Facing a loan denial due to inconsistent income can be overwhelming. Our guide explores how debt consolidation loan employment instability rejection affects your financial strategy and offers actionable steps to rebuild your credit profile. Learn how to address lender concerns and improve your future approval odds. Below are some ready to use template options to help you respond effectively.

Image cover: Navigating Debt Consolidation Rejections Due to Employment Instability: Communication Guide and Templates

Letter Samples List

- Debt Consolidation Loan Decline Letter Due to Employment Instability

- Employment Instability Rejection Letter for Debt Consolidation Application

- Debt Consolidation Denial Letter Regarding Irregular Employment History

- Insufficient Employment Tenure Debt Consolidation Rejection Letter

- Adverse Action Letter for Debt Consolidation Employment Instability

- Debt Consolidation Loan Rejection Letter Based on Employment Verification

- Unstable Income Debt Consolidation Loan Denial Letter

- Debt Consolidation Application Rejection Letter Citing Employment Instability

- Employment History Ineligibility Letter for Debt Consolidation Loan

- Short-Term Employment Debt Consolidation Loan Decline Letter

- Debt Restructuring Loan Rejection Letter Due to Employment Volatility

- Debt Consolidation Credit Denial Letter for Insufficient Employment Duration

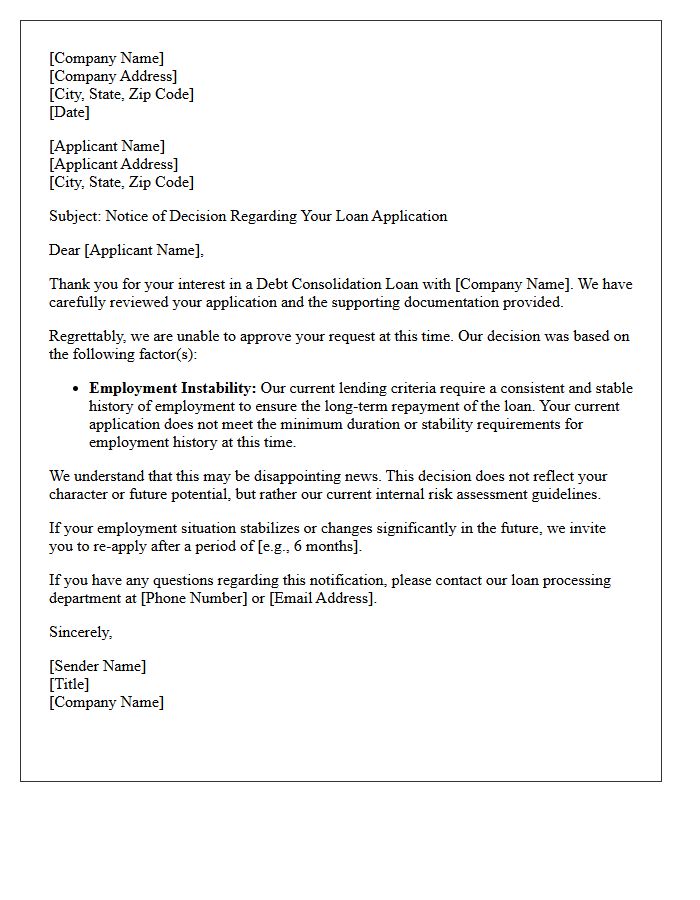

Debt Consolidation Loan Decline Letter Due to Employment Instability

Receiving a debt consolidation loan decline letter due to employment instability indicates that the lender views your current job situation as a financial risk. Lenders prioritize a steady income stream to ensure monthly repayments. If you have frequent gaps in employment, a recent career change, or seasonal work, you may be deemed ineligible. To improve future approval odds, focus on maintaining consistent employment for at least six months and consider providing additional documentation of supplementary income or a co-signer to mitigate the lender's concerns regarding your financial stability.

Employment Instability Rejection Letter for Debt Consolidation Application

Receiving an Employment Instability Rejection Letter means your debt consolidation application was denied due to inconsistent income or brief job tenure. Lenders prioritize repayment reliability; therefore, frequent gaps in employment or a recent career change signal high risk. To improve your chances for future approval, focus on maintaining stable employment for at least six months and documenting steady earnings. If your income is currently fluctuating, consider applying with a co-signer or exploring alternative relief options like credit counseling to manage your debt effectively while building career longevity.

