A Notice of Default and Intent to Foreclose is a formal legal document issued by a lender when a borrower fails to make mortgage payments. It serves as the official warning that the foreclosure process has begun. Understanding your rights and timelines is essential to saving your home. To help you respond effectively, below are some ready to use template options.

Image cover: Official Notice of Default and Intent to Foreclose: Essential Templates and Legal Forms

Letter Samples List

- First Warning Of Mortgage Default Letter

- Official Notice Of Loan Default Letter

- Notice Of Intent To Foreclose Letter

- Delinquent Payment Acceleration Letter

- Breach Of Promissory Note Letter

- Commercial Property Foreclosure Letter

- Residential Mortgage Demand Letter

- Right To Cure Account Default Letter

- Bank Legal Action Intent Letter

- Final Foreclosure Ultimatum Letter

- Secured Asset Repossession Letter

- Notice Of Trustee Sale Letter

First Warning Of Mortgage Default Letter

Receiving a Notice of Default is the first formal step in the foreclosure process. This legal document alerts homeowners that they have breached their loan agreement by missing payments. It is crucial to act immediately by contacting your loan servicer to discuss mitigation options, such as loan modification or forbearance. Ignoring this letter can lead to the loss of your property. Reviewing the document for accuracy and seeking legal counsel or a housing counselor can help you navigate recovery and save your home before the situation escalates.

