An Interest Rate Restriction Notification Letter is a formal document sent by lenders to inform borrowers that their interest rates have been capped or limited due to regulatory changes or policy updates. Understanding this legal notice ensures compliance and financial clarity for both parties. To help you draft this document efficiently, below are some ready to use templates.

Image cover: Official Interest Rate Restriction Notification: Templates and Compliance Guide

Letter Samples List

- Statutory Interest Rate Cap Compliance Letter

- Maximum Allowable Interest Rate Adjustment Letter

- Usury Law Interest Rate Restriction Letter

- Regulatory Interest Rate Ceiling Notification Letter

- Account Interest Rate Modification And Restriction Letter

- Credit Card Interest Rate Limit Notification Letter

- Mortgage Interest Rate Cap Enforcement Letter

- Commercial Loan Interest Rate Restriction Letter

- Central Bank Interest Rate Mandate Notification Letter

- Variable Rate Cap Restriction Notice Letter

- Overdraft Interest Rate Limitation Notification Letter

- Fixed Term Deposit Rate Restriction Letter

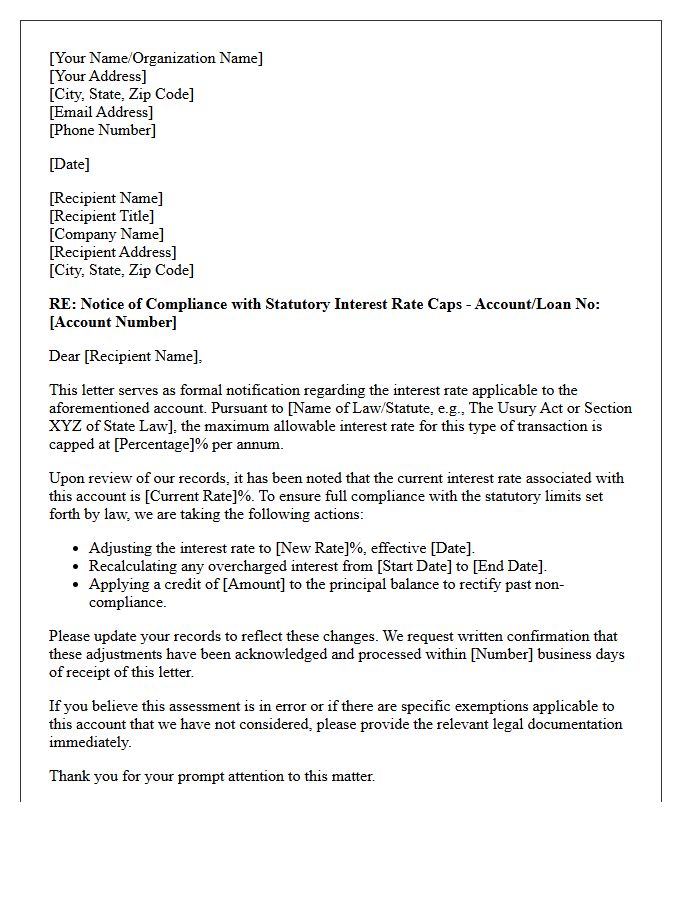

Statutory Interest Rate Cap Compliance Letter

A Statutory Interest Rate Cap Compliance Letter is a formal document verifying that a lender's interest charges remain within legal boundaries set by state or federal laws. This notice protects consumers from usury by ensuring financial institutions do not exceed the maximum allowable rates. It serves as essential proof of regulatory adherence during audits or legal disputes. Maintaining this compliance is vital for financial transparency and mitigating legal risks associated with predatory lending practices, ensuring that all loan agreements remain enforceable and valid under current consumer protection statutes.

