A Deferred Payment Guarantee Letter is a formal commitment issued by a bank ensuring that a buyer's payment to a seller will be made at a specified future date. This instrument mitigates credit risk in international trade and long-term contracts by providing financial security to exporters. Explore our comprehensive guide to understand the legal requirements. Below are some ready to use template.

Image cover: Deferred Payment Guarantee: Formal Letter Samples and Professional Templates

Letter Samples List

- Application for Deferred Payment Guarantee Letter

- Approval of Deferred Payment Guarantee Letter

- Issuance of Deferred Payment Guarantee Letter

- Amendment to Deferred Payment Guarantee Letter

- Extension of Deferred Payment Guarantee Letter

- Cancellation of Deferred Payment Guarantee Letter

- Invocation of Deferred Payment Guarantee Letter

- Demand for Payment Under Deferred Payment Guarantee Letter

- Notice of Default Under Deferred Payment Guarantee Letter

- Rejection of Claim on Deferred Payment Guarantee Letter

- Discharge of Deferred Payment Guarantee Letter

- Counter Guarantee Letter for Deferred Payment

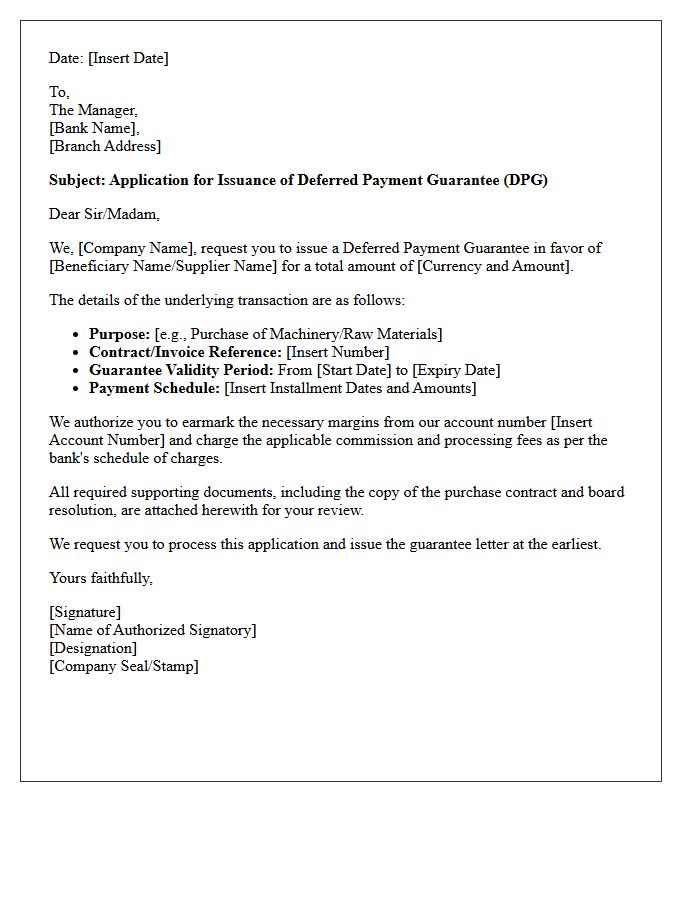

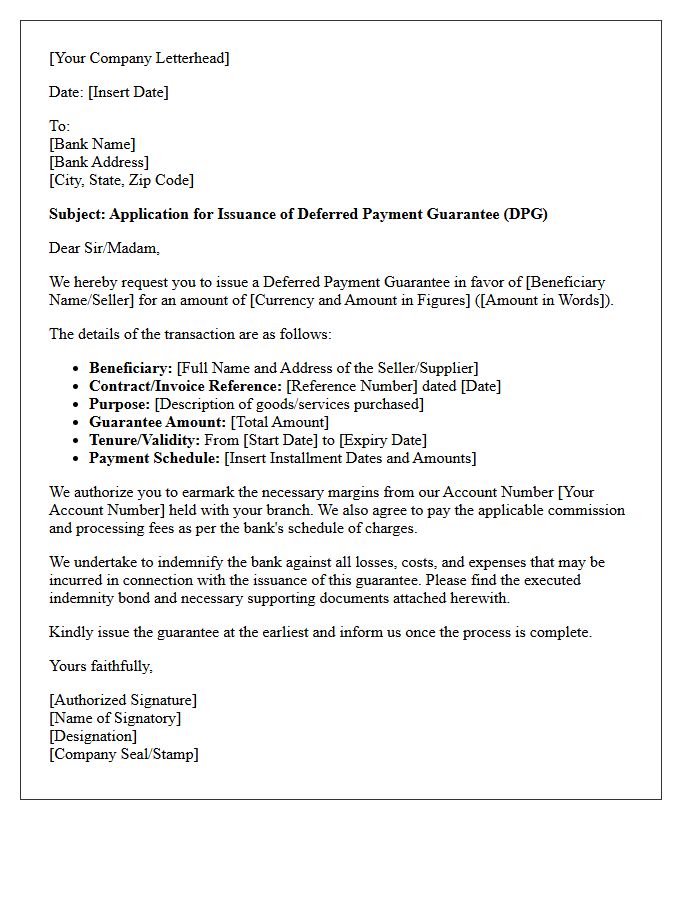

Application for Deferred Payment Guarantee Letter

