A Conditional Mortgage Approval Letter is a formal document from a lender indicating you are approved for a loan, provided specific requirements are met. It outlines necessary documentation like appraisals or income verification needed for final funding. Understanding these conditions helps secure your home financing efficiently. To simplify your application process, below are some ready to use template.

Image cover: Understanding the Conditional Mortgage Approval Letter: Samples and Templates

Letter Samples List

- Mortgage Pre-Qualification Letter

- Mortgage Pre-Approval Letter

- Standard Conditional Mortgage Approval Letter

- Official Mortgage Commitment Letter

- Incomplete Application Notification Letter

- Appraisal Contingency Update Letter

- Interest Rate Lock Confirmation Letter

- Outstanding Loan Condition Request Letter

- Condition Satisfaction Confirmation Letter

- Final Mortgage Approval Letter

- Mortgage Closing Authorization Letter

- Mortgage Loan Counteroffer Letter

- Adverse Action Denial Letter

- Loan Funding Confirmation Letter

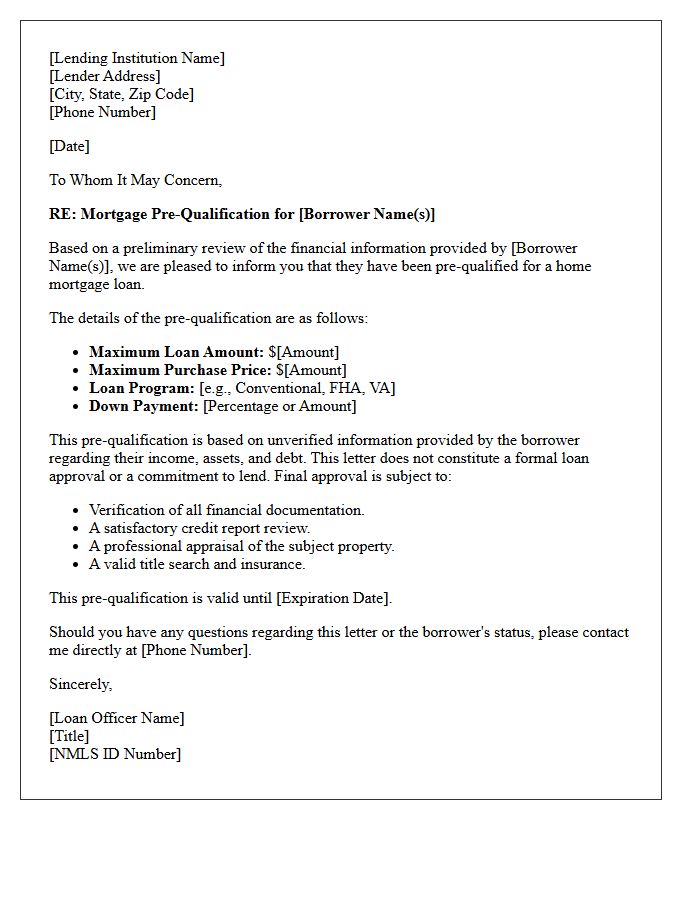

Mortgage Pre-Qualification Letter

A Mortgage Pre-Qualification Letter provides a preliminary estimate of your borrowing power based on self-reported financial data. It is an essential first step in the home-buying process, signaling to sellers that you are a serious buyer. Unlike a formal approval, it relies on unverified information regarding your income, debts, and assets. Obtaining this document helps you understand your budget and streamlines the search for a property within your financial reach. While it is not a binding loan commitment, it serves as a vital tool for early market competitiveness.

