A Notice of Intent to Foreclose is a formal legal warning issued by lenders when a homeowner defaults on mortgage payments. This critical document outlines the total arrears, provides a specific deadline for repayment, and details the steps required to avoid legal action. Understanding your rights during this grace period is essential to saving your home. Below are some ready to use templates.

Image cover: Official Notice of Intent to Foreclose: Templates and Essential Legal Samples

Letter Samples List

- First Mortgage Default Notification Letter

- Final Demand for Mortgage Payment Letter

- Notice of Intent to Foreclose Letter

- Breach of Mortgage Contract Letter

- Pre-Foreclosure Loan Acceleration Letter

- Notice of Default and Right to Cure Letter

- Residential Mortgage Delinquency Warning Letter

- Loss Mitigation Options Disclosure Letter

- Foreclosure Department Referral Letter

- Pending Legal Action Notification Letter

- Homeowner Foreclosure Prevention Letter

- Final Foreclosure Proceeding Warning Letter

- Mortgage Reinstatement Calculation Letter

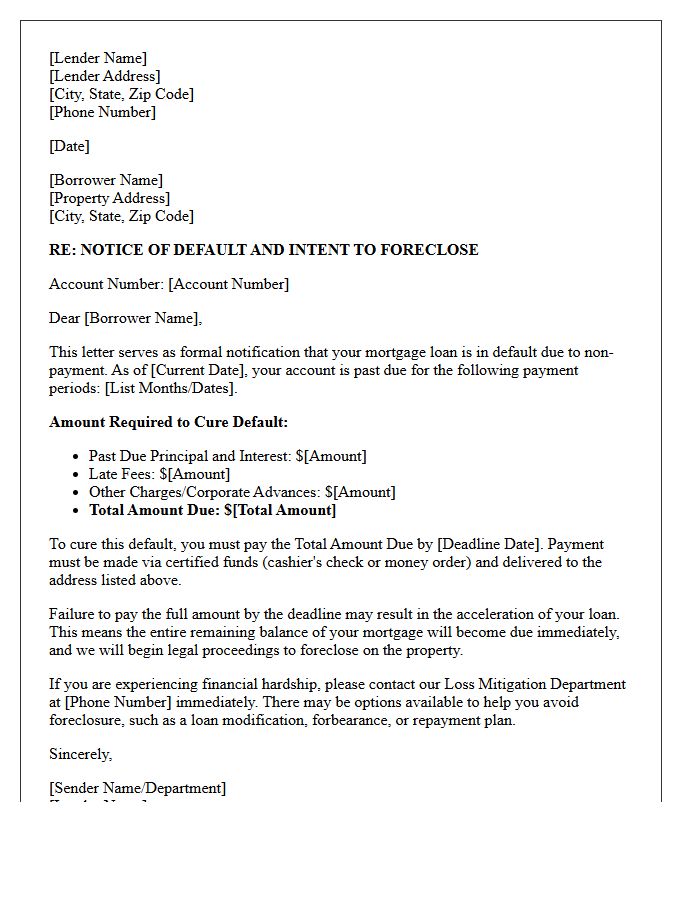

First Mortgage Default Notification Letter

A First Mortgage Default Notification Letter is a formal legal notice issued by a lender when a borrower misses payments. This critical document warns that the loan is in breach of contract and outlines the cure period available to resolve the debt. Receiving this letter signifies the initial step in the foreclosure process. It is essential to act immediately by contacting your servicer to explore loss mitigation options, such as loan modification or repayment plans, to prevent the loss of your property and protect your credit score.