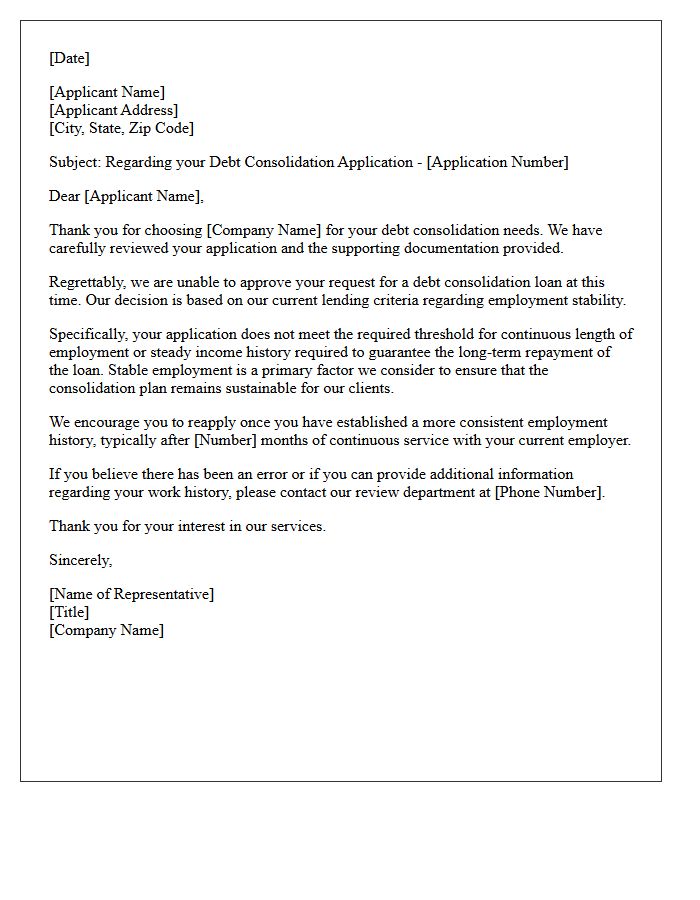

Debt Consolidation Denial Letter Regarding Irregular Employment History

Receiving a debt consolidation denial letter often stems from an irregular employment history, which lenders view as a high-risk factor. Financial institutions prioritize repayment stability; therefore, frequent job gaps or seasonal work can signal inconsistent income. To improve future approval odds, focus on maintaining steady employment for at least six to twelve months. If denied, review your adverse action notice to identify specific concerns. Strengthening your application with a co-signer or providing proof of supplemental income can help mitigate perceived risks associated with professional transitions or career instability.

Insufficient Employment Tenure Debt Consolidation Rejection Letter

Receiving an insufficient employment tenure debt consolidation rejection letter indicates that lenders view a short job history as a financial risk. To qualify for low-interest refinancing, most institutions require at least six to twelve months of continuous service with the same employer. This stability requirement ensures you have a reliable income stream to manage future repayments. If rejected, focus on building consistent work history or consider a co-signer to strengthen your application. Improving your credit score during this period can also increase your chances of approval once your tenure meets the criteria.

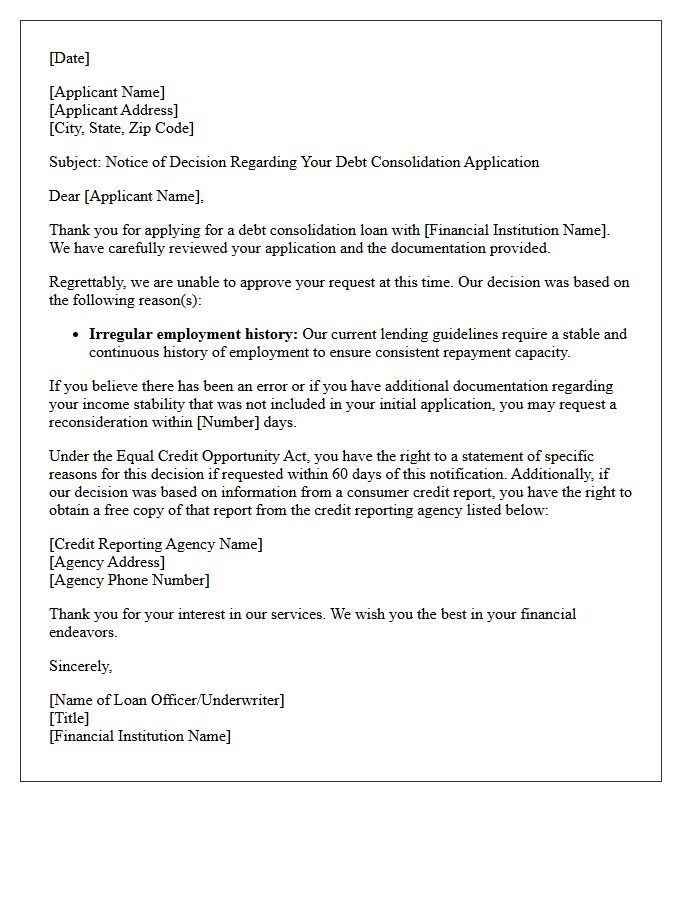

Adverse Action Letter for Debt Consolidation Employment Instability

An Adverse Action Letter is a formal notice sent to applicants when debt consolidation is denied due to employment instability. Lenders view frequent job changes or gaps as a high risk to consistent repayment. Receiving this letter is critical because it explains the specific reasons for rejection and identifies which credit reporting agency provided the data. Under the Fair Credit Reporting Act, you are entitled to a free credit report copy to dispute inaccuracies. Stable income verification is essential to demonstrate your long-term ability to manage consolidated debt effectively.