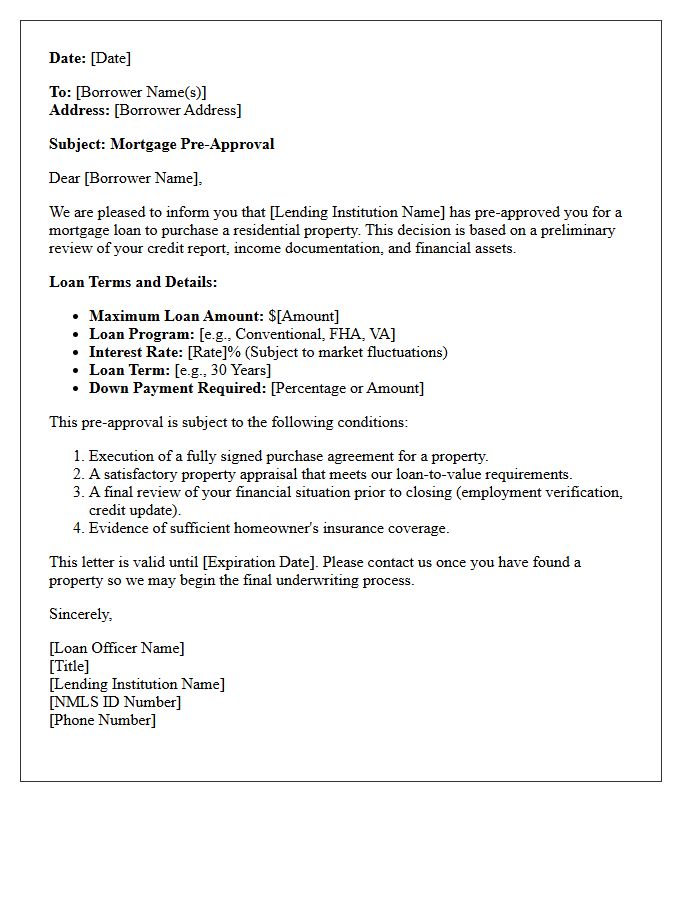

Mortgage Pre-Approval Letter

A Mortgage Pre-Approval Letter is a document from a lender stating the specific loan amount you qualify for based on a preliminary credit and income evaluation. It is an essential tool for homebuyers because it demonstrates financial credibility to real estate agents and sellers. Having this letter ensures your offers are taken seriously in competitive markets, as it confirms you have the necessary backing to secure financing. Always obtain one before starting your property search to understand your budget and strengthen your negotiating power during the home-buying process.