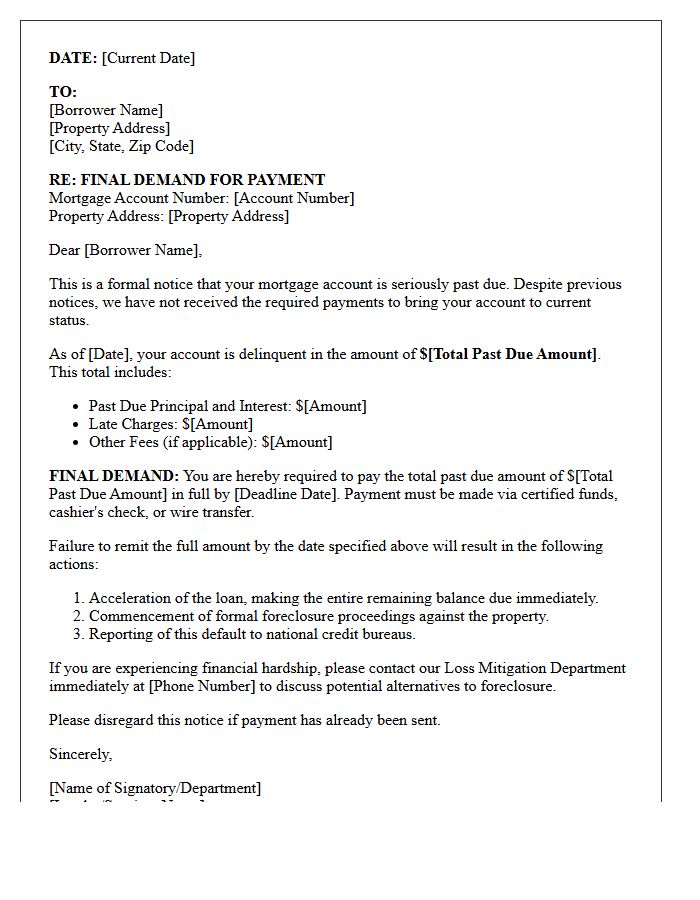

Final Demand for Mortgage Payment Letter

A Final Demand for Mortgage Payment Letter is a critical formal notice sent by lenders before initiating foreclosure proceedings. This document serves as a last warning that the borrower has breached the loan agreement. It specifies the total overdue balance, including late fees and interest, required to reinstate the mortgage. Ignoring this letter can lead to the loss of property rights. Borrowers should immediately contact their servicer to explore loss mitigation options or legal counsel to prevent the acceleration of the entire loan amount.

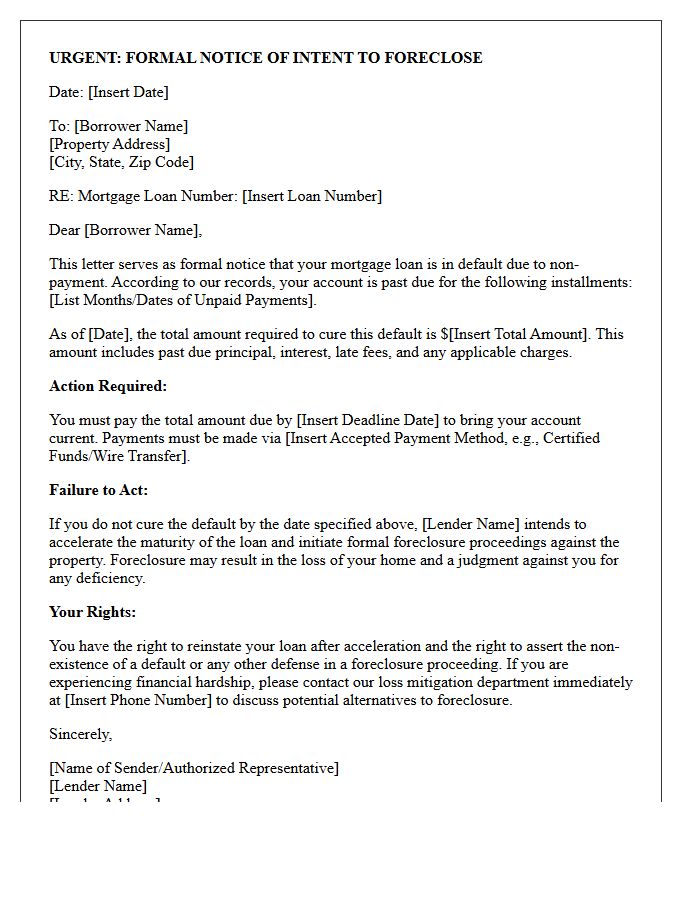

Notice of Intent to Foreclose Letter

A Notice of Intent to Foreclose is a formal legal warning sent by lenders to homeowners in default. This critical document signifies the final step before the foreclosure process officially begins. It outlines the specific amount needed to cure the default and provides a deadline to pay the arrears. Receiving this letter means your legal rights are at stake, making it essential to contact your servicer immediately to explore loss mitigation options. Timely action is the most effective way to prevent the permanent loss of your property and preserve your credit score.

