small Business Loan Default Guarantor Demand Letter is a formal legal notice issued when a borrower fails to repay a debt. It targets the personal guarantor, demanding immediate payment of the outstanding balance. This letter serves as a critical pre-litigation step, notifying the individual that their personal assets are now at risk due to the primary borrower's default. Receiving this document signifies that the lender is initiating acceleration of the debt, meaning the entire loan amount is due before further legal action or asset seizure occurs.

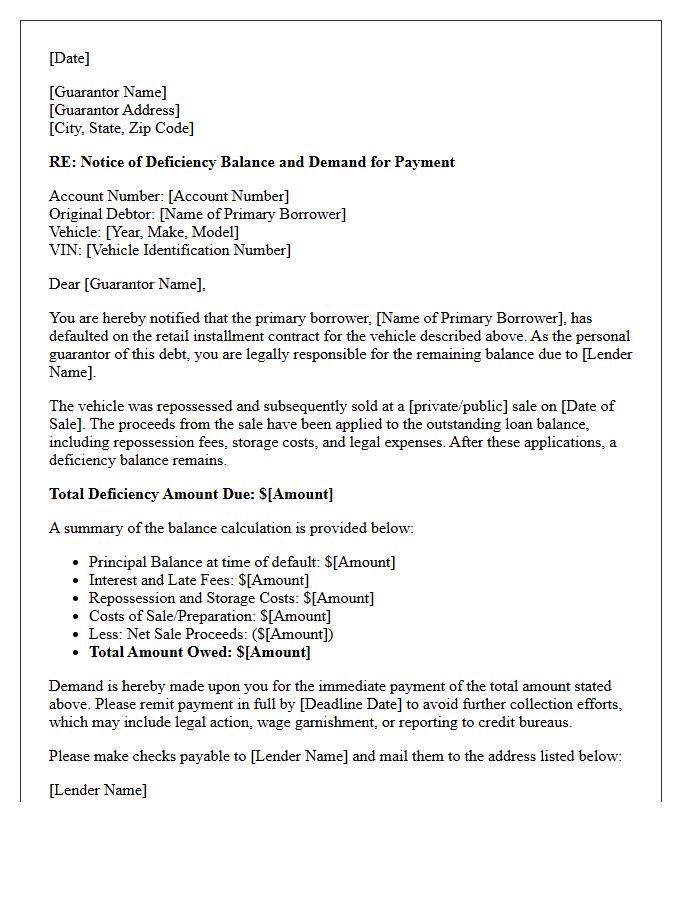

Vehicle Repossession Balance Guarantor Demand Letter

A Vehicle Repossession Balance Guarantor Demand Letter is a formal legal notice sent to a co-signer or guarantor after a vehicle is sold at auction. It demands payment for the deficiency balance, which is the remaining debt after the sale proceeds are applied to the loan. This document outlines the total amount due, including late fees and repossession costs. Failure to settle this outstanding liability can result in legal action, wage garnishment, or severe damage to the guarantor's credit score, as they are equally responsible for the contract.