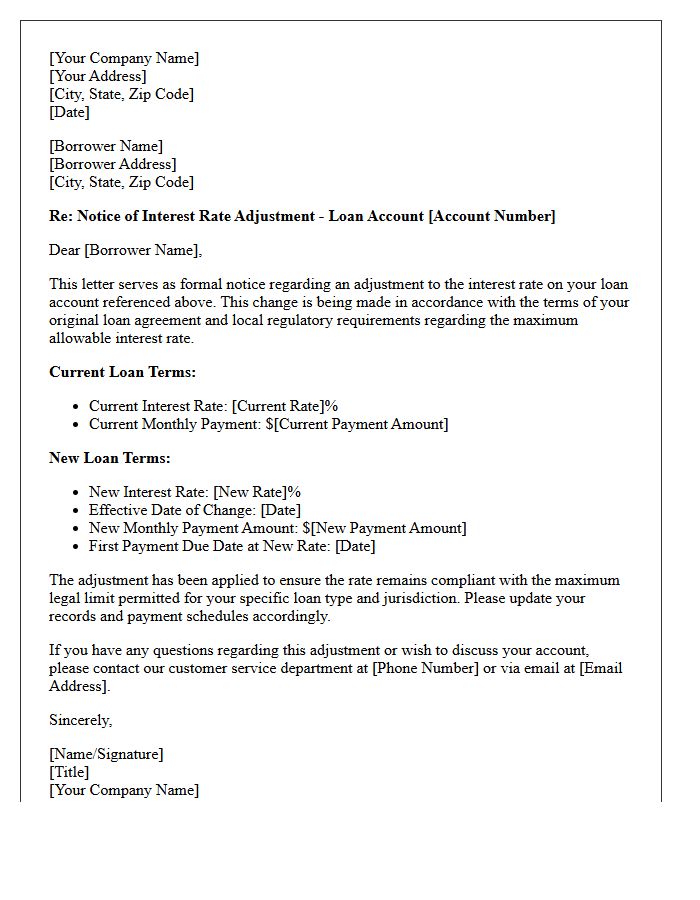

Maximum Allowable Interest Rate Adjustment Letter

A Maximum Allowable Interest Rate Adjustment Letter is a critical notice sent to borrowers when their adjustable-rate mortgage (ARM) reaches its lifetime cap. This legal document confirms that the interest rate has hit the absolute ceiling defined in the loan contract. Once this limit is reached, the rate can never increase further, providing payment stability for the remaining term. Homeowners must review this letter to verify the final interest rate and update their financial planning, as it signals the end of potential upward fluctuations in monthly principal and interest obligations.

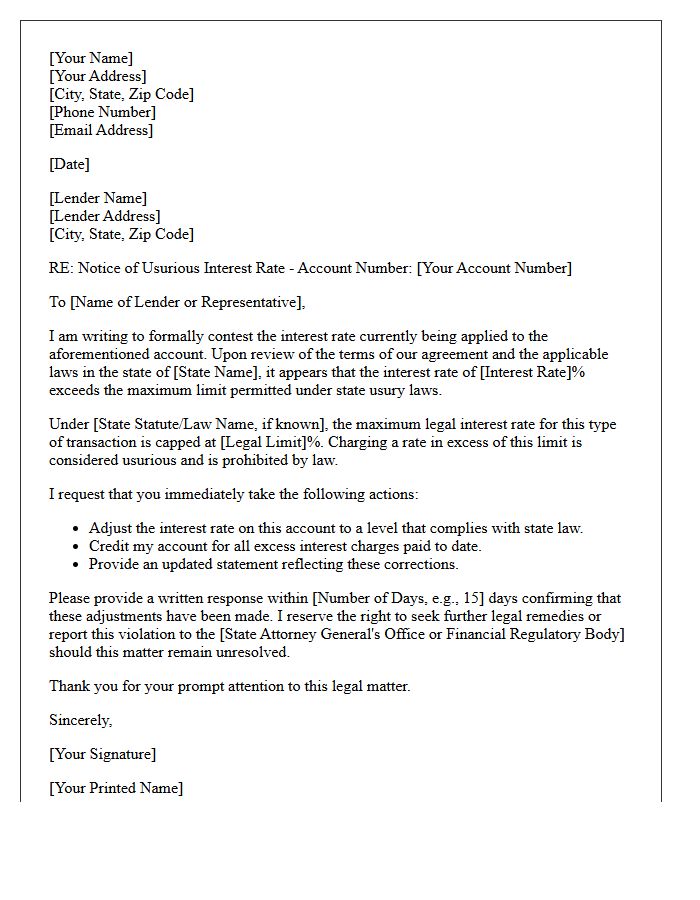

Usury Law Interest Rate Restriction Letter

A Usury Law Interest Rate Restriction Letter is a formal legal notice issued to ensure lending agreements comply with statutory interest rate caps. These laws prevent creditors from charging excessive interest, protecting borrowers from predatory financial practices. The letter typically identifies the specific legal limits within a jurisdiction and demands an immediate adjustment to the loan terms. Failure to adhere to these restrictions can render a contract unenforceable and subject the lender to significant penalties or civil litigation under state or federal consumer protection statutes.

