Experiencing unfair treatment from financial institutions requires a formal response to protect your rights. A Grievance Letter for Discriminatory Banking Practices serves as an official record of bias regarding loans, account closures, or service quality. This document ensures your complaint is documented for regulatory review and internal investigation. To help you take action, below are some ready to use template.

Image cover: Official Templates and Samples: Filing a Formal Grievance for Discriminatory Banking Practices

Letter Samples List

- Grievance Letter for Unfair Mortgage Loan Denial

- Grievance Letter Regarding Redlining Practices

- Grievance Letter for Discriminatory Account Closure

- Grievance Letter for Unequal Credit Card Limit Assignment

- Grievance Letter Regarding Biased Customer Service Treatment

- Grievance Letter for Discriminatory Interest Rate Manipulation

- Grievance Letter Regarding Age Discrimination in Lending

- Grievance Letter for Gender Bias in Small Business Loans

- Grievance Letter Regarding Racial Discrimination in Wealth Management

- Grievance Letter for Discriminatory Credit Scoring Practices

- Grievance Letter Regarding Accessibility Discrimination in Banking Services

- Grievance Letter for Unjustifiable High Fees Based on Demographics

- Grievance Letter Regarding Marital Status Discrimination in Joint Accounts

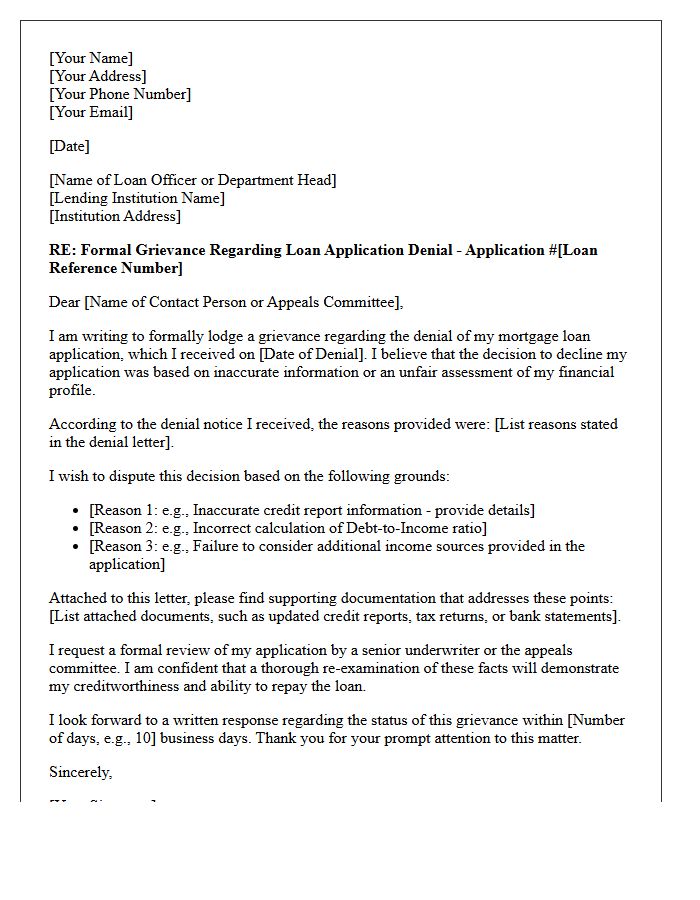

Grievance Letter for Unfair Mortgage Loan Denial

A formal grievance letter serves as a critical tool to challenge an unfair mortgage loan denial. To ensure effectiveness, clearly identify specific errors in the lender's assessment, such as incorrect income data or credit report discrepancies. Explicitly request a detailed explanation for the rejection under the Equal Credit Opportunity Act (ECOA) to ensure transparency. By documenting your legal rights and providing supporting evidence, you create a formal record for escalation to regulatory bodies, forcing the financial institution to re-evaluate your application with greater scrutiny and fairness.

