Managing financial risk requires adherence to the latest Commercial Real Estate Lending Guidance. Regulatory bodies issue these letters to ensure institutions maintain robust underwriting standards, stress testing, and risk management practices amidst market volatility. This article explores key compliance strategies for lenders to navigate evolving property valuations and interest rate shifts. Below are some ready to use templates.

Image cover: Professional Templates and Best Practices for Commercial Real Estate Lending Correspondence

Letter Samples List

- Commercial Real Estate Lending Policy Guidance Letter

- Commercial Real Estate Loan Commitment Letter

- Commercial Real Estate Underwriting Standards Guidance Letter

- Commercial Real Estate Appraisal Review Guidance Letter

- Commercial Real Estate Portfolio Risk Management Letter

- Commercial Real Estate Loan Approval Notification Letter

- Commercial Real Estate Regulatory Compliance Guidance Letter

- Commercial Real Estate Environmental Risk Assessment Letter

- Commercial Real Estate Loan Restructuring Guidance Letter

- Commercial Real Estate Concentration Risk Management Letter

- Commercial Real Estate Stress Testing Policy Letter

- Commercial Real Estate Construction Disbursement Guidance Letter

- Commercial Real Estate Loan Workout Strategy Letter

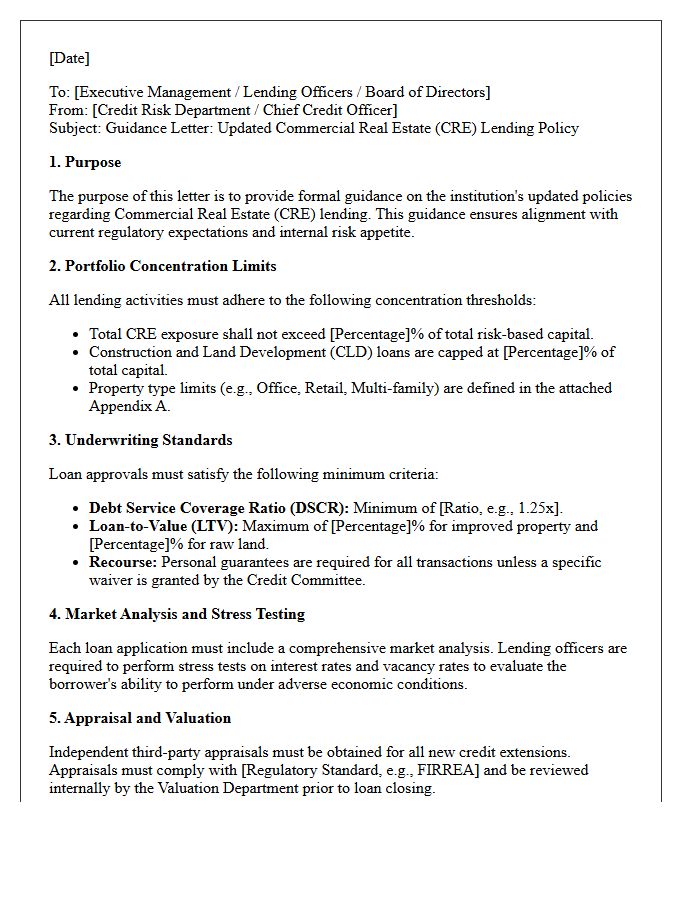

Commercial Real Estate Lending Policy Guidance Letter

The Commercial Real Estate (CRE) Lending Policy Guidance Letter outlines critical supervisory expectations for financial institutions managing high concentration risks. It emphasizes robust risk management frameworks, including stress testing and sensitivity analysis, to mitigate potential losses during market downturns. Lenders must maintain adequate capital reserves and implement rigorous underwriting standards to ensure portfolio resilience. This guidance serves as a vital regulatory benchmark for assessing the safety and soundness of institutions heavily invested in volatile commercial property markets, prioritizing proactive monitoring and strategic risk diversification to maintain financial stability.