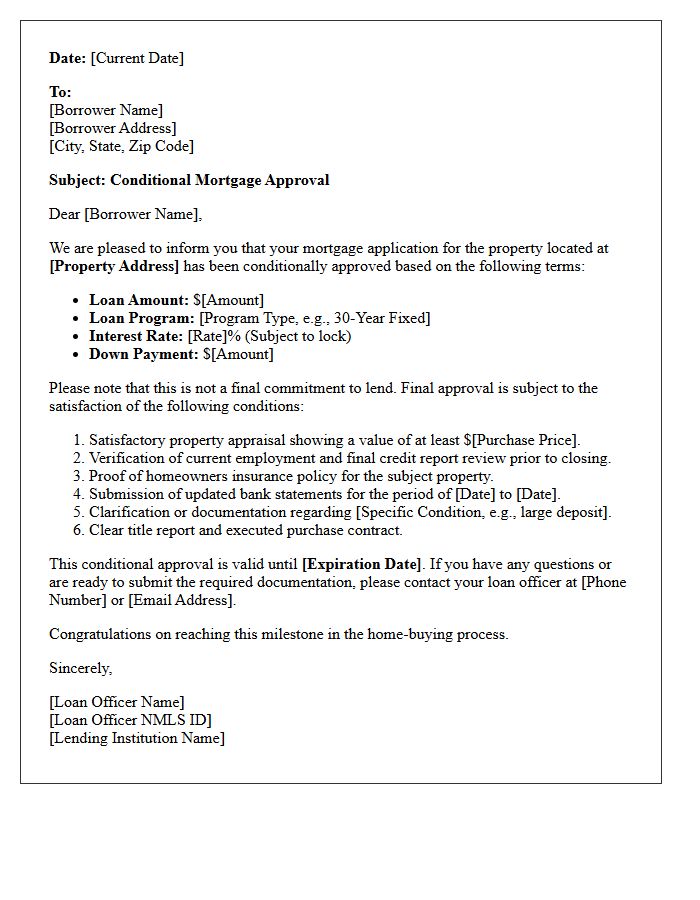

Standard Conditional Mortgage Approval Letter

A standard conditional mortgage approval letter is a formal document from a lender indicating they are willing to fund your home loan, provided specific requirements are met. Unlike a basic pre-approval, this underwriting decision signifies that your credit and income have been verified. Final funding remains contingent on conditions such as a satisfactory property appraisal, clear title search, and no significant changes to your financial status. This letter strengthens your bargaining power, signaling to sellers that you are a qualified buyer nearing the final stages of the mortgage process.

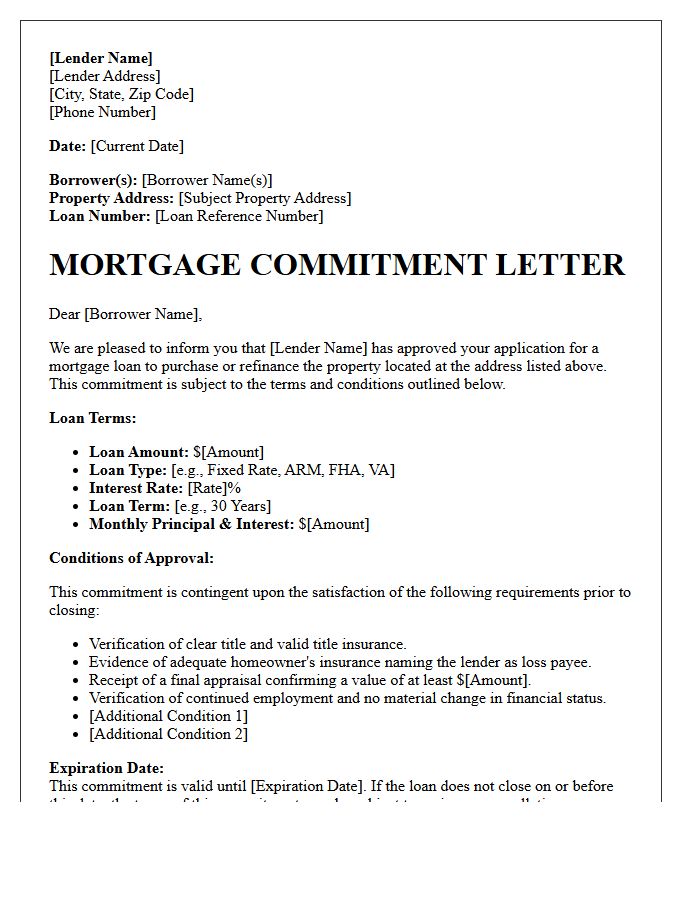

Official Mortgage Commitment Letter

An Official Mortgage Commitment Letter is a legally binding document issued by a lender after completing the full underwriting process. Unlike a pre-approval, this letter confirms that your loan is approved for a specific property and amount, subject to final conditions. It is the most important milestone before closing, signaling to sellers that your financing is secure. Homebuyers should carefully review the expiration date and any outstanding contingencies to ensure a smooth transition to final funding and property ownership.

