Protect your finances by promptly disputing fraudulent transactions with an unauthorized charge affidavit. This formal document serves as a legal statement to your bank, certifying that specific debits were made without your consent. Submitting a clear, accurate letter is essential for reversing charges and initiating a fraud investigation. To help you get started quickly, below are some ready to use templates.

Image cover: Template Guide: Writing an Official Unauthorized Charge Affidavit Letter

Letter Samples List

- Unauthorized Charge Affidavit Letter

- Debit Card Fraud Dispute Letter

- Credit Card Unauthorized Transaction Letter

- Dispute Investigation Acknowledgment Letter

- Provisional Credit Issuance Letter

- Request For Additional Documentation Letter

- Merchant Chargeback Notification Letter

- Fraudulent Activity Claim Approval Letter

- Unauthorized Charge Claim Denial Letter

- Final Dispute Resolution Letter

- Compromised Account Closure Letter

- Identity Theft Victim Affidavit Letter

- Account Security Fraud Alert Letter

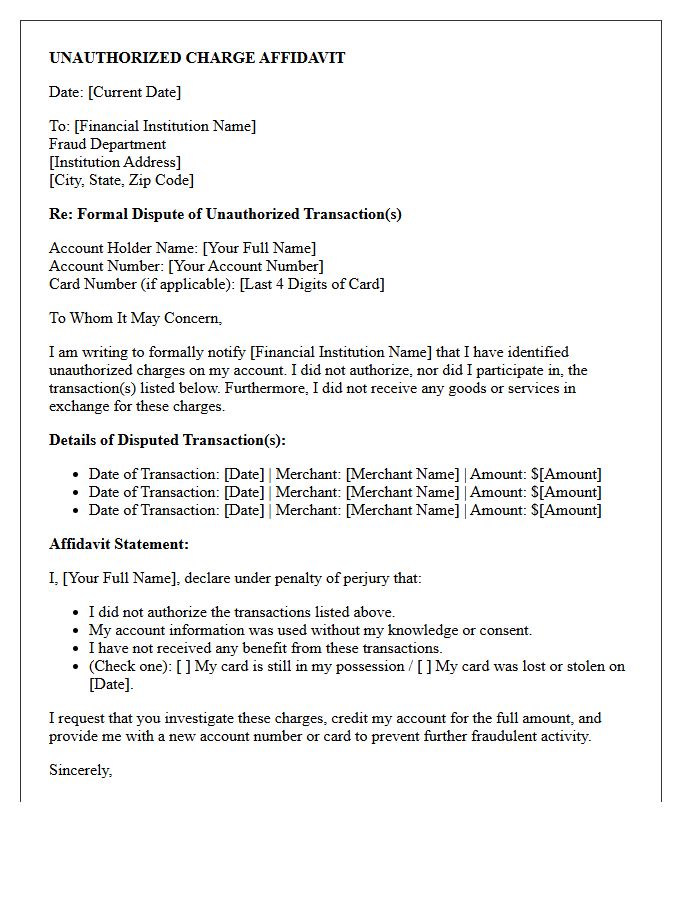

Unauthorized Charge Affidavit Letter

An Unauthorized Charge Affidavit Letter is a formal legal document used to dispute fraudulent transactions on your account. It serves as a sworn statement notifying your financial institution that specific debits were made without your consent. To ensure consumer protection under federal laws like the Electronic Fund Transfer Act, you must submit this written notice promptly. This letter provides a paper trail for investigations, helping you reclaim stolen funds and resolve billing errors. Always include transaction details, account numbers, and your signature to expedite the fraud investigation process effectively.