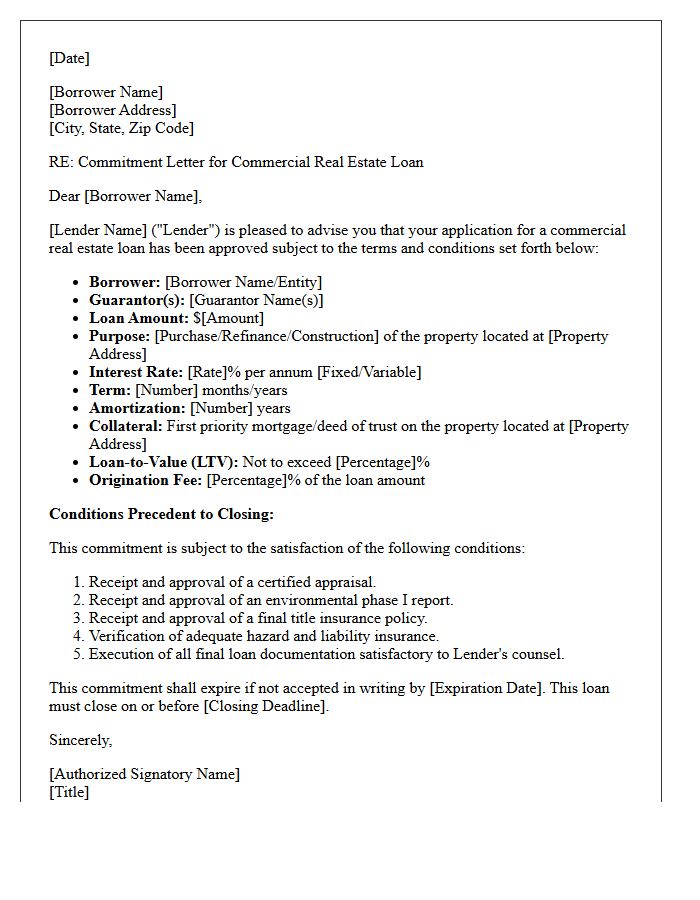

Commercial Real Estate Loan Commitment Letter

A Commercial Real Estate Loan Commitment Letter is a legally binding agreement from a lender outlining the specific terms of a property loan. This document signifies formal approval, detailing the interest rate, repayment schedule, and loan-to-value ratios. It is crucial to review all closing conditions and contingencies, such as appraisals or environmental reports, before signing. Receiving this letter is a pivotal milestone in securing financing, as it transitions the application from underwriting to the final funding stage, ensuring both parties are committed to the transaction's financial obligations.

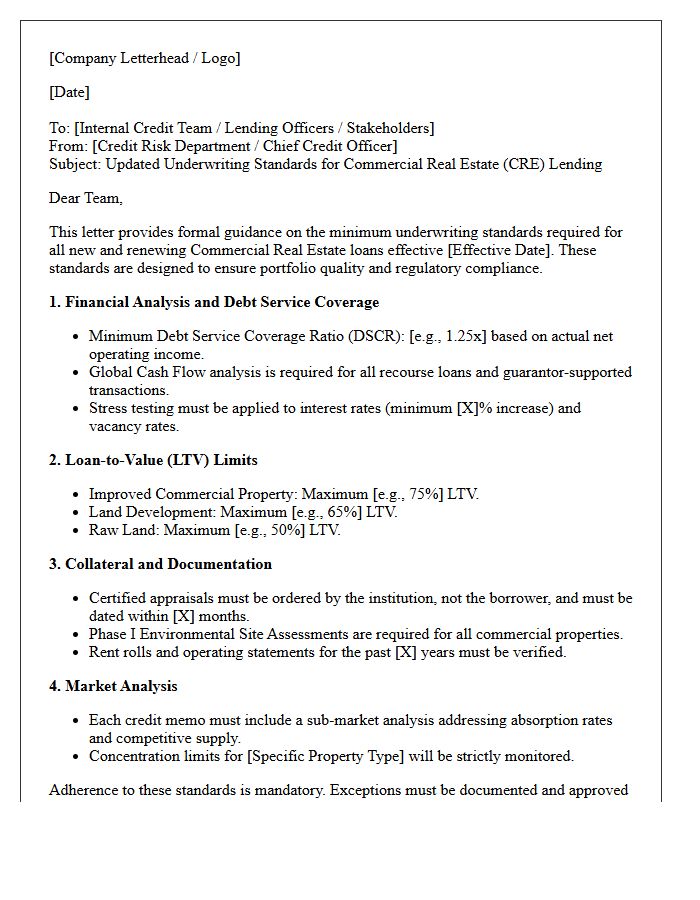

Commercial Real Estate Underwriting Standards Guidance Letter

The Commercial Real Estate Underwriting Standards Guidance Letter outlines critical expectations for financial institutions to maintain prudent lending practices. It emphasizes rigorous credit analysis, realistic appraisals, and sustainable debt service coverage ratios. This regulatory guidance ensures banks manage risks associated with volatile property markets by enforcing loan-to-value limits and stressed sensitivity testing. Adhering to these standards promotes overall financial stability by preventing excessive leverage and ensuring that commercial portfolios remain resilient against economic shifts and interest rate fluctuations.

