The Deposit Insurance Assessment Rate Letter notifies financial institutions of their quarterly premium adjustments based on risk profiles and balance sheets. Understanding these assessments is vital for maintaining regulatory compliance and managing operational costs effectively. This guide outlines the factors influencing rate changes and provides official communication standards for banks. Below are some ready to use template.

Image cover: Official Notification Templates for Deposit Insurance Assessment Rate Changes

Letter Samples List

- Initial Deposit Insurance Assessment Rate Notification Letter

- Deposit Insurance Assessment Rate Appeal Request Letter

- Revised Deposit Insurance Assessment Rate Adjustment Letter

- Deposit Insurance Assessment Rate Acknowledgment Letter

- Deposit Insurance Assessment Rate Payment Remittance Letter

- Deposit Insurance Assessment Base Calculation Review Letter

- Deposit Insurance Assessment Rate Reconsideration Letter

- Quarterly Deposit Insurance Assessment Rate Update Letter

- Deposit Insurance Assessment Rate Discrepancy Dispute Letter

- Deposit Insurance Assessment Rate Exception Request Letter

- Deposit Insurance Assessment Rate Audit Findings Letter

- Deposit Insurance Assessment Rate Late Payment Penalty Letter

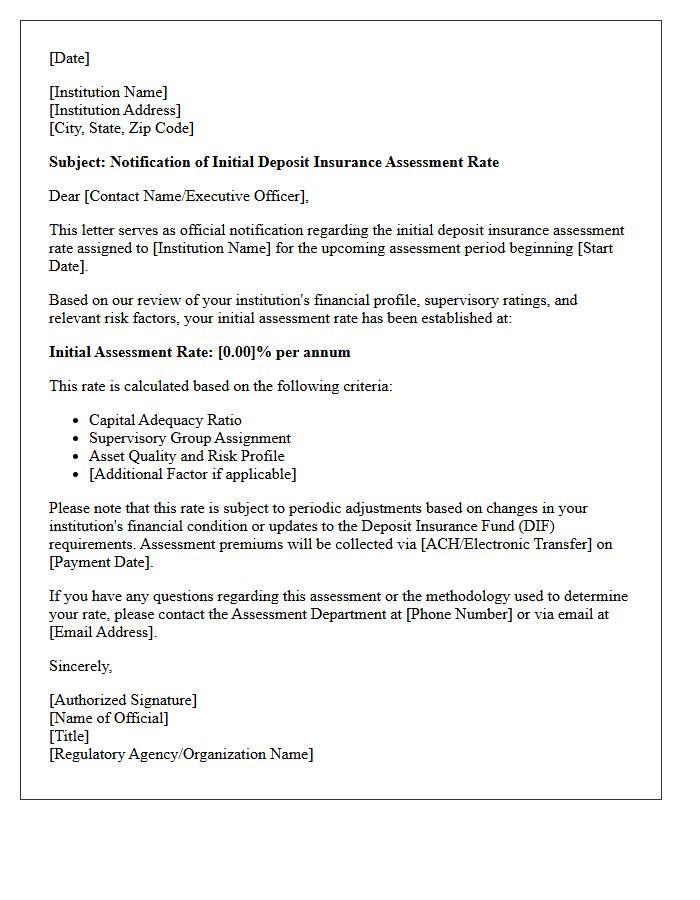

Initial Deposit Insurance Assessment Rate Notification Letter

The Initial Deposit Insurance Assessment Rate Notification Letter is a formal document sent by the FDIC to newly insured financial institutions. It specifies the assessment rate applied to a bank's deposits to determine its insurance premiums. This rate is calculated based on the institution's risk profile and supervisory ratings. Understanding this notification is essential for financial planning, as it dictates the ongoing cost of maintaining federal deposit insurance and ensures compliance with regulatory funding requirements for the Deposit Insurance Fund.