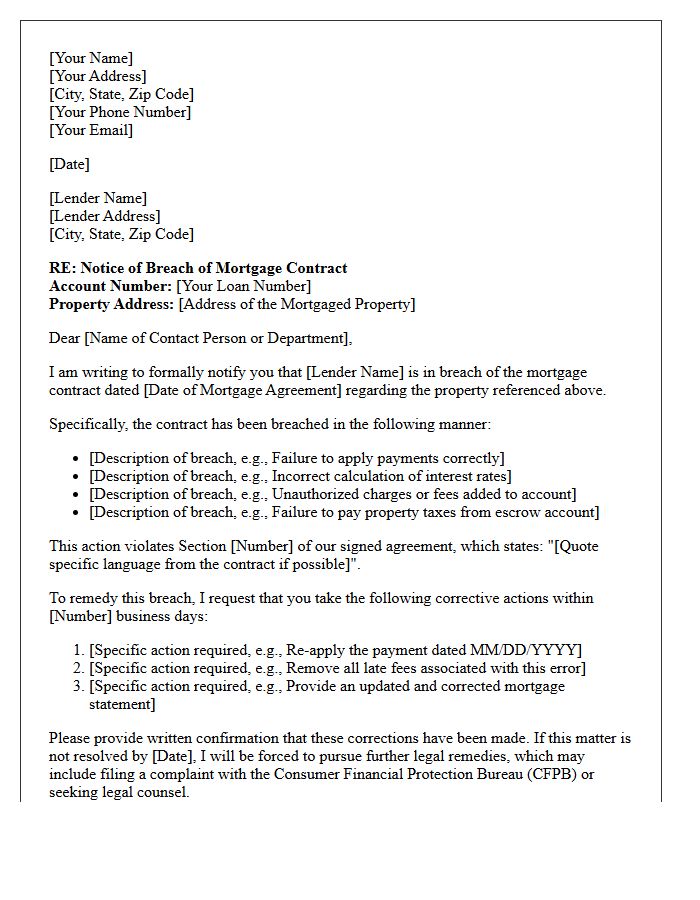

Breach of Mortgage Contract Letter

A Breach of Mortgage Contract Letter is a formal legal notice issued by a lender when a borrower fails to meet specific loan obligations. This document typically highlights delinquent payments or violations of insurance requirements. It serves as a mandatory step before the acceleration of the debt or the initiation of foreclosure proceedings. To resolve the default, the borrower must fulfill the cure demands within the specified timeframe. Understanding this letter is essential for protecting your property rights and negotiating potential loan modifications or repayment plans with your financial institution.

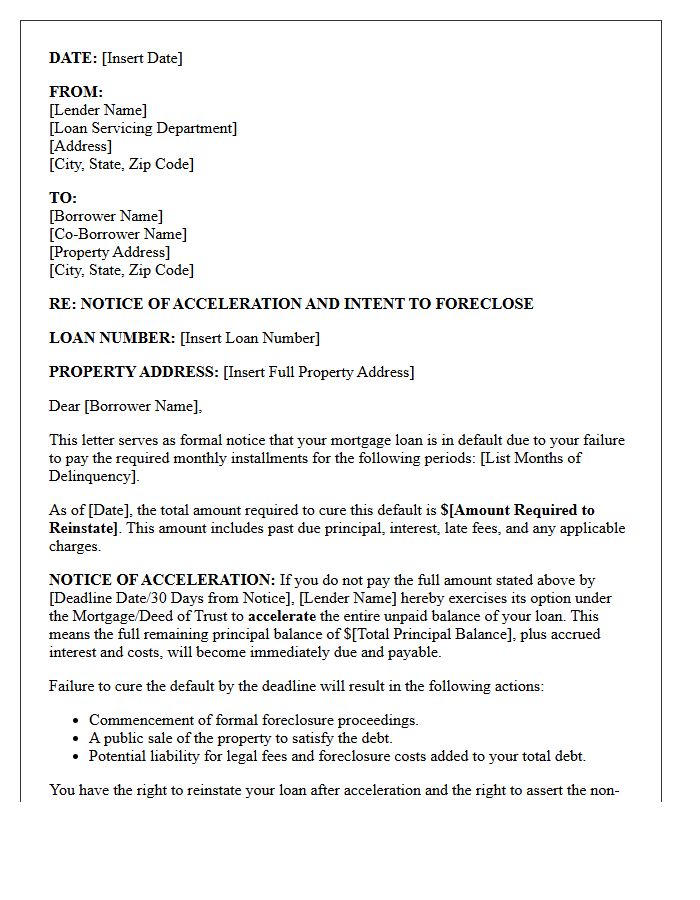

Pre-Foreclosure Loan Acceleration Letter

A pre-foreclosure loan acceleration letter is a formal notice from a lender demanding immediate payment of the entire outstanding mortgage balance. This legal step occurs after multiple missed payments, signaling that the borrower has defaulted. To prevent a foreclosure sale, the homeowner must pay the full amount specified or negotiate a loss mitigation plan. Ignoring this document typically leads to the commencement of judicial proceedings. Acting quickly during this phase is critical to explore reinstatement options or loan modifications to save your property from being repossessed.