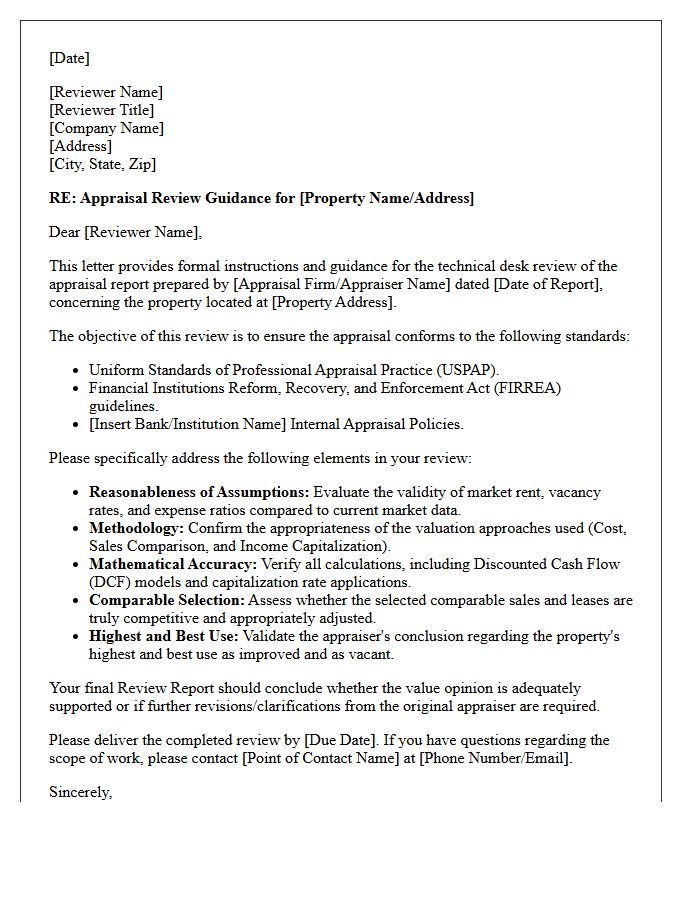

Commercial Real Estate Appraisal Review Guidance Letter

A Commercial Real Estate Appraisal Review Guidance Letter establishes regulatory standards for financial institutions evaluating property valuations. It ensures that internal reviews are independent, objective, and compliant with the Uniform Standards of Professional Appraisal Practice. The letter highlights the importance of verifying market data, methodology, and risk assumptions to prevent inflated asset values. Lenders must follow these protocols to maintain transparency and safety in credit decisions, protecting the institution from potential losses caused by inaccurate or biased appraisal reports during the commercial underwriting process.

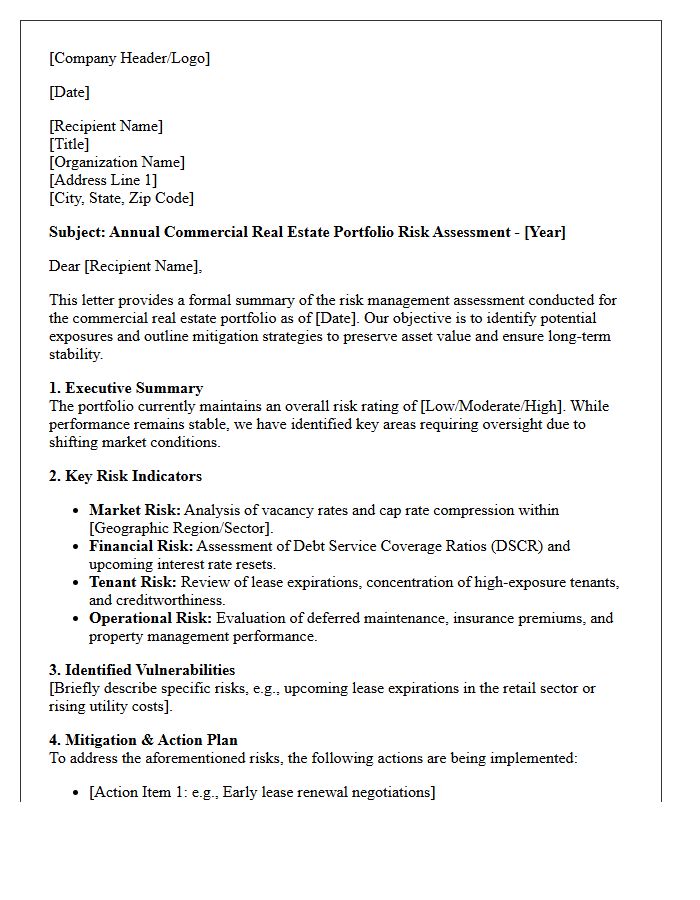

Commercial Real Estate Portfolio Risk Management Letter

A Commercial Real Estate Portfolio Risk Management Letter is a formal document used to communicate exposure levels, mitigation strategies, and financial health to stakeholders. It identifies key vulnerabilities such as market volatility, interest rate fluctuations, and tenant vacancies. This letter ensures transparency by outlining proactive measures taken to safeguard asset value and maintain liquidity. Clear reporting on debt-service coverage ratios and property performance is essential for maintaining investor confidence. Effective risk communication minimizes potential losses and stabilizes long-term growth within a diversified property portfolio.