Debt Consolidation Loan Rejection Letter Based on Employment Verification

Receiving a debt consolidation loan rejection due to employment verification means the lender could not confirm your stable income. Lenders require proof of consistent employment to ensure you can manage monthly repayments. If you are recently self-employed, a seasonal worker, or started a new job, you may appear high-risk. To resolve this, review your employment history for accuracy, provide additional documents like tax returns or pay stubs, and ensure your employer's contact details are current. Improving income stability increases your chances of future approval for consolidating high-interest debt.

Unstable Income Debt Consolidation Loan Denial Letter

Receiving an Unstable Income Debt Consolidation Loan Denial Letter indicates that lenders perceive your fluctuating earnings as a high repayment risk. Financial institutions require consistent cash flow to ensure monthly obligations are met. To improve future approval odds, document all alternative revenue sources, reduce your debt-to-income ratio, or consider a co-signer with steady employment. Review the adverse action notice carefully to identify specific reasons for rejection, such as insufficient employment history or volatile commission structures, allowing you to address these financial stability concerns before reapplying.

Debt Consolidation Application Rejection Letter Citing Employment Instability

Receiving a debt consolidation rejection due to employment instability indicates that lenders perceive your income as unpredictable. Financial institutions require stable employment history to ensure consistent monthly repayments. If you recently changed jobs, have gaps in service, or work in a seasonal industry, you are viewed as a higher risk. To improve future approval odds, maintain your current position for at least six months, provide additional proof of supplemental income, or consider applying with a creditworthy co-signer to mitigate the lender's concerns regarding your professional stability and cash flow.

Employment History Ineligibility Letter for Debt Consolidation Loan

Receiving an employment history ineligibility letter for a debt consolidation loan indicates that your work stability does not meet the lender's criteria. Financial institutions prioritize consistent income to ensure reliable repayment. If you have frequent gaps, recent job changes, or unverifiable income, your application may be denied. To improve your chances, maintain steady employment for at least two years or consider a co-signer. Addressing these concerns is essential for securing favorable loan terms and managing your debt effectively through professional consolidation programs.

Short-Term Employment Debt Consolidation Loan Decline Letter

Receiving a Short-Term Employment Debt Consolidation Loan Decline Letter indicates that your current job stability does not meet the lender's risk criteria. Financial institutions typically require a consistent income history to ensure repayment reliability. To improve future approval odds, focus on maintaining steady employment for at least six months and reducing your debt-to-income ratio. Carefully review the letter for specific adverse action reasons, such as insufficient length of employment or low credit scores, and address these factors before reapplying to strengthen your financial profile and demonstrate long-term stability.

Debt Restructuring Loan Rejection Letter Due to Employment Volatility

Receiving a debt restructuring loan rejection letter due to employment volatility indicates that lenders perceive your income source as unstable. High job turnover or seasonal work patterns suggest a greater risk of default, often leading to a denial of more favorable repayment terms. To improve future outcomes, maintain consistent employment records or provide supplemental proof of income stability. Addressing these concerns is essential for demonstrating your long-term ability to honor debt obligations during the financial recovery process.

Debt Consolidation Credit Denial Letter for Insufficient Employment Duration

Receiving a debt consolidation credit denial letter for insufficient employment duration indicates that the lender perceives your job stability as a risk. Financial institutions typically require a consistent work history, often two years or more, to guarantee a steady income for future repayments. If you have recently changed careers or started a new position, lenders may view your profile as volatile. To improve your chances, consider applying after completing several months in your current role or provide documented proof of previous employment to demonstrate long-term career continuity and financial reliability.

Why was my debt consolidation loan denied due to employment instability?

Lenders reject applications for employment instability if your work history shows frequent gaps, a recent career change, or a lack of continuous income. They require proof of a stable earning environment to ensure you can consistently meet the monthly repayment schedule of a consolidation loan.

Can I get a debt consolidation loan if I just started a new job?

Most lenders prefer at least six months to two years of continuous employment with the same employer. If you received a rejection letter due to a recent job change, you may need to wait until you have completed your probationary period or provide additional documentation, such as a signed employment contract, to prove future stability.

What should I do if I receive a debt consolidation rejection letter citing irregular income?

If your rejection was based on irregular income or gig-economy work, you can appeal by providing two years of tax returns (1040s) and several months of bank statements. This helps demonstrate that while your monthly pay fluctuates, your annual aggregate income is sufficient to cover the consolidated debt payments.

How does a gap in employment history affect debt consolidation approval?

A significant gap in your resume suggests a higher risk of default to lenders. Even if you are currently employed, a recent period of unemployment can trigger an automatic rejection. To improve your chances, focus on building 12 months of steady income before reapplying or consider a co-signer with a stable work history.

Are there alternatives to debt consolidation loans for those with unstable work history?

If employment instability prevents loan approval, alternatives include debt management plans (DMP) through non-profit credit counseling agencies, which do not always require the same rigid income stability as a bank. Other options include hardship programs offered directly by your current creditors or seeking a secured loan using collateral.

Comments