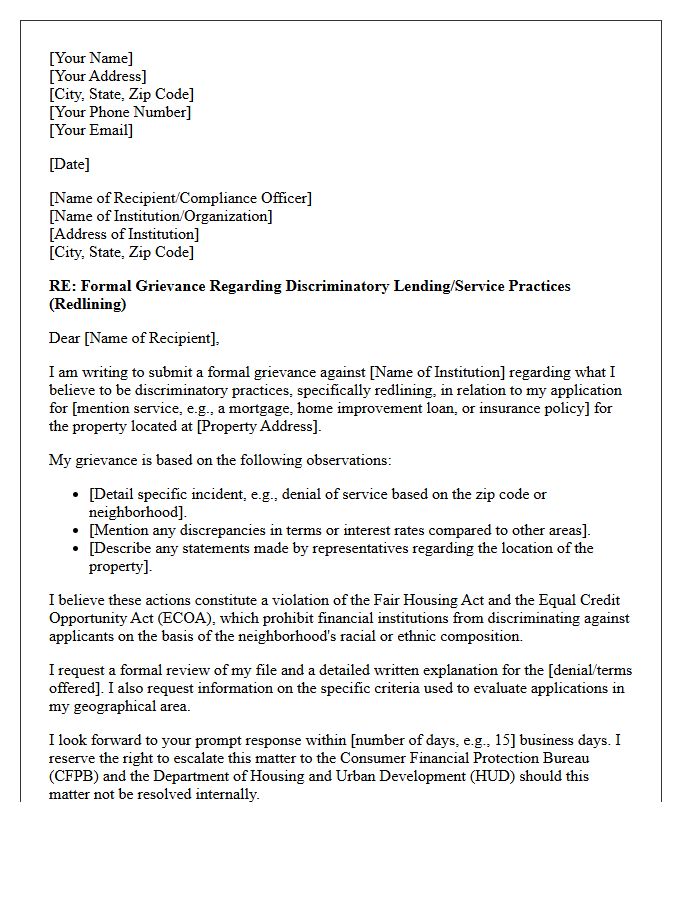

Grievance Letter Regarding Redlining Practices

A grievance letter regarding redlining practices is a formal complaint addressing systemic housing discrimination. It outlines how a financial institution or insurer denies services based on a neighborhood's racial or ethnic demographics rather than individual creditworthiness. To be effective, the letter must cite specific evidence of bias, reference the Fair Housing Act, and demand an immediate investigation. Documenting these discriminatory barriers is essential for protecting civil rights, ensuring equitable access to home loans, and holding predatory lenders accountable for maintaining illegal, exclusionary boundaries in the real estate market.