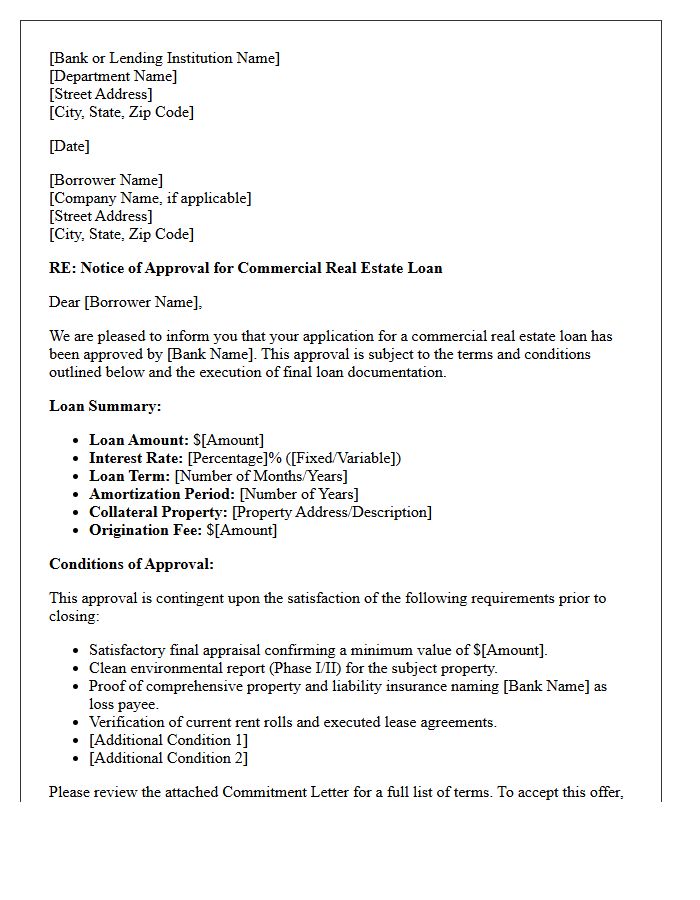

Commercial Real Estate Loan Approval Notification Letter

A Commercial Real Estate Loan Approval Notification Letter is a formal document confirming a lender's commitment to fund a property acquisition or refinance. It outlines critical loan terms such as the interest rate, amortization schedule, and loan-to-value ratio. Borrowers must carefully review the closing conditions and contingencies, which often include third-party appraisals, environmental reports, and financial covenants. This letter serves as a legal bridge between the initial application and the final funding phase, signaling that the borrower has successfully met the institution's underwriting standards and risk requirements.

