A Demand for Payment Under Standby Letter of Credit is a formal request triggered when a beneficiary seeks payment due to a contractual default. This legal document must strictly comply with the terms specified in the original credit agreement to ensure successful fund transfer by the issuing bank. To simplify your documentation process, below are some ready to use templates.

Image cover: Effective Demand for Payment Templates for Standby Letters of Credit

Letter Samples List

- Demand Letter for Payment Under Standby Letter of Credit

- Beneficiary Demand Letter for Standby Letter of Credit Drawdown

- Notice of Default and Demand Letter Under Standby Letter of Credit

- Formal Presentation Letter for Standby Letter of Credit Payment

- Sight Draft and Demand Letter Under Standby Letter of Credit

- Commercial Default Demand Letter for Standby Letter of Credit

- Non-Performance Demand Letter Against Standby Letter of Credit

- Financial Guarantee Demand Letter Under Standby Letter of Credit

- Issuing Bank Presentation Letter for Standby Letter of Credit Demand

- Corporate Beneficiary Demand Letter for Standby Letter of Credit Claim

- Final Notice and Demand Letter Under Standby Letter of Credit

- Standby Letter of Credit Draw Request and Demand Letter

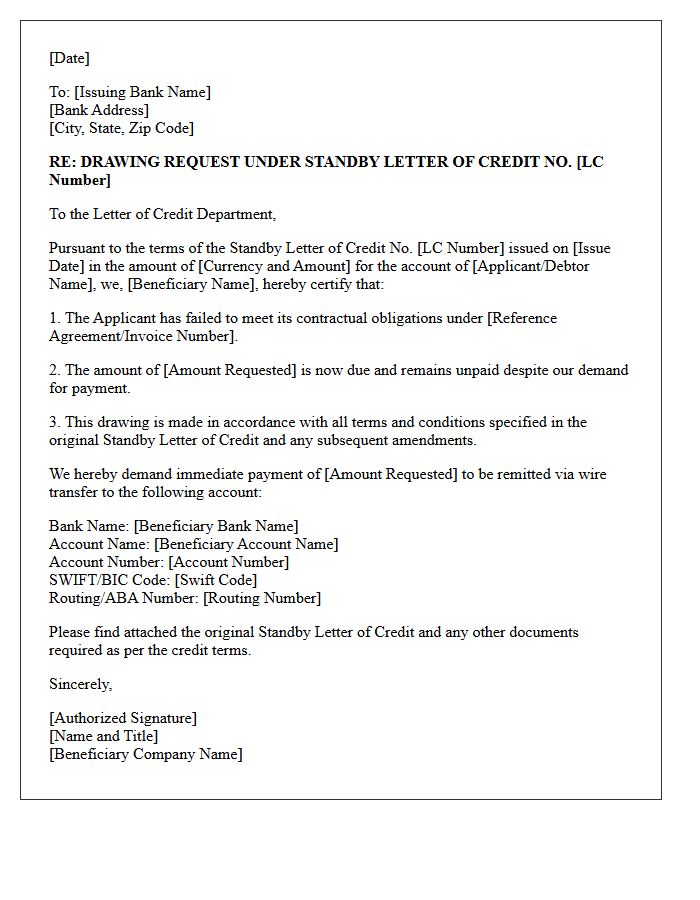

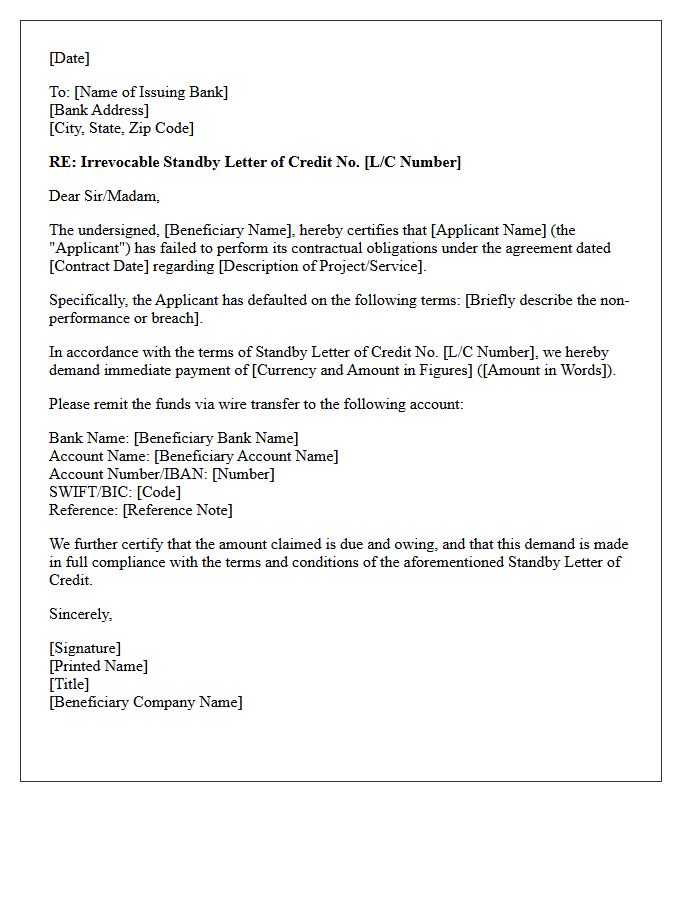

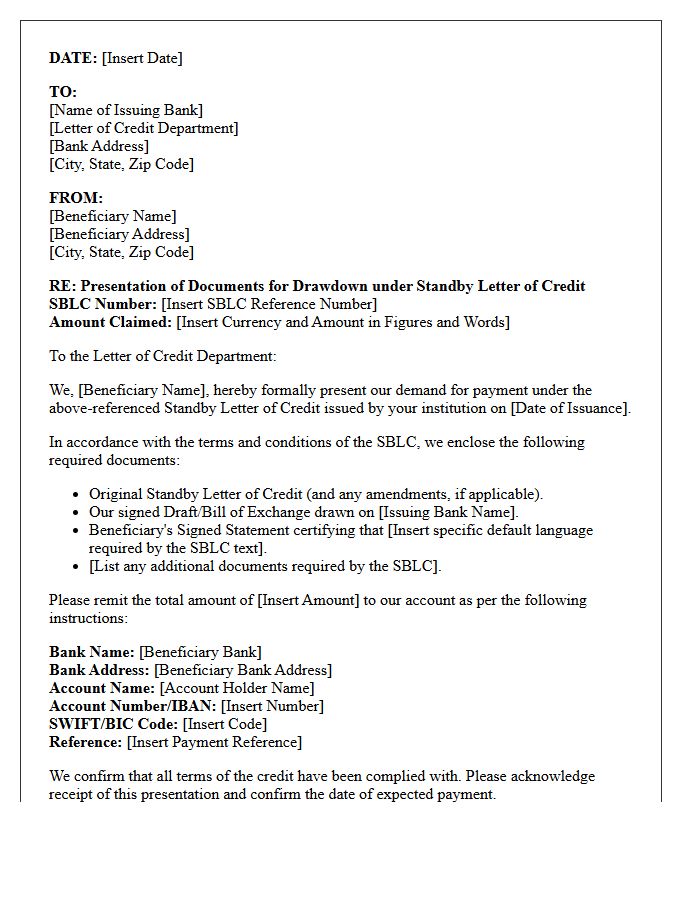

Demand Letter for Payment Under Standby Letter of Credit

To initiate a draw, a beneficiary must submit a formal Demand Letter for Payment to the issuing bank. This document must strictly comply with all terms specified in the Standby Letter of Credit (SBLC). Even minor discrepancies in wording or documentation can lead to rejection. The letter typically includes a statement certifying that the applicant has defaulted on their underlying contractual obligations. Ensuring strict compliance with dates, amounts, and presentation methods is essential to guarantee the bank honors the payment obligation under international banking standards like UCP 600 or ISP98.