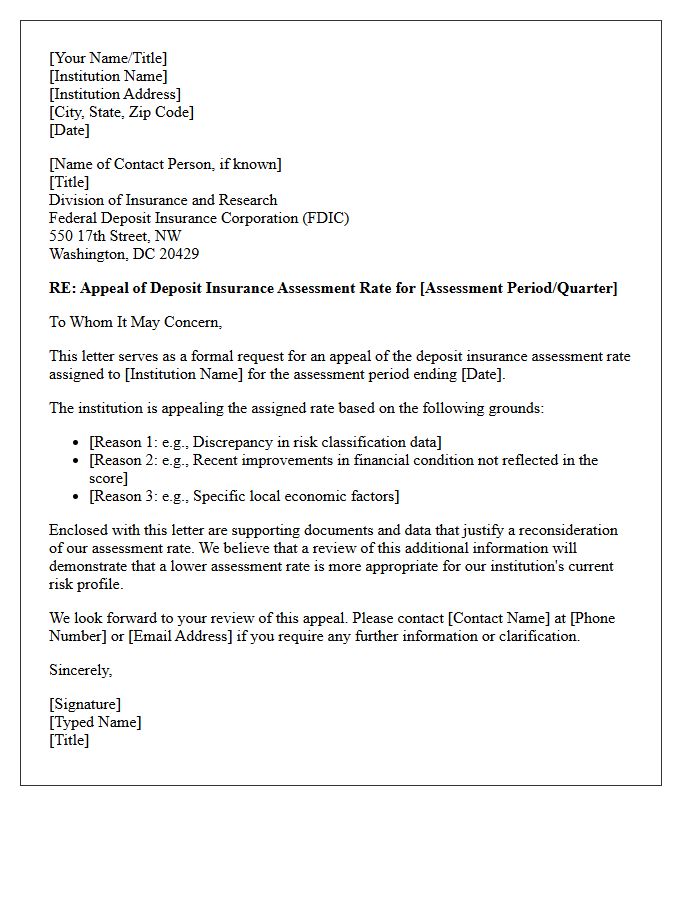

Deposit Insurance Assessment Rate Appeal Request Letter

To challenge a bank levy, institutions must submit a Deposit Insurance Assessment Rate Appeal Request Letter to the FDIC. This formal document must clearly outline the factual or legal errors in the assigned risk category. The request must be filed within 90 days of the assessment notice, providing supporting data to justify a rate reduction. Timely submission is critical to protecting capital and ensuring fair regulatory treatment. A well-structured appeal can significantly lower operational costs by correcting inaccurate risk profiles or financial data used in the calculation.

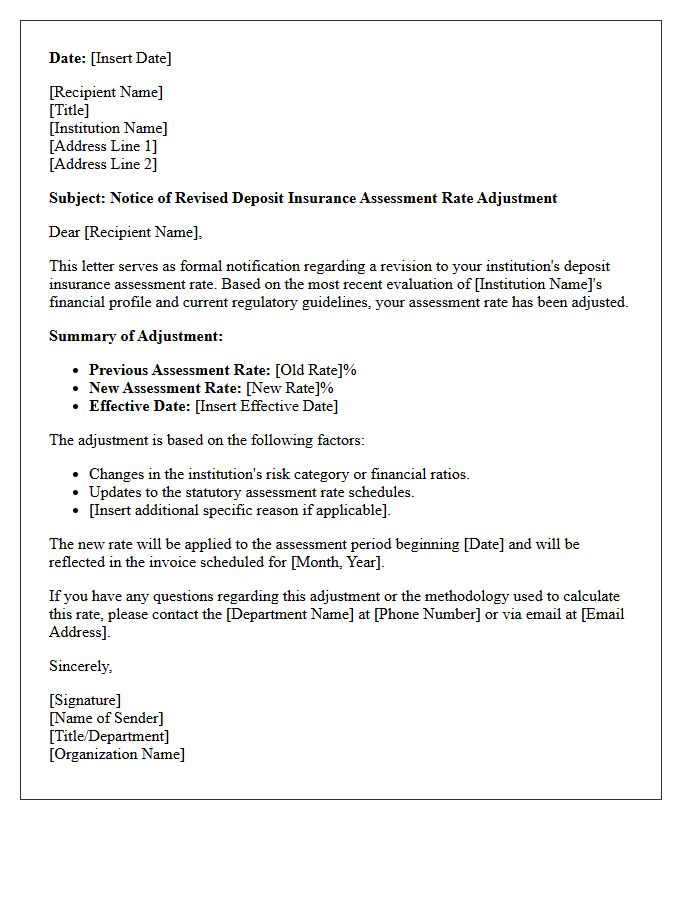

Revised Deposit Insurance Assessment Rate Adjustment Letter

The Revised Deposit Insurance Assessment Rate Adjustment Letter notifies financial institutions of updated schedules for FDIC insurance premiums. This regulatory update ensures the Deposit Insurance Fund (DIF) maintains its statutory reserve ratio. Banks must review these adjustments to accurately forecast operating expenses and ensure compliance with new liquidity requirements. The rates are typically determined by an institution's risk profile, asset size, and supervisory ratings. Understanding these changes is critical for maintaining financial stability and adapting to evolving federal banking regulations and assessment methodologies.