Regulatory Interest Rate Ceiling Notification Letter

A Regulatory Interest Rate Ceiling Notification Letter is a formal legal document informing borrowers of the maximum allowable interest rate permitted by law. This notice ensures transparency by limiting the cost of credit and protecting consumers from usury. It serves as a compliance mechanism to verify that lending terms remain within strict government mandates. Understanding these caps is essential for evaluating debt affordability and ensuring financial institutions adhere to fair lending practices and established statutory rate limits during the loan lifecycle.

Account Interest Rate Modification And Restriction Letter

An Account Interest Rate Modification and Restriction Letter is a formal notice sent by a financial institution to inform a customer about changes to their earning potential. This document details adjustments to the annual percentage yield, often due to market fluctuations or policy updates. It may also outline new limitations on account activity or withdrawal frequencies. Reviewing this letter is essential, as it directly impacts your investment returns and liquidity. Understanding these modifications ensures you can adjust your financial strategy to maintain optimal capital growth and account compliance.

Credit Card Interest Rate Limit Notification Letter

A Credit Card Interest Rate Limit Notification Letter is a formal document informing cardholders of changes to their Annual Percentage Rate (APR). Under financial regulations, lenders must provide a 45-day advance notice before increasing interest rates on existing balances or new purchases. This letter details the specific reasons for the adjustment, the effective date, and the consumer's right to opt-out by closing the account. Reviewing these notifications is essential for managing debt repayment costs and maintaining overall financial health in a changing economic landscape.

Mortgage Interest Rate Cap Enforcement Letter

A Mortgage Interest Rate Cap Enforcement Letter is a formal legal notice sent to lenders to ensure compliance with contractual interest rate ceilings. This document demands that a financial institution strictly adheres to the maximum rate agreed upon in the mortgage contract, preventing overcharges. It is a critical tool for borrowers to challenge unauthorized rate hikes and protect their financial rights. By serving this notice, you hold the lender accountable for breach of contract and ensure your monthly payments remain within the legally defined limits of your loan agreement.

Commercial Loan Interest Rate Restriction Letter

A Commercial Loan Interest Rate Restriction Letter is a legal document used to cap interest rates on business financing. It protects borrowers from market volatility by setting a maximum threshold the lender can charge. This interest rate ceiling ensures predictable debt service costs, especially during periods of inflation or economic shifts. Understanding these terms is vital for maintaining cash flow stability and long-term financial planning. Reviewing the specific triggers and duration within the letter helps mitigate risk and prevents unexpected increases in monthly repayment obligations.

Central Bank Interest Rate Mandate Notification Letter

A Central Bank Interest Rate Mandate Notification Letter is an official communication detailing adjustments to benchmark borrowing costs. This document outlines policy shifts designed to control inflation and stabilize the national currency. It serves as a critical signal for commercial lenders to recalibrate their own lending and savings rates. Understanding this notification is essential for evaluating economic trends, as it directly impacts mortgage affordability, corporate investment strategies, and overall consumer purchasing power within the financial ecosystem.

Variable Rate Cap Restriction Notice Letter

A Variable Rate Cap Restriction Notice Letter informs borrowers that their interest rate has reached its maximum allowable limit under the loan agreement. This formal notification confirms that the periodic cap or lifetime ceiling has been triggered, preventing further increases despite market fluctuations. It is a critical legal document ensuring transparency regarding monthly payment stability and consumer protection rights. Borrowers should review this notice to understand their finalized repayment terms and evaluate long-term financial planning options while the interest rate remains restricted at its contractual peak.