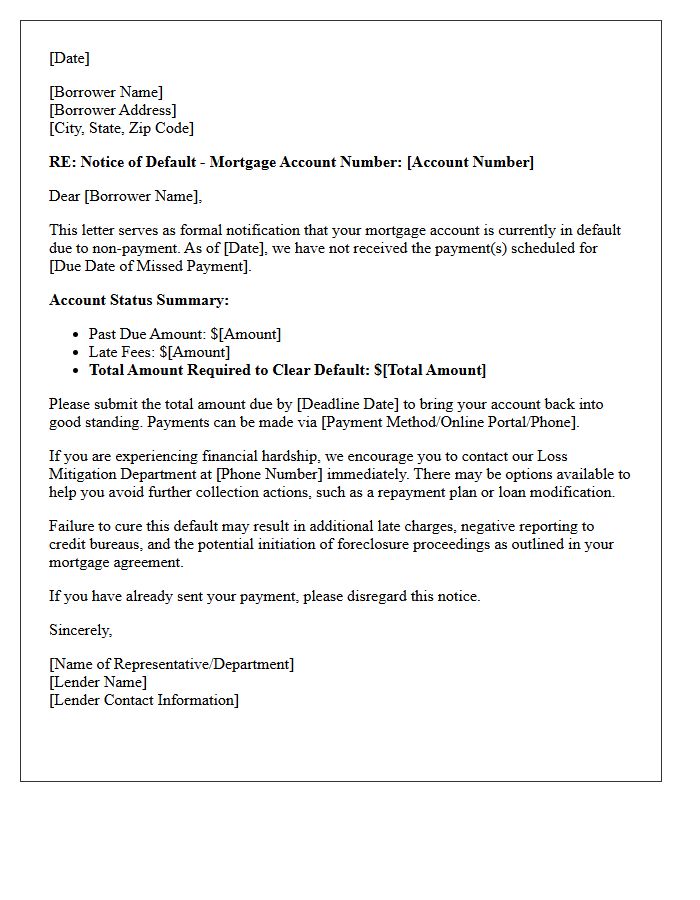

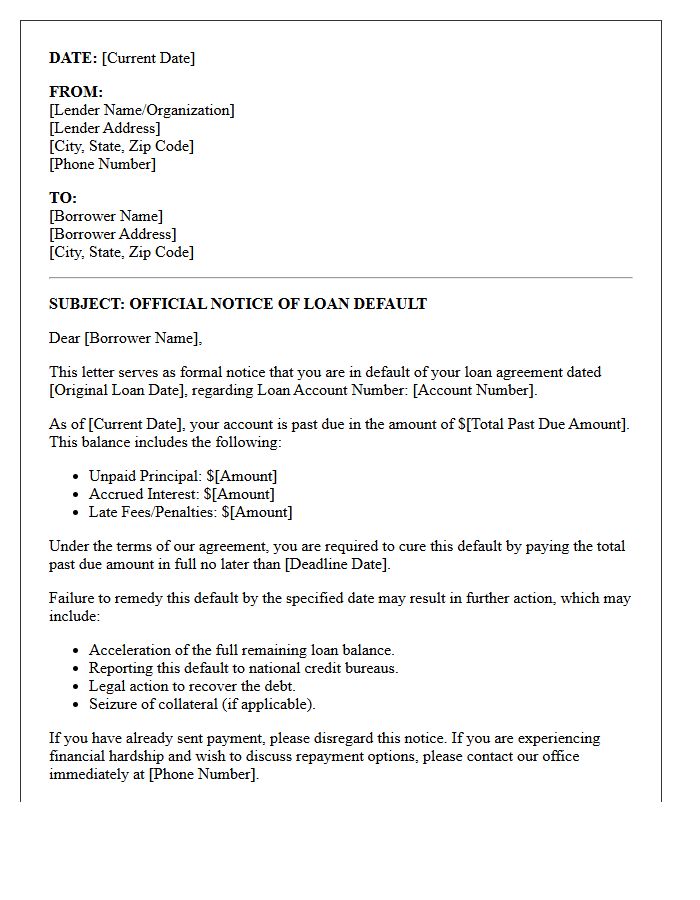

Official Notice Of Loan Default Letter

An Official Notice of Loan Default Letter is a formal legal document issued by a lender when a borrower fails to meet debt obligations. This critical notification serves as a final warning that the loan agreement has been breached. It outlines the total arrears, provides a specific timeframe to cure the default, and warns of impending foreclosure or legal action. Receiving this letter is the final stage before debt acceleration, making it essential for borrowers to contact their creditor immediately to discuss repayment options or loan modification to prevent asset loss.

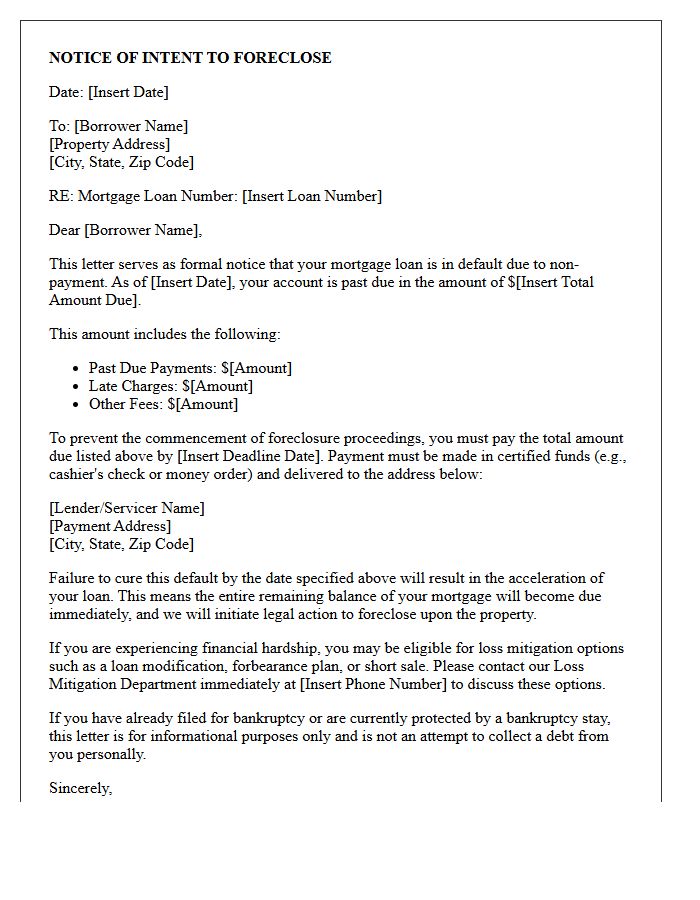

Notice Of Intent To Foreclose Letter

A Notice of Intent to Foreclose is a formal legal warning sent by a mortgage lender to a borrower who has defaulted on payments. This document serves as a pre-foreclosure notification, providing a final window to resolve the delinquency before official court proceedings or a sale begins. It typically outlines the total amount owed, including late fees, and specifies a cure date to pay the balance. Receiving this letter is critical; it represents the last opportunity to seek loss mitigation options, such as loan modification or a repayment plan, to save your home.