Deposit Insurance Assessment Rate Acknowledgment Letter

A Deposit Insurance Assessment Rate Acknowledgment Letter is a formal notification from the FDIC informing an insured depository institution of its specific quarterly assessment risk rank. This document confirms the pricing multipliers used to calculate the premiums a bank must pay to the Deposit Insurance Fund. It is essential for financial compliance and internal auditing, as it outlines the assessment base and risk-based adjustments. Banks should verify this data immediately to ensure accurate capital management and to resolve any discrepancies regarding their institutional risk profile or classification.

Deposit Insurance Assessment Rate Payment Remittance Letter

A Deposit Insurance Assessment Rate Payment Remittance Letter is a formal notice issued by regulatory bodies like the FDIC to financial institutions. This document specifies the assessment rate and the total amount due to maintain the Deposit Insurance Fund. It ensures banks contribute their fair share based on their risk profile and quarterly liabilities. Understanding this letter is crucial for compliance, as it outlines the automated withdrawal date and the calculation methodology used to determine the institution's insurance premiums and overall financial stability requirements.

Deposit Insurance Assessment Base Calculation Review Letter

The Deposit Insurance Assessment Base Calculation Review Letter notifies financial institutions of discrepancies in their reported assessment foundations. It is a critical compliance document issued by the FDIC to ensure banks maintain accurate calculations for insurance premiums. Recipients must reconcile reported data with regulatory standards to rectify potential underpayments or overpayments. Addressing these findings promptly is essential for maintaining regulatory transparency and avoiding financial penalties. Institutions should treat this letter as a formal audit of their liability structure and risk-based assessment profile within the federal banking system.

Deposit Insurance Assessment Rate Reconsideration Letter

A Deposit Insurance Assessment Rate Reconsideration Letter is a formal appeal submitted by a financial institution to the FDIC to challenge its risk classification. This document must provide specific evidence demonstrating that the current assessment does not accurately reflect the bank's true risk profile. It is a critical tool for reducing insurance premiums and correcting data inaccuracies. Timely submission is essential, as banks typically have a 90-day window from the invoice date to request a formal review of their assessment score to ensure fair regulatory pricing.

Quarterly Deposit Insurance Assessment Rate Update Letter

The Quarterly Deposit Insurance Assessment Rate Update Letter informs financial institutions of their specific FDIC assessment rates. It details the costs required to maintain the Deposit Insurance Fund based on risk classifications. Banks must review these statements to verify calculation accuracy and ensure sufficient liquidity for automated withdrawals. Changes in an institution's financial health or regulatory capital levels can significantly impact these quarterly premiums. Monitoring these updates is essential for effective expense management and maintaining regulatory compliance within the banking sector.

Deposit Insurance Assessment Rate Discrepancy Dispute Letter

A Deposit Insurance Assessment Rate Discrepancy Dispute Letter is a formal notification sent to the FDIC to challenge incorrect risk classifications or assessment calculations. Financial institutions use this document to rectify errors in their assessment base or assigned risk category, which directly impacts premium costs. To be effective, the letter must clearly outline the specific factual discrepancy, provide supporting financial documentation, and be submitted within the regulatory appeals deadline. Promptly filing this dispute ensures accurate reporting and prevents the overpayment of mandatory insurance assessments.

Deposit Insurance Assessment Rate Exception Request Letter

A Deposit Insurance Assessment Rate Exception Request Letter is a formal appeal sent to the FDIC or regulatory bodies to adjust a financial institution's premium risk category. Banks submit this document when specific risk metrics or data points do not accurately reflect their actual risk profile. Providing clear evidence of mitigated risks or corrected reporting can lead to lower insurance costs. Timely submission is crucial to ensuring a fair assessment and preserving capital, as this letter directly influences the quarterly assessment rates charged for federal deposit protection.