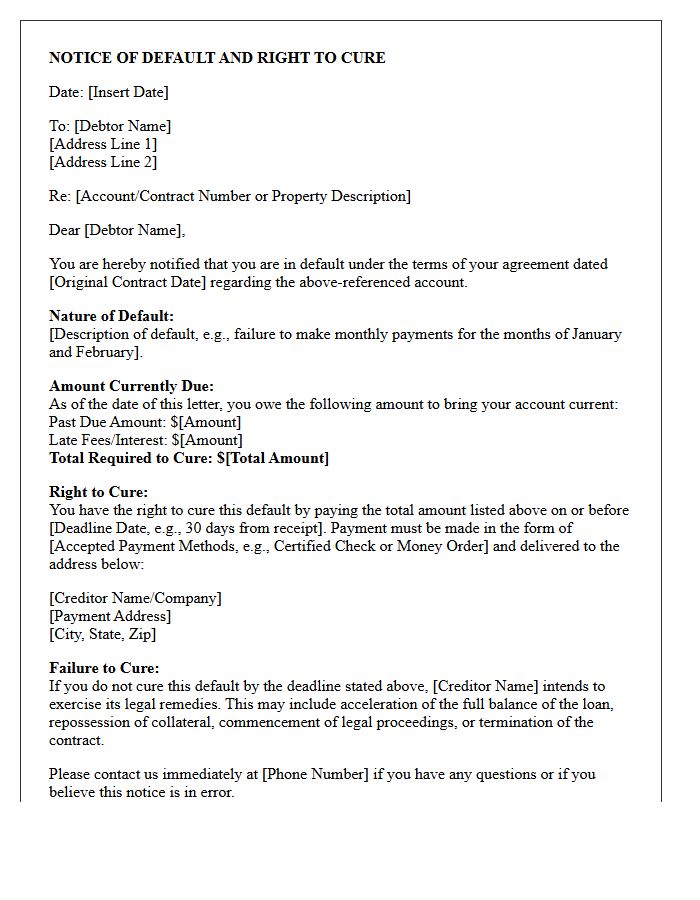

Notice of Default and Right to Cure Letter

A Notice of Default and Right to Cure Letter is a formal legal document issued by a lender when a borrower breaches a contract, typically through missed payments. This notice serves as a final warning before foreclosure or repossession proceedings begin. It specifies the exact amount owed, including late fees, and provides a strict deadline to rectify the delinquency. Understanding this letter is critical because it outlines your legal right to reinstate the loan by paying the arrears, effectively stopping legal action if action is taken within the designated timeframe.