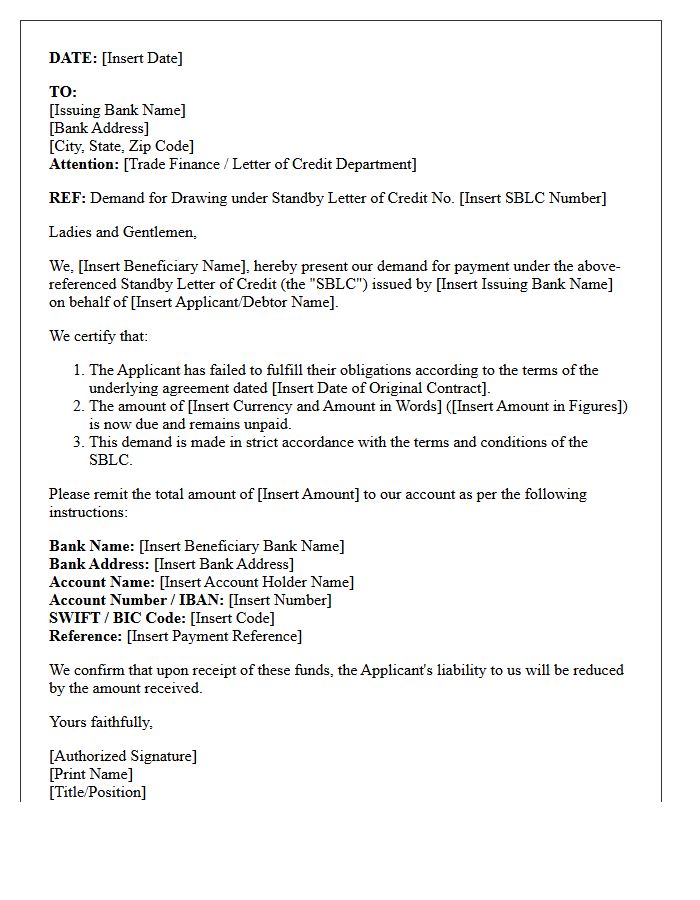

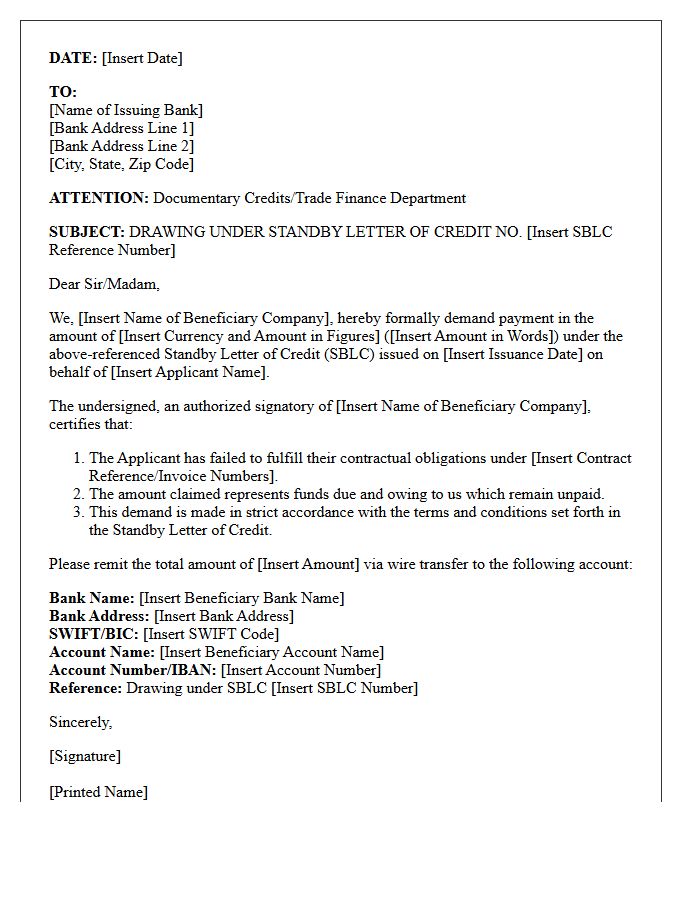

Beneficiary Demand Letter for Standby Letter of Credit Drawdown

A beneficiary demand letter is the formal legal request required to initiate a Standby Letter of Credit drawdown. To ensure payment, the document must strictly adhere to all terms specified in the original credit instrument. The principle of strict compliance dictates that even minor clerical errors can lead to a bank's rejection. Key components include a specific statement of default, the required draw amount, and valid banking instructions. This letter serves as the trigger mechanism that transforms a financial guarantee into immediate liquidity when contractual obligations are not met.

