A Corporate Credit Facility Guarantee Letter is a formal commitment issued by a parent company or third party to ensure a borrower's debt obligations are met. This legal instrument enhances creditworthiness, mitigates lender risk, and secures favorable financing terms for business expansion. It outlines specific repayment responsibilities and liability limits. Below are some ready to use template.

Image cover: Comprehensive Guide and Samples for Corporate Credit Facility Guarantee Letters

Letter Samples List

- Corporate Guarantee Letter

- Standby Letter of Credit

- Unconditional Bank Guarantee Letter

- Letter of Comfort

- Letter of Undertaking

- Financial Guarantee Letter

- Parent Company Guarantee Letter

- Cross Corporate Guarantee Letter

- Letter of Indemnity

- Letter of Awareness

- Payment Guarantee Letter

- Performance Guarantee Letter

- Syndicated Facility Guarantee Letter

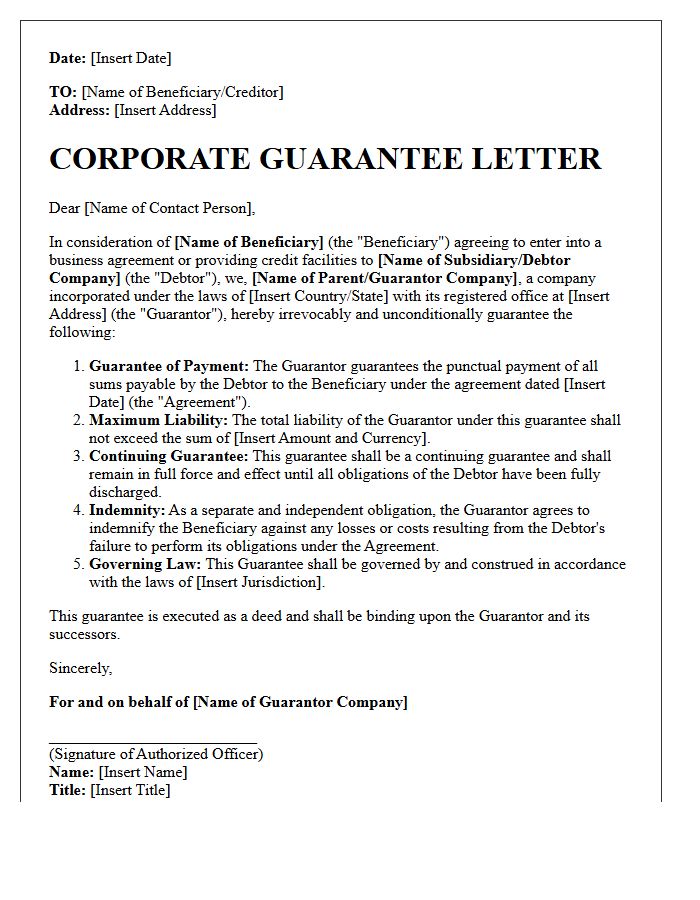

Corporate Guarantee Letter

A Corporate Guarantee Letter is a legally binding commitment where a parent company or third party assumes financial liability for a debtor's obligations. This document provides repayment assurance to lenders or suppliers, significantly reducing credit risk. By issuing this letter, the guarantor pledges its assets to satisfy debts if the primary borrower defaults. It is an essential tool for securing favorable credit terms and enhancing the credibility of subsidiaries during high-value commercial transactions or loan applications.

