Receiving a Demand for Payment is a critical warning that your lender may initiate legal action. If left unaddressed, this process often escalates into a threat of foreclosure, risking the loss of your home. Understanding your rights and responding promptly is essential to protecting your property and financial future. To help you take immediate action, below are some ready to use templates.

Image cover: Essential Templates and Legal Notices for Foreclosure Prevention and Payment Demands

Letter Samples List

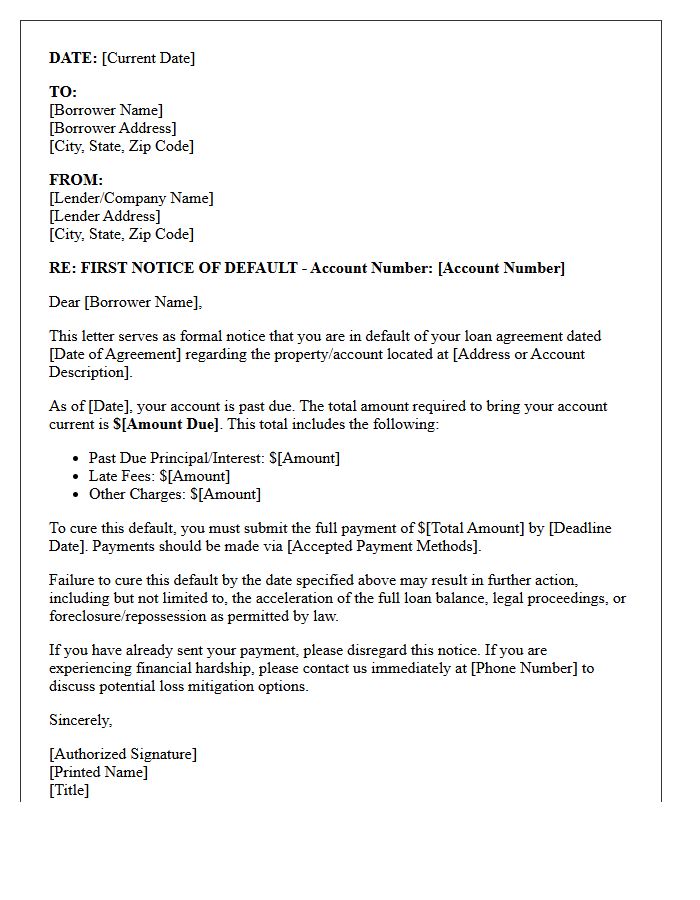

- First Notice of Default Letter

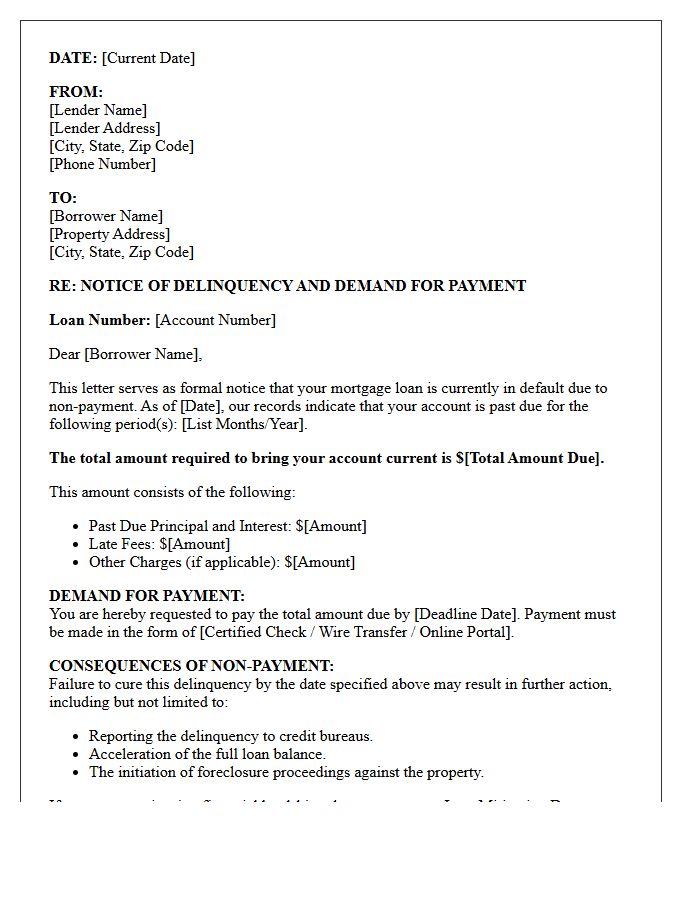

- Mortgage Delinquency Demand Letter

- Pre-Foreclosure Payment Demand Letter

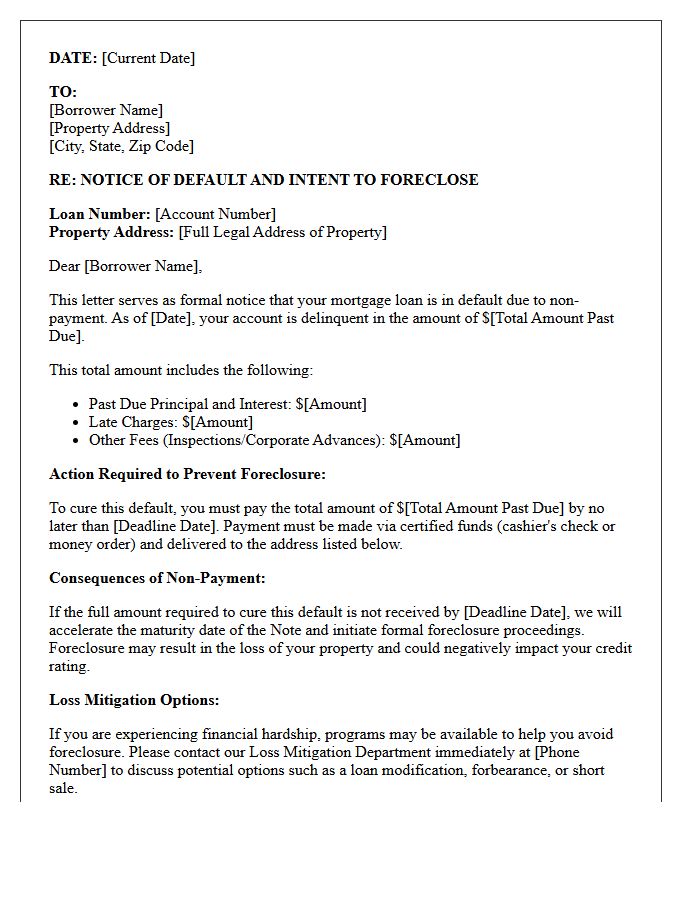

- Notice of Intent to Foreclose Letter

- Loan Acceleration Warning Letter

- Final Demand for Payment Letter

- Breach of Mortgage Agreement Letter

- Outstanding Balance and Foreclosure Warning Letter

- Commercial Loan Foreclosure Demand Letter

- Notice of Acceleration and Foreclosure Letter

- Final Warning Before Foreclosure Letter

- Mortgage Arrears Payment Demand Letter

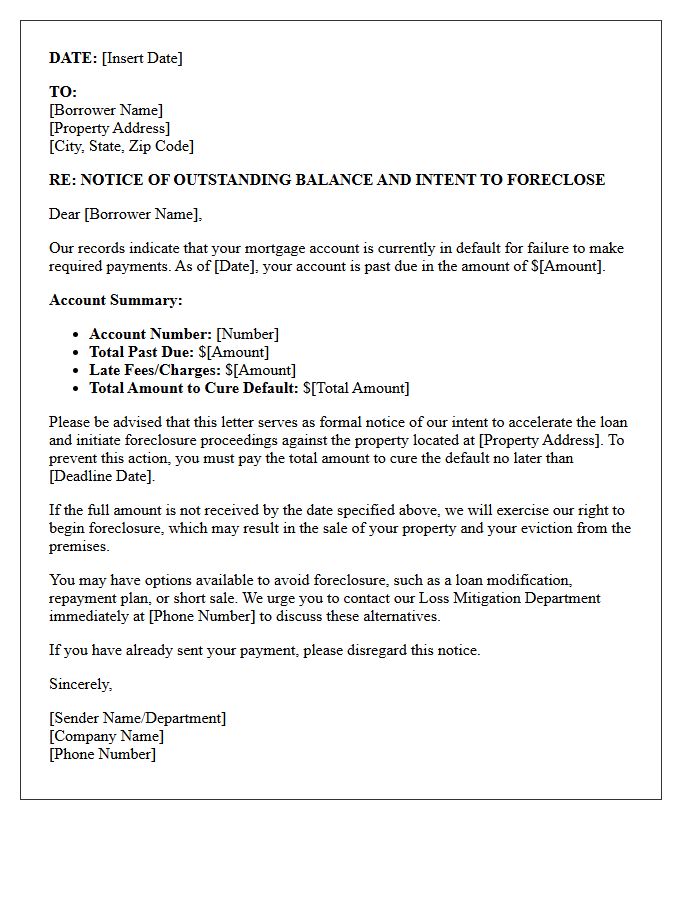

First Notice of Default Letter

A First Notice of Default is a formal legal document issued by a lender when a borrower falls significantly behind on mortgage payments. This letter marks the official commencement of the foreclosure process, providing a final warning to rectify the delinquency. It outlines the total amount owed, including late fees and interest, and specifies a cure period to pay the debt. Receiving this notice is critical because it signifies that your property is at immediate risk, requiring urgent action or legal consultation to prevent foreclosure and protect your home equity.

Mortgage Delinquency Demand Letter

A Mortgage Delinquency Demand Letter is a formal notice sent by lenders when a borrower misses payments. This critical document serves as a final warning before foreclosure proceedings begin. It outlines the total overdue amount, including late fees, and provides a specific deadline to cure the default. Understanding this letter is vital because it specifies the acceleration clause, meaning the entire loan balance could become due if the debt remains unpaid. Borrowers should prioritize immediate communication with their servicer to explore loss mitigation options and protect their home equity.

Pre-Foreclosure Payment Demand Letter

A Pre-Foreclosure Payment Demand Letter is a formal legal notice sent by lenders to borrowers who have defaulted on their mortgage. This document serves as a final warning, detailing the specific amount required to reinstate the loan. It outlines a strict deadline to pay the arrears before the bank initiates formal foreclosure proceedings. Receiving this letter is a critical stage for homeowners to seek loss mitigation options, such as loan modification or a short sale, to prevent the permanent loss of their property and severe credit damage.