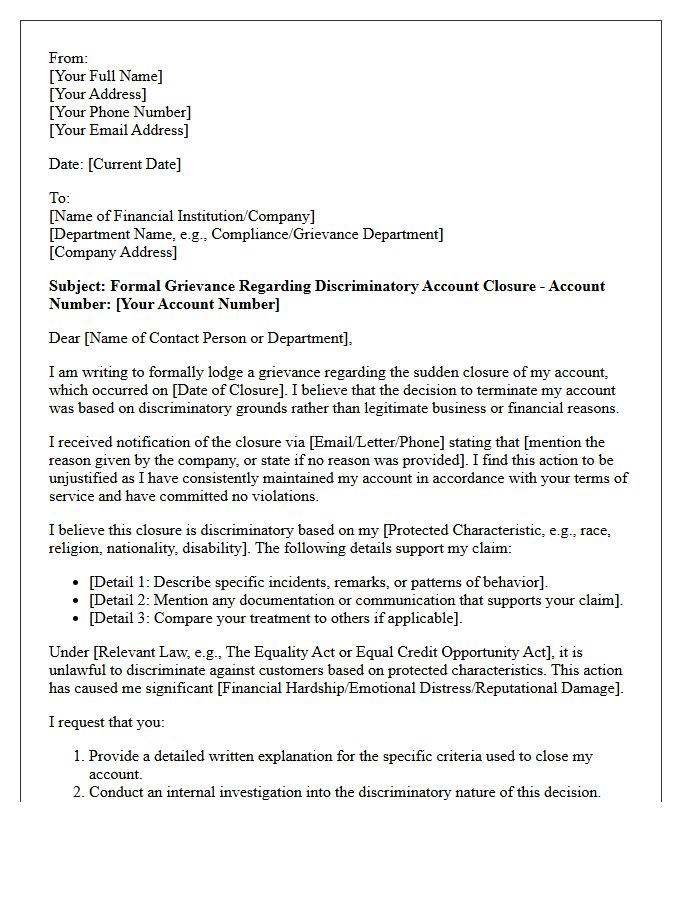

Grievance Letter for Discriminatory Account Closure

A grievance letter for discriminatory account closure must clearly state that the termination violated equality laws. You should provide a chronological timeline of events and request a detailed explanation for the sudden loss of service. Highlight if the action targeted a protected characteristic like race, religion, or disability. Formally demand an internal review or account reinstatement to resolve the dispute. Keeping copies of all communication is essential for potential legal recourse if the institution fails to provide a non-discriminatory justification for their decision.

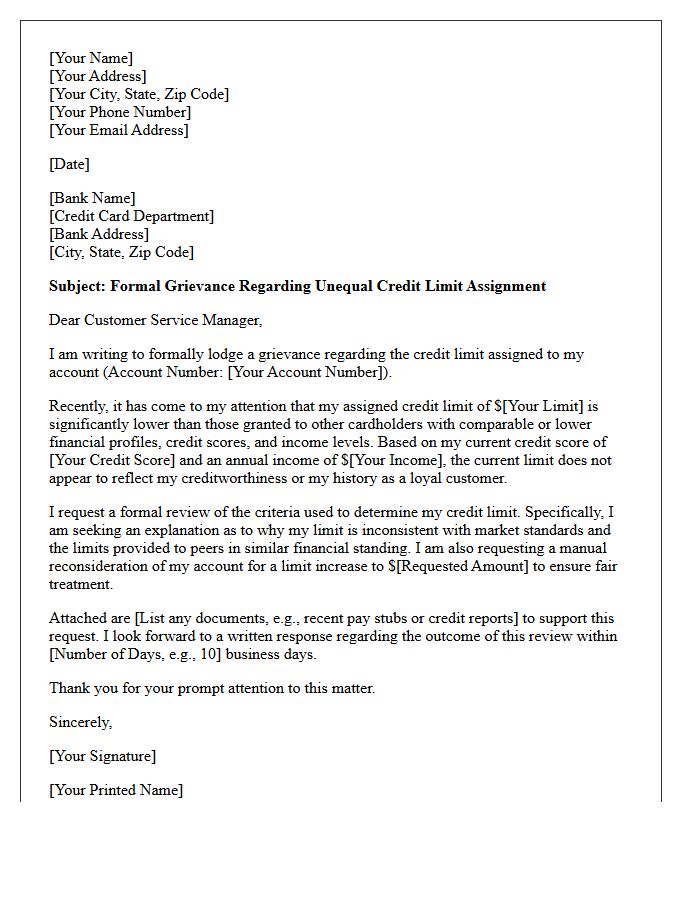

Grievance Letter for Unequal Credit Card Limit Assignment

When drafting a grievance letter for unequal credit card limit assignment, you must demand a clear explanation based on fair lending practices. Under regulations like the ECOA, lenders cannot discriminate based on protected characteristics. Clearly state your income, credit score, and financial history to demonstrate why your current limit is unjustified compared to peers. Formally requesting a manual secondary review ensures a human underwriter assesses your profile beyond automated algorithms. Documenting this discrepancy creates a paper trail essential for formal disputes or regulatory complaints regarding biased credit distribution.