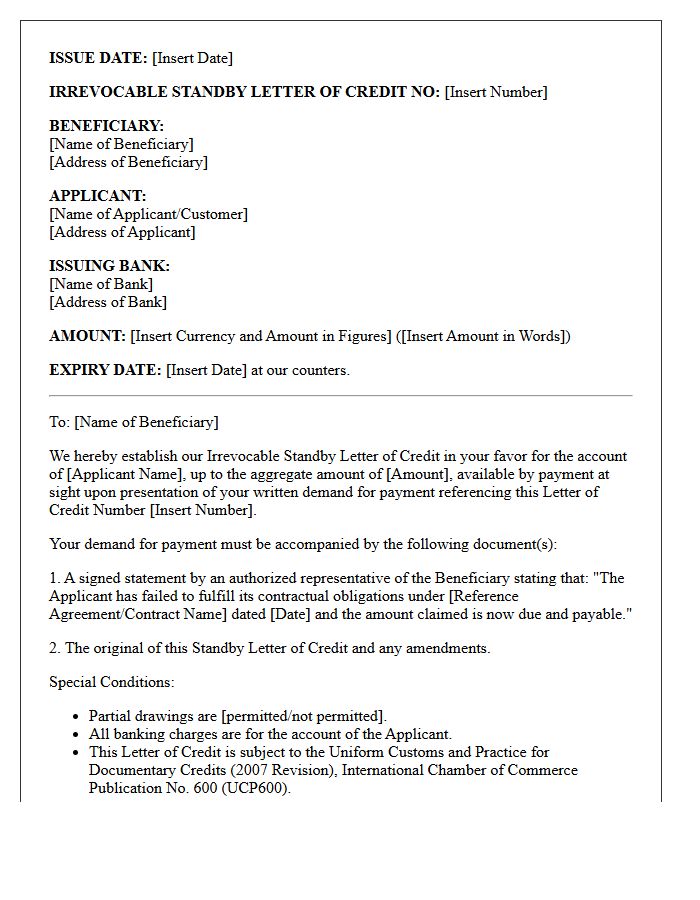

Standby Letter of Credit

A Standby Letter of Credit (SBLC) serves as a powerful legal instrument ensuring payment security in international commerce. It acts as a financial guarantee issued by a bank on behalf of a client, promising to pay the beneficiary if the applicant defaults on a contractual obligation. Unlike a standard letter of credit used for active trade, an SBLC is a secondary payment mechanism intended only as a safety net. It reduces risk for sellers by substituting the bank's creditworthiness for the buyer's, facilitating trust and enabling complex global business transactions.

