Securing a First-Time Homebuyer Loan Approval Letter is the essential first step in your property search. This document proves to sellers that you are a qualified buyer with verified financing, giving you a competitive edge in the real estate market. Understanding the requirements helps streamline your journey toward homeownership. To help you get started, below are some ready to use templates.

Image cover: Securing Your First Home: Pre-Approval Letter Templates and Examples

Letter Samples List

- First-Time Homebuyer Pre-Qualification Letter

- First-Time Homebuyer Conditional Loan Approval Letter

- First-Time Homebuyer Final Loan Approval Letter

- First-Time Homebuyer Mortgage Commitment Letter

- First-Time Homebuyer Clear To Close Approval Letter

- First-Time Homebuyer Rate Lock Confirmation Letter

- First-Time Homebuyer Down Payment Assistance Approval Letter

- First-Time Homebuyer Government Grant Award Letter

- First-Time Homebuyer Underwriting Approval Letter

- First-Time Homebuyer Appraisal Acceptance Letter

- First-Time Homebuyer Closing Disclosure Acknowledgment Letter

- First-Time Homebuyer Funding Authorization Letter

- First-Time Homebuyer Welcome And Payment Instruction Letter

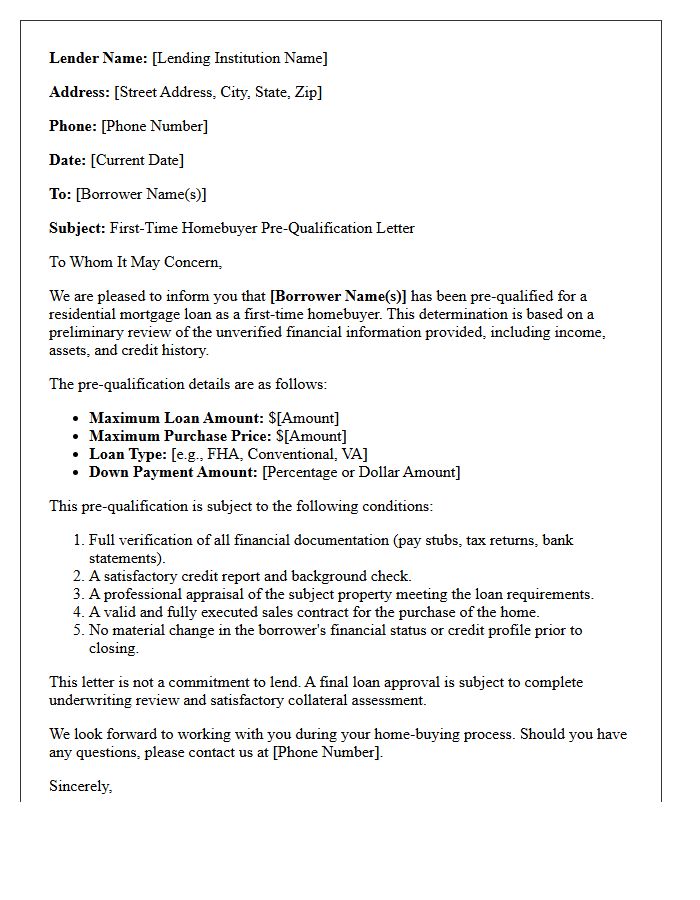

First-Time Homebuyer Pre-Qualification Letter

A Pre-Qualification Letter is an essential first step for any first-time homebuyer. It provides an estimate of how much you can borrow based on self-reported financial data, such as income, debts, and assets. This document shows sellers you are a serious contender and helps you understand your budget before touring properties. While not a final loan approval, it acts as a financial roadmap, allowing you to narrow your search to affordable homes and strengthening your position when submitting an initial offer in a competitive real estate market.

