Financial institutions must adhere to strict regulatory standards to prevent money laundering and terrorist financing. This overview explores the latest Bank Secrecy Act Compliance Advisory Letter, detailing essential risk management strategies and reporting obligations for compliance officers. Understanding these updates ensures your organization maintains institutional integrity and avoids significant legal penalties. Below are some ready to use template.

Image cover: Standardized Bank Secrecy Act Compliance Advisory Letter Templates and Professional Samples

Letter Samples List

- Bank Secrecy Act Initial Compliance Advisory Letter

- Customer Due Diligence Information Request Letter

- Enhanced Due Diligence Policy Update Advisory Letter

- Currency Transaction Reporting Exemption Status Letter

- Beneficial Ownership Information Certification Letter

- High-Risk Account Monitoring Notification Letter

- Unusual Transaction Activity Inquiry Letter

- Anti-Money Laundering Program Audit Findings Letter

- Unregistered Money Services Business Warning Letter

- Account Closure Due to Compliance Violation Letter

- Cash-Intensive Business Compliance Advisory Letter

- Wire Transfer Originator Information Requirement Letter

- Periodic Know Your Customer Profile Update Letter

- Correspondent Banking Due Diligence Advisory Letter

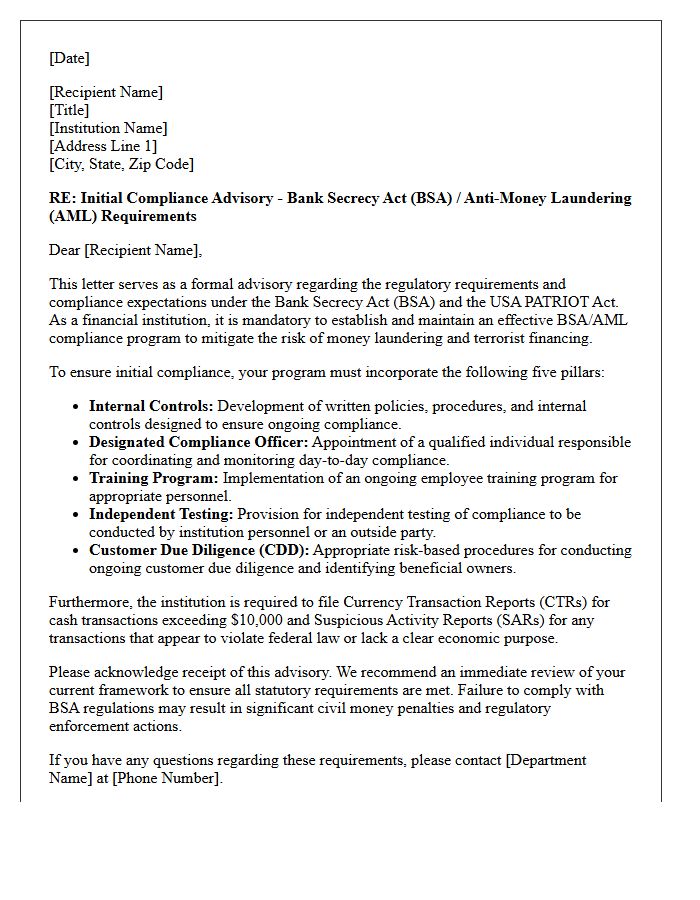

Bank Secrecy Act Initial Compliance Advisory Letter

The Bank Secrecy Act Initial Compliance Advisory Letter is a formal notification issued by regulators to newly chartered financial institutions. It serves as a compliance roadmap, outlining essential expectations for establishing a robust Anti-Money Laundering (AML) framework. The letter emphasizes the importance of customer due diligence, suspicious activity reporting, and internal controls to prevent financial crimes. Reviewing this document is critical for ensuring regulatory alignment and avoiding early enforcement actions, as it sets the standard for ongoing supervision and the institution's initial safety and soundness examinations.