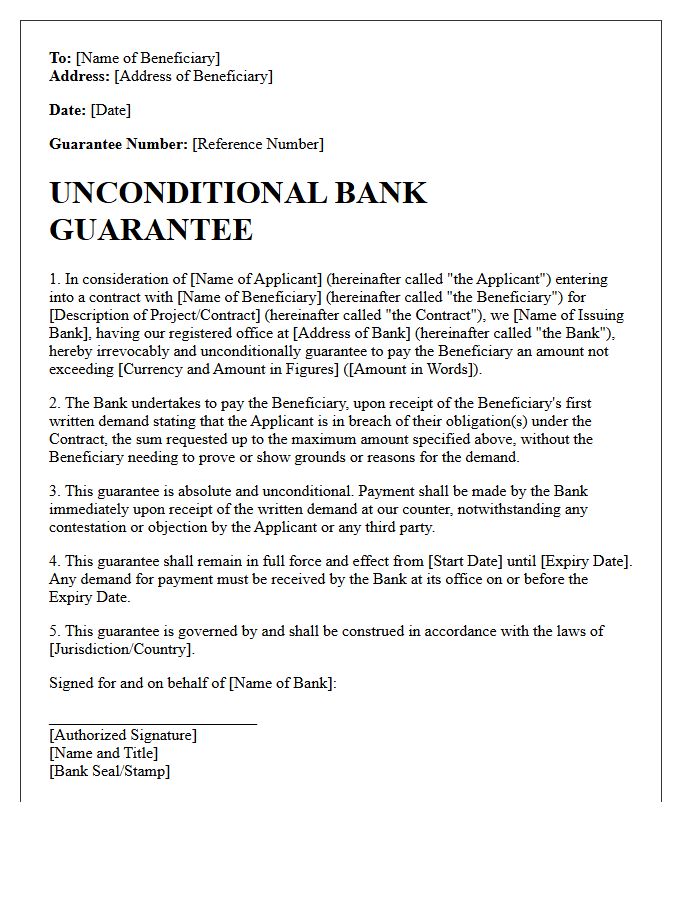

Unconditional Bank Guarantee Letter

An Unconditional Bank Guarantee Letter serves as a powerful financial instrument ensuring payment security. It represents an irrevocable commitment by a bank to pay a specific amount to a beneficiary upon first demand, without requiring proof of default or any conditions. This document minimizes risk in international trade and construction contracts by providing immediate liquidity. Because the bank must pay regardless of underlying contract disputes, it functions as a cash equivalent, making it essential for parties seeking absolute payment certainty and performance assurance in high-value commercial transactions.

Letter of Comfort

A Letter of Comfort is a document issued by a parent company to a lender, providing assurance regarding a subsidiary's ability to fulfill financial obligations. While it signals support, it typically lacks the legal enforceability of a formal guarantee, serving instead as a moral or psychological commitment. Investors and banks use these letters to assess creditworthiness and reduce perceived risk during lending processes. Understanding the specific language used is critical, as certain phrasing can inadvertently create binding legal liabilities depending on the jurisdiction and intent of the parties involved.

Letter of Undertaking

A Letter of Undertaking (LUT) is a formal assurance used primarily in international trade and taxation. It serves as a binding commitment where one party promises to fulfill specific obligations or cover potential liabilities to another. In India, exporters use an LUT under GST to ship goods or services without paying integrated tax upfront. This legal document streamlines cash flow by eliminating the need for tax refunds, provided the exporter adheres to the underlying statutory requirements and timelines specified by the governing authority.

Financial Guarantee Letter

A Financial Guarantee Letter is a formal document issued by a bank or sponsor to ensure that a person or entity can meet specific monetary obligations. It acts as a legal commitment to cover costs if the primary party defaults. This document is essential for visa applications, international student admissions, or commercial contracts to prove financial solvency. It must clearly state the total funds available, the duration of support, and the guarantor's contact details to provide credible assurance of payment to the recipient party.

Parent Company Guarantee Letter

A Parent Company Guarantee Letter is a legally binding commitment where a holding company ensures the contractual obligations of its subsidiary. This document mitigates risk for clients by providing financial recourse if the subsidiary fails to perform or becomes insolvent. It is essential for high-value projects, as it enhances creditworthiness and ensures project completion. By signing this guarantee, the parent entity assumes full liability for any defaults, offering a layer of security that protects the beneficiary against potential losses during business transactions or long-term infrastructure agreements.