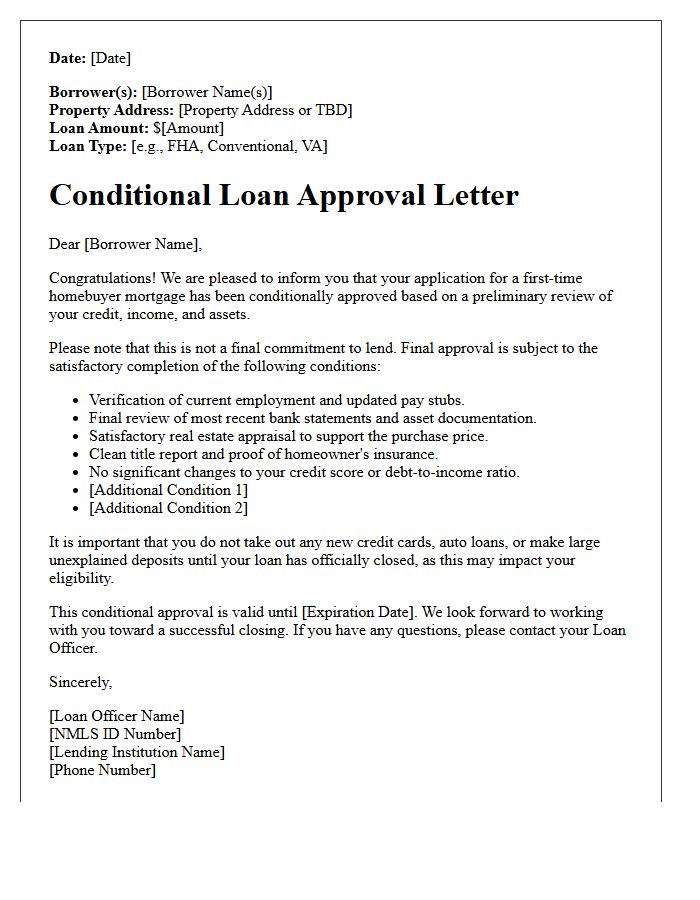

First-Time Homebuyer Conditional Loan Approval Letter

A Conditional Loan Approval Letter is a critical milestone for first-time homebuyers, signaling that a lender is willing to finance the property provided specific conditions are met. Unlike a basic pre-approval, this document follows a formal underwriter review of your financial profile. To secure final funding, you must satisfy outstanding requirements, such as a satisfactory home appraisal, verified employment, or updated bank statements. Receiving this letter strengthens your negotiating position, demonstrating to sellers that you are a qualified buyer nearing the final stages of the mortgage process.

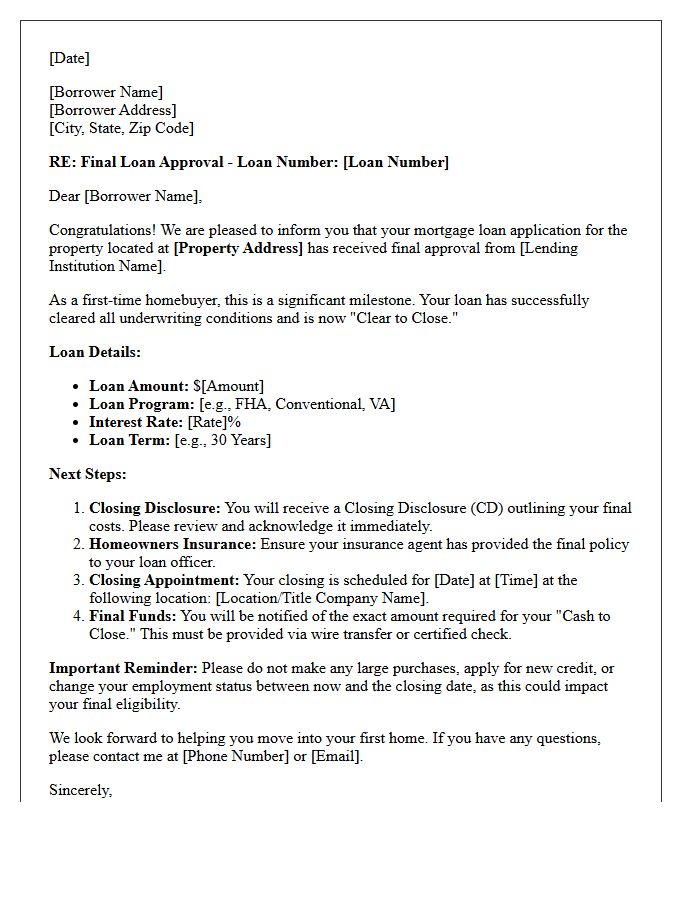

First-Time Homebuyer Final Loan Approval Letter

A Final Loan Approval Letter, often called "clear to close," is the most critical document in the mortgage process. It signifies that the underwriter has verified all financial data and satisfied every contingency. For first-time buyers, this letter confirms that funding is secured and legal documents are ready for signing. It is essential to avoid new debts or job changes after receiving this notice, as lenders may perform a final credit check before releasing funds. This document is your official green light to complete the home purchase.