An application for a Deferred Payment Guarantee Letter is a formal request to a bank to secure credit purchases. It ensures that the seller receives payment on a future date, even if the buyer defaults. Key requirements include a valid commercial contract, creditworthiness assessment, and specific collateral. This instrument facilitates trade finance by providing payment security to exporters while allowing importers to manage cash flow effectively. Applicants must clearly state the guarantee amount, expiry date, and governing law to ensure legal enforceability and smooth international transactions.

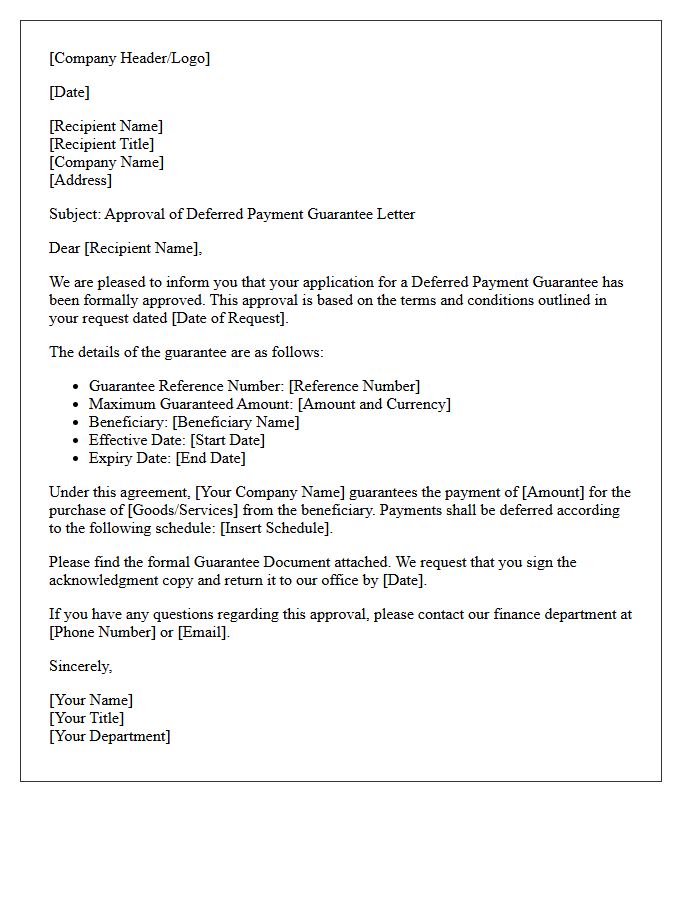

Approval of Deferred Payment Guarantee Letter

A Deferred Payment Guarantee Letter is a formal commitment issued by a bank ensuring that a buyer's payment to a seller will be made at a specified future date. To obtain approval, the applicant must undergo a rigorous credit assessment to demonstrate financial stability. Once authorized, this instrument facilitates international trade by providing payment security to exporters while allowing importers to receive goods before settling the balance. It effectively mitigates non-payment risks, acting as a crucial tool for managing corporate liquidity and strengthening global commercial relationships through verified bank backing.