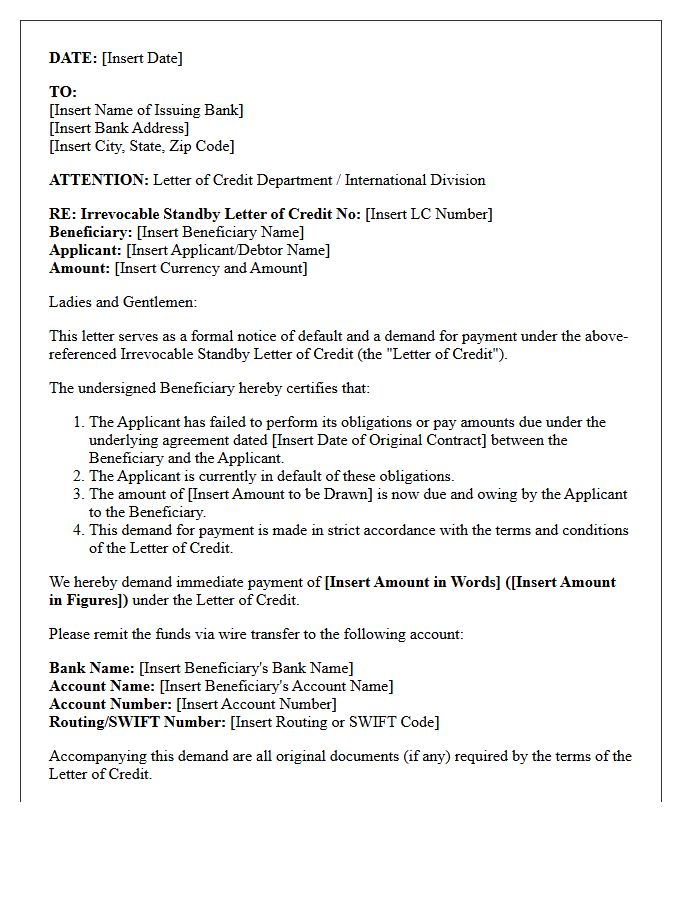

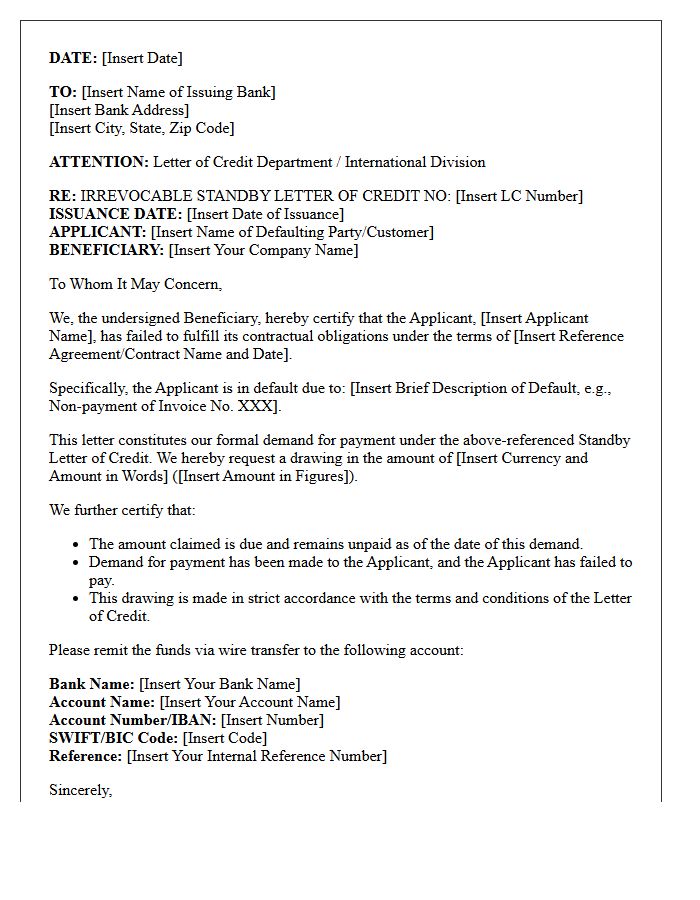

Notice of Default and Demand Letter Under Standby Letter of Credit

A Notice of Default and Demand Letter is a formal legal document required to trigger payment under a Standby Letter of Credit (SBLC). It serves as official certification that the applicant has failed to meet their contractual obligations. Beneficiaries must strictly adhere to the presentation period and specific wording mandates outlined in the original credit terms. Any minor discrepancy in documentation can lead to a bank rejection. This demand acts as the final enforcement mechanism to secure guaranteed funds when a underlying transaction fails.

