Receiving an Agriculture Loan Denial Letter due to insufficient acreage or low projected yield can stall your farming operations. Lenders often reject applications when land size or production history fails to meet strict collateral requirements. Understanding these risk factors is essential for successfully appealing a decision or seeking alternative financing. To help you respond effectively, below are some ready to use template.

Image cover: Sample Denial Letters for Agricultural Loans: Insufficient Acreage Yield and Productivity Standards

Letter Samples List

- Agriculture Loan Insufficient Acreage Yield Denial Letter

- Farm Operating Loan Inadequate Crop Yield Rejection Letter

- Commercial Agribusiness Loan Low Acreage Production Denial Letter

- Crop Production Loan Substandard Acreage Output Denial Letter

- Agricultural Line Of Credit Deficient Harvest Yield Rejection Letter

- Agricultural Real Estate Loan Insufficient Acreage Revenue Denial Letter

- Rural Farming Loan Low Per-Acre Yield Denial Letter

- Small Farm Financing Inadequate Acreage Projection Rejection Letter

- Livestock And Crop Loan Subpar Acreage Yield Denial Letter

- Agricultural Equipment Loan Insufficient Crop Return Rejection Letter

- Harvest Financing Loan Deficient Acreage Yield Denial Letter

- Commercial Farming Loan Inadequate Acreage Profitability Denial Letter

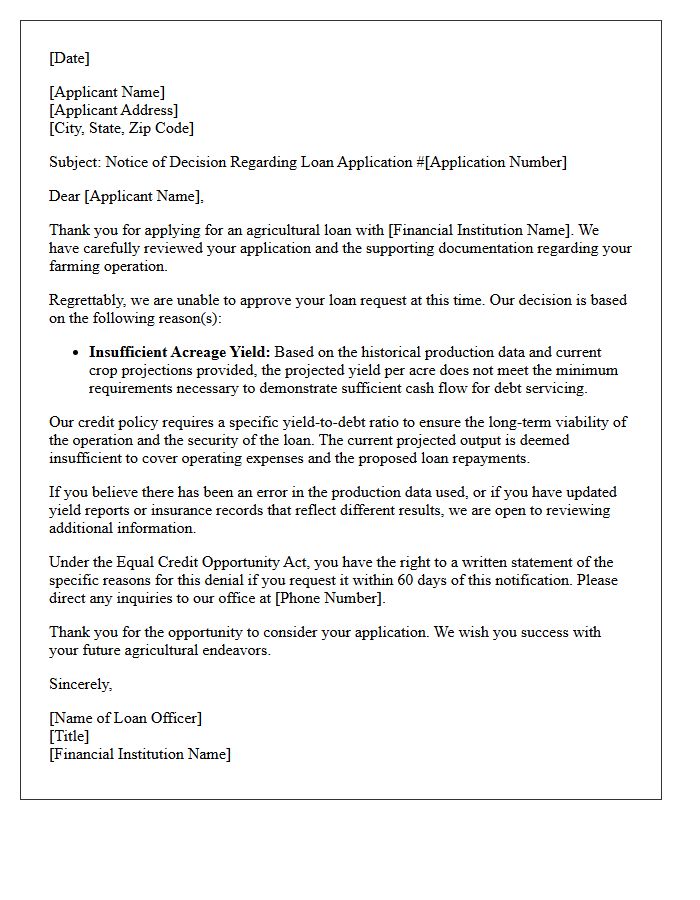

Agriculture Loan Insufficient Acreage Yield Denial Letter

An Agriculture Loan Denial Letter for insufficient acreage yield typically occurs when a farm's historical production data fails to meet underwriting requirements. Lenders analyze your average yields to determine if the projected income can sustain debt obligations. If your proven yield per acre is too low compared to regional benchmarks, the loan is deemed high-risk. To appeal, provide documented production evidence, such as yield monitors or crop insurance records, to demonstrate that localized factors or specific management practices justify a higher revenue potential than the initial assessment suggested.