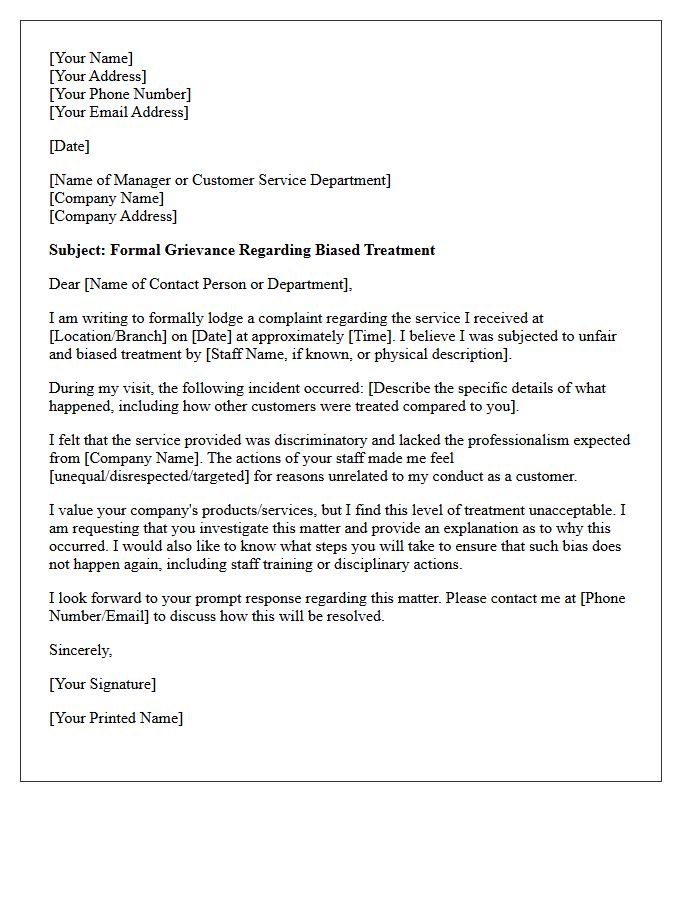

Grievance Letter Regarding Biased Customer Service Treatment

When drafting a grievance letter regarding biased customer service, it is essential to remain professional and objective. Clearly document the date, time, and specific details of the interaction, including the names of involved staff. Explicitly state how the treatment was discriminatory or inconsistent with company policy. Use a factual tone to describe the impact of the bias and clearly define your desired resolution. Providing evidence or witness accounts strengthens your claim, ensuring management addresses the systemic issue or individual misconduct to prevent future prejudice against other customers.