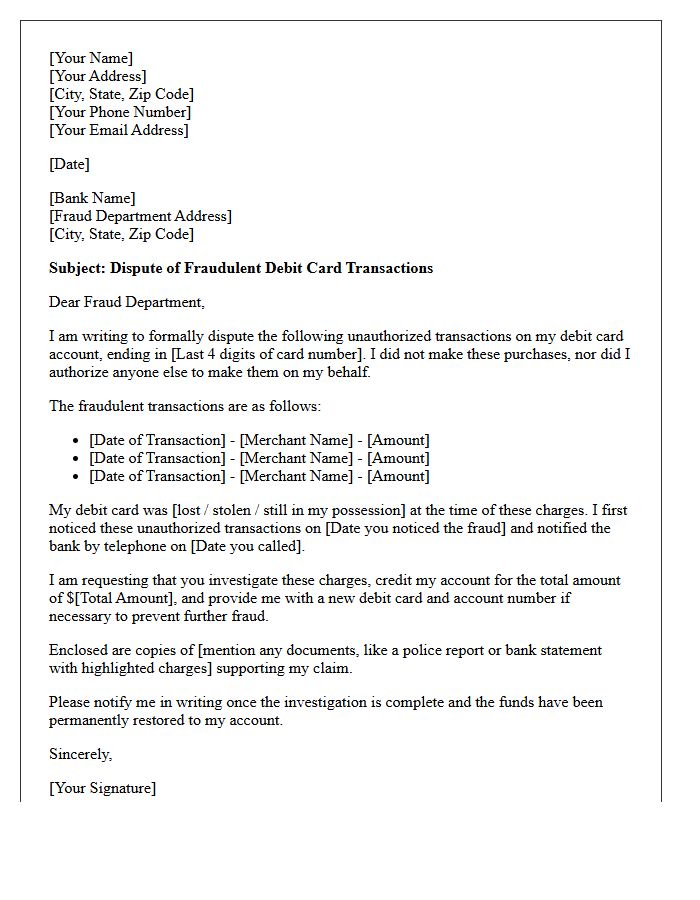

Debit Card Fraud Dispute Letter

A Debit Card Fraud Dispute Letter is a formal legal notification sent to your bank to report unauthorized transactions. To protect your rights under the Electronic Fund Transfer Act, you must submit this written notice within 60 days of the statement date. The letter should clearly list the disputed amounts, transaction dates, and a request for a reimbursement. Providing a detailed account helps initiate a formal investigation, ensuring the bank reviews the fraudulent activity and restores your missing funds promptly while maintaining a clear paper trail for legal protection.

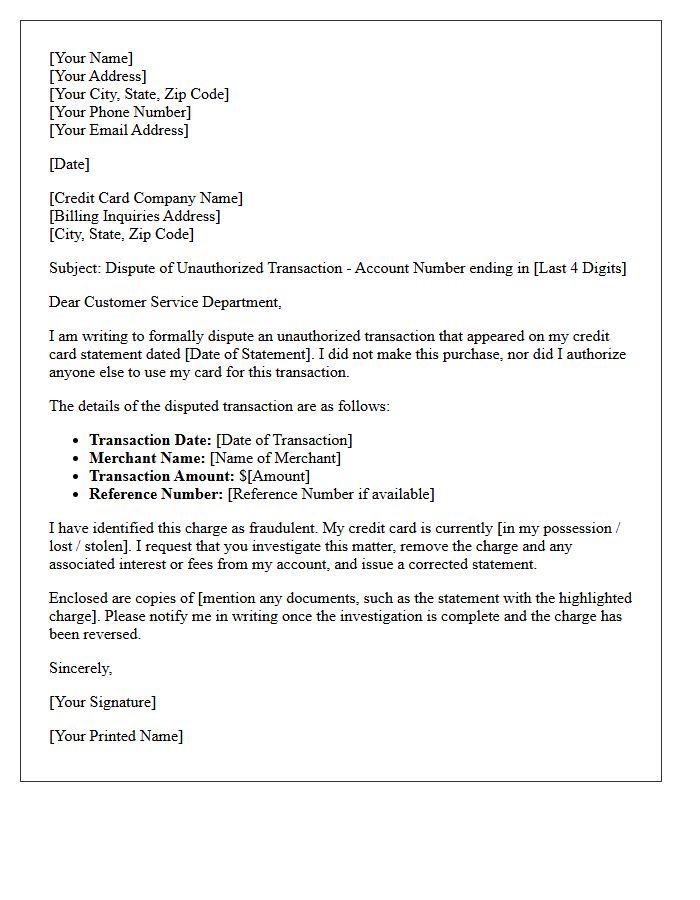

Credit Card Unauthorized Transaction Letter

A Credit Card Unauthorized Transaction Letter is a formal legal notification sent to your bank to dispute fraudulent charges. Under the Fair Credit Billing Act, you must submit this written notice within 60 days of the statement date to protect your consumer rights. Clearly state your account details, specify the exact disputed amount, and provide evidence that the transaction was not authorized. Sending this letter via certified mail ensures a paper trail, mandating the financial institution to investigate and resolve the error while limiting your potential liability for the theft.

Dispute Investigation Acknowledgment Letter

A Dispute Investigation Acknowledgment Letter is a formal notice sent by a credit bureau or financial institution confirming they have received your claim regarding reporting errors. This document is crucial because it triggers the legal timeframe, typically 30 days, mandated by the Fair Credit Reporting Act to complete an inquiry. It serves as verifiable proof that your dispute is being processed. Always retain this letter to track compliance and ensure your consumer rights are protected during the correction process of your financial records.