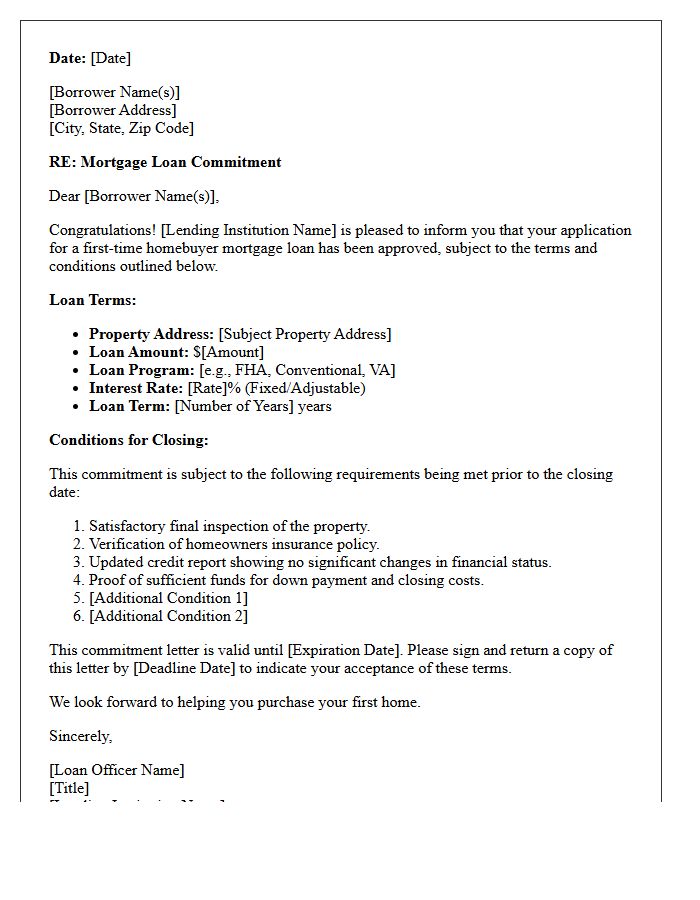

First-Time Homebuyer Mortgage Commitment Letter

A mortgage commitment letter is a formal binding agreement from a lender stating they will provide a loan under specific terms. For a first-time homebuyer, this document is the final hurdle before closing, signifying that underwriting is complete and financial backing is guaranteed. Unlike a pre-approval, it confirms the property and borrower have passed all rigorous checks. It is the most important document to present to sellers to prove you are a qualified buyer ready to finalize the transaction securely and professionally.

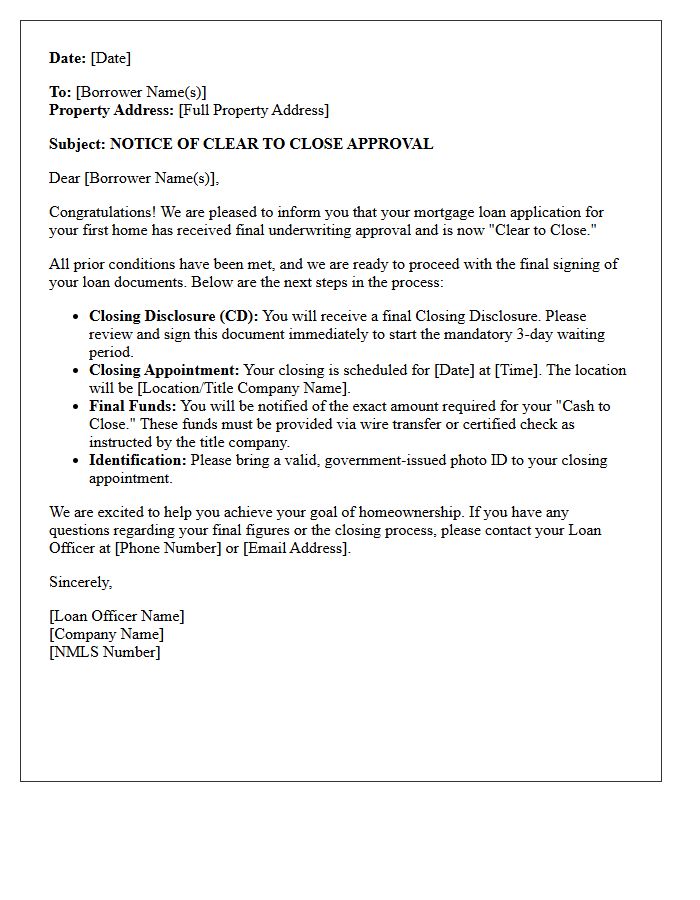

First-Time Homebuyer Clear To Close Approval Letter

Receiving a Clear to Close (CTC) approval letter is the final milestone for a first-time homebuyer. It signifies that the underwriter has verified all financial documentation and satisfied every loan condition. Once issued, your lender has authorized the funding of your mortgage, allowing you to sign the final documents. To ensure a smooth transition, avoid opening new credit lines or making large purchases after this stage. This letter is the definitive green light that officially transitions you from an applicant to a homeowner, confirming your closing date is set.