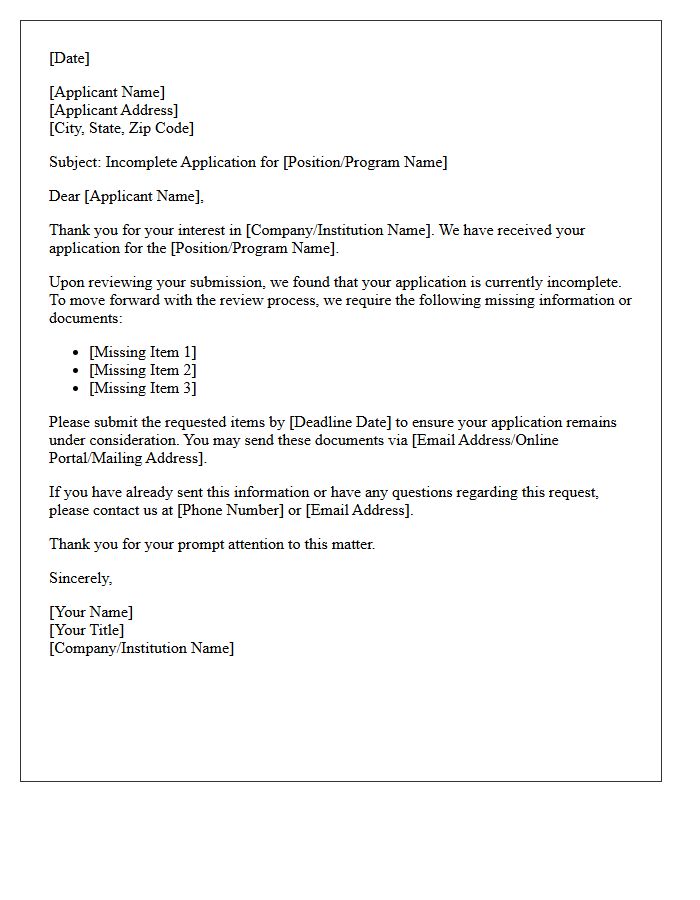

Incomplete Application Notification Letter

An Incomplete Application Notification Letter is a formal document sent by organizations to inform applicants that their submission lacks required information or documentation. Receiving this letter means your application is on hold and will not be processed until the missing details are provided. It typically specifies a strict deadline for submission to avoid automatic rejection. To ensure a successful outcome, you must review the listed deficiencies carefully and respond promptly with the accurate data. Timely action is essential to maintain your eligibility and keep your application moving forward through the evaluation phase.

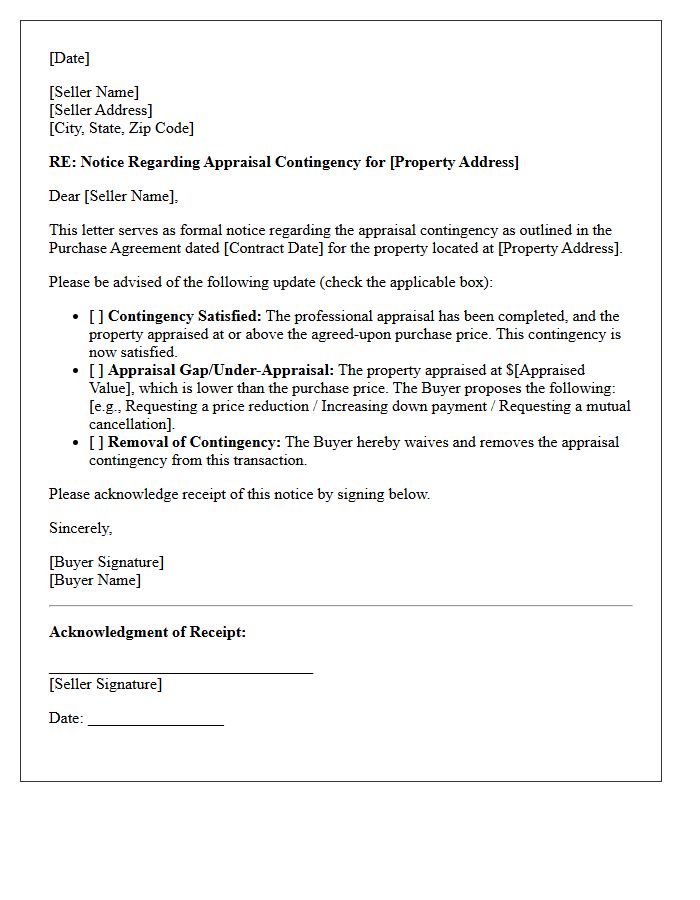

Appraisal Contingency Update Letter

An Appraisal Contingency Update Letter is a formal document used to notify parties when a property's appraised value differs from the purchase price. This update is critical for mortgage approval, as lenders base loan amounts on the appraisal results. If a valuation gap occurs, the letter initiates negotiations to adjust the price, increase the down payment, or exercise a contingency exit. Timely delivery is essential to protect the buyer's earnest money deposit and ensure legal compliance within the contract's specified due diligence timelines.