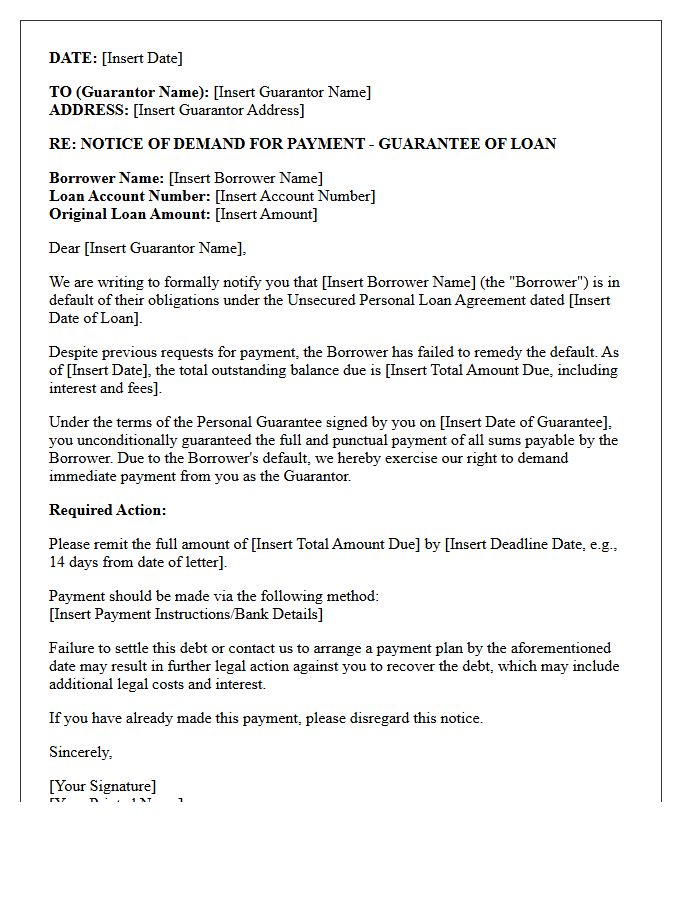

Unsecured Personal Loan Guarantor Payment Demand Letter

An Unsecured Personal Loan Guarantor Payment Demand Letter is a formal legal notice issued when a primary borrower defaults. It officially informs the guarantor of their legal obligation to settle the outstanding debt. Since the loan lacks collateral, the lender pursues the guarantor's personal assets for recovery. Receiving this document signifies that the grace period has ended and immediate action is required to avoid litigation or severe credit score damage. Understanding the specific repayment terms and deadlines outlined in the letter is essential for protecting your financial standing and legal rights.

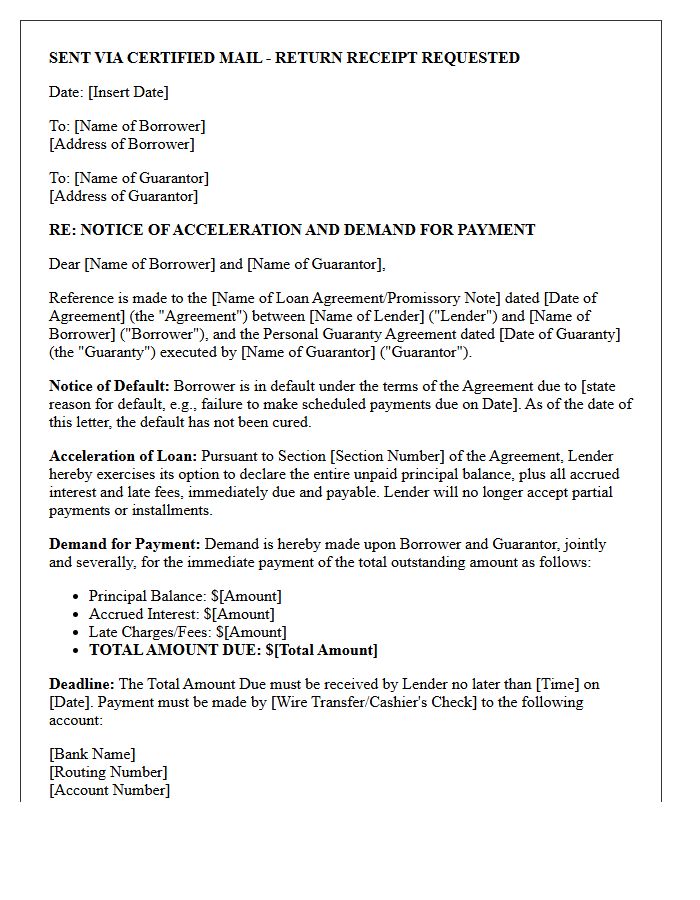

Loan Acceleration And Guarantor Payment Demand Letter

A Loan Acceleration notice is a formal legal demand that matures the entire debt immediately, typically triggered by a default. When accompanied by a Guarantor Payment Demand Letter, the lender bypasses the primary borrower to seek full repayment from the individual or entity providing the security. It is critical to recognize that this document signifies the end of standard installment billing and the start of potential litigation. Receiving this requires urgent attention to evaluate cure rights, potential defenses, or restructuring options before the lender initiates formal collection or foreclosure proceedings.