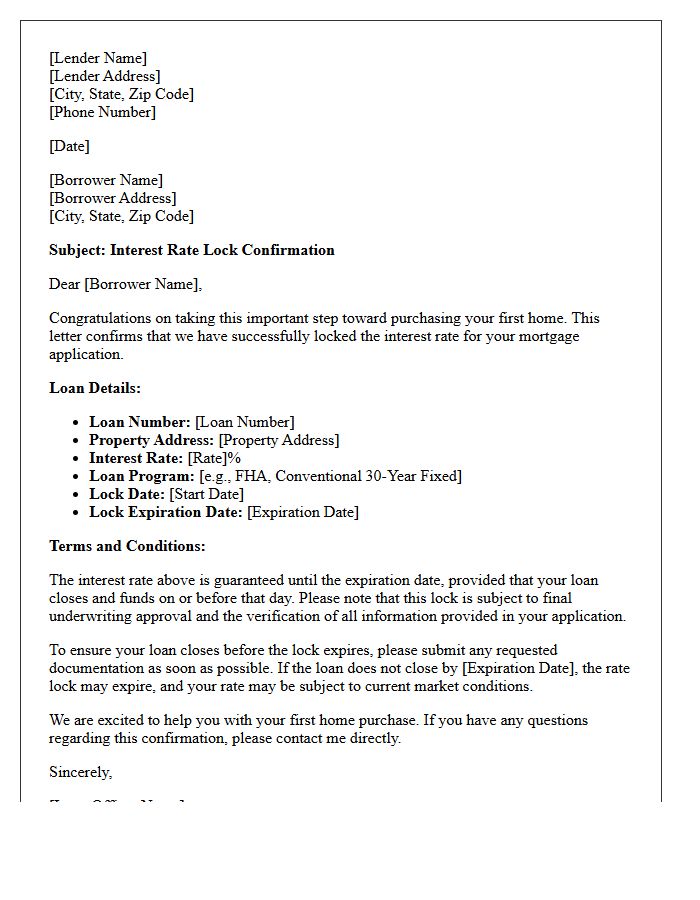

First-Time Homebuyer Rate Lock Confirmation Letter

A First-Time Homebuyer Rate Lock Confirmation Letter is a vital document from your lender that guarantees a specific interest rate for a set period. This protects you against market fluctuations while your loan is processed. It is essential to verify the expiration date and any associated fees to ensure the rate remains valid until closing. Always review the letter carefully to confirm that the agreed-upon terms, such as the loan program and points, are accurately reflected before proceeding with your home purchase.