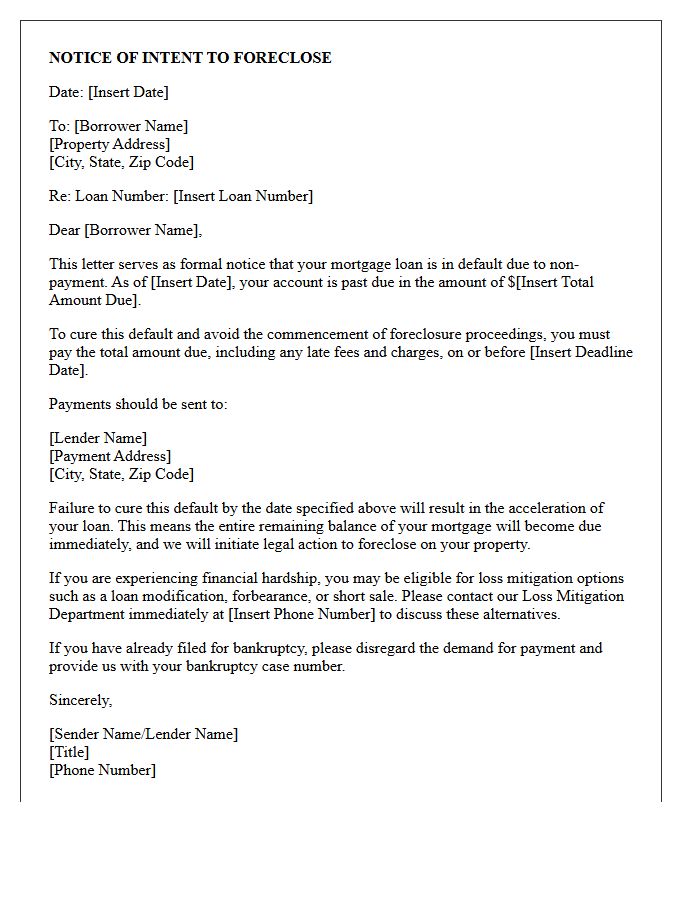

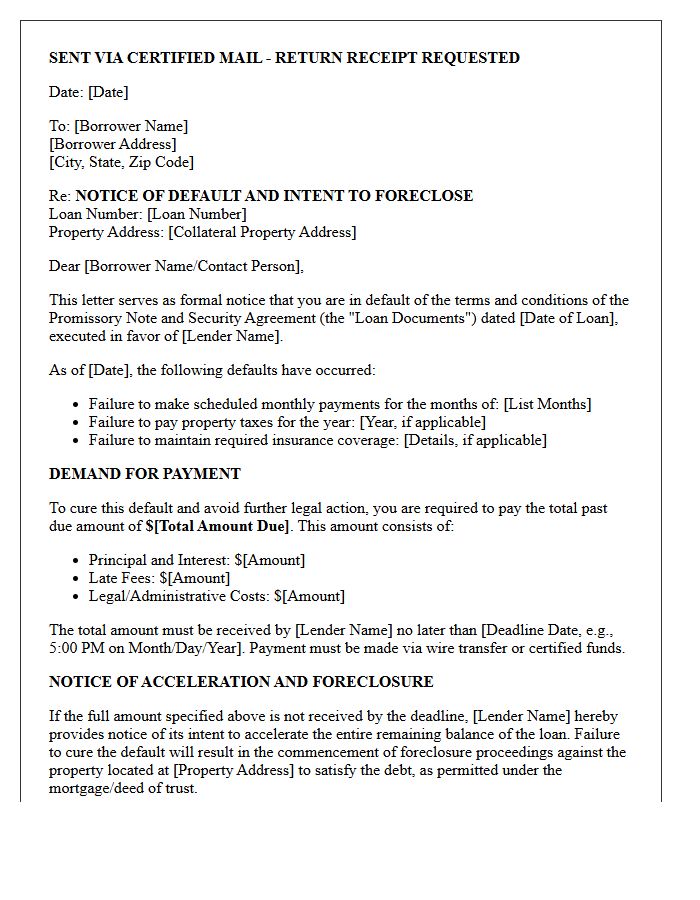

Notice of Intent to Foreclose Letter

A Notice of Intent to Foreclose is a formal legal warning sent by lenders to homeowners who have defaulted on mortgage payments. This document serves as a final opportunity to resolve the delinquency before the official foreclosure process begins. It outlines the specific amount required to cure the default and provides a deadline for payment. Understanding this notice is critical because it marks the transition from missed payments to potential property loss. Homeowners should immediately explore loss mitigation options, such as loan modification or repayment plans, to avoid further legal action.