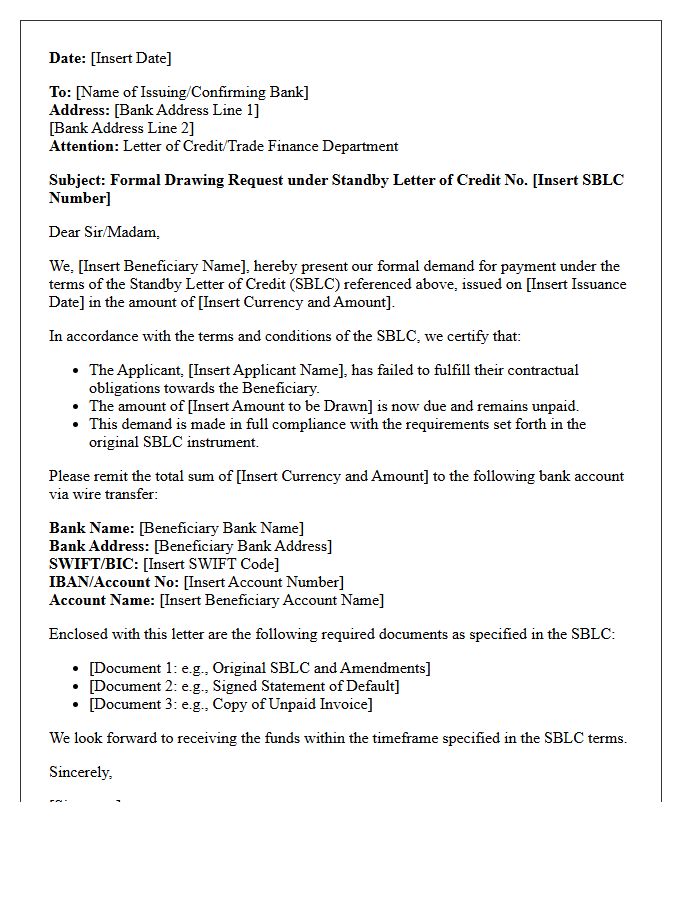

Formal Presentation Letter for Standby Letter of Credit Payment

A formal presentation letter is a mandatory demand document required to trigger payment under a Standby Letter of Credit (SBLC). It must strictly adhere to the uniform customs and practice (UCP 600) guidelines. This letter serves as a legal certification that the applicant has failed to meet their contractual obligations. To ensure a successful draw, the beneficiary must guarantee that all information, including dates and amounts, matches the credit terms exactly. Any discrepancy in wording can lead to immediate rejection by the issuing bank, delaying essential fund transfers.