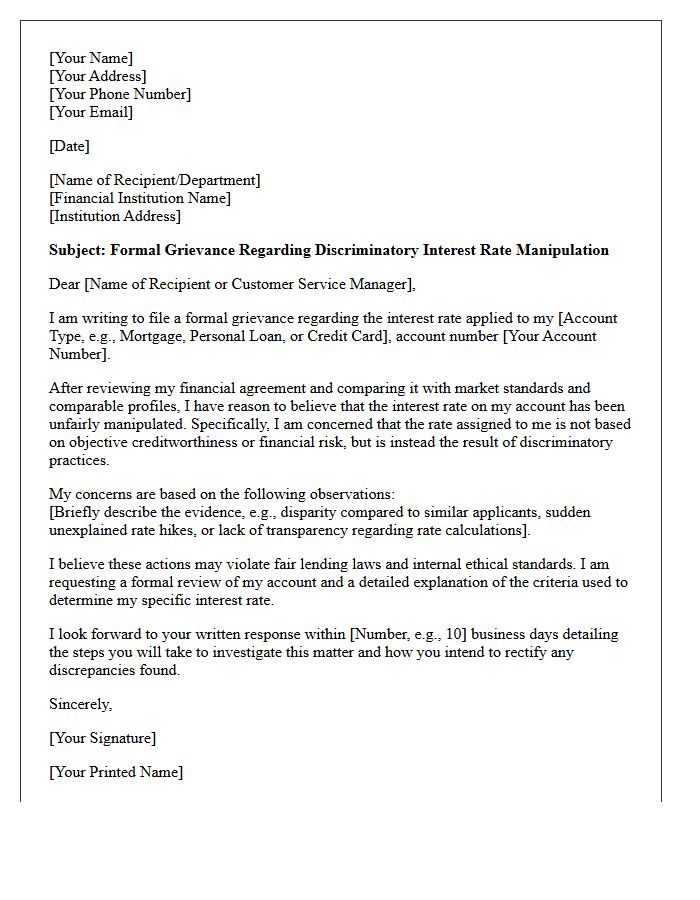

Grievance Letter for Discriminatory Interest Rate Manipulation

A grievance letter for discriminatory interest rate manipulation is a formal document used to challenge unfair lending practices based on protected characteristics like race or gender. When submitting this complaint, you must provide clear evidence of rate disparities compared to similar applicants. Explicitly state that the conduct violates fair lending laws, such as the Equal Credit Opportunity Act. Demand a detailed recalculation of terms and a formal written explanation to ensure legal accountability. Addressing these discrepancies promptly helps protect your financial rights and can lead to restitution or adjusted loan conditions.

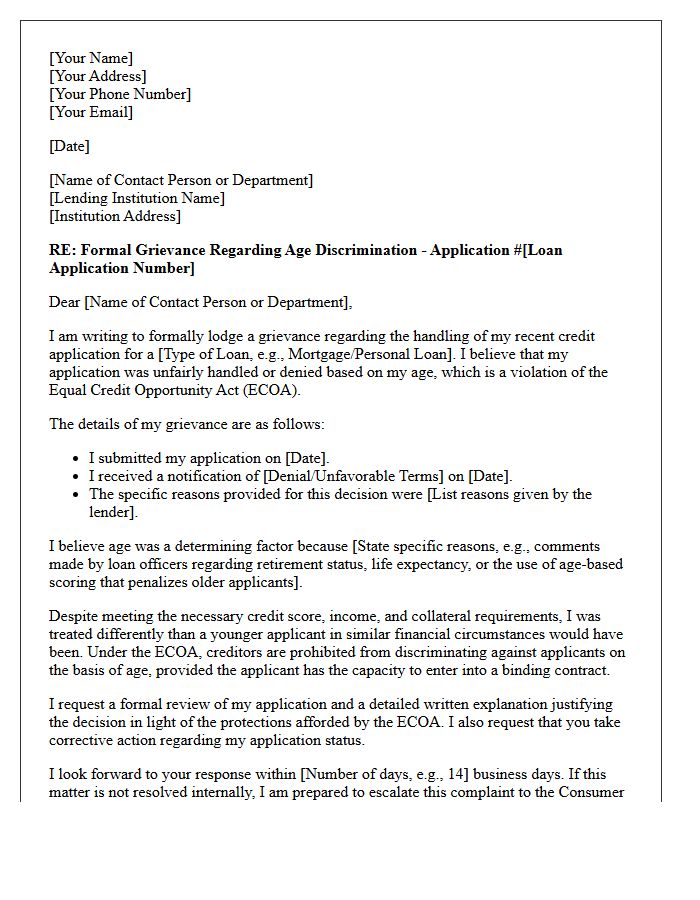

Grievance Letter Regarding Age Discrimination in Lending

A formal grievance letter regarding age discrimination in lending must clearly document instances where credit was unfairly denied or terms were altered based on age. It is essential to cite the Equal Credit Opportunity Act (ECOA), which prohibits lenders from discriminating against applicants because of their age, provided they have the legal capacity to contract. Your letter should include specific dates, names, and a detailed description of the adverse action taken. Requesting a written explanation and filing a report with the Consumer Financial Protection Bureau ensures your legal rights are protected and documented.

Grievance Letter for Gender Bias in Small Business Loans

A grievance letter regarding gender bias in small business loans serves as a formal dispute against discriminatory lending practices. When drafting this document, it is essential to provide specific evidence of unfair treatment compared to male applicants, such as disparate interest rates or unjustified denials. Clearly reference the Equal Credit Opportunity Act (ECOA) to strengthen your legal position. By maintaining a professional tone and outlining the financial impact on your company, you create a documented paper trail that is vital for internal reviews, regulatory complaints, or potential legal mediation.