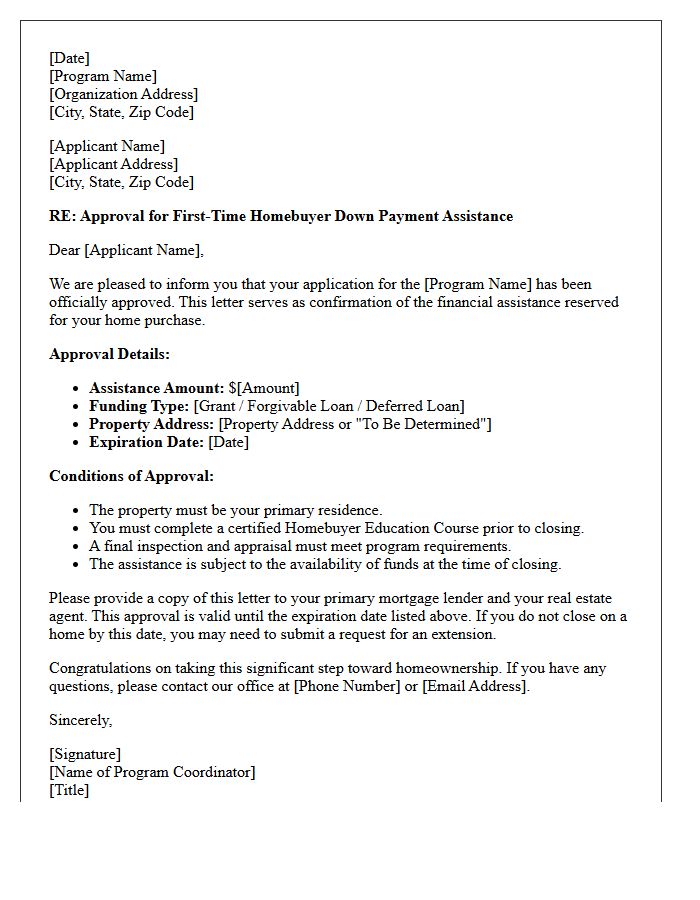

First-Time Homebuyer Down Payment Assistance Approval Letter

A First-Time Homebuyer Down Payment Assistance Approval Letter is a critical document confirming your eligibility for financial grants or low-interest loans. This official statement proves to sellers that you have secured the necessary upfront capital to cover closing costs and equity requirements. Issued by government agencies or non-profits, it specifies the maximum subsidy amount you can receive. Having this letter in hand strengthens your purchase offer, demonstrating that your funding sources are verified and ready, which significantly increases your credibility in a competitive real estate market.

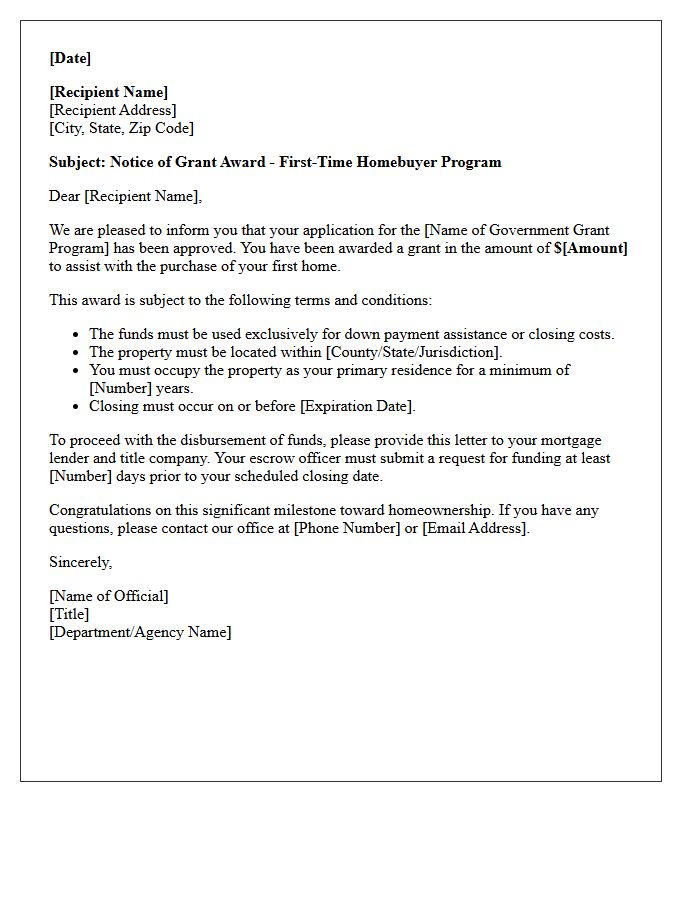

First-Time Homebuyer Government Grant Award Letter

A First-Time Homebuyer Government Grant Award Letter is an official document confirming you have been approved for financial assistance. This letter specifies the exact grant amount, any required conditions, and the intended use of funds, such as down payment or closing costs. It serves as formal proof for lenders during the mortgage underwriting process, verifying your eligibility for subsidized support. Always ensure the letter is signed by the issuing agency and keep a copy for your records to ensure a smooth closing on your first home purchase.