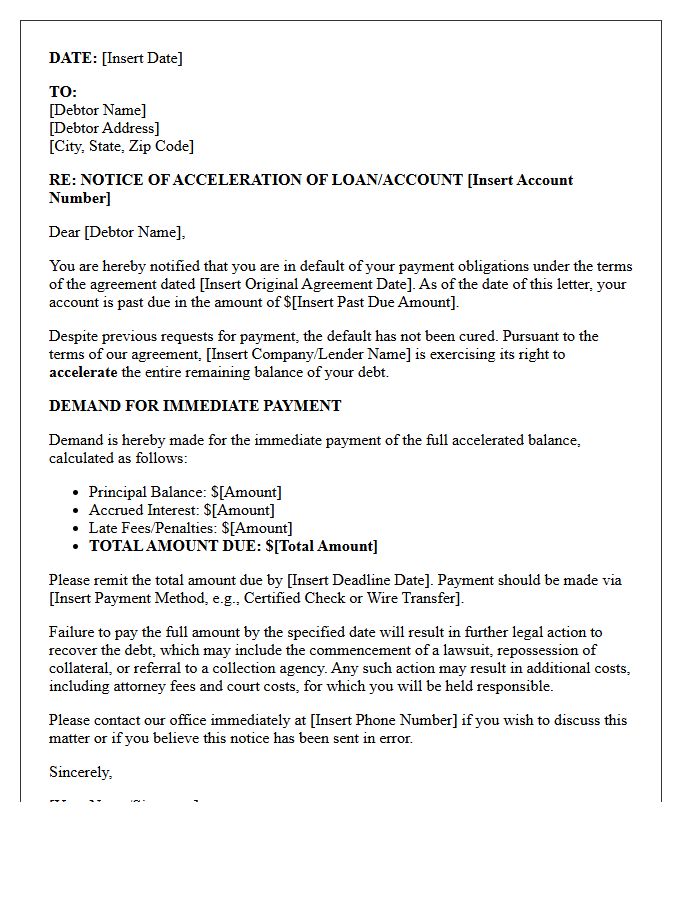

Delinquent Payment Acceleration Letter

A Delinquent Payment Acceleration Letter is a formal legal notice from a lender demanding immediate full repayment of the entire loan balance. This occurs after a borrower breaches the promissory note through non-payment. Once the acceleration clause is triggered, the borrower loses the right to pay in installments. It serves as a final warning before foreclosure or legal action, making it critical to contact the creditor immediately to discuss reinstatement options or loss mitigation to avoid losing the asset.