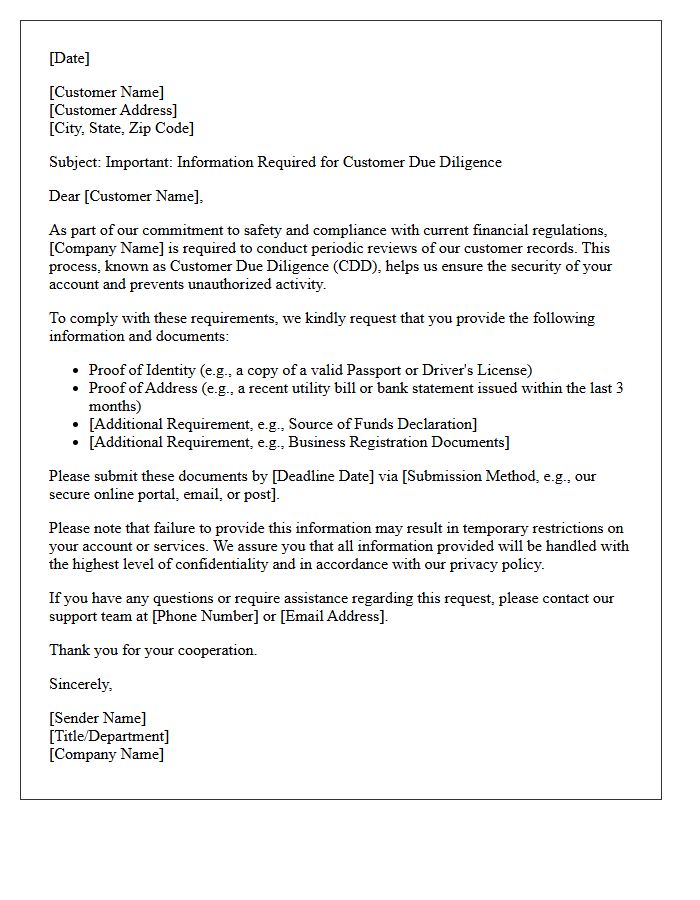

Customer Due Diligence Information Request Letter

A Customer Due Diligence (CDD) information request letter is a formal notice from a financial institution to verify your identity and assess potential risks. To comply with Anti-Money Laundering (AML) regulations, banks must collect updated documentation regarding your source of funds, business activities, and ultimate beneficial ownership. It is crucial to respond promptly to these requests; failing to provide the required evidence can lead to account restrictions or service termination. Ensuring accuracy in your submission maintains your compliance status and secures your ongoing banking relationship.

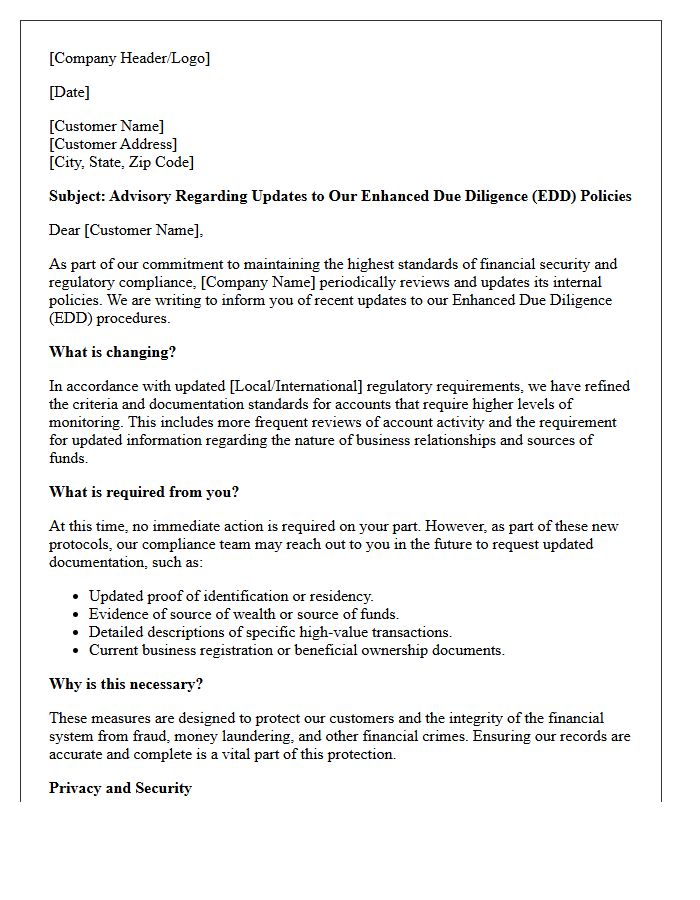

Enhanced Due Diligence Policy Update Advisory Letter

The Enhanced Due Diligence (EDD) Policy Update Advisory Letter informs clients about strengthened compliance measures. This regulatory notice outlines revised protocols for verifying high-risk accounts to mitigate financial crimes. It is essential to provide requested documentation promptly to ensure uninterrupted service. By updating KYC requirements and monitoring procedures, the institution aligns with global anti-money laundering (AML) standards. Please review the specific compliance obligations detailed in your letter to maintain account standing and transparency during this mandatory transition period.