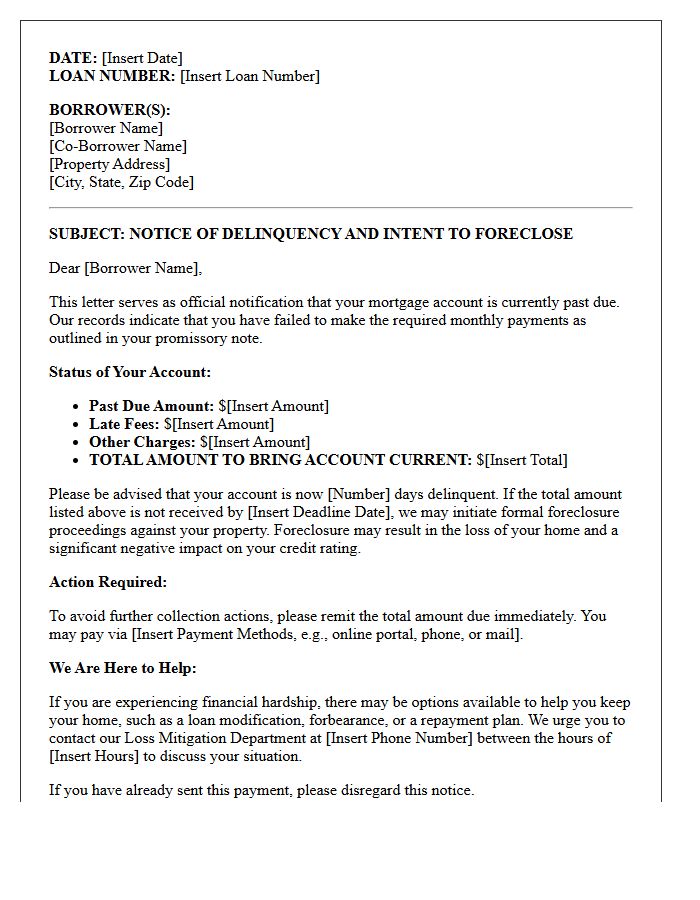

Residential Mortgage Delinquency Warning Letter

A Residential Mortgage Delinquency Warning Letter is a formal notification issued by lenders when a borrower misses a scheduled payment. This crucial document serves as a legal notice that the loan is in default, potentially leading to foreclosure if the balance is not rectified. It outlines the specific amount overdue, late fees, and a deadline for payment to avoid further penalties. Receiving this letter is a serious signal to contact your loan servicer immediately to discuss loss mitigation options or repayment plans to protect your home ownership status.

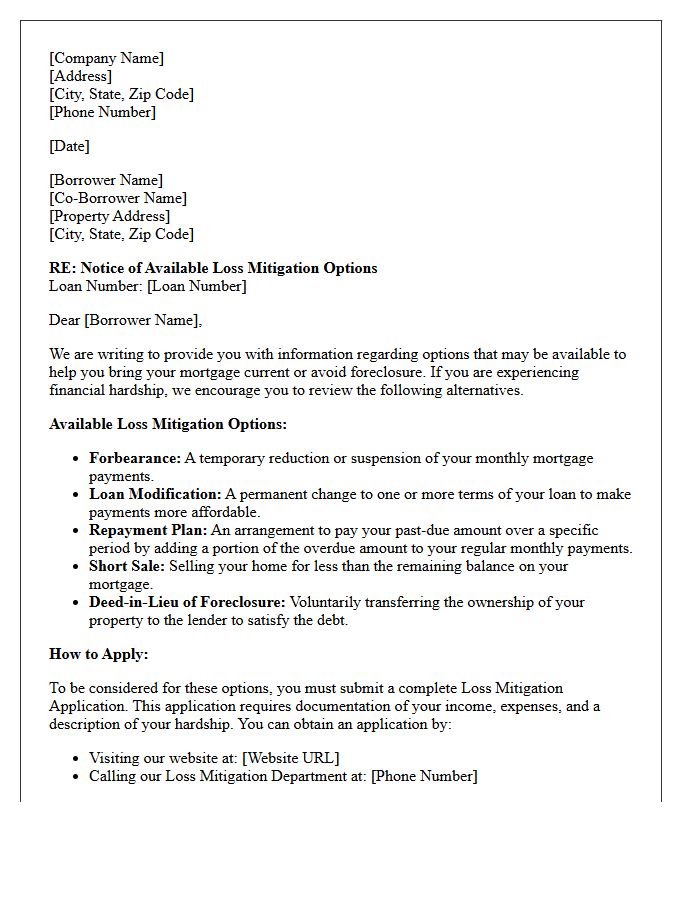

Loss Mitigation Options Disclosure Letter

A Loss Mitigation Options Disclosure Letter is a critical legal document sent by mortgage servicers to homeowners facing financial hardship. It outlines available alternatives to foreclosure, such as loan modifications, short sales, or deeds-in-lieu. This notice is a mandatory regulatory requirement under federal law, ensuring borrowers understand their rights to seek assistance. Reviewing this letter promptly is essential for protecting homeownership, as it provides specific deadlines and instructions for submitting a complete loss mitigation application to evaluate eligibility for relief programs.