Issuance of Deferred Payment Guarantee Letter

An Issuance of Deferred Payment Guarantee Letter is a formal commitment by a bank ensuring that a buyer's payment to a seller will be made on a specific future date. This instrument facilitates trade by allowing the importer to take possession of goods immediately while delaying actual payment. It mitigates risk for the exporter, as the bank becomes legally obligated to settle the debt if the buyer defaults. Effectively, it serves as a credit enhancement tool that provides financial security and promotes trust between international trading partners during high-value transactions.

Amendment to Deferred Payment Guarantee Letter

An Amendment to Deferred Payment Guarantee Letter is a formal legal modification to an existing financial commitment. It allows parties to adjust crucial terms such as the expiry date, guarantee amount, or specific payment schedules. This document ensures that the bank's irrevocable undertaking remains aligned with updated contractual obligations between the buyer and seller. Properly executing an amendment is essential for maintaining financial security and ensuring the enforceability of the guarantee during long-term trade transactions or infrastructure projects.

Extension of Deferred Payment Guarantee Letter

An Extension of Deferred Payment Guarantee Letter is a formal legal amendment that prolongs the validity of an existing financial security. It is crucial for maintaining contractual compliance when project timelines shift or payment obligations are delayed. This document ensures the beneficiary remains protected against default while the applicant avoids immediate cash outlays. To remain valid, the extension must be formally approved by the issuing bank and clearly state the new expiry date to prevent a lapse in financial coverage and potential breach of contract.

Cancellation of Deferred Payment Guarantee Letter

The cancellation of a Deferred Payment Guarantee Letter requires the formal return of the original document to the issuing bank. This process typically necessitates a discharge letter signed by the beneficiary, confirming all financial obligations are satisfied. It is crucial to ensure the expiry date has passed or that a written release is obtained to stop commission charges. Proper legal discharge protects the applicant from ongoing liabilities, ensuring the credit facility is restored and the bank's contingent commitment is officially terminated within the global trade system.

Invocation of Deferred Payment Guarantee Letter

An invocation of a Deferred Payment Guarantee Letter occurs when a buyer fails to meet scheduled payment obligations. This legal instrument ensures the beneficiary receives guaranteed funds from the issuing bank upon default. To trigger payment, the seller must present a formal demand complying strictly with all documentary terms. It acts as a vital risk mitigation tool in international trade, providing financial security by shifting the credit risk from the buyer to the bank, ensuring the exporter is compensated despite the importer's non-payment or insolvency.