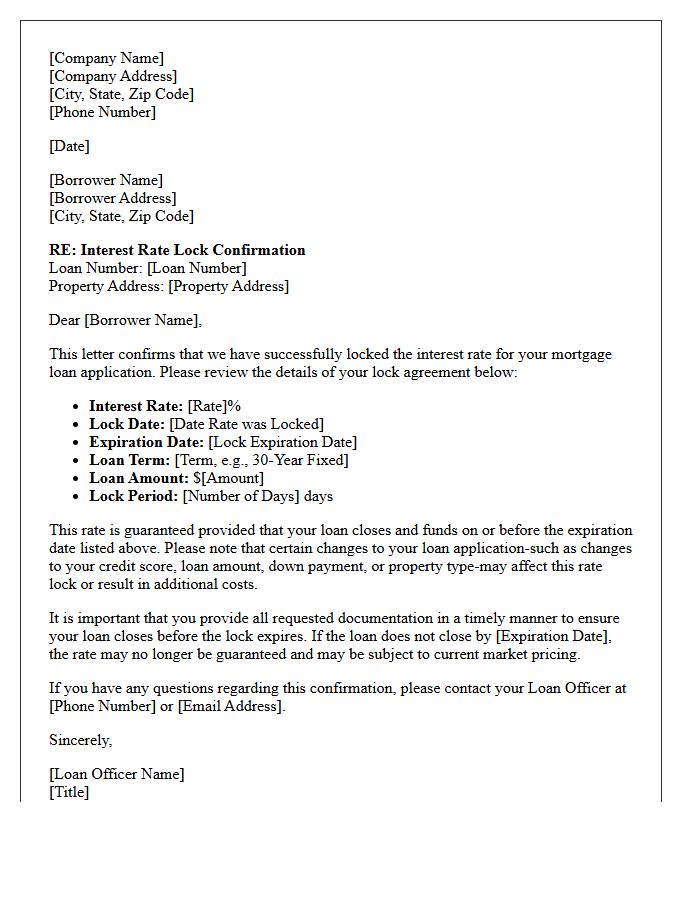

Interest Rate Lock Confirmation Letter

An Interest Rate Lock Confirmation Letter is a vital document from your lender that guarantees a specific interest rate for a set period. This protection ensures your monthly payment remains unchanged despite market fluctuations while your loan is processed. It specifies the expiration date, points, and loan terms. To maintain this rate, you must close your mortgage before the lock expires. Reviewing this document carefully is essential to verify that the agreed-upon financial terms are accurately recorded and legally secured for your home purchase or refinance.