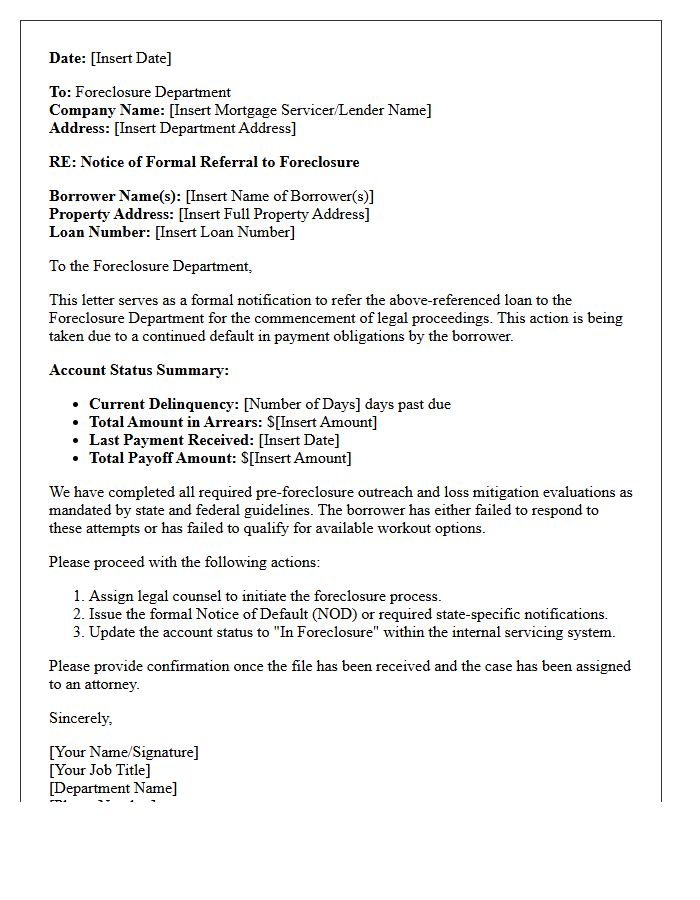

Foreclosure Department Referral Letter

A foreclosure department referral letter is a formal notice from a mortgage servicer informing a borrower that their delinquent account has been moved to the legal department or an attorney to begin the foreclosure process. This step typically occurs after 120 days of non-payment. It signifies the end of standard loss mitigation efforts and the start of official litigation. Receiving this letter is a critical warning to seek legal counsel or immediate loan modification to prevent the loss of the property through a public auction or sale.

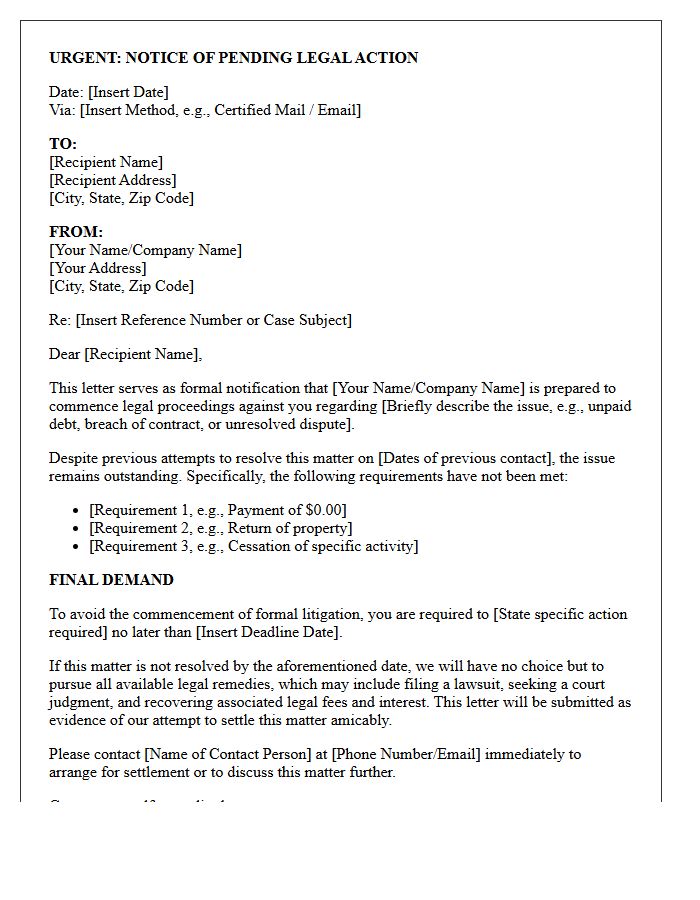

Pending Legal Action Notification Letter

A Pending Legal Action Notification Letter, often called a Ligation Hold, is a formal notice sent to individuals or organizations regarding potential lawsuits. This crucial document mandates the preservation of all relevant evidence, including physical records and electronic data. Ignoring this notice can lead to severe penalties, such as spoliation sanctions or unfavorable court rulings. It serves as an official warning to halt routine document destruction protocols immediately to ensure transparency during discovery. Timely response and compliance are essential to protecting your legal rights and maintaining integrity throughout the judicial process.