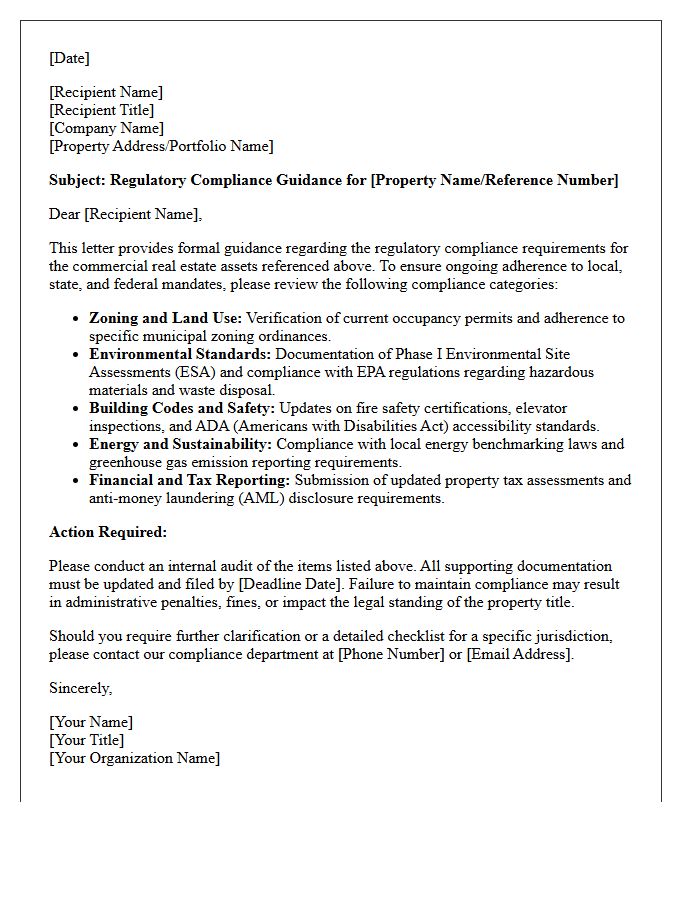

Commercial Real Estate Regulatory Compliance Guidance Letter

The Commercial Real Estate Regulatory Compliance Guidance Letter provides essential directives for financial institutions to manage credit risk effectively. It emphasizes the importance of maintaining robust risk management frameworks, particularly during market fluctuations. Banks must ensure accurate property valuations and prudent lending limits to safeguard capital stability. This guidance serves as a regulatory roadmap for identifying vulnerability within loan portfolios. By adhering to these standards, lenders can mitigate potential losses and ensure long-term financial compliance with federal oversight expectations in the evolving commercial property sector.

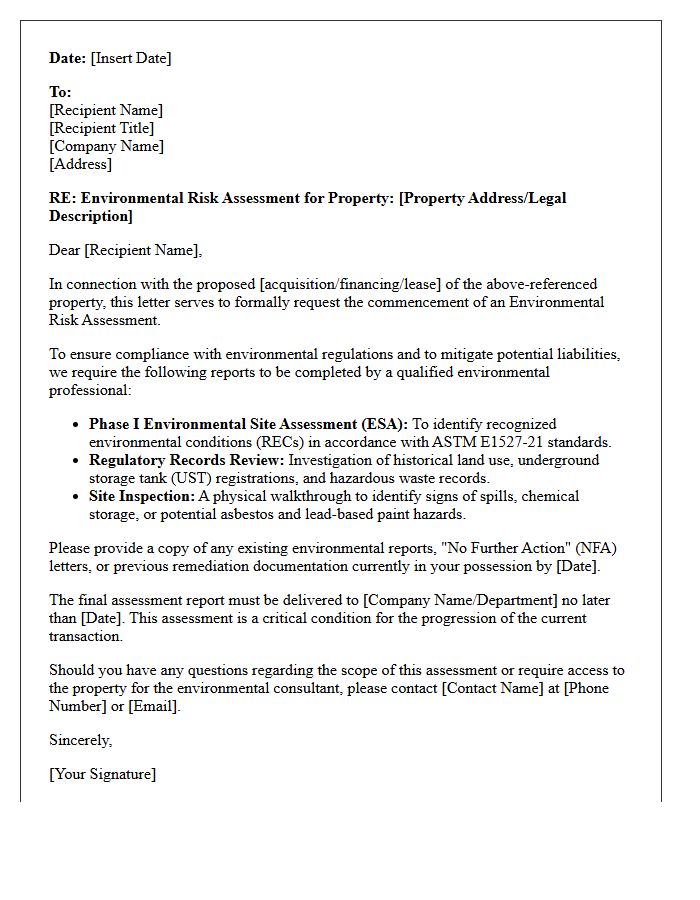

Commercial Real Estate Environmental Risk Assessment Letter

A Commercial Real Estate Environmental Risk Assessment Letter is a crucial Phase I Environmental Site Assessment (ESA) summary used by lenders to identify potential liabilities. This document evaluates risks such as soil contamination, groundwater pollution, or hazardous waste from past land use. Obtaining this letter is essential for due diligence to protect investors from future legal costs and environmental cleanup responsibilities. It ensures the property meets regulatory standards before a transaction or loan approval. Understanding these environmental risks helps mitigate financial exposure and ensures a safe, compliant real estate investment.