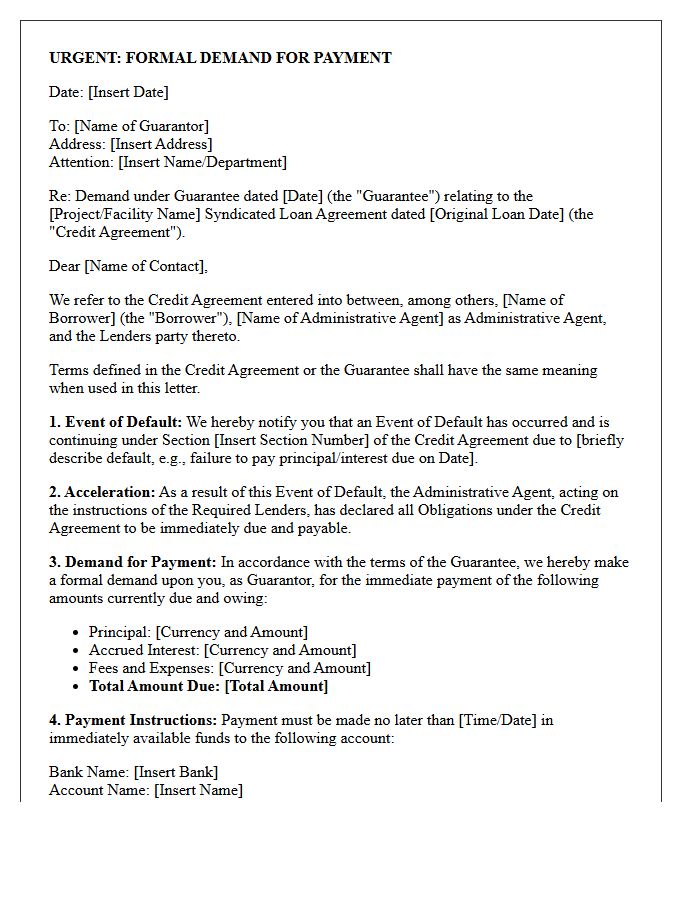

Syndicated Loan Default Guarantor Demand Letter

A Syndicated Loan Default Guarantor Demand Letter is a formal legal notice issued by an administrative agent on behalf of a group of lenders. When a borrower fails to meet its obligations, this document triggers the secondary liability of the guarantor. It serves as an official demand for immediate repayment of the outstanding debt. Precision in stating the default event and the specific amount due is critical to ensure enforceability under the guarantee agreement, often serving as the final prerequisite before pursuing litigation or asset seizure to recover capital.

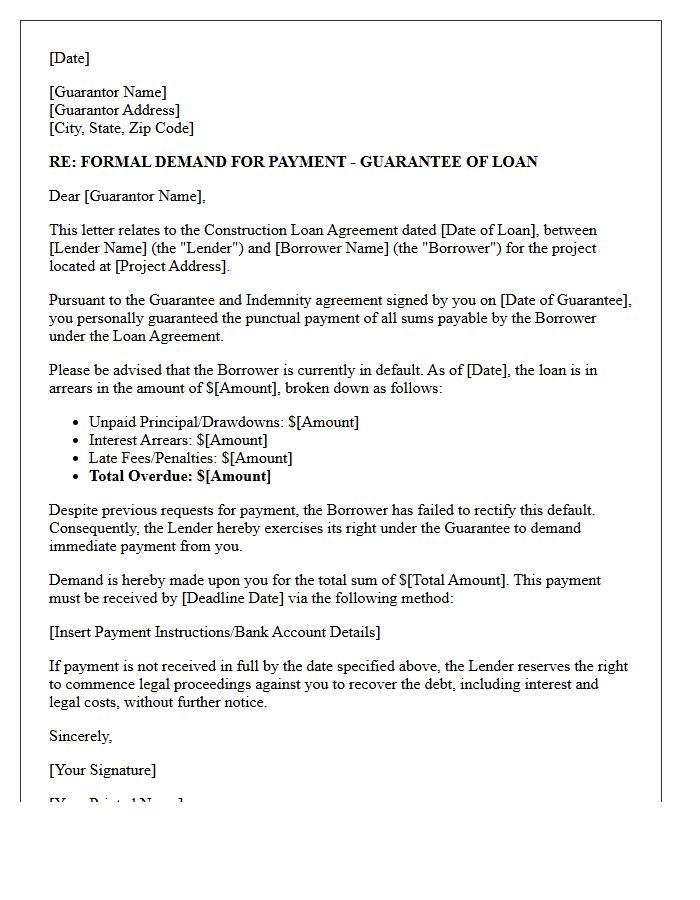

Construction Loan Arrears Guarantor Demand Letter

A construction loan arrears guarantor demand letter is a formal legal notice issued by a lender when a borrower defaults on repayments. This document serves as a final warning, officially notifying the guarantor of their contractual obligation to settle the outstanding debt. It highlights the personal liability involved, often preceding legal action or asset foreclosure. Timely response is critical to avoid additional penalty interest and litigation costs. Understanding the specific default terms within the original guarantee agreement is essential for managing financial risk and negotiating potential restructuring options with the financial institution.

What is a Demand for Payment From Guarantor?

A Demand for Payment From Guarantor is a formal legal notice sent to an individual or entity that has co-signed or guaranteed a loan, notifying them that the primary borrower has defaulted and they are now legally responsible for satisfying the debt.

When can a lender issue a demand for payment to a guarantor?

A lender can typically issue a demand for payment once the primary debtor fails to meet the terms of the credit agreement and a "Notice of Default" has been issued, provided the guarantee agreement includes a "payment on demand" clause.

What details should be included in a formal Guarantor Demand Letter?

A formal demand letter should include the original debtor's name, the total outstanding balance (including interest and fees), reference to the specific Guarantee Agreement, a deadline for payment, and instructions on how the funds should be remitted.

Can a guarantor refuse to pay a demand for payment?

A guarantor may only refuse payment if there are valid legal defenses, such as the original contract being materially altered without their consent, evidence that the debt has already been satisfied, or if the guarantee document was signed under duress or fraud.

What are the consequences if a guarantor ignores a demand for payment?

If a guarantor ignores a formal demand, the creditor may initiate legal action to obtain a judgment, which can lead to wage garnishment, property liens, a significant decrease in credit scores, and liability for the lender's legal collection costs.

Comments