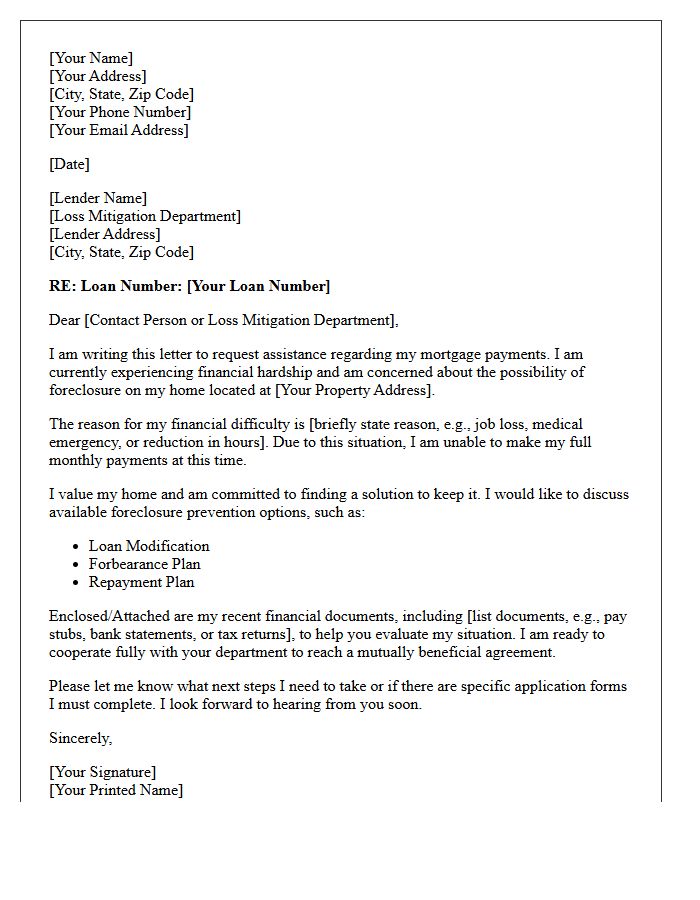

Homeowner Foreclosure Prevention Letter

A Homeowner Foreclosure Prevention Letter is a critical formal notice sent by mortgage lenders to borrowers in default. This document outlines specific repayment options, such as loan modifications or forbearance, to avoid legal action. Understanding the deadline stated in the letter is vital to preserving your property rights. Acting quickly allows you to engage in loss mitigation strategies that can stop the foreclosure process. Always verify the sender's authenticity to avoid scams while seeking immediate housing counseling to navigate your financial recovery effectively.

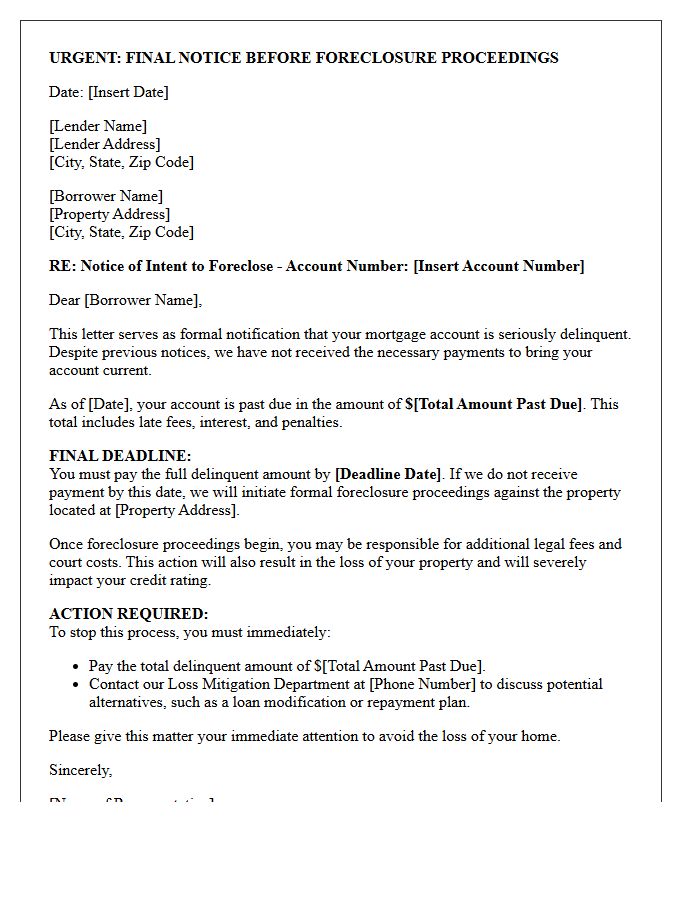

Final Foreclosure Proceeding Warning Letter

A Final Foreclosure Proceeding Warning Letter is a formal legal notice indicating that your lender is initiating litigation to seize your property. This document marks the end of the pre-foreclosure phase and serves as a final opportunity to resolve mortgage delinquency. It typically outlines the total amount owed, including legal fees, and sets a strict deadline for payment. Ignoring this warning leads directly to a court summons or an auction date. Homeowners must immediately seek legal counsel or loss mitigation options to prevent the permanent loss of their home equity.