Overdraft Interest Rate Limitation Notification Letter

An Overdraft Interest Rate Limitation Notification Letter is a formal document issued by financial institutions to inform customers about legally mandated caps on borrowing costs. This notice ensures transparency regarding the maximum interest rates applied to overdrawn accounts, protecting consumers from excessive fees. It typically outlines the effective date, specific rate adjustments, and any regulatory compliance measures taken. Reviewing this letter is essential for managing personal finances, as it directly impacts the total cost of short-term credit and helps account holders understand their financial obligations under current banking laws.

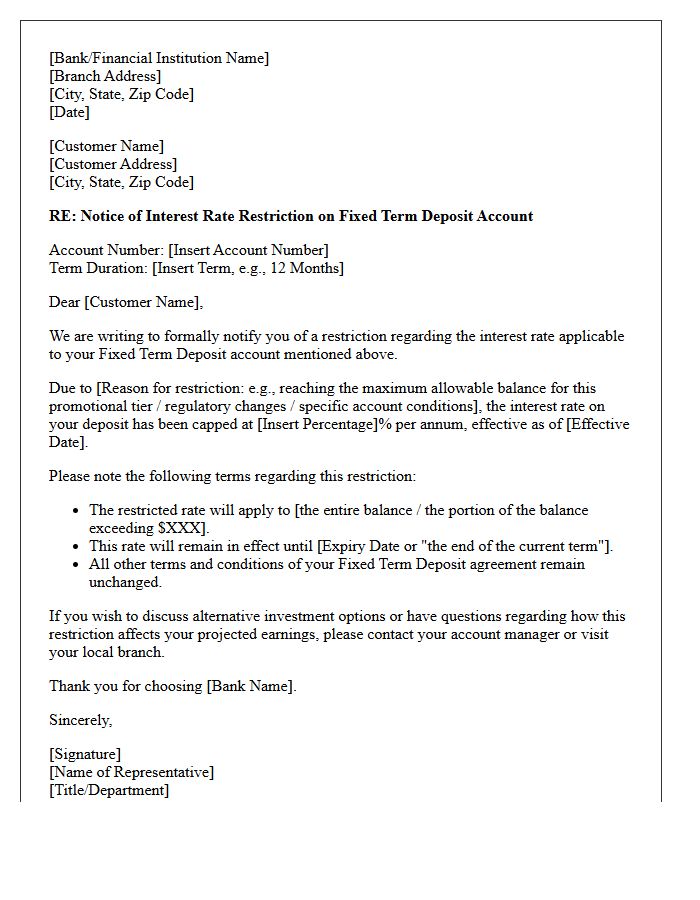

Fixed Term Deposit Rate Restriction Letter

A Fixed Term Deposit Rate Restriction Letter is a formal notice issued by financial regulators, such as the Central Bank, to a specific credit institution. This directive limits the maximum interest rate the bank can offer on new or renewing deposits. Such restrictions are typically implemented as a supervisory measure to ensure financial stability and prevent aggressive competition for funding that could jeopardize a bank's liquidity profile. For depositors, it means the bank cannot exceed a specific yield ceiling regardless of market trends or previous promotional offers.

What is an Interest Rate Restriction Notification Letter?

An Interest Rate Restriction Notification Letter is a formal document sent by a financial institution to inform a borrower that a legal cap or contractual limit has been applied to the interest rate on their loan or credit facility, often due to regulatory changes or specific relief acts like the SCRA.

Why did I receive a notice regarding interest rate restrictions?

You received this notice because your account qualifies for a maximum interest rate limit under federal or state law, or as a result of a proactive adjustment by the lender to comply with usury laws or military service protections.

How does an interest rate restriction affect my monthly payments?

An interest rate restriction typically lowers your monthly interest charge, resulting in a reduced total monthly payment or a larger portion of your payment being applied to the principal balance of the loan.

Is an interest rate restriction the same as a fixed-rate conversion?

No, an interest rate restriction is a ceiling placed on the rate to prevent it from exceeding a specific percentage, whereas a fixed-rate conversion permanently stabilizes the rate regardless of market fluctuations or legal caps.

Do I need to take action after receiving an Interest Rate Restriction Notification Letter?

In most cases, no action is required as the lender applies the restriction automatically; however, you should review the letter to confirm the effective date and ensure your billing statements reflect the updated lower rate.

Comments