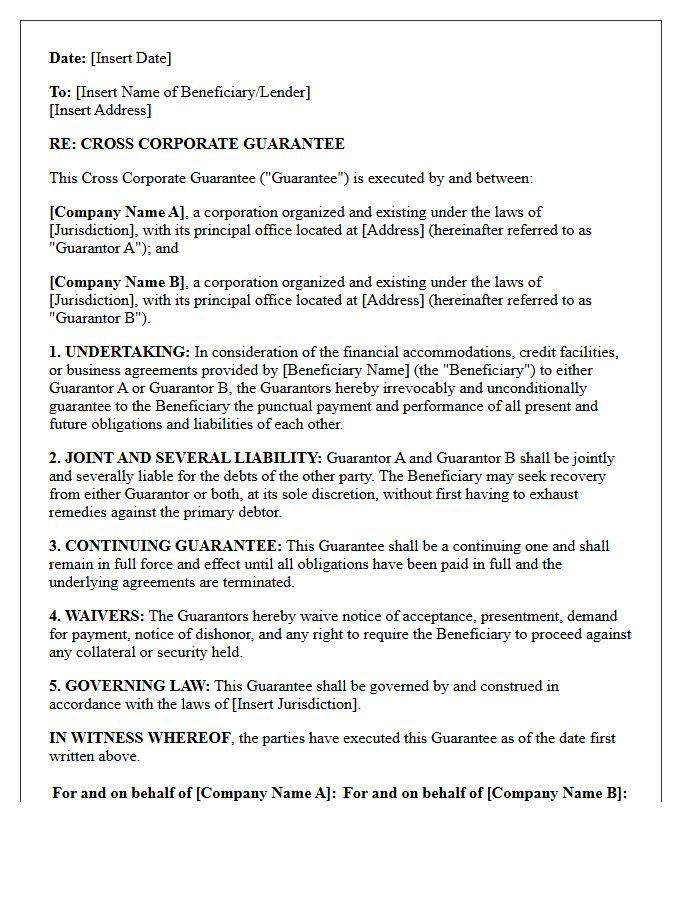

Cross Corporate Guarantee Letter

A Cross Corporate Guarantee Letter is a legally binding agreement where multiple entities within a business group guarantee each other's financial obligations. This document provides lenders with additional security by ensuring that if one subsidiary defaults, the parent company or sister affiliates are liable for the debt. It effectively consolidates the group's creditworthiness to secure better financing terms or higher loan amounts. However, it also increases financial risk, as a single entity's insolvency can trigger repayment demands across the entire corporate structure.

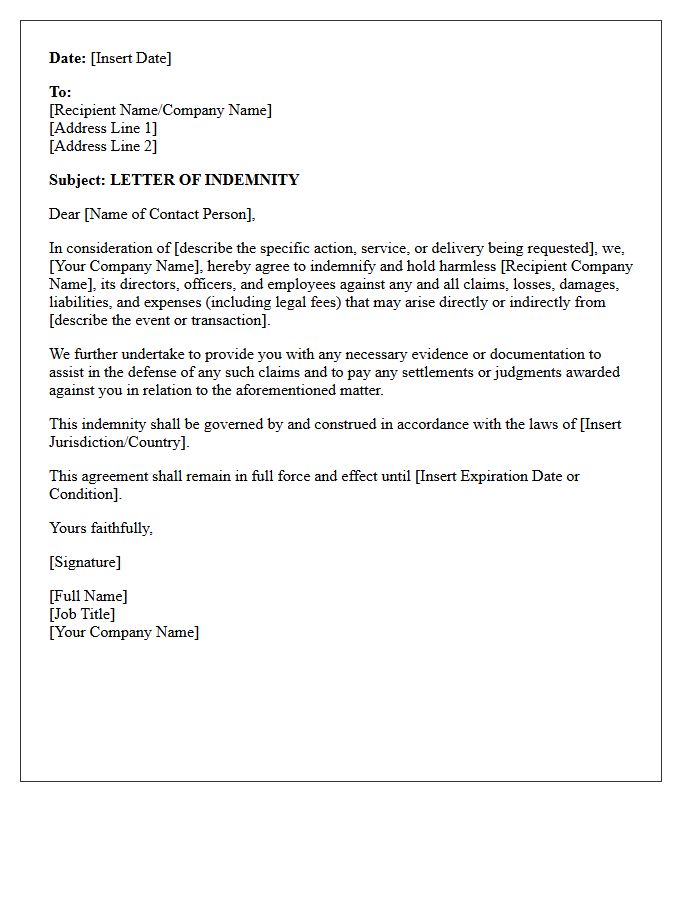

Letter of Indemnity

A Letter of Indemnity (LOI) is a contractual document where one party guarantees to compensate another for potential losses or damages. In shipping and trade, it is often used to facilitate the release of cargo without the presentation of original bills of lading. By signing an LOI, the requester assumes full financial legal responsibility, protecting the carrier from third-party claims. While essential for maintaining supply chain speed, it carries significant risk as it may void insurance coverage if the underlying action is deemed a breach of contract.