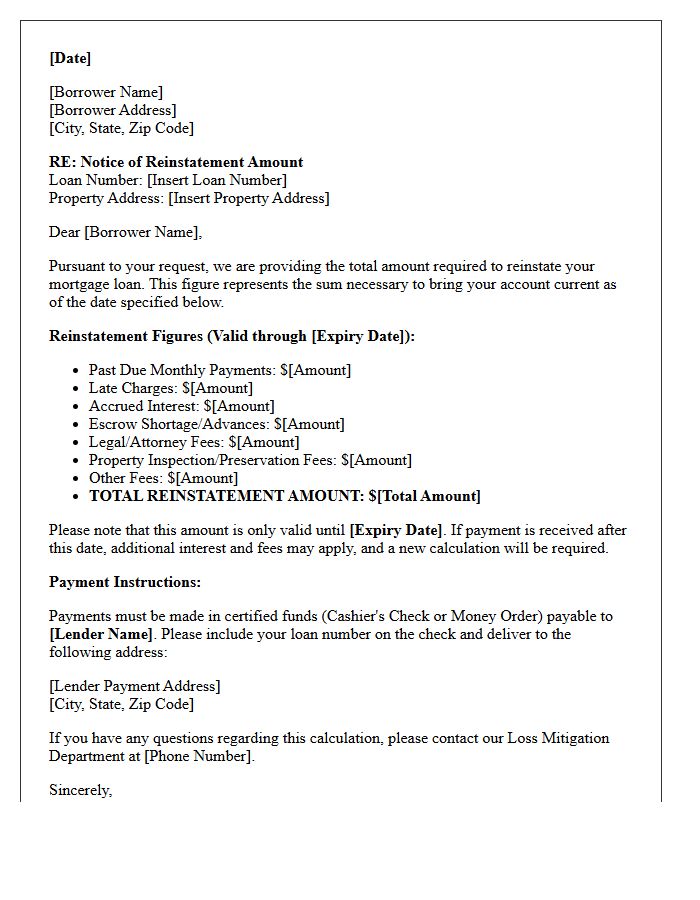

Mortgage Reinstatement Calculation Letter

A Mortgage Reinstatement Calculation Letter is a formal document from your lender detailing the exact total required to bring a delinquent loan current. It highlights the reinstatement amount, which includes all missed monthly payments, late fees, inspection costs, and legal charges accrued during default. This letter provides a specific deadline for payment to stop the foreclosure process. Understanding these figures is vital for homeowners seeking to restore their original loan terms and protect their property rights before a scheduled sale date.

What is a Notice of Intent to Foreclose on a residential mortgage?

A Notice of Intent to Foreclose (NOI) is a formal legal document sent by a mortgage lender to notify a homeowner that they are in default of their loan agreement and that the lender plans to initiate formal foreclosure proceedings if the delinquency is not resolved.

How many days do I have to respond after receiving a Notice of Intent to Foreclose?

The timeline varies by state law, but typically a Notice of Intent provides a 30-day "cure period." During this window, the homeowner has the legal right to pay the past-due balance, including late fees and interest, to reinstate the mortgage and stop the foreclosure process.

What information must be included in a valid Notice of Intent to Foreclose?

A legally compliant Notice of Intent must include the total amount required to cure the default, a clear deadline for payment, the contact information for the mortgage servicer, and a description of the homeowner's rights, including the availability of housing counseling services.

Does receiving a Notice of Intent to Foreclose mean I have to move out immediately?

No, receiving a Notice of Intent is the preliminary step before a foreclosure lawsuit or sale is filed. You still legal own the home and have the right to remain in the property while you explore loss mitigation options, such as a loan modification, short sale, or deed-in-lieu of foreclosure.

What should I do if I receive a Notice of Intent to Foreclose on my home?

Upon receiving the notice, you should immediately contact your mortgage servicer to discuss loss mitigation options. It is also highly recommended to consult with a HUD-approved housing counselor or a foreclosure defense attorney to understand your rights and prevent a formal filing in court.

Comments