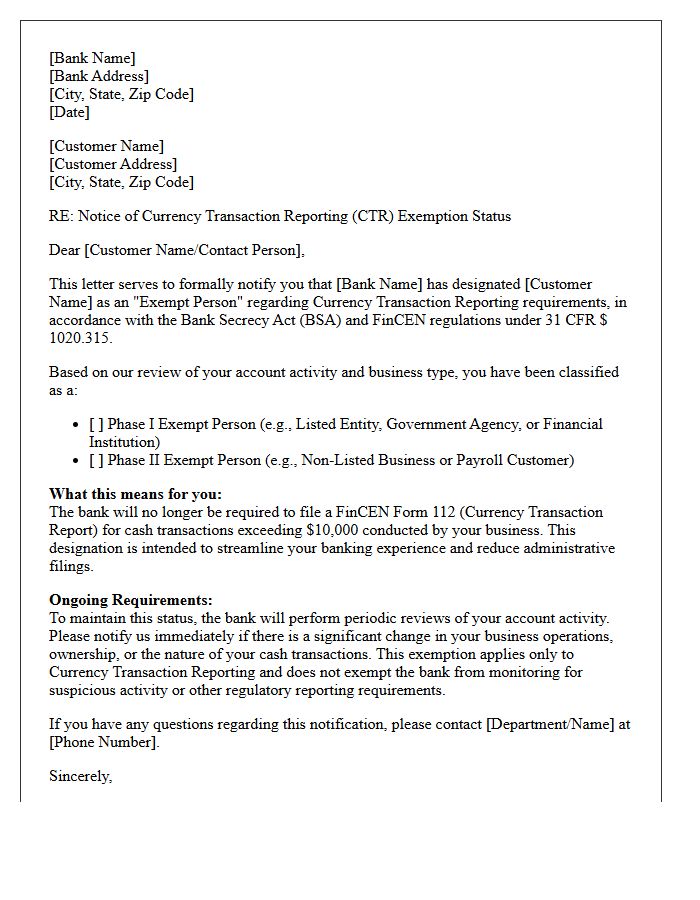

Currency Transaction Reporting Exemption Status Letter

A Currency Transaction Reporting Exemption Status Letter is a formal document used by financial institutions to notify the Financial Crimes Enforcement Network (FinCEN) when a customer is designated as an Exempt Person. This status allows banks to bypass filing individual CTRs for large cash transactions exceeding $10,000. It is primarily reserved for government agencies, publicly traded companies, or qualified Phase II entities like payroll customers. Maintaining an accurate exemption list ensures regulatory compliance with the Bank Secrecy Act while streamlining operational efficiency and reducing unnecessary paperwork for routine business activities.