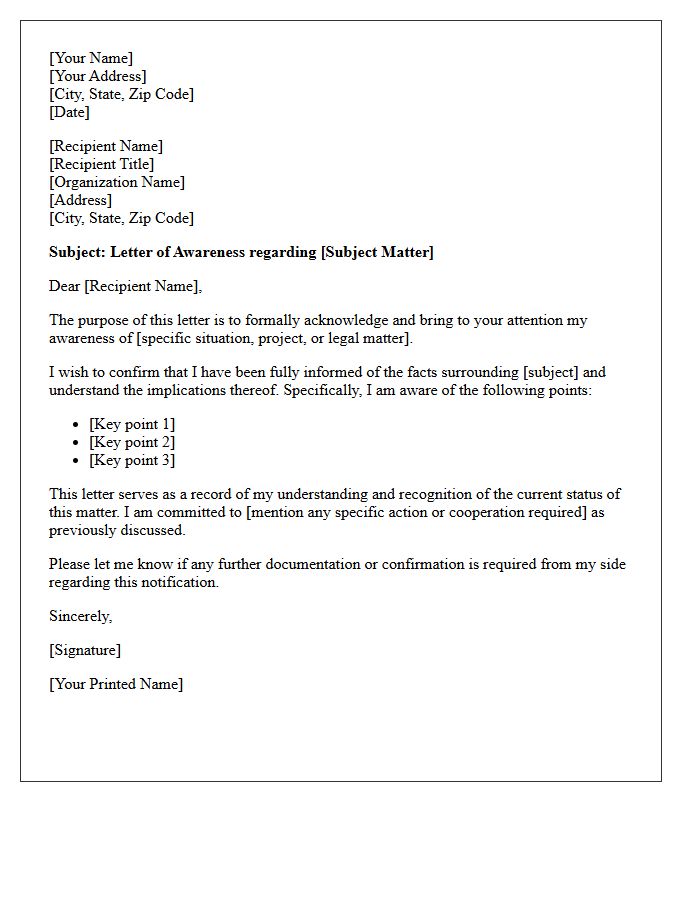

Letter of Awareness

A Letter of Awareness is a legal document issued by a parent company to a lender, acknowledging a subsidiary's loan obligation. While it signals moral support and confirms the parent's knowledge of the debt, it is typically non-binding and does not constitute a formal financial guarantee. Investors and creditors use these letters to assess the relationship between corporate entities, but must remain cautious as they provide limited legal recourse in the event of a default. Understanding its legal limitations is essential for effective risk management in corporate financing.