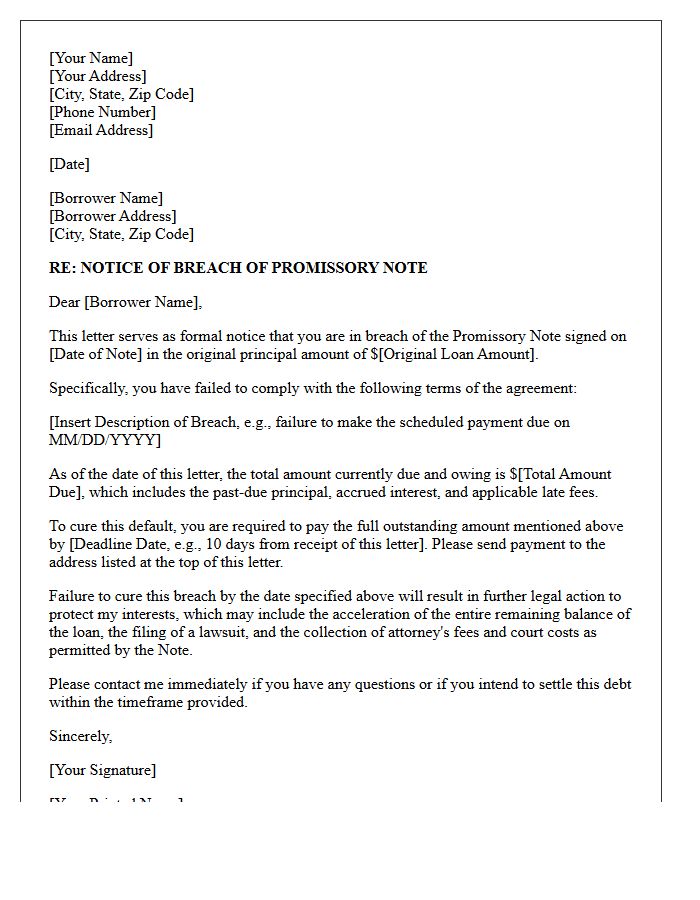

Breach Of Promissory Note Letter

A Breach of Promissory Note Letter is a formal legal notice sent to a borrower who has failed to make payments as agreed. It serves as a notice of default, officially documenting the violation of the loan contract. The letter typically outlines the outstanding balance, specifies the missed deadlines, and demands immediate restitution to avoid further legal action or litigation. Issuing this document is a critical first step in debt recovery, ensuring a clear paper trail for potential court proceedings or credit reporting actions.

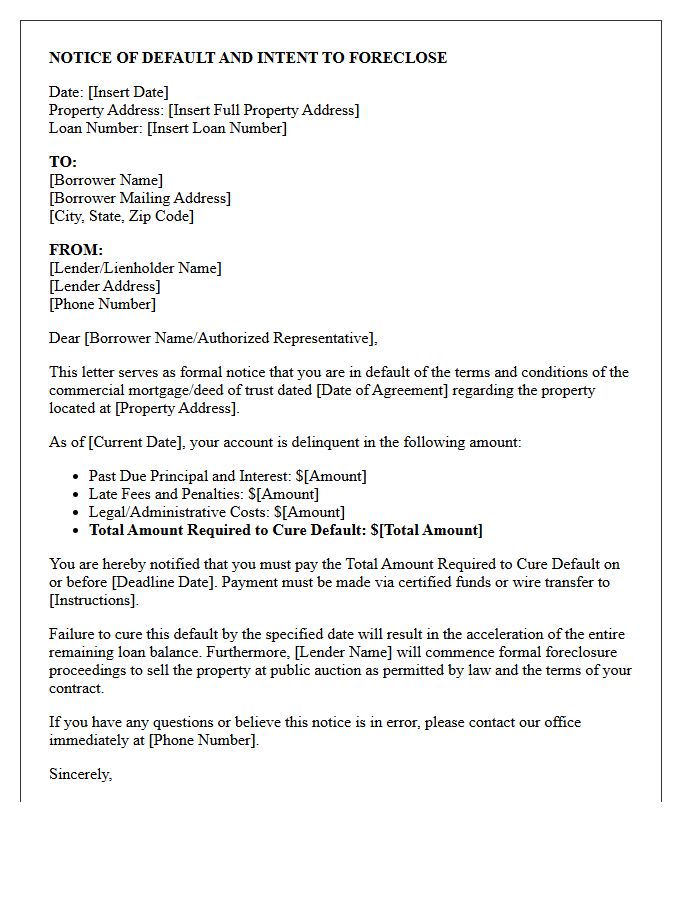

Commercial Property Foreclosure Letter

Receiving a commercial property foreclosure letter signifies that a lender has initiated legal action due to a mortgage default. This formal notice, often called a Notice of Default, indicates that your property is at risk of being seized and sold at auction. To protect your investment, you must act quickly to explore loss mitigation options, such as loan modification, refinancing, or a deed in lieu of foreclosure. Reviewing the specific cure period deadlines listed in the document is essential to preventing a permanent loss of title and equity.