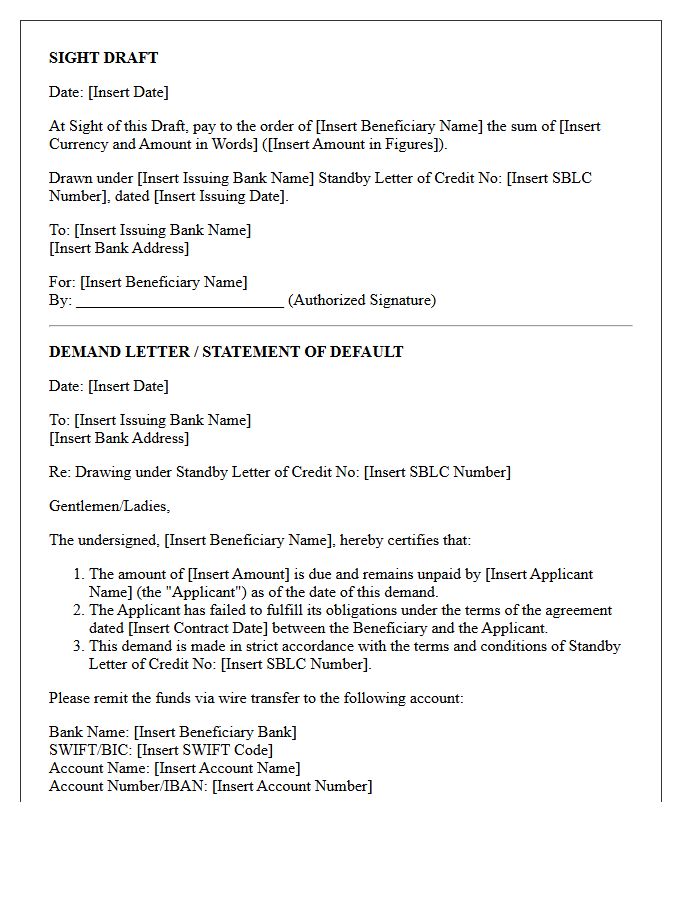

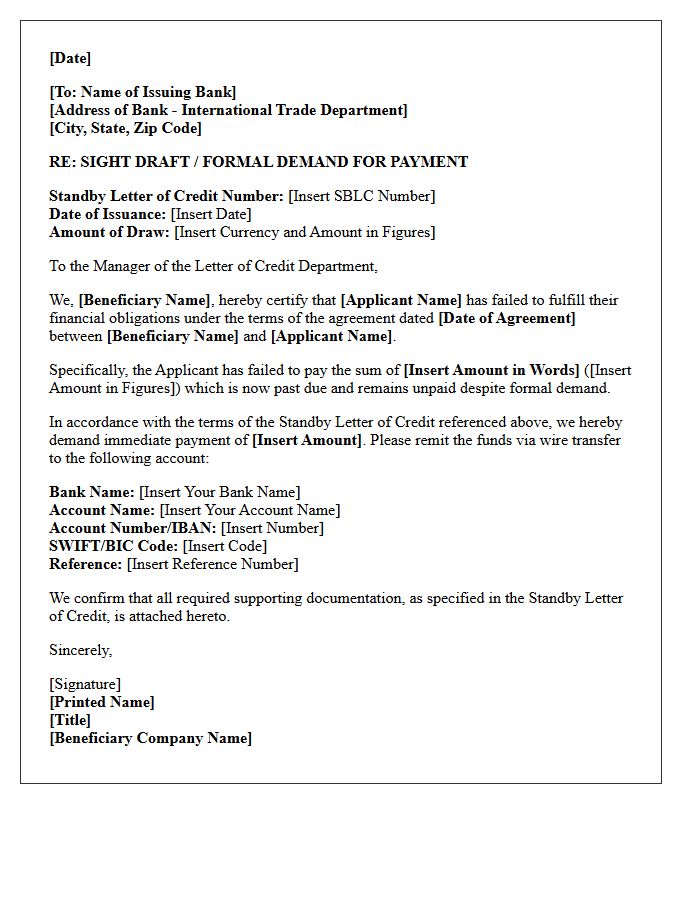

Sight Draft and Demand Letter Under Standby Letter of Credit

A Sight Draft is a formal payment instrument used to demand immediate funds under a Standby Letter of Credit (SBLC). Unlike deferred payments, it requires the issuing bank to pay "at sight" once compliant documents are presented. This process typically requires a formal Demand Letter, which serves as a certified statement confirming the applicant has defaulted on their obligations. Together, these documents trigger the financial guarantee, ensuring the beneficiary receives payment promptly. Understanding the strict compliance rules of the International Standby Practices (ISP98) is essential for successful execution.

Commercial Default Demand Letter for Standby Letter of Credit

A Commercial Default Demand Letter is a formal legal document required to trigger payment under a Standby Letter of Credit (SBLC). It serves as a certified statement confirming that the applicant has failed to meet their contractual obligations. To ensure successful liquidity, the letter must strictly adhere to the exact wording and documentary requirements specified in the credit agreement. Any discrepancy in the presentation can lead to a bank's refusal to honor the draw, making precise compliance essential for securing owed funds during a default.