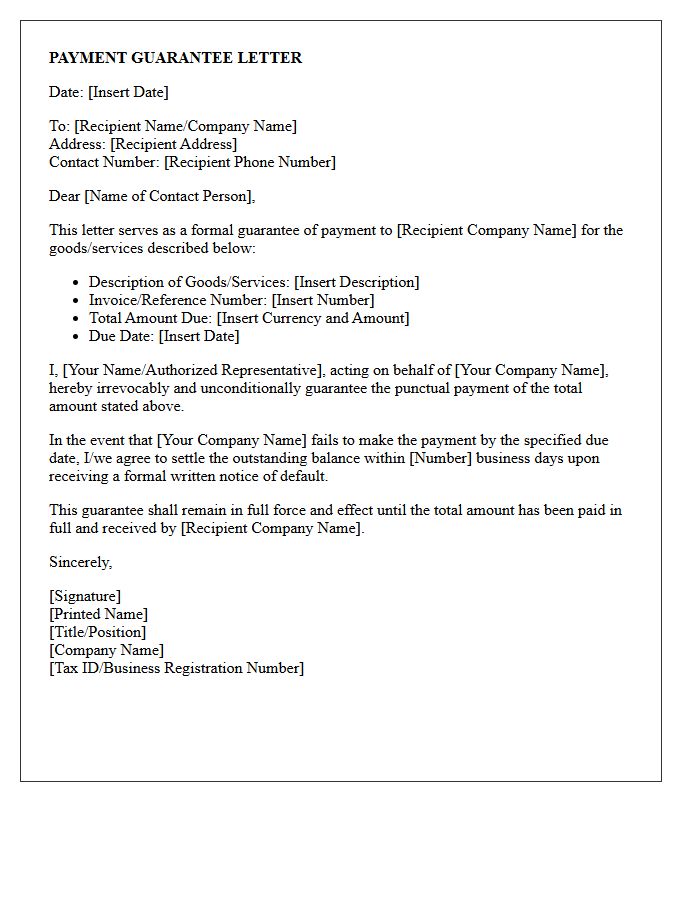

Payment Guarantee Letter

A Payment Guarantee Letter is a legally binding document issued by a bank or financial institution to ensure that a seller receives full payment for goods or services. It serves as a financial security instrument, protecting the beneficiary if the buyer defaults on their contractual obligations. By reducing credit risk in international trade and large commercial transactions, it builds trust between parties. Understanding the specific terms and conditions is essential, as the guarantor is obligated to pay the agreed sum upon a valid claim, ensuring business continuity and fiscal reliability.

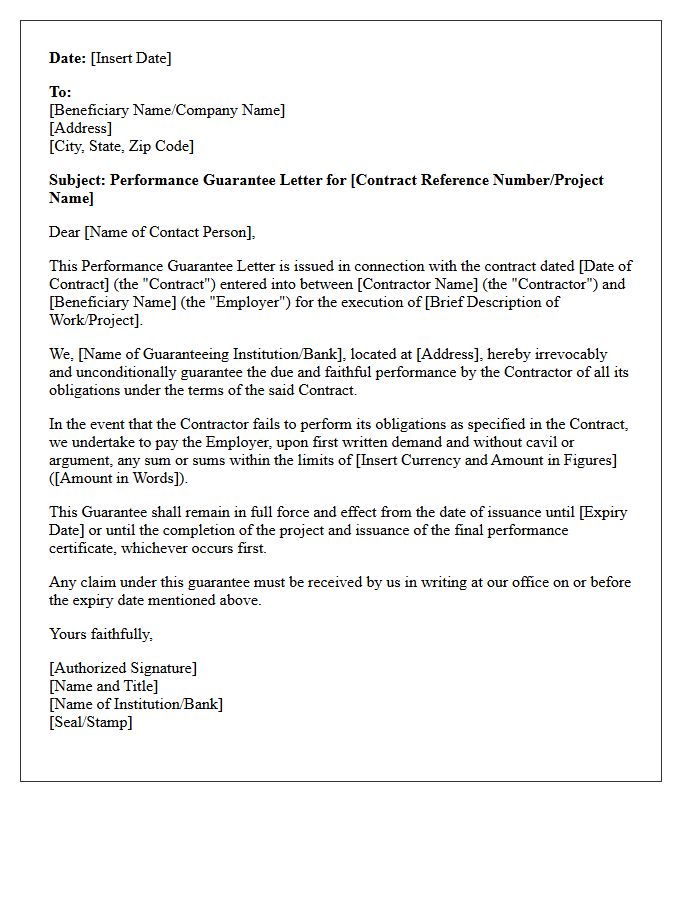

Performance Guarantee Letter

A Performance Guarantee Letter is a binding financial instrument issued by a bank to ensure a contractor fulfills their contractual obligations. It protects the client by providing monetary compensation if the agreed-upon project specifications or deadlines are not met. This document acts as a critical risk mitigation tool in construction and international trade, building trust between parties. If the supplier defaults, the beneficiary can claim the guarantee amount to cover resulting losses. Essentially, it serves as a security deposit that ensures professional accountability and project completion.