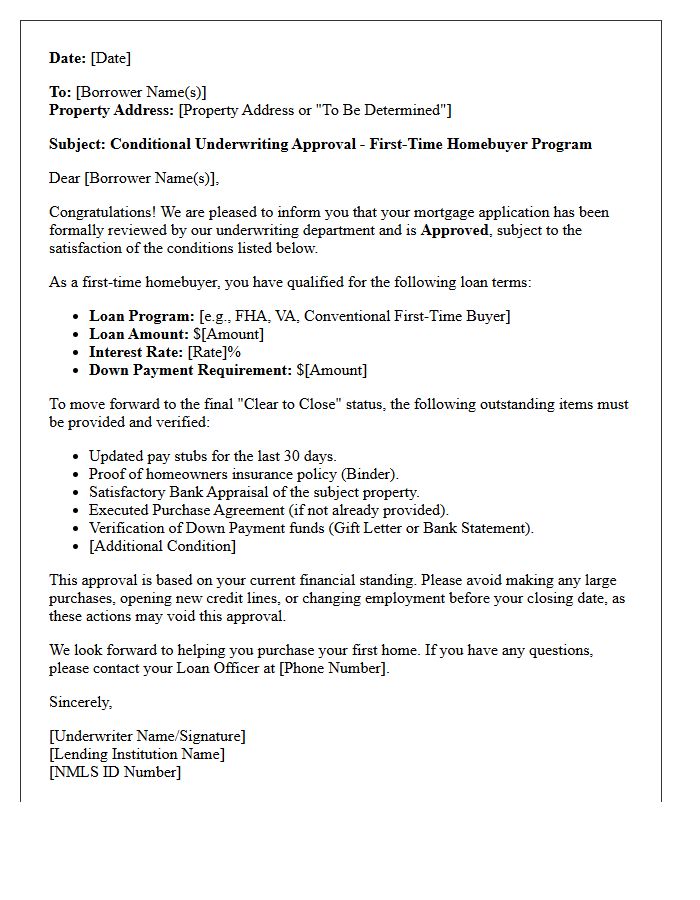

First-Time Homebuyer Underwriting Approval Letter

A First-Time Homebuyer Underwriting Approval Letter is a formal commitment from a lender indicating a loan officer has verified your financial documentation. Unlike a basic pre-qualification, this document signifies that your credit, income, and assets have passed a rigorous review process. It provides a competitive advantage in real estate negotiations by proving to sellers that your financing is secure. To obtain this, you must submit tax returns, pay stubs, and bank statements for evaluation, ensuring your mortgage reliability before officially making an offer on a property.

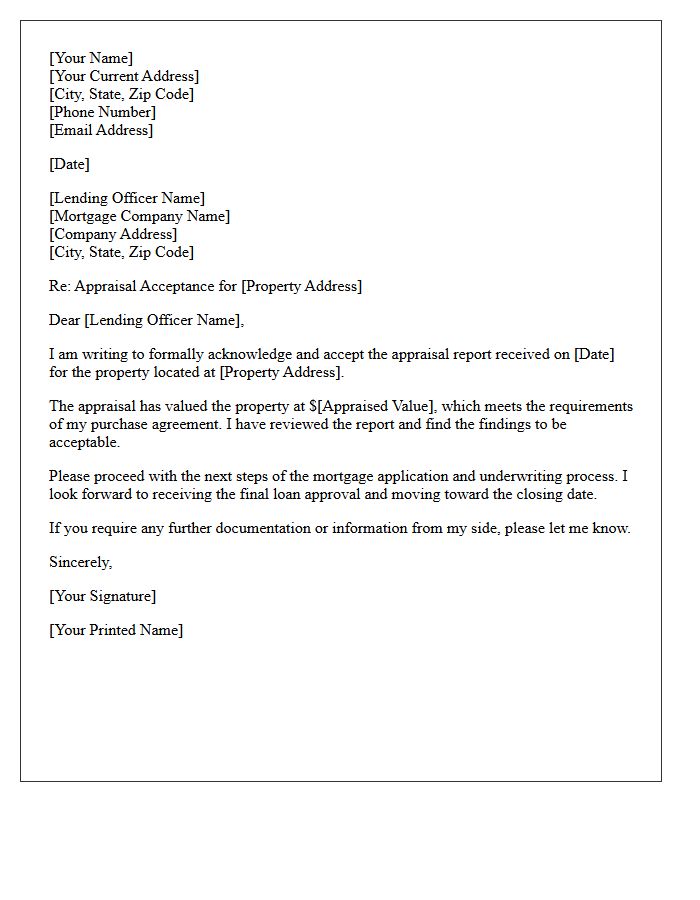

First-Time Homebuyer Appraisal Acceptance Letter

A First-Time Homebuyer Appraisal Acceptance Letter is a formal document confirming that a professional valuation matches or exceeds the agreed purchase price. This letter is crucial for mortgage approval, as lenders will not finance an amount higher than the appraised value. Receiving this notice signifies that the collateral for your loan is secure, allowing the underwriting process to proceed. Understanding this document ensures you are protected from overpaying and keeps your journey toward homeownership on track toward a successful closing.