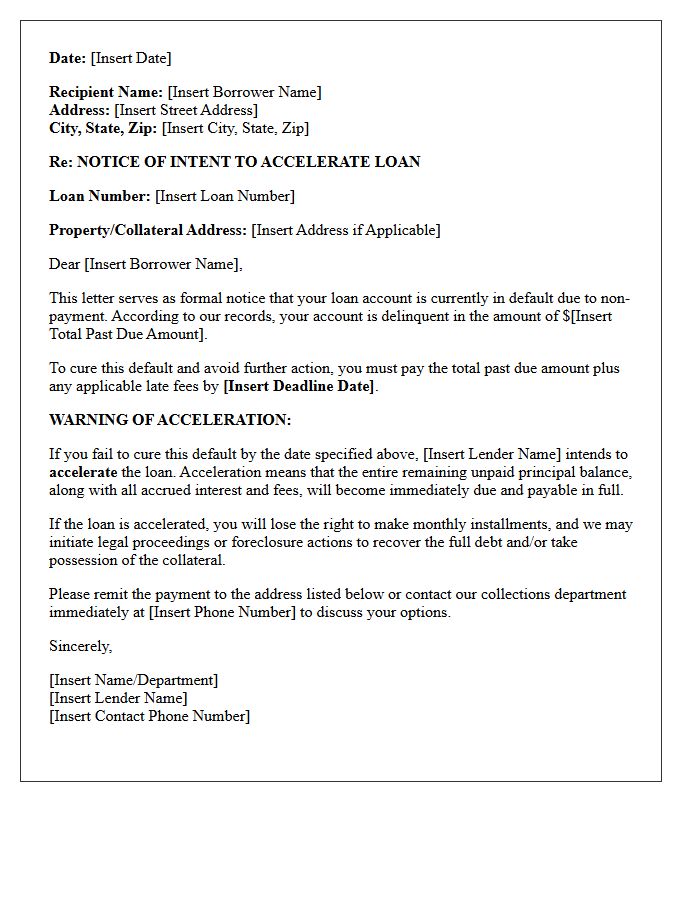

Loan Acceleration Warning Letter

A Loan Acceleration Warning Letter is a formal notice from a lender stating that a borrower has breached their contract, typically through default. This document serves as a final opportunity to cure the delinquency before the entire balance becomes due immediately. If the arrears are not paid within the specified timeframe, the lender will "accelerate" the debt, leading to foreclosure or legal action. It is a critical legal step that signifies the end of standard installment payments and the beginning of aggressive debt recovery procedures.