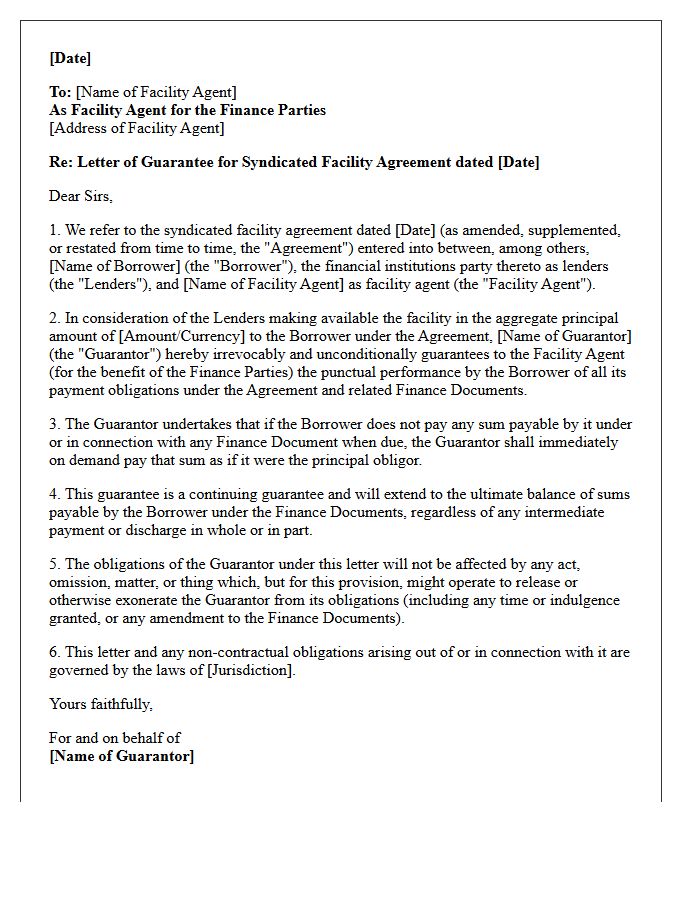

Syndicated Facility Guarantee Letter

A Syndicated Facility Guarantee Letter is a critical legal document where a guarantor provides a formal assurance to a group of lenders. It ensures that the borrower's financial obligations will be met in the event of a default. In large-scale corporate financing, this letter mitigates credit risk by backing the debt with additional collateral or third-party credit support. It establishes a direct legal link between the guarantor and the syndicate, ensuring repayment security across complex, multi-lender credit facilities and protecting the collective interests of all participating financial institutions.

What is a Corporate Credit Facility Guarantee Letter?

A Corporate Credit Facility Guarantee Letter is a legally binding document issued by a parent company or a third-party guarantor to a financial institution, promising to fulfill the debt obligations of a borrower if they default on their credit facility.

What are the primary components of a corporate guarantee for credit lines?

The essential elements include the identities of the guarantor, borrower, and lender, the maximum liability amount, the specific credit facility being covered, the duration of the guarantee, and the conditions under which the guarantee can be invoked.

What is the difference between a limited and an unlimited corporate guarantee?

A limited guarantee restricts the guarantor's liability to a specific dollar amount or a percentage of the debt, whereas an unlimited guarantee holds the guarantor responsible for the entire outstanding balance, including interest and legal fees, without a predefined cap.

How does a guarantee letter affect a corporation's financial statements?

While not always recorded as a direct liability on the balance sheet, a Corporate Credit Facility Guarantee Letter must typically be disclosed in the footnotes of financial statements as a contingent liability, as it represents a potential future financial obligation.

Can a Corporate Credit Facility Guarantee Letter be revoked?

Revocation is generally subject to the terms of the agreement; most guarantees are "continuing" and remain in effect until the underlying debt is fully repaid. However, a guarantor may sometimes terminate future liability by providing written notice, though they remain liable for debt incurred prior to the notice period.

Comments