Deposit Insurance Assessment Rate Audit Findings Letter

A Deposit Insurance Assessment Rate Audit Findings Letter is a formal notification issued by regulatory bodies like the FDIC. This document summarizes the results of an evaluation regarding a financial institution's assessment base and risk classifications. It identifies any reporting discrepancies that may have led to underpayments or overpayments of premiums. Banks must carefully review these findings to ensure future regulatory compliance and adjust their financial records. Timely responses and corrective actions are essential to maintain accurate insurance funding and avoid potential penalties related to deposit insurance calculations.

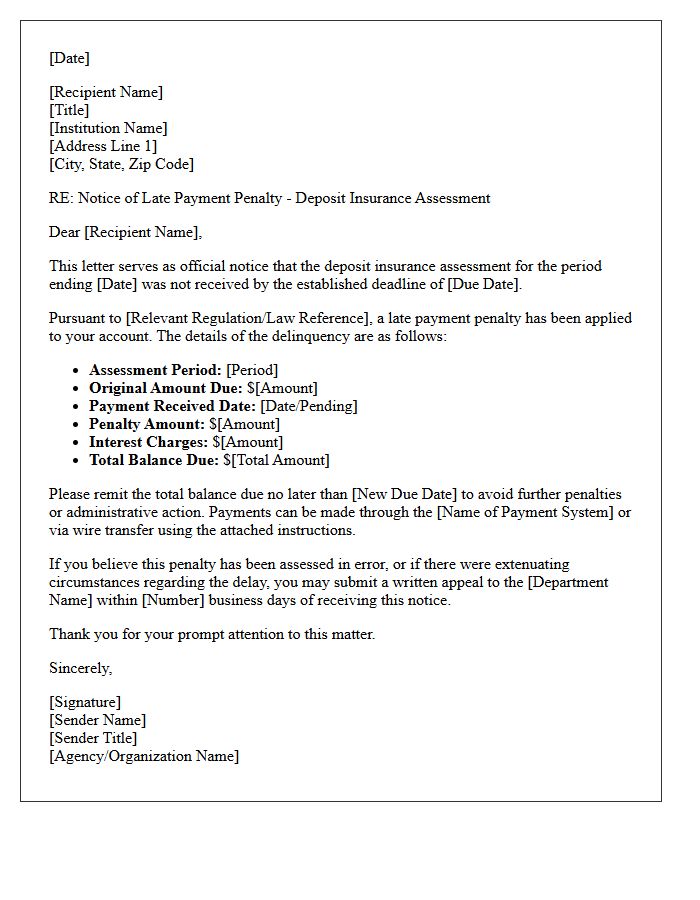

Deposit Insurance Assessment Rate Late Payment Penalty Letter

Receiving a Deposit Insurance Assessment Rate Late Payment Penalty Letter indicates that an insured institution failed to submit its quarterly assessment by the deadline. The FDIC imposes strict penalties calculated as a percentage of the overdue amount. It is essential to review the specific invoice details and payment instructions immediately to stop further accrual. Failure to resolve these delinquent balances can negatively affect your institution's compliance standing. Prompt electronic payment is the most effective way to address the notice and ensure your FDIC assessment status remains current.

What is a Deposit Insurance Assessment Rate Letter?

A Deposit Insurance Assessment Rate Letter is an official notification sent by regulatory authorities, such as the FDIC, to insured financial institutions. It details the specific assessment rate applied to the institution's deposits to determine the premiums owed to the insurance fund.

How is my institution's deposit insurance assessment rate calculated?

Assessment rates are calculated based on the institution's risk profile, taking into account factors such as supervisory ratings (CAMELS), financial ratios, and the institution's overall risk category as defined by federal regulations.

Where can I view my latest Assessment Rate Letter?

Authorized personnel can typically access and download the Assessment Rate Letter through the regulatory agency's secure online portal, such as the FDIC Connect (FC) website, under the assessment reporting section.

Can an institution appeal the assessment rate listed in the letter?

Yes, financial institutions have the right to request a formal review or appeal of their assessment risk assignment if they believe there is a factual or calculation error. Requests must generally be submitted in writing within the timeframe specified in the letter.

How often are assessment rate letters distributed to banks?

Assessment rate letters are generally issued on a quarterly basis, coinciding with the assessment invoice cycle, to reflect any changes in the institution's financial condition or updates to federal assessment regulations.

Comments