Provisional Credit Issuance Letter

A Provisional Credit Issuance Letter notifies a bank customer that temporary funds have been credited to their account during an ongoing ACH or card transaction dispute. This formal notice confirms that the financial institution is investigating a reported error or unauthorized charge. While the credit allows immediate access to funds, it remains temporary pending the final investigation outcome. If the claim is later denied, the bank reserves the right to reverse the credit, making it essential for customers to monitor their balance until the dispute is officially resolved.

Request For Additional Documentation Letter

A Request for Additional Documentation Letter is a formal notice issued by an entity, such as an insurance company or government agency, indicating that your initial submission is incomplete. It is crucial to respond promptly to avoid claim denials or processing delays. Always provide the specific evidence requested, such as medical records or financial statements, to substantiate your case. Ensuring accuracy and meeting the stated deadline are the most important steps to successfully resolving your application or inquiry.

Merchant Chargeback Notification Letter

A Merchant Chargeback Notification Letter is a formal alert from a payment processor informing a business that a customer has disputed a transaction. It is critical to review the specific reason code and deadline provided to respond effectively. Merchants must submit compelling evidence, such as delivery receipts or communication logs, to rebut the claim and recover lost revenue. Ignoring these notifications can lead to permanent financial loss and increased processing fees. Timely action is essential to maintain a healthy merchant account and protect your business against potential friendly fraud.

Fraudulent Activity Claim Approval Letter

A Fraudulent Activity Claim Approval Letter is an official document from a financial institution confirming that your dispute regarding unauthorized transactions was successful. It signifies that the bank has verified the identity theft or unauthorized access reported. Key details include the specific refund amount credited to your account and notice that any provisional credits have now been made permanent. Retain this letter as formal evidence that the fraudulent charges were legally cleared and your account security has been restored.

Unauthorized Charge Claim Denial Letter

An Unauthorized Charge Claim Denial Letter is a formal notice from a financial institution rejecting a request to reverse a disputed transaction. Banks typically deny claims if their investigation confirms authorized participation, insufficient evidence of fraud, or a failure to report the incident within legal timeframes. It is crucial to review the provided reason for denial and your right to appeal. Understanding the Fair Credit Billing Act can help you request specific documentation used in the decision to further contest the ruling and protect your consumer rights.

Final Dispute Resolution Letter

A Final Dispute Resolution Letter serves as the definitive legal notice concluding a disagreement between parties. This document outlines the final settlement terms, payment obligations, or closing actions required to resolve the conflict permanently. It is critical because it prevents future litigation by including a release of liability clause, ensuring both sides agree that the matter is fully settled. Always verify that the language is clear and legally binding before signing, as this formal communication marks the end of the dispute process and bars further claims related to the issue.

Compromised Account Closure Letter

A Compromised Account Closure Letter is a formal notification sent to security-breached users. It explains that an account was terminated to prevent unauthorized access and data theft. This document must clearly state the reason for closure, the date of the incident, and any necessary steps for identity protection. Providing contact information for support is essential to help users recover assets or open a new, secure account while ensuring compliance with privacy regulations and maintaining institutional trust during a digital security crisis.