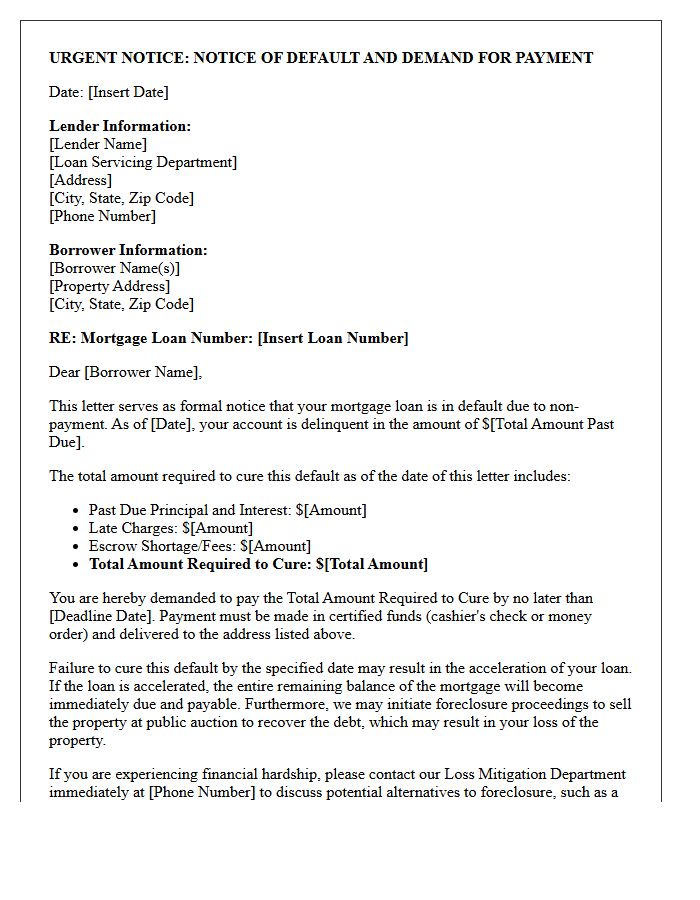

Residential Mortgage Demand Letter

A Residential Mortgage Demand Letter is a formal legal notice sent by a lender when a borrower defaults on loan payments. This document serves as a final warning before the initiation of foreclosure proceedings. It specifies the exact amount required to cure the delinquency, including late fees and interest, and provides a strict deadline for payment. Understanding this letter is crucial for homeowners to take immediate action, such as seeking a loan modification or repayment plan, to protect their property rights and avoid losing their home through legal seizure.

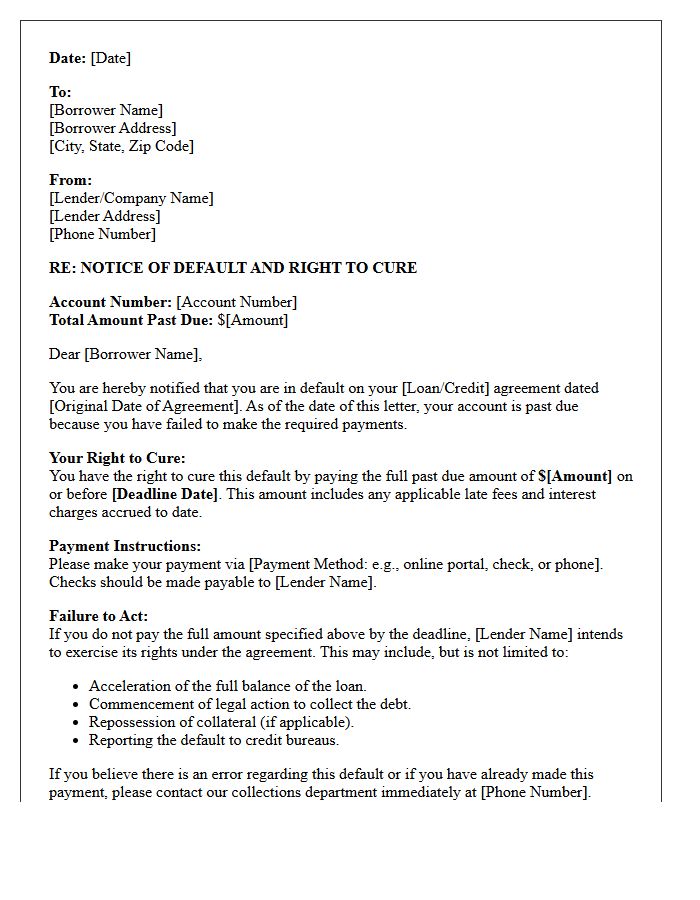

Right To Cure Account Default Letter

A Right to Cure notice is a formal legal document sent by lenders when a borrower defaults on a loan. It serves as a final opportunity to resolve past-due balances before the creditor initiates repossession or foreclosure. To exercise this right, the debtor must pay the full amount specified within a strict deadline, typically thirty days. Failure to act allows the lender to accelerate the debt and seize collateral. This mandatory notice ensures transparency and protects consumer rights by providing a clear pathway to reinstate the account and avoid legal action.