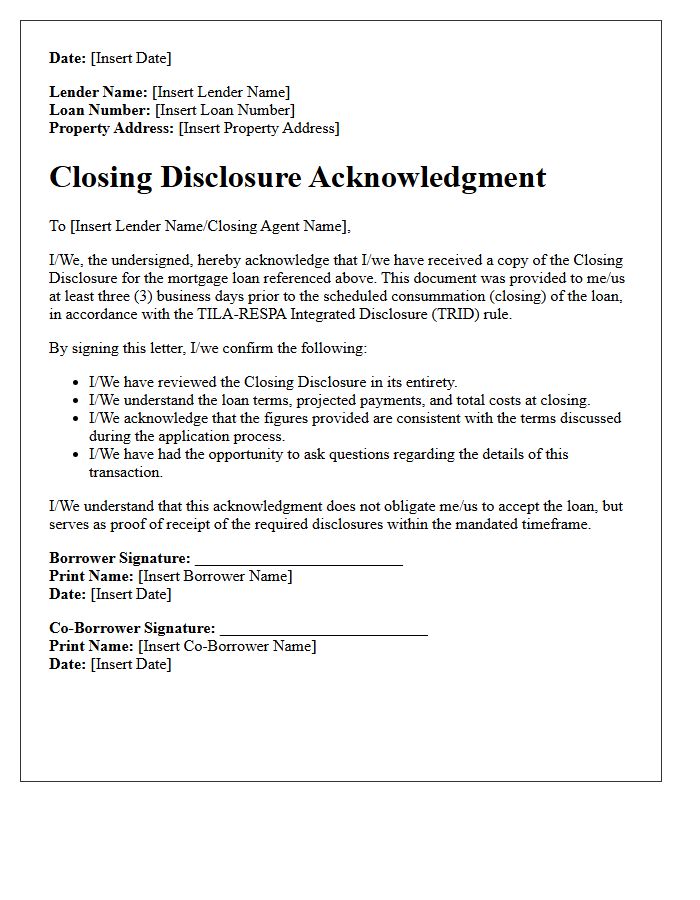

First-Time Homebuyer Closing Disclosure Acknowledgment Letter

The First-Time Homebuyer Closing Disclosure Acknowledgment Letter is a vital document confirming you have received and reviewed your final loan terms. By signing, you acknowledge the three-day cooling-off period required by federal law before settlement. This ensures you understand your interest rate, monthly payments, and total closing costs. Carefully compare this letter against your initial Loan Estimate to identify any discrepancies in fees. It is not a commitment to the loan, but a legal receipt proving you were given time to make an informed financial decision.