Non-Performance Demand Letter Against Standby Letter of Credit

A Non-Performance Demand Letter is the formal legal mechanism used to trigger payment under a Standby Letter of Credit (SBLC). It serves as a certified statement confirming the applicant failed to meet their contractual obligations. To ensure successful liquidation, the beneficiary must strictly adhere to the exact wording and documentary requirements specified in the credit. Precise alignment with the issuer's terms is vital, as any minor clerical discrepancy can lead to a rejection of the claim and a delay in receiving guaranteed funds.

Financial Guarantee Demand Letter Under Standby Letter of Credit

A financial guarantee demand letter is a formal legal instrument used to activate payment under a Standby Letter of Credit (SBLC). It serves as an official certification that the applicant has defaulted on their contractual obligations. To be valid, the beneficiary must ensure the presentation of documents strictly complies with the specific terms outlined in the credit agreement. Any discrepancy in wording or formatting can lead to immediate rejection by the issuing bank. This document acts as the primary trigger to secure guaranteed funds when a counterparty fails to perform or pay.

Issuing Bank Presentation Letter for Standby Letter of Credit Demand

An Issuing Bank Presentation Letter is a formal document used to demand payment under a Standby Letter of Credit. It serves as the official certification that the beneficiary has met all required conditions. The letter must strictly adhere to the beneficiary's statement requirements specified in the original credit. Precise alignment with the UCP 600 or ISP98 rules is essential to ensure the issuing bank honors the draw. Any clerical discrepancy between the presentation letter and the credit terms can lead to a valid rejection of the payment demand.

Corporate Beneficiary Demand Letter for Standby Letter of Credit Claim

A corporate beneficiary demand letter is a formal legal notification used to trigger payment under a Standby Letter of Credit (SBLC). To ensure a successful claim, the beneficiary must provide strict compliance with all terms specified in the original credit instrument. The letter must explicitly state that the applicant has defaulted on their contractual obligations. Accuracy in documentation, including specific reference numbers and precise monetary amounts, is vital to prevent bank rejection. This document serves as the final mechanism to secure guaranteed funds when a business partner fails to perform or pay.

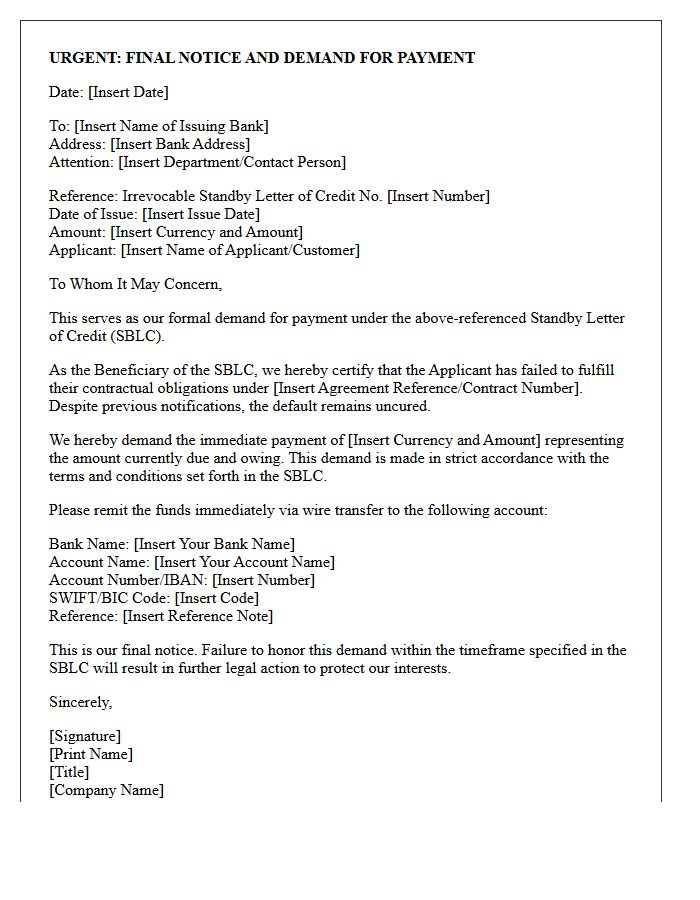

Final Notice and Demand Letter Under Standby Letter of Credit

A Final Notice and Demand Letter is a formal legal instrument required to trigger payment under a Standby Letter of Credit (SBLC). It serves as official notification that the applicant has defaulted on their contractual obligations. Beneficiaries must strictly adhere to the specific wording and presentation requirements dictated by the issuing bank to avoid discrepancies. Ensuring the demand is submitted before the expiry date is critical, as any non-compliance can result in a rejection of the claim and loss of financial security.