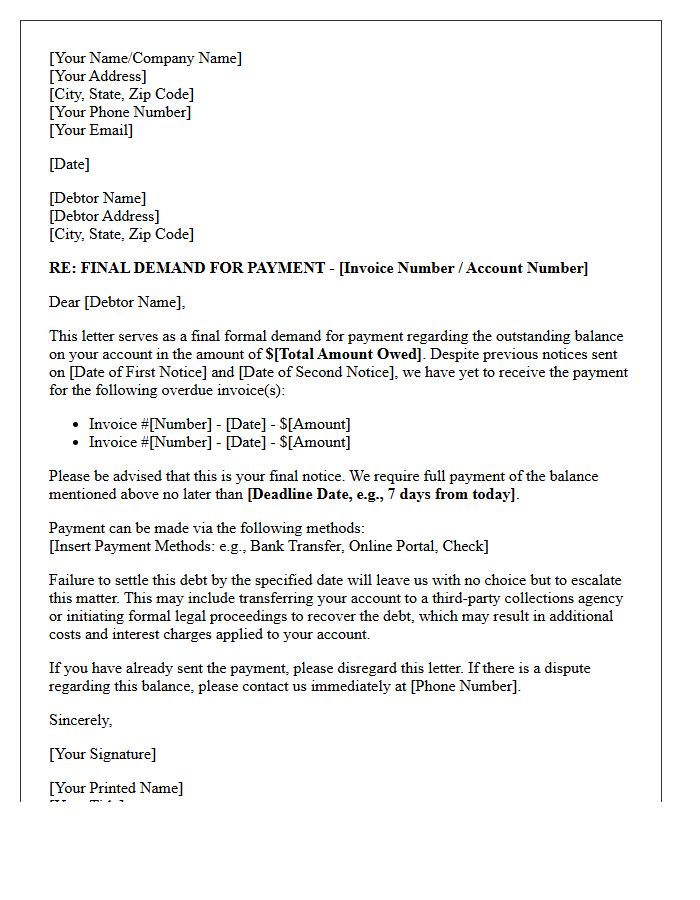

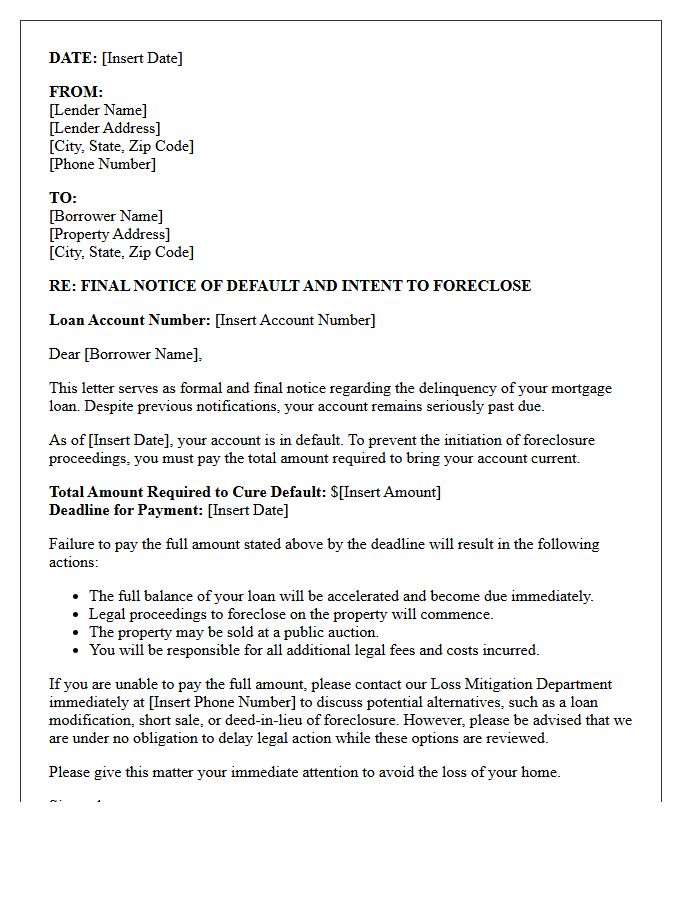

Final Demand for Payment Letter

A Final Demand for Payment Letter serves as a critical formal notice sent before initiating legal action. It explicitly outlines the outstanding debt, provides a specific deadline for settlement, and details the consequences of non-compliance, such as litigation or credit reporting. This document functions as essential evidence in court, demonstrating a good faith effort to resolve the dispute amicably. By clearly stating the intent to sue if payment is not received, it often prompts immediate resolution from delinquent debtors while establishing a clear paper trail for debt recovery procedures.