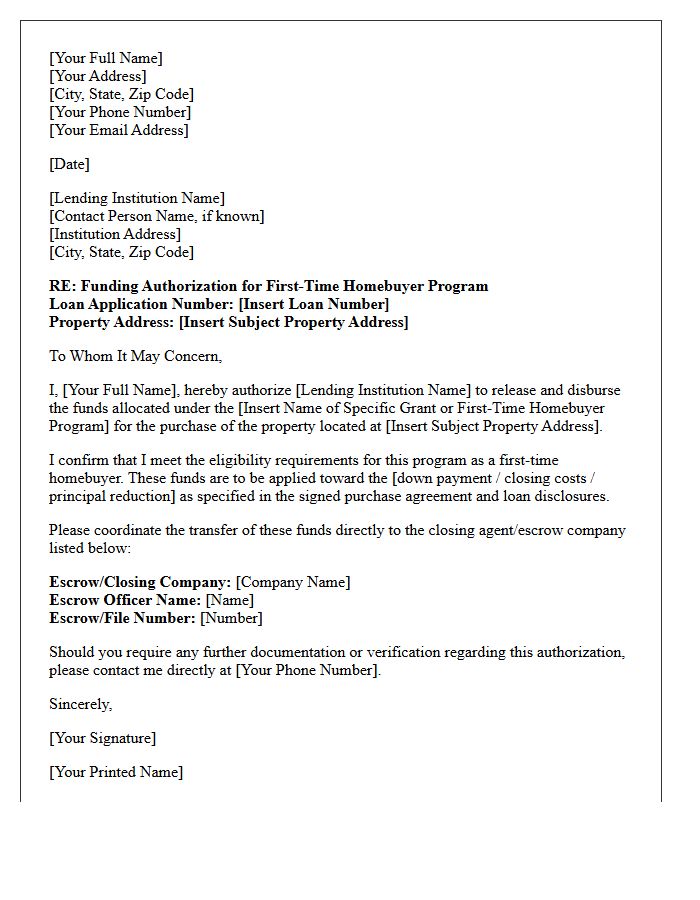

First-Time Homebuyer Funding Authorization Letter

A First-Time Homebuyer Funding Authorization Letter is a critical document that confirms a lender's formal commitment to provide financial backing for your property purchase. Unlike a basic pre-approval, this letter verifies that your credit, income, and assets have undergone a rigorous review process. It serves as official proof of funds, giving sellers confidence that your financing is secure. Obtaining this authorization strengthens your negotiating position, ensures a smoother closing process, and confirms the specific loan amount you are qualified to borrow in today's competitive real estate market.

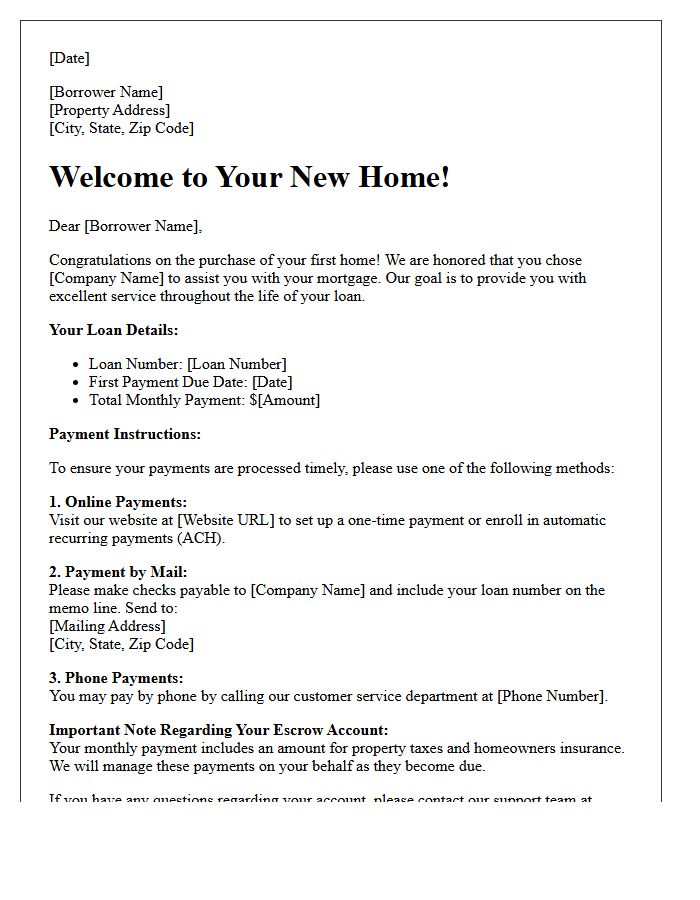

First-Time Homebuyer Welcome And Payment Instruction Letter

The First-Time Homebuyer Welcome and Payment Instruction Letter is a critical document received after closing. It confirms your new loan details and provides official payment instructions to ensure your first mortgage installment is processed correctly. This letter prevents payment delays and protects you from potential wire fraud by verifying the legitimate servicing address. Always review the breakdown of your monthly escrow, interest, and principal amounts listed. Keep this document in your permanent records as it serves as the formal bridge between your closing agent and your long-term mortgage servicer.

What is a first-time homebuyer loan approval letter?

A first-time homebuyer loan approval letter, also known as a pre-approval letter, is a document from a mortgage lender stating the specific loan amount you are qualified to borrow based on an evaluation of your credit score, income, and financial history.

How do I get a mortgage approval letter as a first-time buyer?

To obtain an approval letter, you must submit a formal loan application to a lender, providing documentation such as W-2s, pay stubs, bank statements, and tax returns for a comprehensive credit and financial review.

How long is a home loan pre-approval letter valid?

Most mortgage approval letters are valid for 60 to 90 days. Because credit reports and financial documents expire, lenders require an updated review if you do not find a property within that timeframe.

Why is a loan approval letter important for making an offer?

An approval letter proves to sellers and real estate agents that you are a serious, qualified buyer with secured financing, which is often a mandatory requirement for submitting a winning bid in a competitive housing market.

Does a pre-approval letter guarantee that I will get the loan?

No, a pre-approval letter is not a final guarantee. Final loan approval is subject to a satisfactory home appraisal, a title search, and no significant changes to your financial status or credit score before the closing date.

Comments