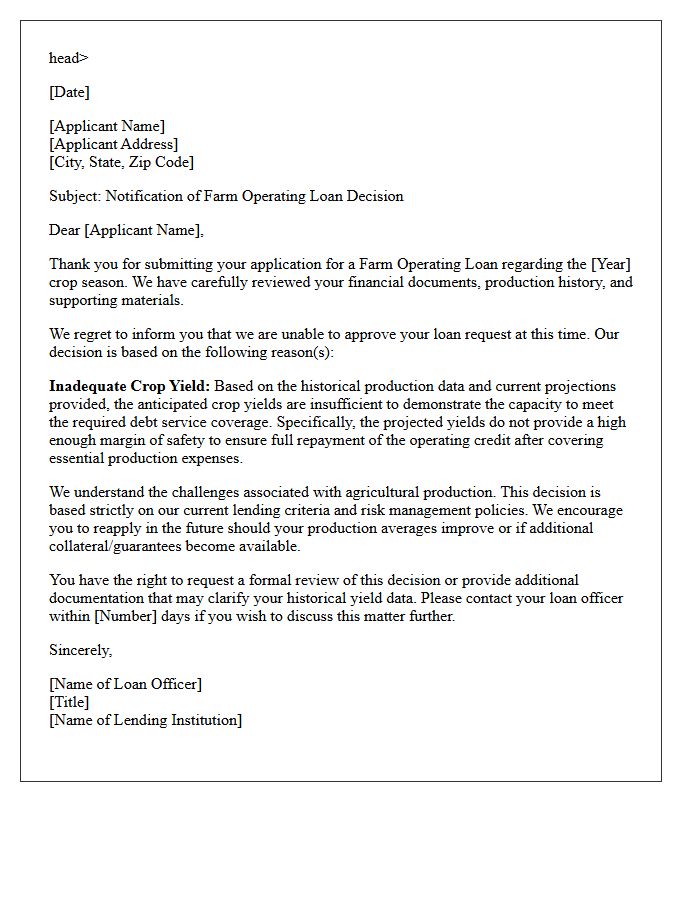

Farm Operating Loan Inadequate Crop Yield Rejection Letter

A Farm Operating Loan Inadequate Crop Yield Rejection Letter is a formal notice from a lender denying credit due to low historical production. This document specifies that the applicant's average yields do not meet the minimum benchmarks required to prove repayment capacity. It serves as a critical financial record for farmers, often highlighting a need for improved crop insurance, better soil management, or updated yield documentation. Understanding this rejection is vital for risk management and helps producers address specific output gaps before reapplying for agricultural financing to sustain future operations.

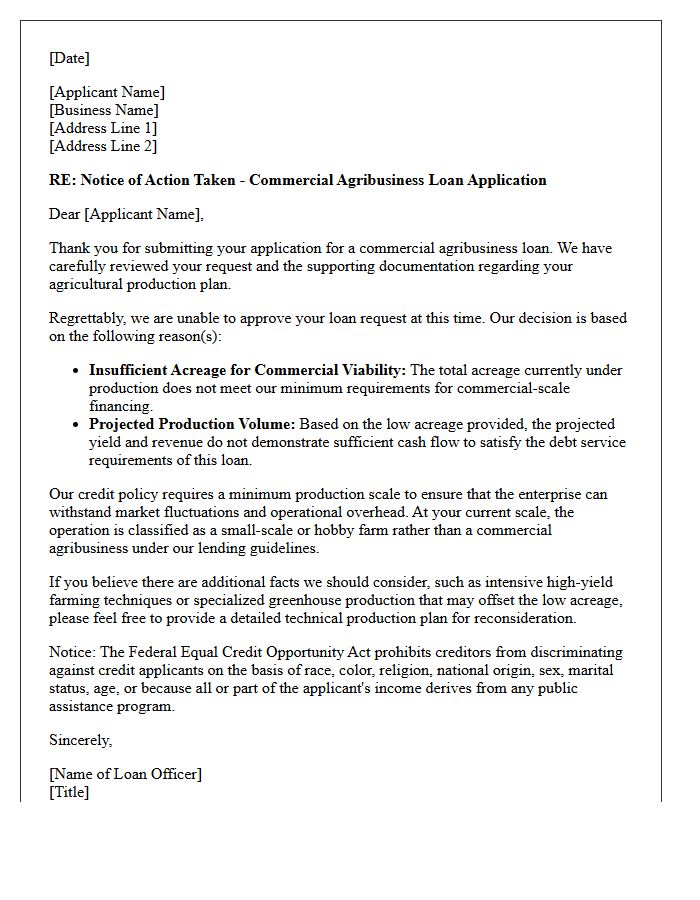

Commercial Agribusiness Loan Low Acreage Production Denial Letter

Receiving a Commercial Agribusiness Loan denial letter for low acreage production often stems from failing to meet minimum economies of scale. Lenders typically require a specific land-to-income ratio to ensure the operation can cover overhead and debt service. If your production footprint is deemed too small, the bank perceives a higher default risk due to limited revenue potential. To challenge this, provide a detailed business plan highlighting high-value crop yields or specialized intensive farming techniques that prove profitability despite smaller land size.

Crop Production Loan Substandard Acreage Output Denial Letter

A Crop Production Loan Substandard Acreage Output Denial Letter is a formal notification issued by agricultural lenders when an operation fails to meet minimum yield expectations. Receiving this document indicates that your collateral value is insufficient to secure the requested financing. The denial typically stems from historical data showing poor soil quality, inadequate irrigation, or consistent low yields on specific land tracts. Understanding this letter is vital for farmers to identify underperforming acreage and explore alternative risk mitigation strategies or government-backed programs to address potential funding gaps in their production cycle.

Agricultural Line Of Credit Deficient Harvest Yield Rejection Letter

An Agricultural Line of Credit Deficient Harvest Yield Rejection Letter is a formal notification from a lender denying further financing. This occurs when a farm's actual production history fails to meet the minimum benchmarks required for collateral security. Lenders issue this notice because low crop volumes increase the risk of loan default. To contest this decision, farmers should provide documented proof of force majeure events, such as extreme weather, or present updated crop insurance claims to demonstrate future repayment capacity and restore their borrowing eligibility.