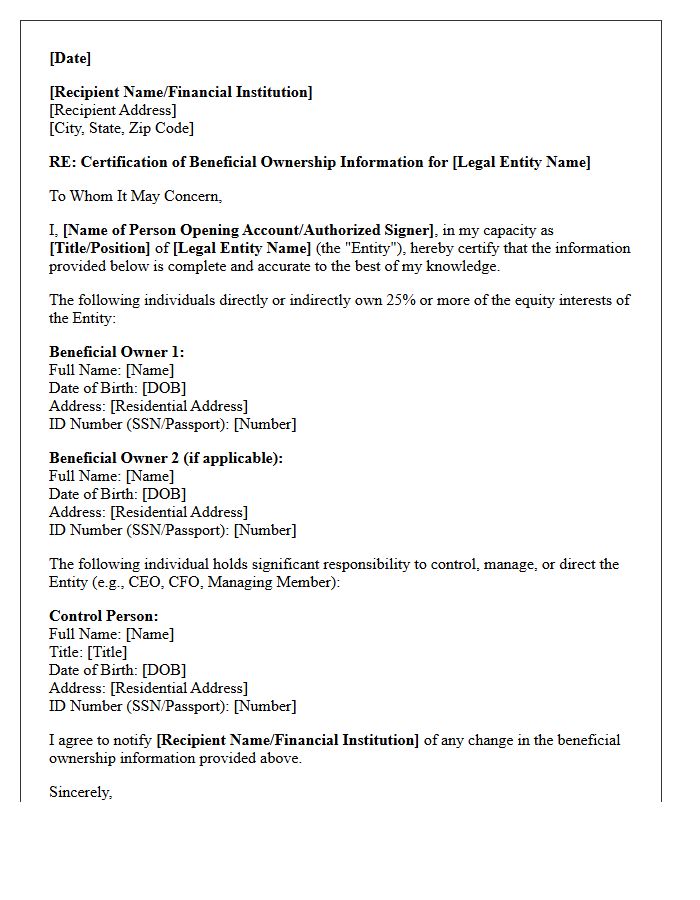

Beneficial Ownership Information Certification Letter

A Beneficial Ownership Information Certification Letter is a mandatory document used to verify the identities of individuals who own or control a company. Financial institutions require this form to comply with Anti-Money Laundering (AML) regulations and the Corporate Transparency Act. It ensures transparency by disclosing anyone with at least 25% ownership or significant management responsibility. Providing accurate information is essential to prevent financial crimes like tax evasion and fraud. Business entities must keep this certification updated to maintain legal compliance and ensure uninterrupted access to banking services and corporate accounts.

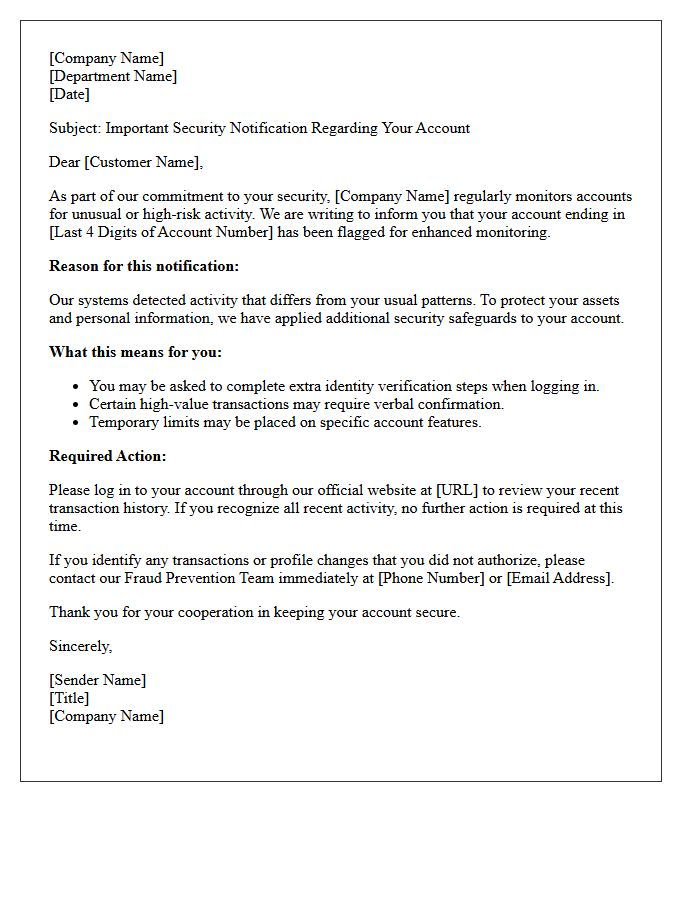

High-Risk Account Monitoring Notification Letter

A High-Risk Account Monitoring Notification Letter is an official alert issued by financial institutions when suspicious activity or significant profile changes are detected. This compliance measure aims to prevent fraud, money laundering, and unauthorized access. Receiving this letter often requires the account holder to verify their identity or provide additional documentation to ensure security. It is a critical protective step, not necessarily an accusation of wrongdoing. Promptly responding to these notifications is essential to maintain account functionality and safeguard your financial assets from potential exploitation or regulatory restrictions.