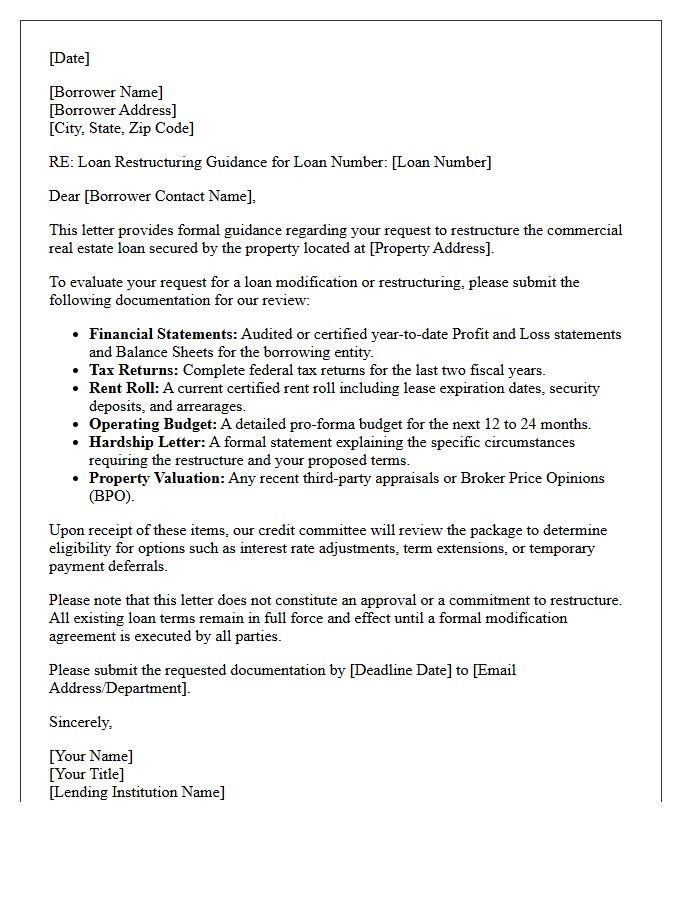

Commercial Real Estate Loan Restructuring Guidance Letter

The 2023 Commercial Real Estate Loan Restructuring guidance provides financial institutions with updated frameworks for managing stressed assets. It encourages lenders to work proactively with creditworthy borrowers through prudent workouts, such as term extensions or interest rate adjustments, rather than forcing immediate foreclosures. Key to this policy is the classification of Troubled Debt Restructurings (TDRs), ensuring that modified loans are evaluated based on their revised payment capacity. This regulatory shift aims to maintain financial stability while offering flexibility amidst rising interest rates and shifting market demand for office and retail spaces.

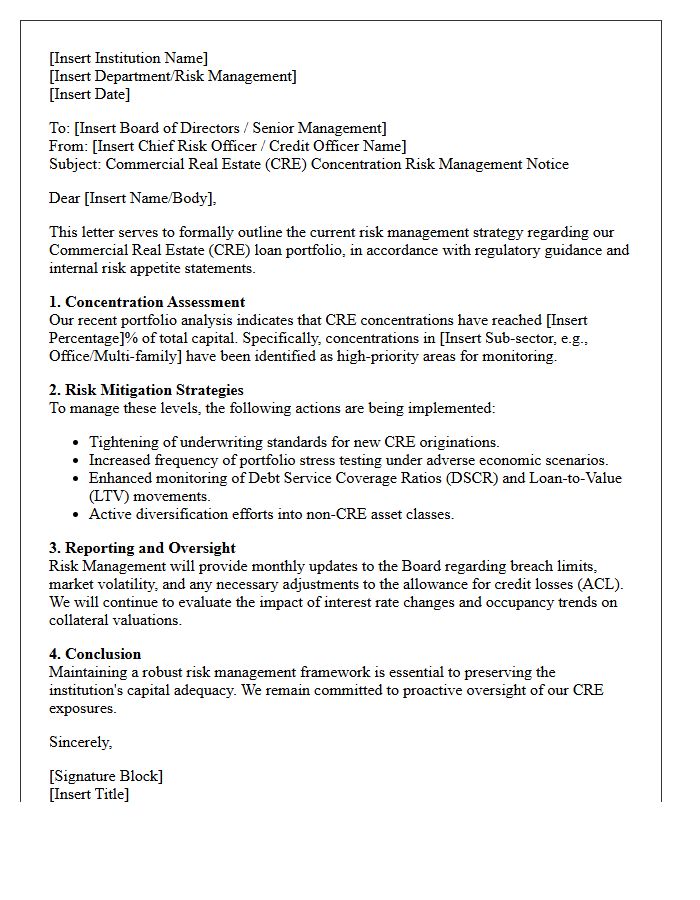

Commercial Real Estate Concentration Risk Management Letter

A Commercial Real Estate Concentration Risk Management Letter is a formal communication from regulators, such as the FDIC, addressing concerns over high exposure to CRE loans. It outlines expectations for heightened risk management practices, including robust stress testing, portfolio diversification, and increased capital levels. Banks must demonstrate effective board oversight and sophisticated internal controls to mitigate potential losses from market volatility. Adhering to these guidelines ensures institutional stability and regulatory compliance when credit concentrations exceed specific thresholds relative to total capital.