Grievance Letter Regarding Racial Discrimination in Wealth Management

A formal grievance letter addressing racial discrimination in wealth management must clearly document specific incidents of unequal treatment, such as biased investment advice or predatory fee structures. It is essential to highlight how these actions violate anti-discrimination laws and internal corporate policies. To ensure legal weight, include dates, names, and evidence of disparate impact compared to other clients. This document serves as a critical foundation for potential legal recourse or regulatory complaints, demanding an immediate investigation into systemic bias to protect your financial interests and civil rights.

Grievance Letter for Discriminatory Credit Scoring Practices

A grievance letter for discriminatory credit scoring is a formal legal document used to challenge bias in automated lending algorithms. Under the Equal Credit Opportunity Act (ECOA), creditors must provide transparency and avoid penalizing applicants based on race, gender, or age. When drafting your complaint, explicitly state the suspected disparate impact and request a detailed explanation of the scoring criteria used. This written record is essential for escalating disputes to the Consumer Financial Protection Bureau (CFPB) to ensure fair financial treatment and hold institutions accountable for systemic biases.

Grievance Letter Regarding Accessibility Discrimination in Banking Services

A formal grievance letter is a vital legal tool for addressing accessibility discrimination in banking. It must clearly outline how specific barriers, such as inaccessible digital apps or physical obstacles, violate the Americans with Disabilities Act (ADA). Clearly state the reasonable accommodations required to ensure equal access to financial services. Send the document via certified mail to the bank's compliance officer to create an official paper trail. This formal notice protects your rights and serves as essential evidence if further legal action or a regulatory complaint becomes necessary.

Grievance Letter for Unjustifiable High Fees Based on Demographics

A grievance letter addressing unjustifiable high fees must clearly challenge discriminatory pricing based on demographics like race, gender, or location. This formal document should highlight price discrimination and request a transparent breakdown of charges to prove inconsistencies. It is essential to cite relevant consumer protection laws or equality acts to strengthen your claim. Providing comparative evidence of lower rates offered to other groups can demonstrate bias. State a firm deadline for a written response to ensure accountability and potential legal recourse if the unfair disparity remains unresolved.

Grievance Letter Regarding Marital Status Discrimination in Joint Accounts

When drafting a grievance letter regarding marital status discrimination in joint accounts, you must clearly state that a financial institution's denial or restriction based solely on your legal relationship status violates fair lending and equality laws. Explicitly reference relevant regulations, such as the Equal Credit Opportunity Act (ECOA), to demonstrate legal non-compliance. Detail how the policy unfairly excludes unmarried partners or treats them differently than spouses. Request a formal review and an immediate remedy to ensure equal access to banking services regardless of marital standing.

What should I include in a grievance letter for discriminatory banking practices?

A formal grievance letter should include your account details, a clear chronological description of the discriminatory incident, the names of involved staff members, the specific protected characteristic involved (such as race, gender, or disability), and a request for a formal investigation and resolution.

What are common examples of discriminatory banking practices?

Common examples include being unfairly denied a loan or credit card, receiving less favorable interest rates based on protected characteristics, experiencing hostile customer service, or facing unnecessary hurdles during account opening that are not applied to other demographic groups.

How do I prove discrimination in my banking grievance letter?

To prove discrimination, provide evidence of disparate treatment. This includes comparing your experience with banking policies, citing specific comments made by bank representatives, or highlighting instances where you were asked for documentation that is not standard for other applicants in similar financial positions.

To whom should I address a grievance letter regarding bank discrimination?

The letter should be addressed to the bank's Formal Complaints Department or the Chief Compliance Officer. If the bank has a dedicated Diversity and Inclusion or Fair Lending officer, you may also copy them on the correspondence to ensure the matter is handled by the appropriate internal authorities.

What can I do if the bank rejects my grievance letter regarding discrimination?

If the bank's internal response is unsatisfactory, you can escalate your claim by filing a formal complaint with government regulatory bodies, such as the Consumer Financial Protection Bureau (CFPB), or seek legal counsel to pursue a claim under the Equal Credit Opportunity Act (ECOA).

Comments