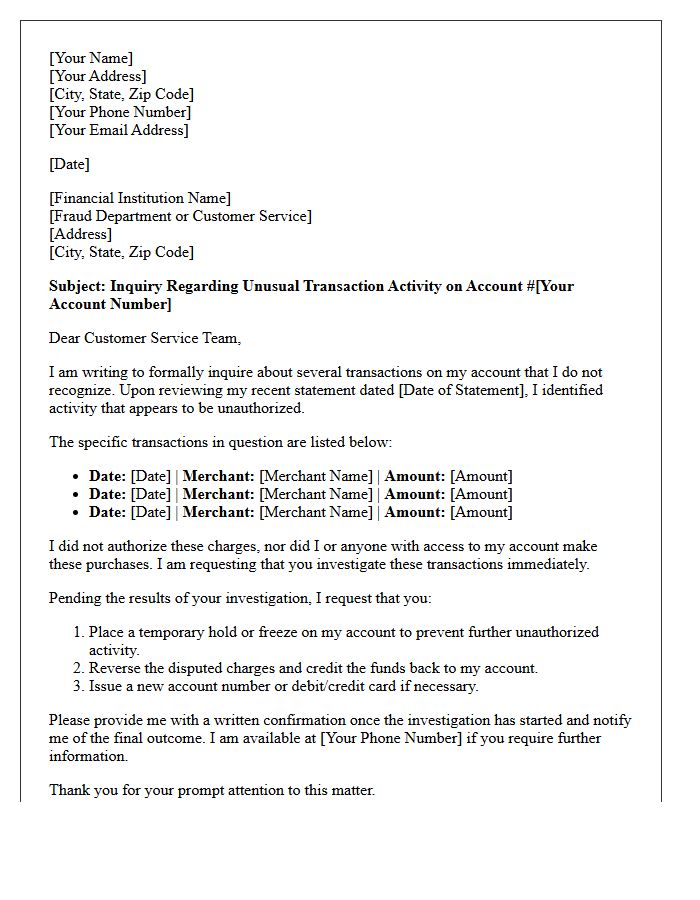

Unusual Transaction Activity Inquiry Letter

An Unusual Transaction Activity Inquiry Letter is a formal notification sent by a financial institution to verify suspicious account movements. It serves as a vital security measure to prevent identity theft and unauthorized access. When you receive this document, you must promptly confirm or dispute the listed charges to protect your funds. Providing accurate details during this verification process ensures your account security remains intact. Always use official contact channels provided in the letter to avoid phishing scams and maintain the integrity of your financial records.

Anti-Money Laundering Program Audit Findings Letter

An Anti-Money Laundering (AML) audit findings letter is a formal document issued by auditors or regulators detailing compliance deficiencies discovered during an examination. It highlights internal control weaknesses, policy gaps, or failures in suspicious activity monitoring that require immediate remediation. Receiving this letter necessitates a prompt, detailed management response to address regulatory risks and prevent potential penalties. Understanding these findings is essential for strengthening your financial crime prevention framework and ensuring your institution maintains legal standing with governing authorities like FinCEN or local financial regulators.

Unregistered Money Services Business Warning Letter

Receiving an Unregistered Money Services Business Warning Letter indicates that federal regulators, such as FinCEN, suspect your activities require formal registration as a Money Services Business (MSB). This official notice serves as a formal alert that non-compliance with anti-money laundering regulations carries severe risks. To avoid civil penalties or potential criminal prosecution, you must immediately evaluate your operations against legal definitions. Addressing these regulatory requirements promptly is essential to ensure your business operates legally and avoids shutdown or significant fines within the financial sector.

Account Closure Due to Compliance Violation Letter

Receiving an Account Closure Due to Compliance Violation letter means the financial institution has terminated your relationship due to internal policy breaches or regulatory concerns. Common triggers include suspicious activity, Anti-Money Laundering (AML) failures, or providing inaccurate documentation. This action is usually final and non-negotiable. It is crucial to review the notice for instructions on recovering remaining balances and to update your records immediately. Failure to address these underlying compliance risks can lead to being blacklisted by other banks or facing increased scrutiny during future financial applications.

Cash-Intensive Business Compliance Advisory Letter

The Cash-Intensive Business Compliance Advisory Letter is a formal notice from tax authorities highlighting reporting obligations for companies handling high volumes of physical currency. It serves as an educational tool to ensure accurate income disclosure and adherence to anti-money laundering regulations. Receiving this letter indicates that your industry is under increased scrutiny for potential underreporting. To maintain compliance, businesses must implement robust internal controls and maintain precise financial records. Timely professional advice is recommended to mitigate audit risks and address any identified discrepancies in cash management practices.