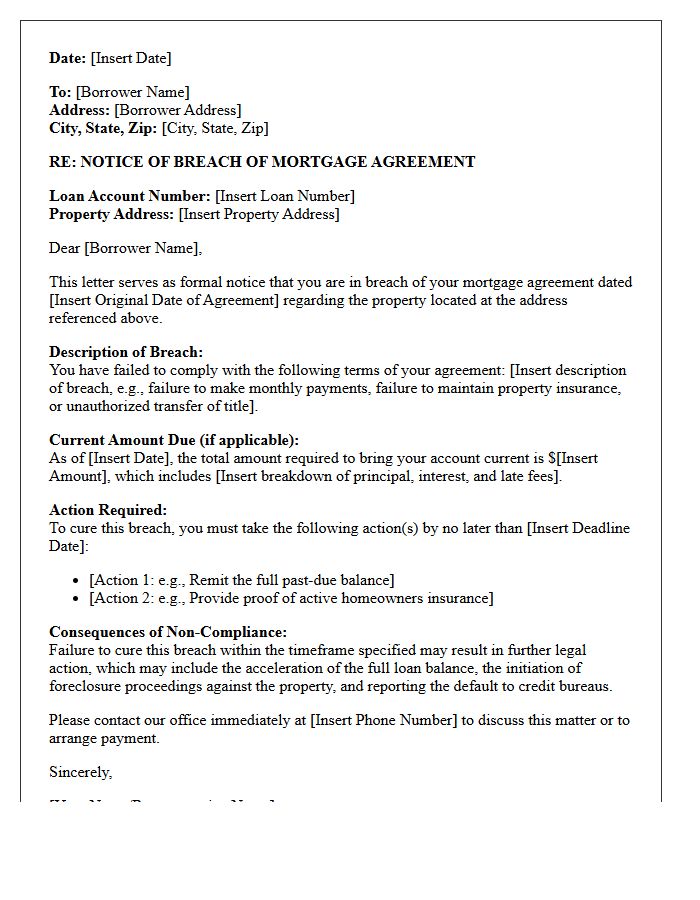

Breach of Mortgage Agreement Letter

A Breach of Mortgage Agreement Letter is a formal legal notice issued by a lender when a borrower violates specific loan terms. This document typically highlights delinquent payments or failure to maintain property insurance. It serves as a final warning before the lender initiates foreclosure proceedings. Recipients must act immediately by paying the arrears or contacting the servicer to discuss loss mitigation options. Ignoring this letter can lead to the permanent loss of the property and severe damage to your credit score.