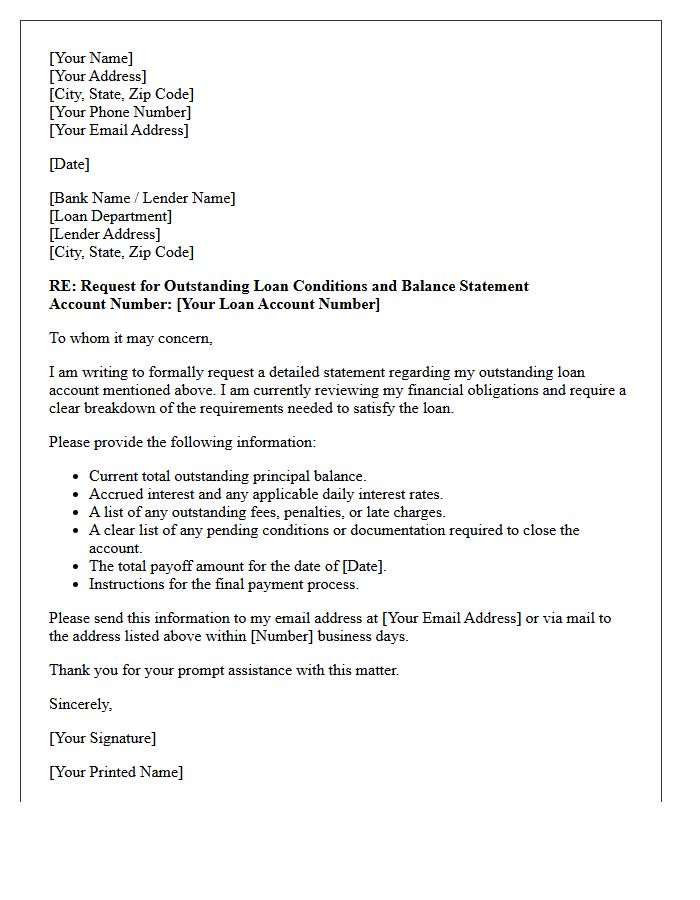

Outstanding Loan Condition Request Letter

An Outstanding Loan Condition Request Letter is a formal document sent to a financial institution to obtain a precise payoff statement. It serves as an official inquiry to verify the remaining principal, accrued interest, and any applicable penalties. This transparency is essential for effective debt management or refinancing. To ensure accuracy, the letter should include your account number, contact information, and a specific date for the financial disclosure. Accurate documentation protects the borrower's rights and ensures a clear path toward total loan settlement and credit health improvement.

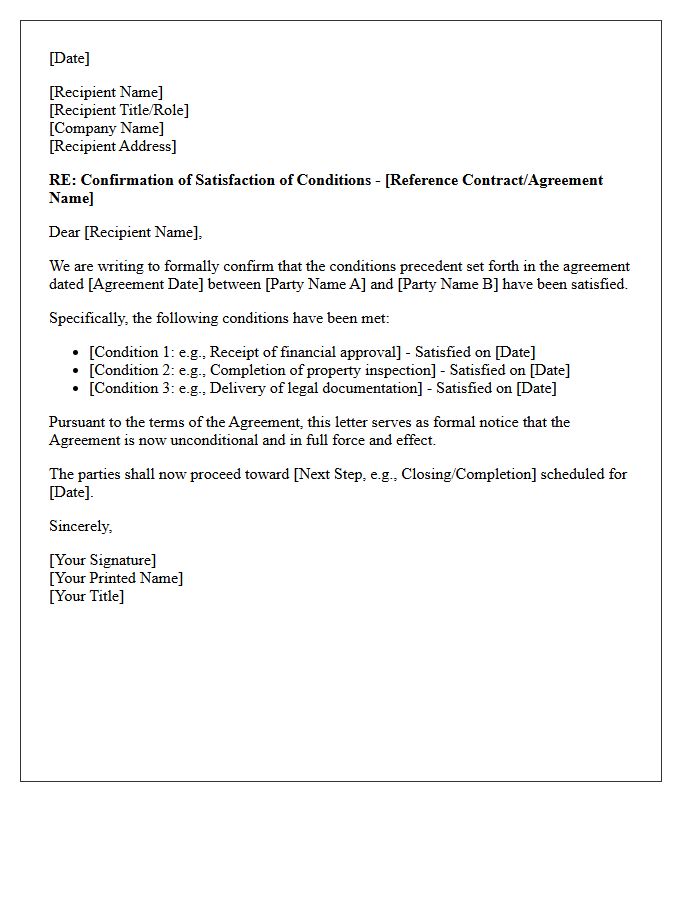

Condition Satisfaction Confirmation Letter

A Condition Satisfaction Confirmation Letter is a formal legal document used to verify that all contingencies within a contract have been met. Typically issued during real estate transactions, it signifies that requirements like financing, inspections, or repairs are fulfilled. Once signed, this letter transforms a conditional agreement into a binding contract, preventing parties from withdrawing without penalty. It provides essential legal protection by establishing a clear written record that all specific obligations are satisfied, ensuring a smooth transition toward the final closing process and ownership transfer.