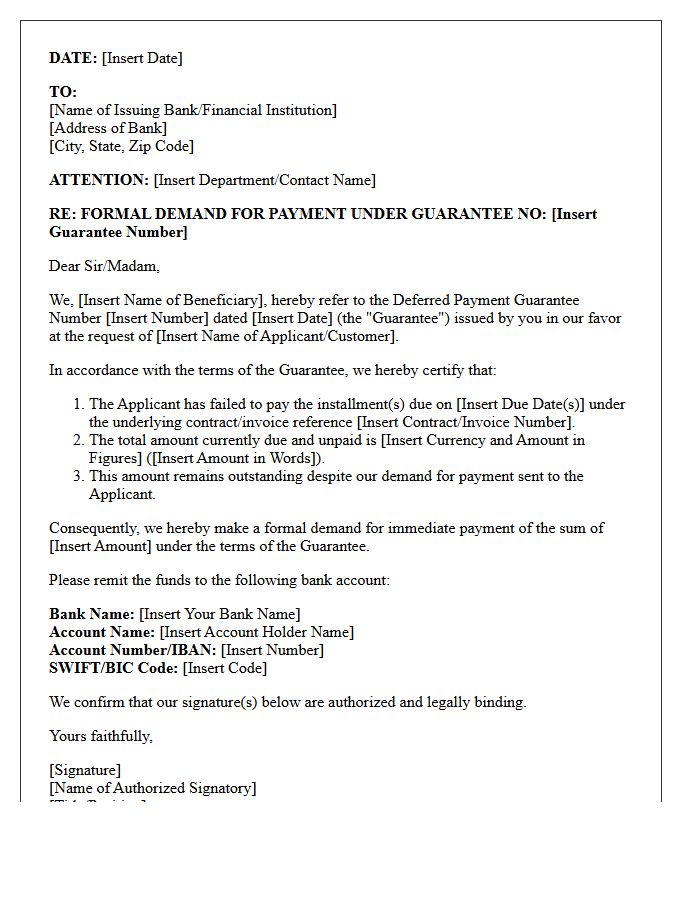

Demand for Payment Under Deferred Payment Guarantee Letter

A Demand for Payment under a Deferred Payment Guarantee is a formal claim triggered when a buyer fails to meet scheduled installments. To ensure a successful claim, the beneficiary must submit a strictly compliant written demand before the expiry date. This document confirms that the underlying payment obligation is due and unpaid. Since banks operate solely on the basis of documents rather than physical goods, any discrepancy in the demand can lead to rejection. It is the primary legal mechanism for a seller to secure funds under a structured credit arrangement.

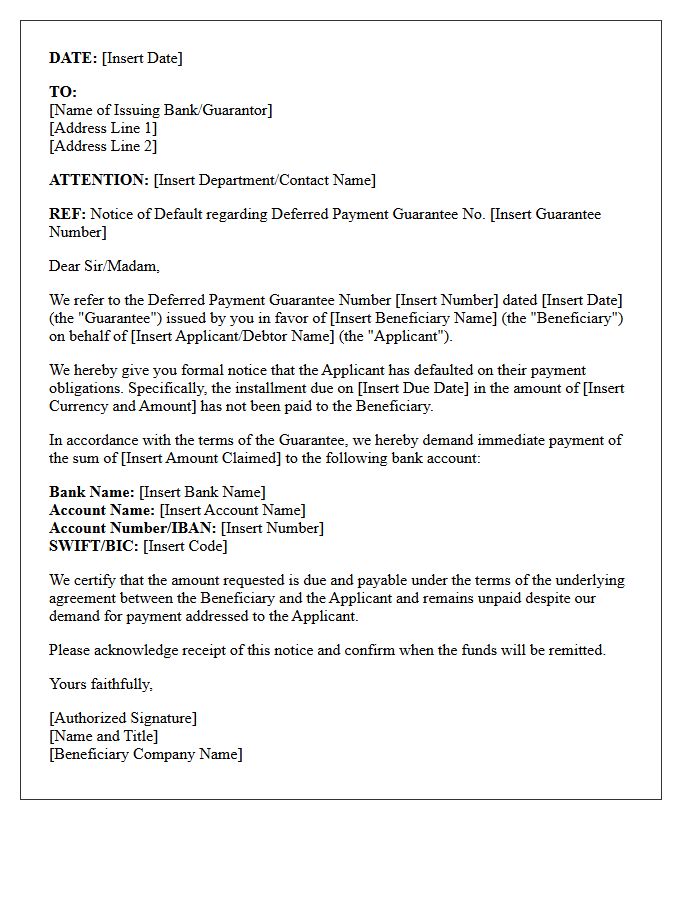

Notice of Default Under Deferred Payment Guarantee Letter

A Notice of Default under a Deferred Payment Guarantee Letter is a critical legal formalization issued when a buyer fails to meet scheduled installments. This document serves as an official demand for payment, notifying the guarantor bank that the underlying financial obligation has been breached. Receiving this notice triggers the immediate activation of the bank's liability to settle the debt on behalf of the applicant. It is the essential prerequisite for enforcing security, potentially leading to legal litigation and severe credit rating damage if the outstanding balance is not promptly rectified.