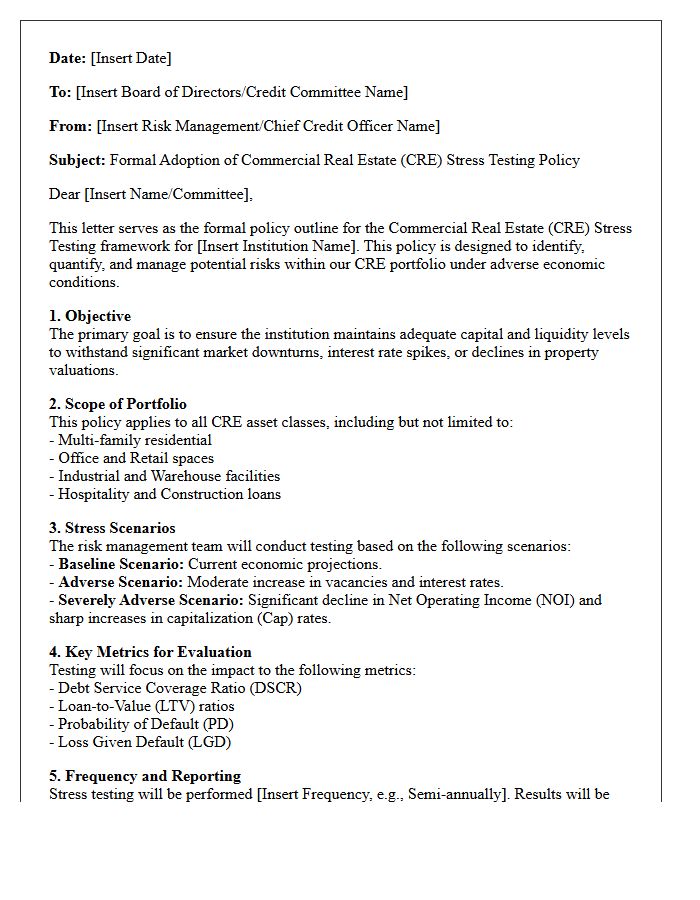

Commercial Real Estate Stress Testing Policy Letter

The Commercial Real Estate Stress Testing Policy Letter serves as a critical regulatory framework for financial institutions. It mandates rigorous portfolio analysis to evaluate resilience against adverse economic shifts, such as rising interest rates or declining occupancy. Banks must employ forward-looking scenarios to identify potential vulnerabilities in their lending practices. This policy ensures capital adequacy and promotes proactive risk management to maintain financial stability. Adherence to these guidelines is essential for mitigating losses during market volatility and ensuring the long-term health of commercial property investments.

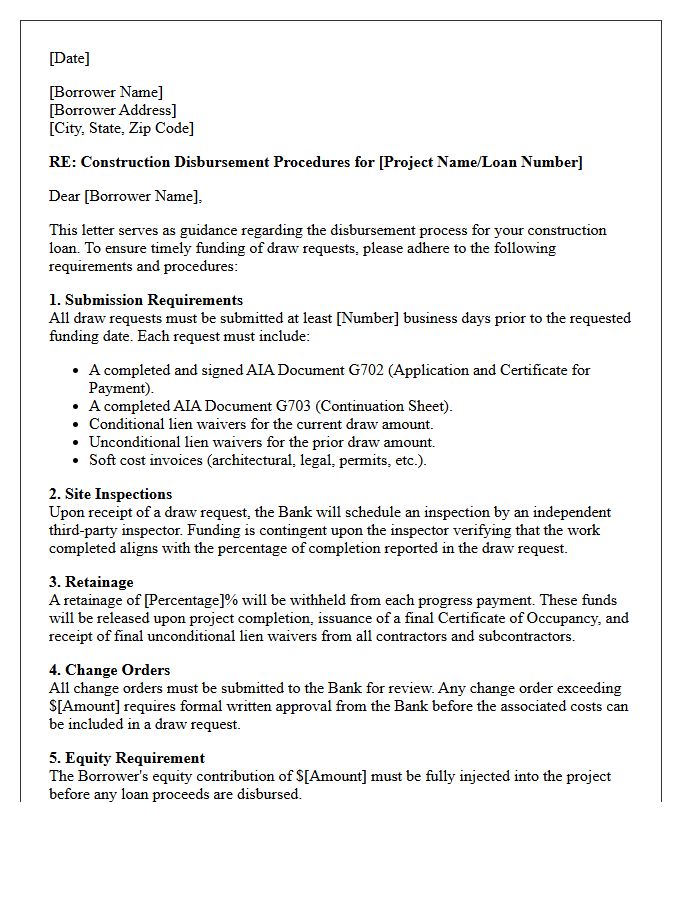

Commercial Real Estate Construction Disbursement Guidance Letter

A Construction Disbursement Guidance Letter is a critical legal document outlining the specific procedures for releasing loan funds during a project. It establishes the compliance requirements, such as lien waivers, architect certifications, and inspection reports, necessary to mitigate financial risk. By clearly defining the draw request process and budget oversight expectations, the letter ensures transparent communication between lenders and developers. Adhering to these guidelines prevents funding delays and protects the lender's priority interest throughout the commercial real estate development lifecycle.