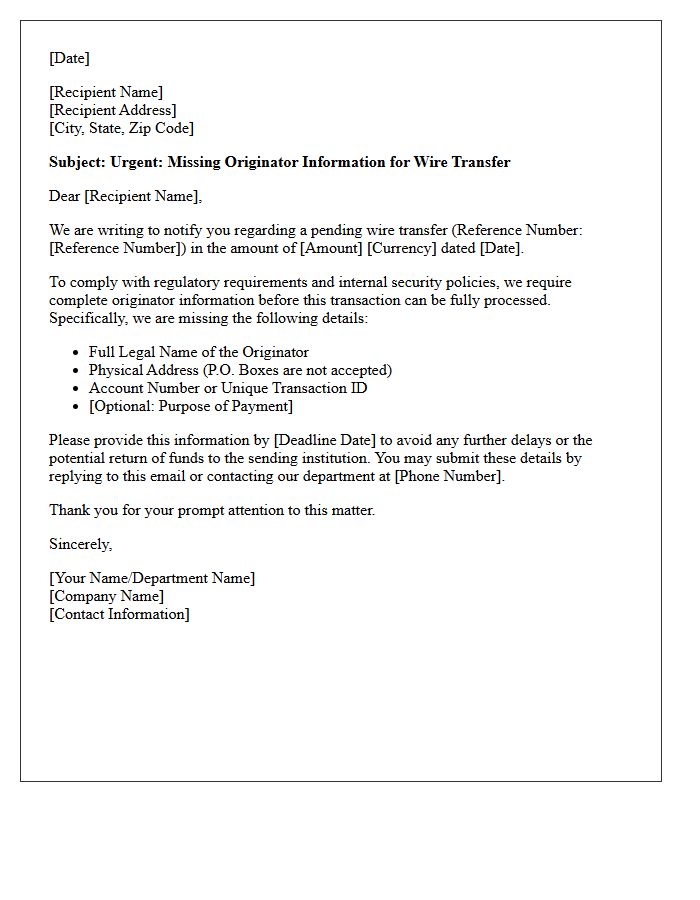

Wire Transfer Originator Information Requirement Letter

A Wire Transfer Originator Information Requirement Letter is a formal request from a financial institution to verify the identity and source of funds for a payment. To comply with AML (Anti-Money Laundering) and KYC regulations, banks must ensure that sender details are complete and accurate. Failure to provide the requested information promptly can lead to transaction delays or the rejection of the transfer. This process is essential for maintaining global financial security and preventing fraudulent activities within the international banking network.

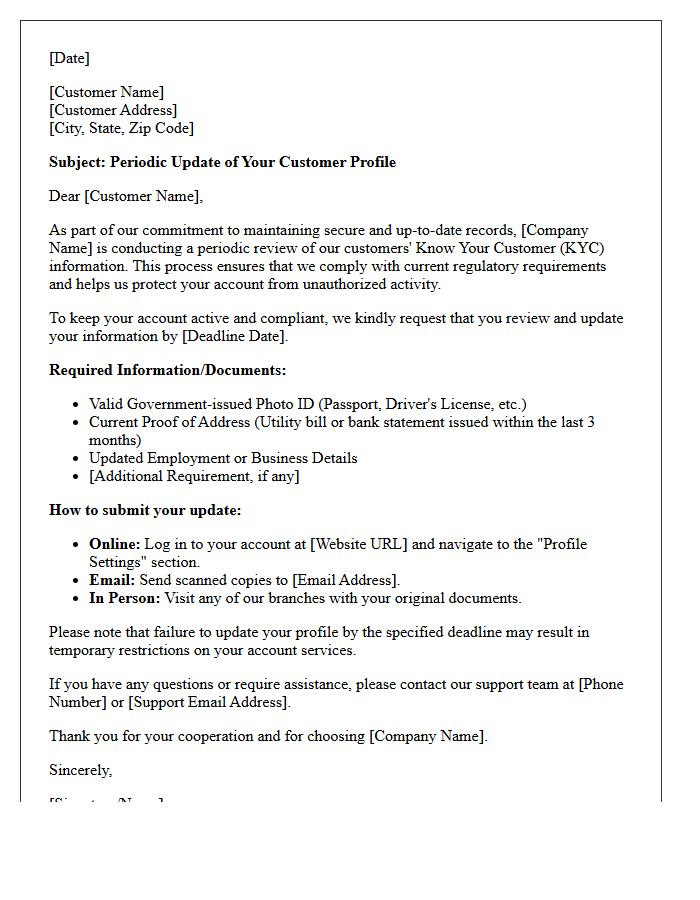

Periodic Know Your Customer Profile Update Letter

A Periodic Know Your Customer (KYC) Profile Update Letter is a mandatory request from financial institutions to ensure your account information remains accurate and current. Banks must comply with anti-money laundering (AML) regulations by verifying your identity, source of funds, and employment status. Failure to respond to this compliance mandate may result in temporary account restrictions or closure. It is essential to provide the requested documentation promptly to maintain financial security and ensure uninterrupted access to your banking services and global transactions.