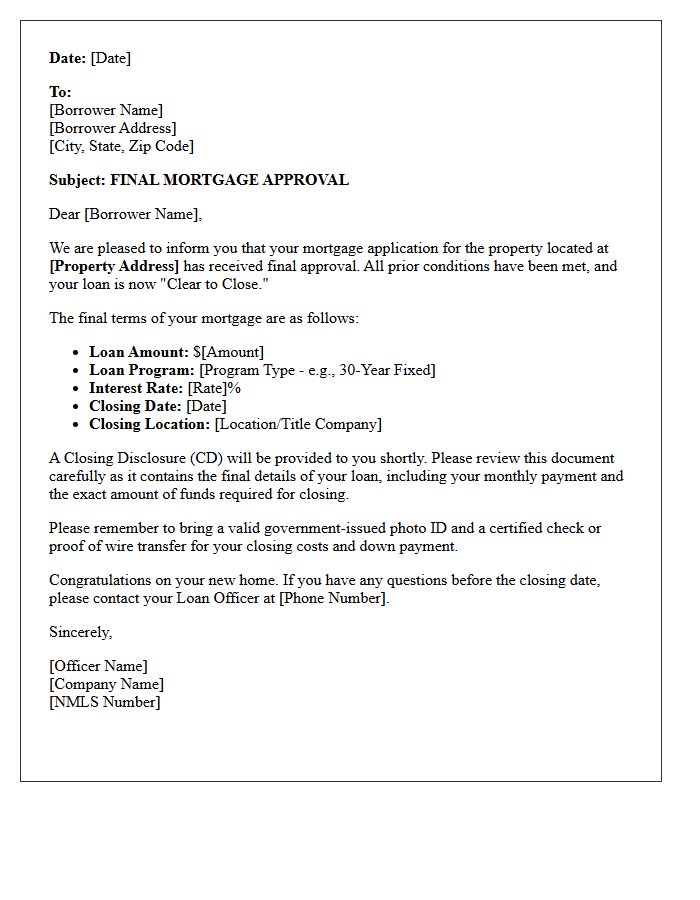

Final Mortgage Approval Letter

A Final Mortgage Approval Letter, often called "Clear to Close," is the definitive document confirming your lender has verified all financial data and met every underwriting condition. This letter signifies that loan funding is authorized, allowing you to proceed to the settlement table. Crucially, you must avoid major credit changes or employment shifts until the keys are in hand, as lenders perform a final credit refresh before disbursing funds. Receiving this document means your home purchase is officially secured and ready for legal completion.