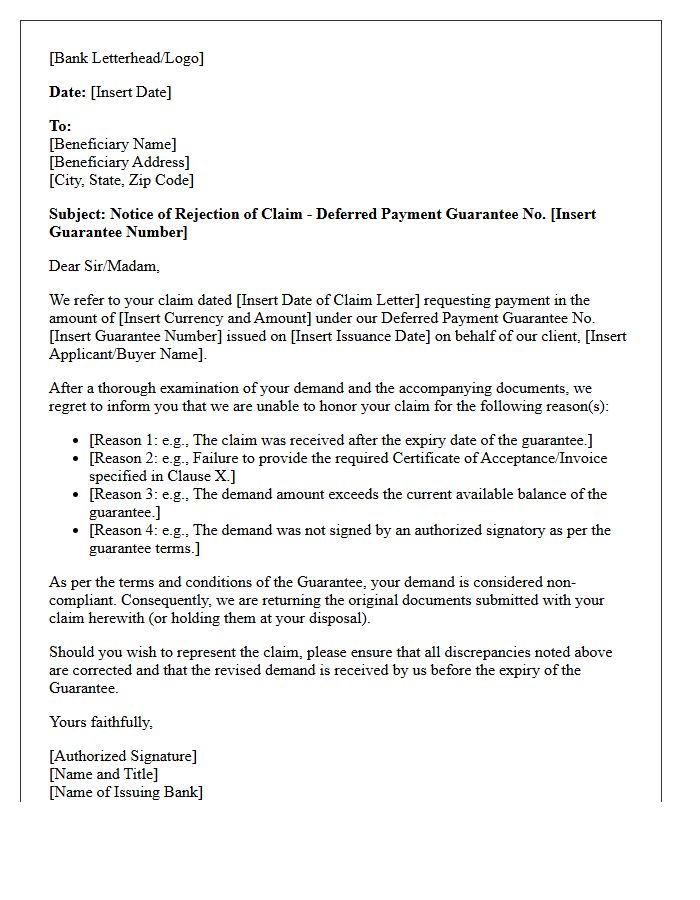

Rejection of Claim on Deferred Payment Guarantee Letter

A rejection of claim on a Deferred Payment Guarantee occurs when the beneficiary's demand fails to strictly comply with the letter's specific terms. Common reasons include late presentation, missing documentation, or incorrect financial figures. Since these guarantees cover future installment obligations, any discrepancy in the default notice or non-conformity with the Uniform Rules for Demand Guarantees (URDG) can lead to a formal refusal. Banks operate under the principle of strict compliance, meaning even minor clerical errors may justify a payment denial regardless of the underlying commercial contract.

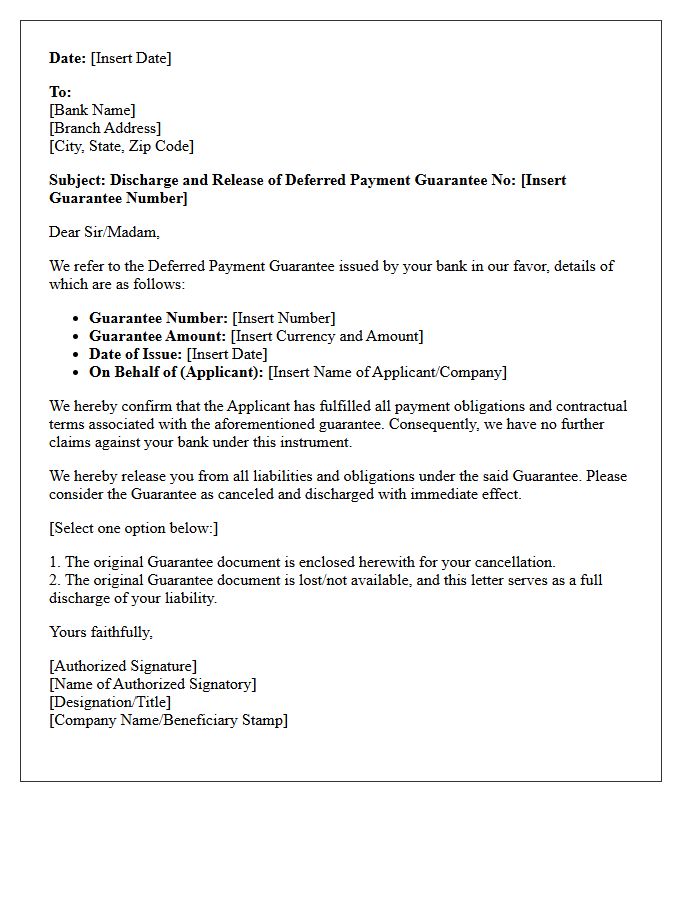

Discharge of Deferred Payment Guarantee Letter

A Discharge of Deferred Payment Guarantee Letter is a formal document issued by a beneficiary to release a bank from its financial obligations. It confirms that the buyer has fulfilled all installment payments for goods or services received. This cancellation process is essential to restore the applicant's credit limit and finalize the transaction. Once the bank receives this written release, the guarantee becomes null and void, ensuring no further claims can be made against the underlying collateral or credit line.