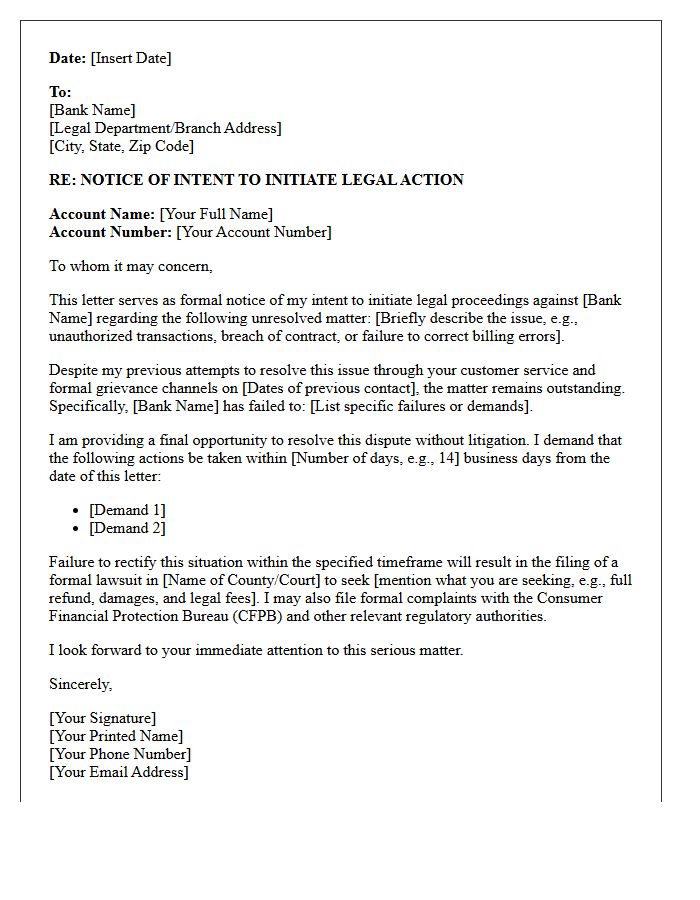

Bank Legal Action Intent Letter

A Bank Legal Action Intent Letter is a formal notice indicating that a financial institution plans to initiate litigation due to unresolved debt. This document serves as a final warning, granting the debtor a specific timeframe to settle balances or arrange a payment plan. Receiving this letter is critical because it precedes aggressive measures like asset seizure or wage garnishment. Promptly contacting the bank or seeking legal advice is essential to prevent a lawsuit and mitigate long-term damage to your credit score and financial standing.