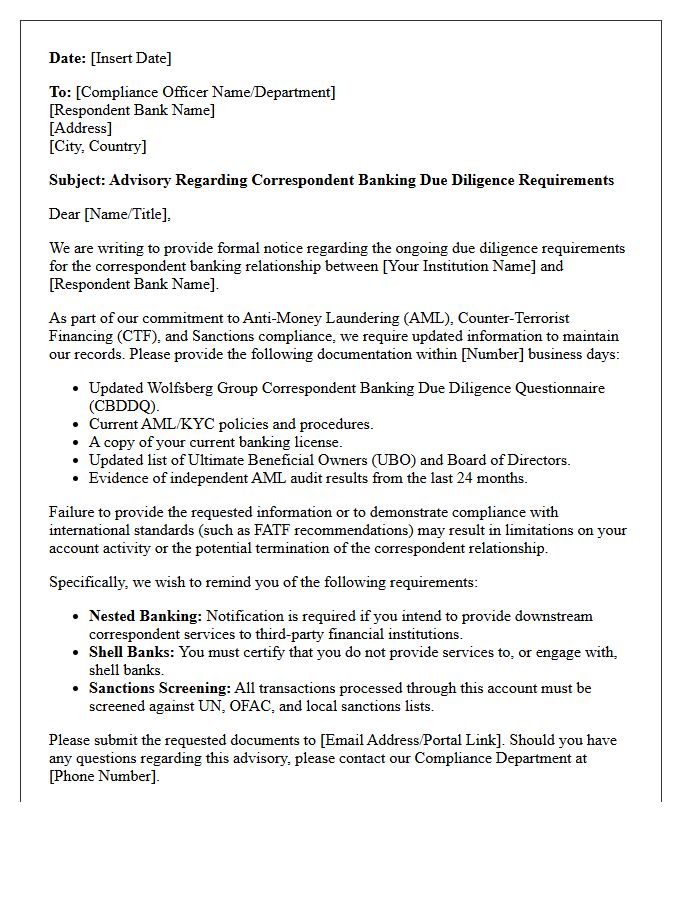

Correspondent Banking Due Diligence Advisory Letter

The Correspondent Banking Due Diligence Advisory Letter provides critical guidance for financial institutions to mitigate risks associated with cross-border payments. It outlines the necessity of risk-based assessments when establishing or maintaining relationships with foreign respondent banks. Compliance officers must evaluate the respondent's anti-money laundering (AML) controls and beneficial ownership structures to prevent financial crime. Adhering to these regulatory expectations ensures transparency and protects the global financial system from illicit activities, making rigorous due diligence an essential component of modern banking operational security and legal compliance.

What is the purpose of a Bank Secrecy Act (BSA) Compliance Advisory Letter?

A BSA Compliance Advisory Letter is issued by regulatory bodies to provide financial institutions with guidance on emerging risks, updates to anti-money laundering (AML) regulations, and expectations for maintaining an effective compliance program.

What are the core components of a BSA Compliance Program mentioned in advisory letters?

An effective program must include five pillars: a system of internal controls, independent testing, the designation of a qualified compliance officer, ongoing training for personnel, and appropriate risk-based customer due diligence (CDD) procedures.

How should financial institutions respond to a BSA Compliance Advisory regarding high-risk transactions?

Institutions should update their risk assessment frameworks, enhance monitoring for suspicious activity, and ensure that Suspicious Activity Reports (SARs) are filed accurately and timely in accordance with the specific typologies identified in the letter.

What are the consequences of non-compliance with BSA Advisory guidelines?

Failure to adhere to BSA requirements can result in formal enforcement actions, significant monetary penalties, heightened regulatory oversight, and reputational damage to the financial institution.

How often are BSA Compliance Advisory Letters issued?

Advisory letters are issued on an ad hoc basis by agencies like FinCEN or the OCC whenever there are significant shifts in financial crime trends, legislative changes (such as the Anti-Money Laundering Act of 2020), or identified systemic weaknesses in industry compliance.

Comments