Outstanding Balance and Foreclosure Warning Letter

Receiving an Outstanding Balance and Foreclosure Warning Letter is a critical legal notice indicating you are behind on mortgage payments. This document serves as a final demand for payment before your lender initiates formal legal action to seize the property. It outlines the total amount overdue, including late fees and interest. To prevent the loss of your home, you must take immediate action by contacting your servicer to discuss loss mitigation options, such as a loan modification or repayment plan, before the specified deadline expires.

Commercial Loan Foreclosure Demand Letter

A commercial loan foreclosure demand letter is a formal legal notice issued by a lender when a borrower defaults on a mortgage. This critical document specifies the default event, calculates the total outstanding debt, and provides a strict deadline for payment. It serves as a mandatory precursor to foreclosure proceedings, officially accelerating the debt and terminating the borrower's right to cure the default under original terms. Receiving this letter signifies the final opportunity to negotiate a workout agreement or face immediate legal action and potential loss of the commercial property.

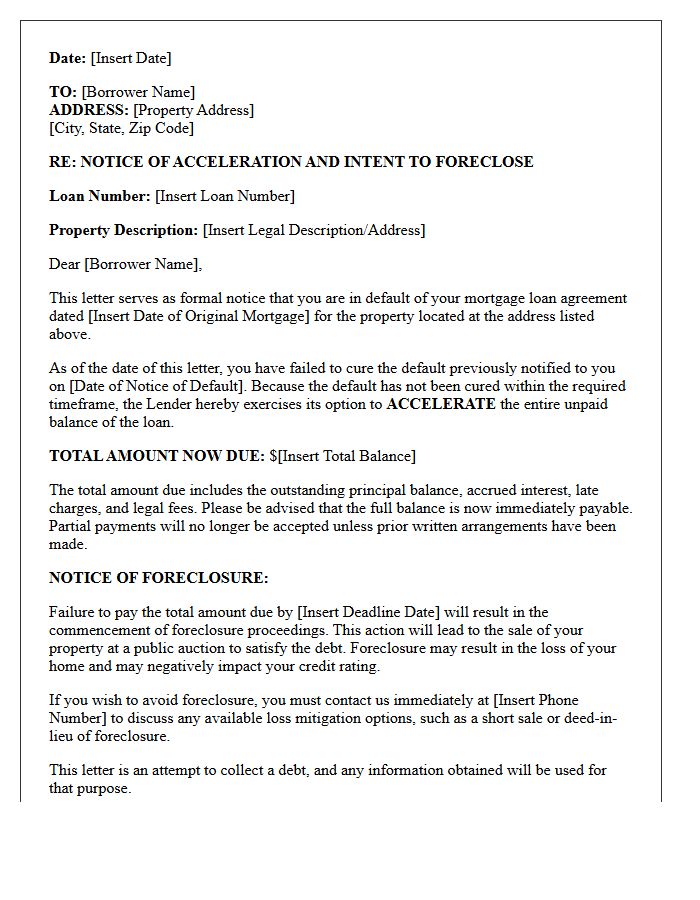

Notice of Acceleration and Foreclosure Letter

A Notice of Acceleration and Foreclosure is a critical legal document informing a borrower that their mortgage loan has been declared immediately due in full. This usually occurs after multiple missed payments, effectively terminating the installment plan. Receiving this letter signifies the final step before the lender initiates a formal foreclosure sale of the property. To prevent losing the home, homeowners must act quickly to negotiate a reinstatement, seek a loan modification, or explore legal defenses to halt the legal proceedings and resolve the outstanding debt.

Final Warning Before Foreclosure Letter

A Final Warning Before Foreclosure Letter is the last formal notice a lender sends before initiating legal action to seize a property. It signifies that the acceleration clause has been triggered, demanding full payment of the outstanding mortgage balance immediately. Receiving this document indicates that your window for loss mitigation or loan modification is closing rapidly. To prevent the loss of your home, you must contact your servicer or a housing counselor instantly to explore reinstatement options or alternative repayment plans before the case moves to court.