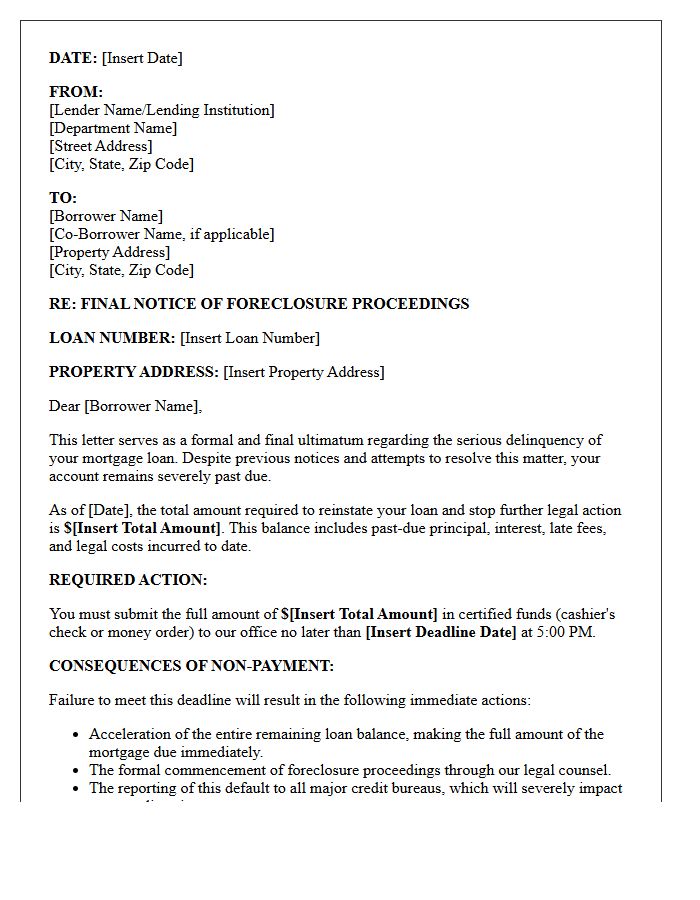

Final Foreclosure Ultimatum Letter

A Final Foreclosure Ultimatum Letter is a formal legal notice issued by a lender demanding immediate payment of the total mortgage arrears. This document serves as the final warning before the acceleration clause is triggered, meaning the entire loan balance becomes due. It outlines a strict deadline, usually 30 days, to cure the default. Receiving this letter signifies that judicial proceedings or an auction are imminent. To protect your property, you must prioritize loan reinstatement or contact your servicer to discuss loss mitigation options before the specified expiration date.

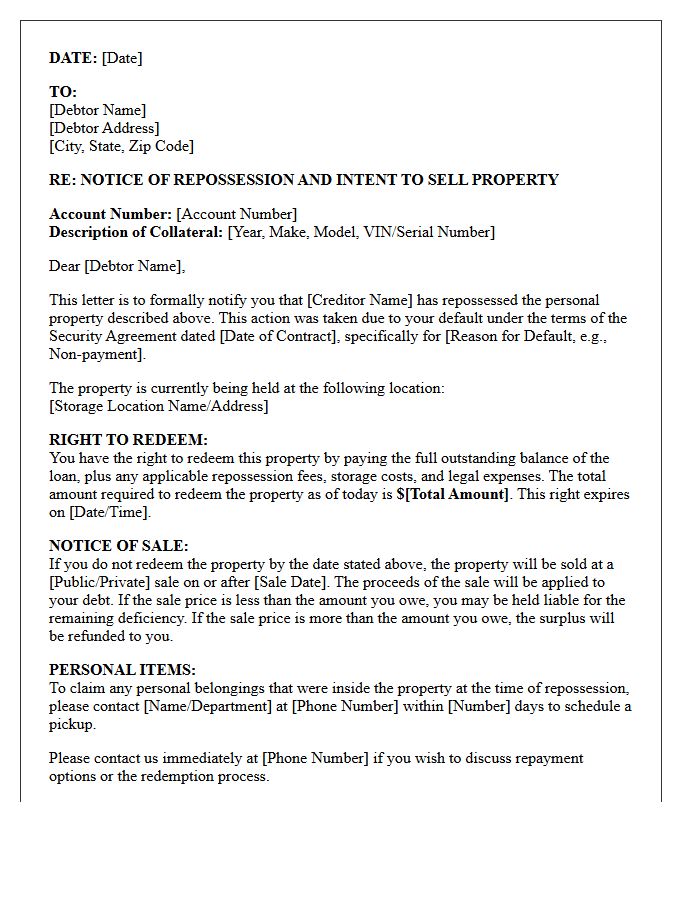

Secured Asset Repossession Letter

A Secured Asset Repossession Letter is a formal legal notice issued by a lender when a borrower defaults on a secured loan. It officially informs the debtor that the creditor intends to seize the collateral, such as a vehicle or property, to satisfy the outstanding debt. This document outlines the default cure period, providing a final opportunity to pay the arrears before the physical seizure occurs. Understanding your rights during this process is critical, as the letter must comply with specific state laws and consumer protection regulations to be legally valid.