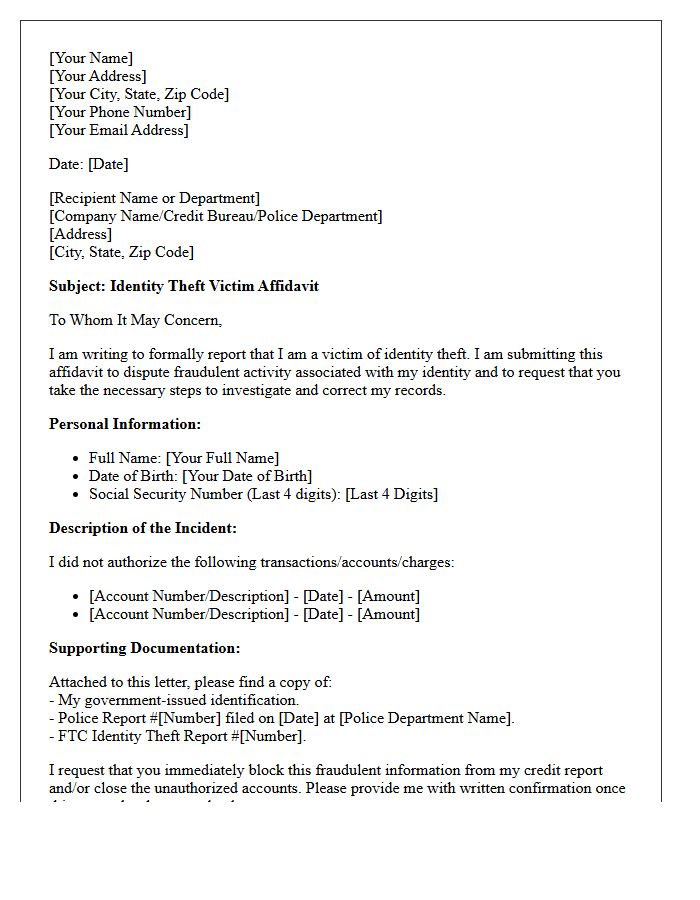

Identity Theft Victim Affidavit Letter

An Identity Theft Victim Affidavit Letter is a formal document used to report fraudulent activity to creditors and bureaus. This legal declaration asserts that you are not responsible for specific debts incurred by an imposter. To ensure it is effective, you must include a sworn statement, a copy of your police report, and detailed evidence of the disputed transactions. Filing this affidavit promptly is essential for restoring your credit and reclaiming your legal identity after a security breach.

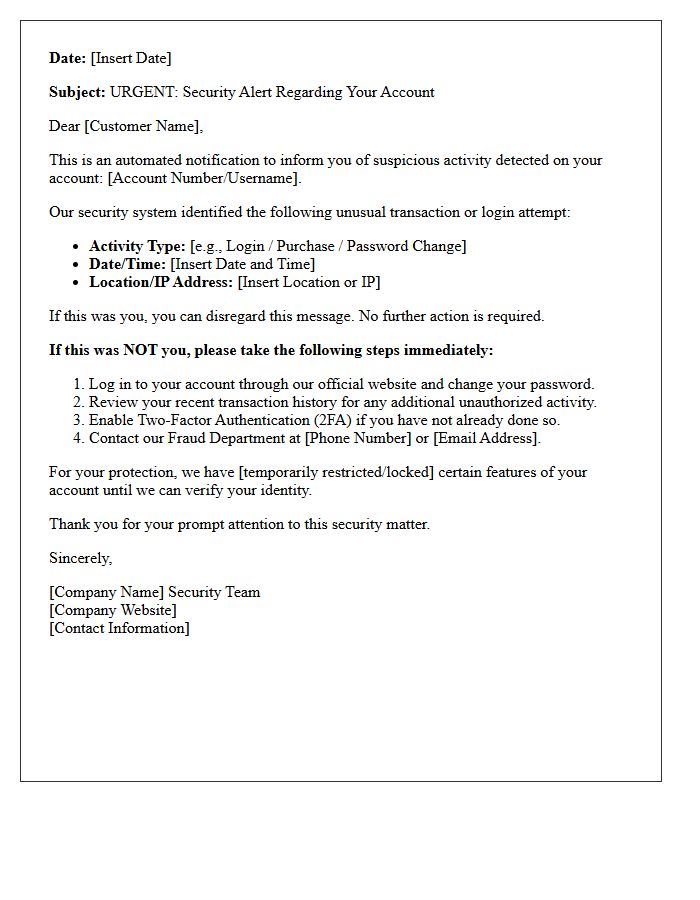

Account Security Fraud Alert Letter

An Account Security Fraud Alert Letter is a formal notification from a financial institution regarding suspicious activity. If you receive one, prioritize verifying its authenticity before clicking links to avoid phishing. Legitimate alerts never request your full password or PIN via email. Immediately contact your bank using the official number on your card to secure your identity and dispute unauthorized transactions. Prompt action is the most effective way to mitigate potential financial loss and ensure your sensitive personal data remains protected against unauthorized access or further exploitation.

What is an Unauthorized Charge Affidavit Letter?

An Unauthorized Charge Affidavit Letter is a formal, written statement used to dispute fraudulent transactions on a bank account or credit card. It serves as a legal declaration to your financial institution that specific charges were not authorized by you or any authorized user on your account.

What information should be included in a dispute letter for unauthorized charges?

A comprehensive affidavit should include your full name, account number, a detailed list of the fraudulent transactions (dates and amounts), a statement confirming you did not authorize the charges, and a formal request for a refund or reversal of the funds.

How soon should I send an affidavit letter after discovering fraud?

Under the Electronic Fund Transfer Act and the Fair Credit Billing Act, you should ideally report unauthorized charges within 60 days of the statement date. Sending your affidavit letter promptly via certified mail ensures you meet legal deadlines for liability protection.

Is an Unauthorized Charge Affidavit legally binding?

Yes, when signed and submitted to a financial institution, this document is a sworn statement. Providing false information on an affidavit can lead to legal consequences, including perjury charges or the permanent closure of your bank accounts.

Should I notarize my Unauthorized Charge Affidavit Letter?

While not always required by every bank, having your affidavit notarized adds a layer of legal credibility and is often requested for high-value fraud claims. Check with your specific financial institution's fraud department to see if they require a notarized signature to process the dispute.

Comments