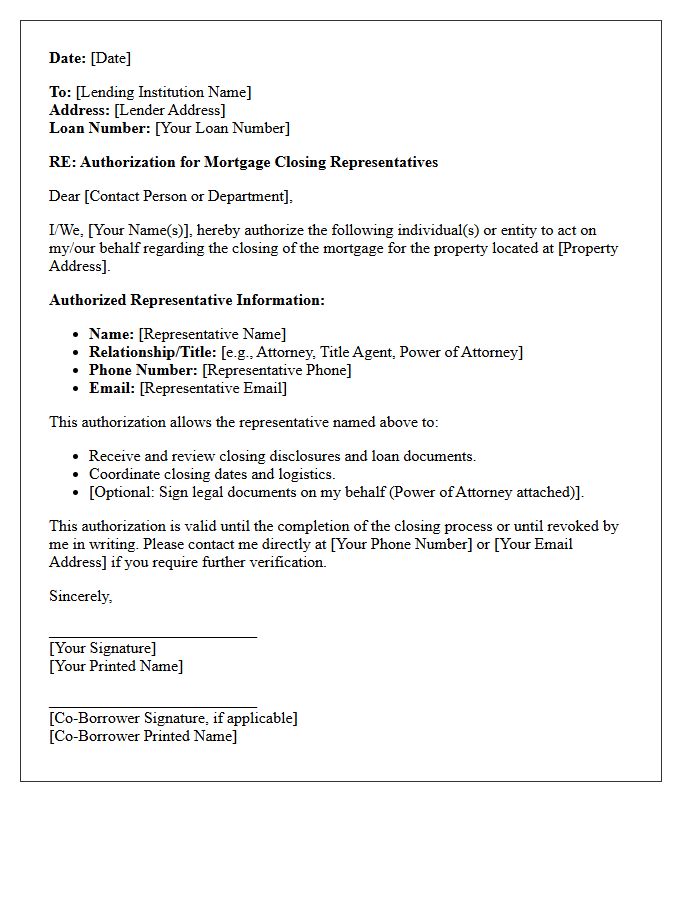

Mortgage Closing Authorization Letter

A Mortgage Closing Authorization Letter is a formal document that permits a third party to act on your behalf during a real estate transaction. It is essential when a borrower cannot attend the final signing in person. This letter must explicitly state the agent's identity and the specific powers granted, such as signing loan documents or transferring funds. To ensure legal validity, the document typically requires a notary acknowledgment. This authorization prevents processing delays, ensuring the property transfer and loan funding proceed smoothly and securely according to lender requirements.

Mortgage Loan Counteroffer Letter

A mortgage loan counteroffer letter is a formal response from a lender indicating they cannot approve your original application but propose alternative financing terms. This document typically outlines changes to the loan amount, interest rate, or required down payment. It is crucial to review these modifications carefully to ensure the new terms remain affordable. Applicants have a specific timeframe to either accept, reject, or further negotiate the proposal. Receiving a counteroffer is a common part of the underwriting process, signaling that the lender is still interested in your business under adjusted conditions.

Adverse Action Denial Letter

An Adverse Action Denial Letter is a legally required notice sent to consumers when a business denies credit, insurance, or employment based on information in a credit report. Under the Fair Credit Reporting Act (FCRA), lenders must disclose the specific reasons for the rejection and identify the credit bureau used. Receiving this letter entitles you to a free credit report within sixty days to ensure the data is accurate. Reviewing these details is essential for identifying errors or identity theft that may have negatively impacted your application status.

Loan Funding Confirmation Letter

A Loan Funding Confirmation Letter is an official document issued by a lender verifying that a loan has been approved and the capital is ready for disbursement. This letter serves as formal proof of financing, detailing the specific loan amount, interest rates, and transfer dates. It is essential for borrowers to demonstrate financial credibility to third parties, such as home sellers or business partners, ensuring that the necessary funds are secured to complete a transaction successfully and legally.

What is a conditional mortgage approval letter?

A conditional mortgage approval letter is a formal document from a lender stating they are willing to lend you a specific amount, provided you meet certain outstanding requirements or "conditions" before closing.

What are the common conditions listed in a conditional approval?

Common conditions include providing additional pay stubs, verifying the source of a large deposit, proof of homeowners insurance, a satisfactory property appraisal, and a final credit refresh to ensure no new debt has been taken on.

How does a conditional approval differ from a pre-approval?

While a pre-approval is an initial estimate of your borrowing power, a conditional approval occurs after an underwriter has reviewed your full application and documentation, moving you significantly closer to the final "clear to close" status.

Can a mortgage be denied after receiving a conditional approval letter?

Yes, a mortgage can still be denied if the borrower fails to satisfy the listed conditions, experiences a drop in credit score, loses their job, or if the property appraisal comes in significantly lower than the purchase price.

How long does it take to get a conditional mortgage approval?

The process typically takes 1 to 2 weeks after you have submitted your full mortgage application and all initial supporting financial documents to the lender's underwriting department.

Comments