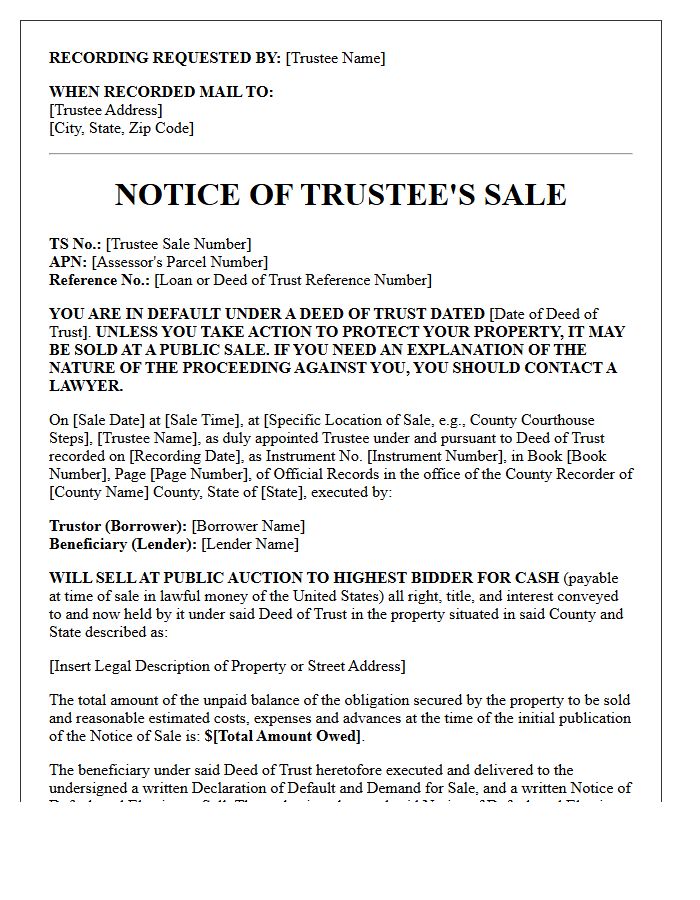

Notice Of Trustee Sale Letter

A Notice of Trustee Sale is a formal legal document signaling the final stage of the foreclosure process. It officially announces that a property will be sold at public auction on a specific date because the homeowner defaulted on their mortgage. This letter serves as a final warning, detailing the auction location and time. Receiving this notice means you have limited time to seek legal counsel, negotiate a loan modification, or pay the debt to prevent losing ownership of the home to the highest bidder.

What is a Notice of Default and Intent to Foreclose?

A Notice of Default (NOD) is a formal legal notification sent by a mortgage lender to a borrower stating that they have failed to make payments on time. It serves as the official first step in the foreclosure process, documenting the delinquency and providing a specific period for the borrower to resolve the debt before the property is seized.

What details are included in a Notice of Intent to Foreclose?

The notice typically includes the total amount of past-due payments, accumulated late fees, and legal costs required to bring the loan current. It also outlines the deadline for payment (reinstatement period), the lender's contact information, and a warning that failure to pay will result in the property being sold at a foreclosure auction.

How long do I have to respond after receiving a Notice of Default?

The timeline varies by state law, but borrowers generally have 30 to 90 days after receiving the notice to "cure the default" by paying the total arrears. If the debt is not settled or an agreement is not reached within this window, the lender can proceed to file a Notice of Sale or move toward a judicial foreclosure hearing.

Can I stop a foreclosure after receiving a Notice of Intent to Foreclose?

Yes, you can stop the process through several methods, including loan reinstatement (paying the full amount owed), a loan modification to change your monthly payments, a short sale, or a deed-in-lieu of foreclosure. Filing for bankruptcy also triggers an "automatic stay," which temporarily halts all foreclosure proceedings.

What is the difference between a Notice of Default and a Notice of Sale?

A Notice of Default is the initial warning that you are behind on payments and the foreclosure process has begun. A Notice of Sale is a subsequent legal document filed after the default period has expired, which announces the specific date, time, and location where the property will be auctioned to the highest bidder.

Comments