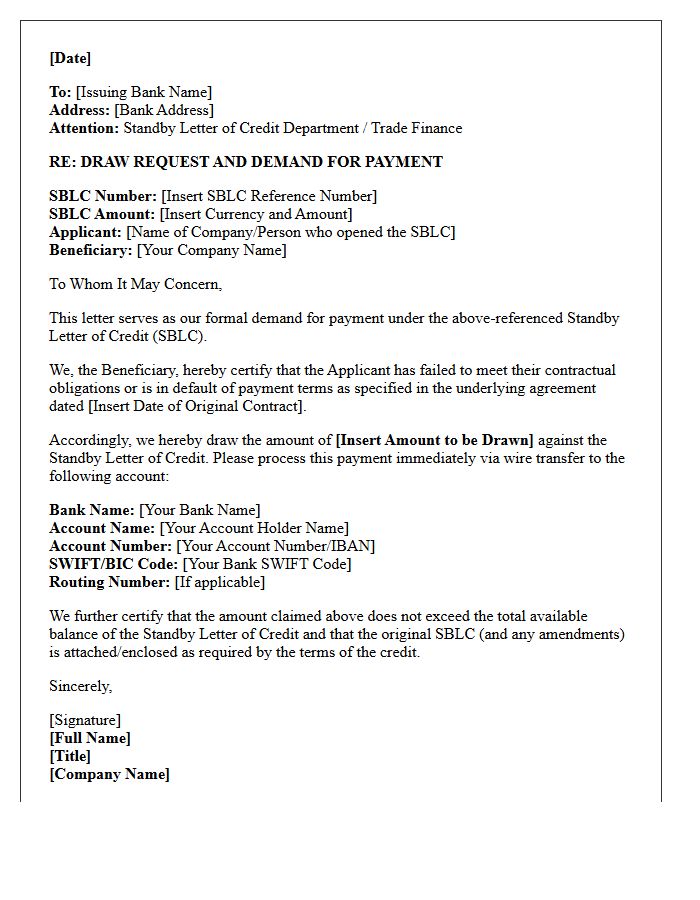

Standby Letter of Credit Draw Request and Demand Letter

A Standby Letter of Credit (SBLC) draw request is a formal demand for payment triggered when a secondary obligation is not met. To initiate the process, the beneficiary must submit a demand letter strictly complying with the specific terms outlined in the credit instrument. This document serves as legal certification that the applicant has defaulted on their contractual duties. Banks operate under the principle of strict compliance; therefore, any discrepancy in the presentation of documents can lead to an immediate rejection of the claim and non-payment.

What is a Demand for Payment under a Standby Letter of Credit (SBLC)?

A Demand for Payment is a formal written request submitted by the beneficiary to the issuing bank, asserting that the applicant has failed to meet their contractual obligations. This document triggers the bank's obligation to pay the specified amount under the terms of the Standby Letter of Credit.

What documents are typically required to make a Demand for Payment?

Requirements vary based on the SBLC terms, but typically include a signed statement of default, a formal draft (bill of exchange), and any specific third-party documents or certifications mandated by the credit agreement to prove non-performance.

What is the "Principle of Strict Compliance" in SBLC demands?

Strict compliance means that the Demand for Payment and all supporting documents must exactly match the terms and conditions outlined in the SBLC. Even minor typographical errors or discrepancies can lead to a bank's refusal to honor the demand and release funds.

Can an issuing bank refuse a Demand for Payment under a Standby Letter of Credit?

Yes, a bank can refuse payment if the demand is presented after the expiry date, if the documents contain discrepancies, or if the demand exceeds the available credit balance. Under UCP 600 or ISP98 rules, the bank must provide a notice of dishonor detailing the specific reasons for refusal.

How long does a bank have to process a Demand for Payment?

Under international standards such as ISP98 or UCP 600, the issuing bank generally has a "reasonable time," typically not exceeding five to seven business days following the day of presentation, to examine the documents and determine whether to honor or dishonor the demand.

Comments