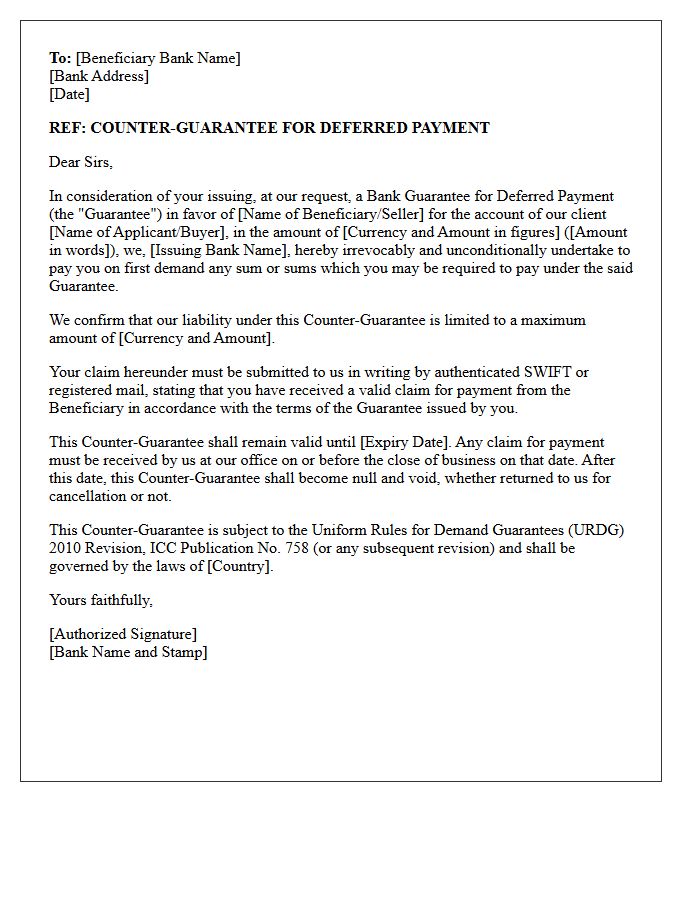

Counter Guarantee Letter for Deferred Payment

A Counter Guarantee Letter is a legal commitment issued by a bank to another bank, securing a primary guarantee for deferred payment obligations. It ensures that the issuing bank will reimburse the intermediary if the buyer fails to meet future payment deadlines. This instrument is essential in international trade to mitigate credit risks and facilitate long-term financing. By providing this additional layer of security, it builds trust between exporters and importers, ensuring that financial liabilities are covered even when payments are scheduled for a later date.

What is a Deferred Payment Guarantee Letter?

A Deferred Payment Guarantee Letter is a financial instrument issued by a bank on behalf of a buyer, promising to pay the seller a specific amount at a predetermined future date. It serves as a credit security that ensures the beneficiary receives payment for goods or services even if the buyer defaults.

How does a Deferred Payment Guarantee differ from a Letter of Credit?

While both provide security, a Letter of Credit is a primary payment mechanism where the bank pays upon presentation of shipping documents. A Deferred Payment Guarantee acts as a secondary obligation, serving as a safety net that is invoked only if the buyer fails to meet their scheduled future payment obligations.

What are the primary benefits of using a Deferred Payment Guarantee for importers?

Importers benefit by obtaining goods immediately while preserving cash flow, as the payment is postponed to a later date. It also enhances their credibility with international suppliers, allowing them to negotiate better trade terms without providing immediate liquidity.

What information must be included in a Deferred Payment Guarantee document?

The document must clearly state the maximum guaranteed amount, the specific expiry date, the underlying contract details, the payment schedule, and the conditions under which a claim can be made. It also specifies the governing laws and the parties involved, including the applicant, beneficiary, and issuing bank.

What are the typical costs associated with obtaining a Deferred Payment Guarantee?

The costs generally include a bank issuance fee, which is often a percentage of the total guarantee value per annum, plus administrative processing charges. The specific rate depends on the applicant's creditworthiness, the duration of the guarantee, and the relationship with the issuing financial institution.

Comments