Agricultural Real Estate Loan Insufficient Acreage Revenue Denial Letter

Receiving an Agricultural Real Estate Loan Denial Letter due to insufficient acreage revenue indicates that the property size fails to generate enough income to meet debt service coverage requirements. Lenders analyze the land's productivity and yield potential to ensure it can support the loan repayment independently. To address this, applicants should provide documented proof of specialized high-value crops, alternative income streams, or additional collateral. Understanding these production benchmarks is vital for securing financing, as it proves the farm's financial viability and long-term operational sustainability within the competitive agricultural market.

Rural Farming Loan Low Per-Acre Yield Denial Letter

Receiving a Rural Farming Loan Denial Letter due to low per-acre yield indicates that your land's productivity falls below the lender's risk threshold. To appeal or reapply, you must provide documented historical production data or proof of mitigating circumstances like extreme weather. Lenders prioritize repayment capacity, so improving your soil health or optimizing crop management is essential. Enhancing your business plan with updated yield projections and conservation practices can demonstrate future viability and help secure the necessary agricultural financing for your farm operations.

Small Farm Financing Inadequate Acreage Projection Rejection Letter

Receiving a Small Farm Financing Inadequate Acreage Projection Rejection Letter typically indicates that your business plan lacks sufficient land to meet revenue targets. Lenders reject applications when the projected crop yields or livestock density appear unrealistic for the specified plot size. To appeal, you must provide a detailed farm management plan, soil productivity data, or proof of high-intensity farming techniques like vertical cropping or greenhouses. Demonstrating financial viability through precise historical data or expert endorsements is essential to prove that your limited acreage can successfully sustain the proposed debt repayment schedule.

Livestock And Crop Loan Subpar Acreage Yield Denial Letter

A Livestock and Crop Loan Subpar Acreage Yield Denial Letter notifies producers that their financing request was rejected due to insufficient productivity benchmarks. Lenders issue these notices when historical or projected harvests fail to meet the minimum yield thresholds required to secure the debt. This document typically cites a lack of collateral value or high repayment risk linked to historical performance data. It is essential to review the letter for specific data discrepancies and to understand your rights regarding the appeal process or potential restructuring of the loan application.

Agricultural Equipment Loan Insufficient Crop Return Rejection Letter

An Agricultural Equipment Loan Insufficient Crop Return Rejection Letter notifies a borrower that their application was denied due to low historical yields or projected revenue. Lenders issue this document when repayment capacity cannot be verified against the requested debt. It typically details the financial shortfall, citing that current agricultural output is inadequate to cover equipment installments. To improve future eligibility, farmers should focus on risk mitigation strategies and providing updated production data. This formal notice ensures transparency regarding the lender's credit decision based on projected harvest income.

Harvest Financing Loan Deficient Acreage Yield Denial Letter

A Harvest Financing Loan Deficient Acreage Yield Denial Letter is a formal notice issued when a lender determines your crop production or acreage falls below the required threshold for funding. This document signifies that the collateral value is insufficient to secure the requested capital. Receiving this letter often necessitates an immediate re-evaluation of yield data or proof of alternative risk mitigation. To resolve a denial, farmers should review their Actual Production History (APH) records and provide updated documentation to demonstrate future harvest potential and debt repayment capacity.

Commercial Farming Loan Inadequate Acreage Profitability Denial Letter

Receiving a commercial farming loan denial letter due to inadequate acreage signifies that your land base is insufficient to generate projected profits. Lenders evaluate the debt service coverage ratio to ensure the operational scale supports repayment. To overcome this, focus on high-value niche crops or integrate vertical farming techniques to maximize profitability per square foot. Providing a detailed business plan that proves efficiency can mitigate concerns regarding physical size. Addressing these land utilization gaps is essential for securing future agricultural financing and demonstrating long-term commercial viability.

Why was my agriculture loan denied due to insufficient acreage?

Your agriculture loan application was denied because the total tillable acreage listed in your farm operating plan does not meet the minimum land base requirements necessary to generate sufficient revenue for debt service and operating expenses.

How does land acreage impact the approval of an agricultural operating loan?

Lenders evaluate acreage to determine if the scale of production is large enough to cover the fixed costs of farming, provide a living for the operator, and ensure there is enough collateral and cash flow to repay the loan principal and interest.

What does "insufficient projected yield" mean in a loan denial letter?

Insufficient projected yield indicates that your historical production records or regional averages suggest the output per acre will not produce enough gross income to satisfy the financial obligations of the requested loan and your existing overhead.

Can I appeal a loan denial based on acreage or yield calculations?

Yes, you can appeal by providing updated soil quality reports, proof of intensive farming techniques (such as high-yield specialty crops), or long-term lease agreements that demonstrate an increase in your total operational land base.

How can I improve my eligibility for an agriculture loan after a denial for low acreage?

To improve eligibility, consider expanding your operation through land leases, integrating higher-value organic or specialty crops that require less acreage for profit, or providing a co-signer or additional non-farm income to offset the production gap.

Comments