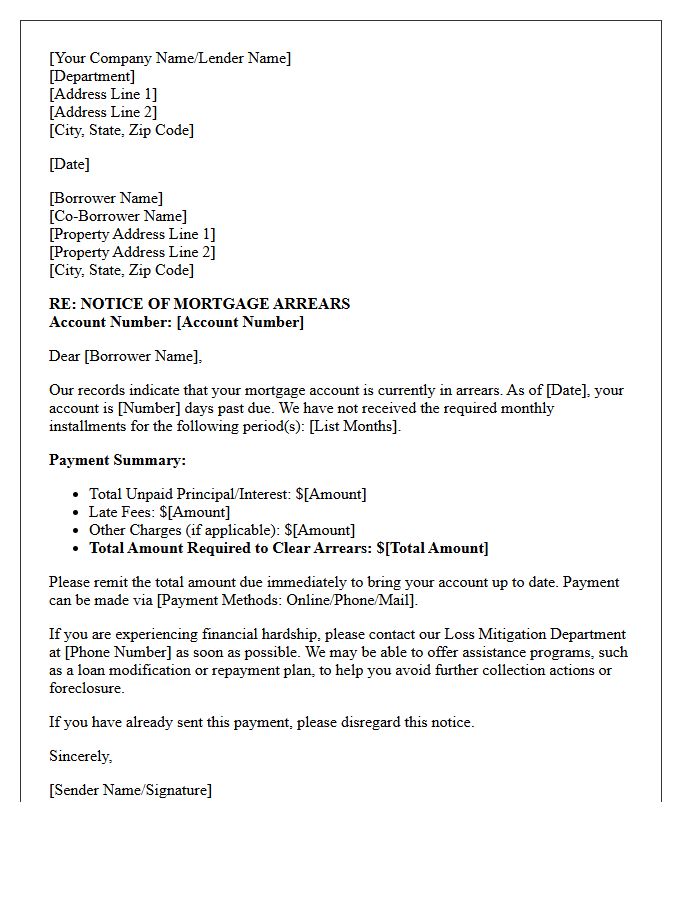

Mortgage Arrears Payment Demand Letter

A Mortgage Arrears Payment Demand Letter is a formal notice sent by lenders when a borrower misses scheduled payments. This document serves as a critical legal warning, outlining the total overdue balance and providing a specific deadline for rectification. Ignoring this letter can trigger the foreclosure process and severely impact your credit score. It is essential to communicate with your financial institution immediately to discuss repayment plans or loan modifications. Understanding this notice is the first step in protecting your property rights and preventing the loss of your home through legal default proceedings.

What is a Demand for Payment letter in the foreclosure process?

A Demand for Payment, often called a Notice of Default or Breach Letter, is a formal notification from a lender stating that a borrower has missed payments. This document serves as a final warning that the lender intends to accelerate the loan and initiate foreclosure proceedings if the total overdue balance is not paid by a specific deadline.

How long do I have to respond to a threat of foreclosure?

Typically, a Demand for Payment provides a 30-day window to "cure" the default by paying the outstanding amount. However, timelines vary by state law and mortgage contracts; failure to act within this period usually results in the file being transferred to an attorney to begin the legal foreclosure process.

Can a lender start foreclosure immediately after one missed payment?

While a lender may technically issue a late notice after one payment, federal law generally prohibits a servicer from officially starting foreclosure (filing the first legal notice) until the borrower is more than 120 days delinquent. This period is designed to allow homeowners to explore loss mitigation options.

What are the most effective ways to stop a foreclosure after receiving a demand letter?

Homeowners can halt foreclosure by applying for loss mitigation options such as a loan modification, a repayment plan, or a forbearance agreement. Reinstating the loan by paying the full past-due amount or negotiating a short sale are also viable methods to prevent the bank from seizing the property.

Does a Demand for Payment negatively affect my credit score?

Yes, by the time you receive a formal Demand for Payment, your credit score has likely already decreased due to reported 30, 60, or 90-day delinquencies. If the threat of foreclosure progresses to a public filing or a foreclosure sale, it can lower a credit score by 100 points or more and remain on a credit report for seven years.

Comments