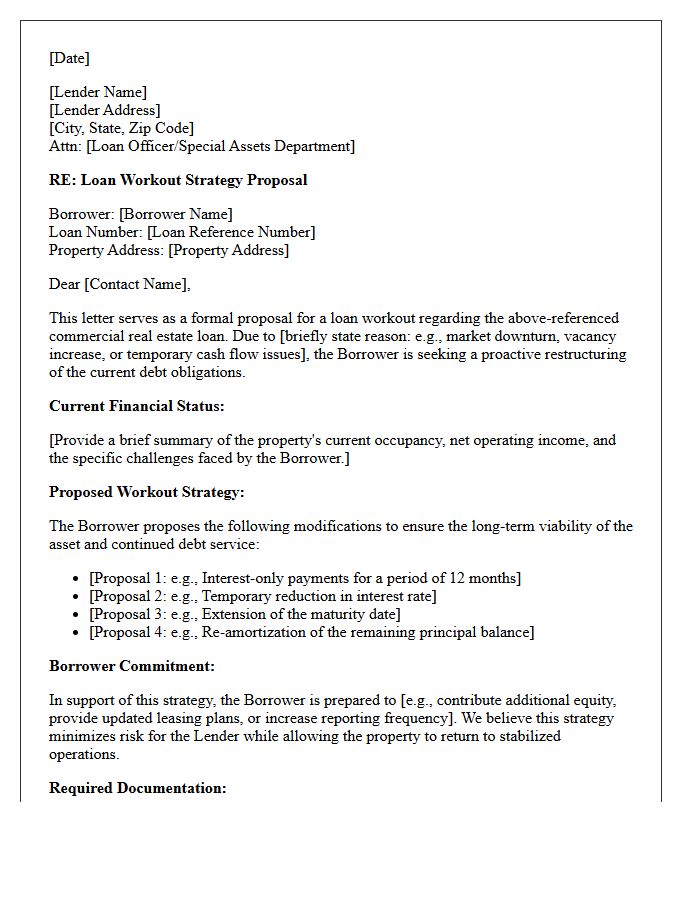

Commercial Real Estate Loan Workout Strategy Letter

A Commercial Real Estate Loan Workout Strategy Letter is a formal proposal sent by a borrower to a lender to initiate debt restructuring. It serves as a pre-negotiation tool to address financial distress and avoid foreclosure. The document outlines the borrower's current financial hardship, property performance, and a proposed plan for modified terms, such as interest rate reductions or maturity extensions. Clear financial transparency and a viable recovery roadmap are essential to demonstrate good faith and convince the lender that a workout is more beneficial than legal recovery actions.

What is the primary purpose of a Commercial Real Estate (CRE) Lending Guidance Letter?

A CRE Lending Guidance Letter is issued by financial regulators to provide banking institutions with expectations for managing risks associated with high concentrations in commercial real estate. It outlines best practices for portfolio stress testing, underwriting standards, and capital adequacy to ensure institutional stability during market fluctuations.

When are CRE concentration levels considered a regulatory concern?

Regulators typically flag institutions for enhanced monitoring if total commercial real estate loans represent 300% or more of total risk-based capital, or if construction and land development loans represent 100% or more of total risk-based capital. Exceeding these thresholds often triggers a requirement for more robust risk management frameworks.

What risk management practices are recommended in CRE lending guidance?

Guidance letters emphasize the necessity of frequent portfolio stress testing, rigorous sensitivity analysis of interest rates and vacancy levels, and the maintenance of diversified loan types. Institutions are also expected to perform regular appraisals and market analysis to ensure collateral values remain aligned with outstanding debt.

How does CRE guidance impact loan underwriting standards?

The guidance encourages lenders to maintain disciplined Loan-to-Value (LTV) ratios, Debt Service Coverage Ratios (DSCR), and formal contingency planning. It discourages "relaxed" underwriting during periods of high competition and requires lenders to document clear exceptions to internal credit policies.

What are the consequences of non-compliance with CRE lending guidance?

Failure to adhere to the guidance can result in formal enforcement actions, higher capital requirements (Pillar 2 charges), and mandatory restrictions on further CRE portfolio growth. Regulators may also require the institution to increase its Allowance for Credit Losses (ACL) to mitigate potential exposure.

Comments