Receiving a Hardship Forbearance Account Closure Notice indicates that your temporary payment relief period has ended or the account has been permanently closed due to specific policy terms. Understanding the implications for your credit and future repayment is essential for financial recovery. This guide explains your options and next steps. Below are some ready to use templates.

Image cover: Navigating Hardship Forbearance: Official Account Closure Notice Templates and Guide

Letter Samples List

- Notice of Account Closure Following Hardship Forbearance Expiration Letter

- Final Account Closure and Forbearance Termination Notice Letter

- Hardship Forbearance Exhaustion and Account Closure Letter

- Unresolved Financial Hardship Forbearance Closure Notice Letter

- Medical Hardship Forbearance Account Closure Notification Letter

- Permanent Account Closure Post Hardship Forbearance Letter

- Defaulted Hardship Forbearance Account Closure Warning Letter

- Pre-Closure Notification for Hardship Forbearance Account Letter

- Post-Forbearance Hardship Account Settlement and Closure Letter

- Involuntary Account Closure Due to Hardship Forbearance Letter

- Hardship Forbearance Period End Account Closure Notice Letter

- Approved Hardship Debt Forgiveness and Account Closure Letter

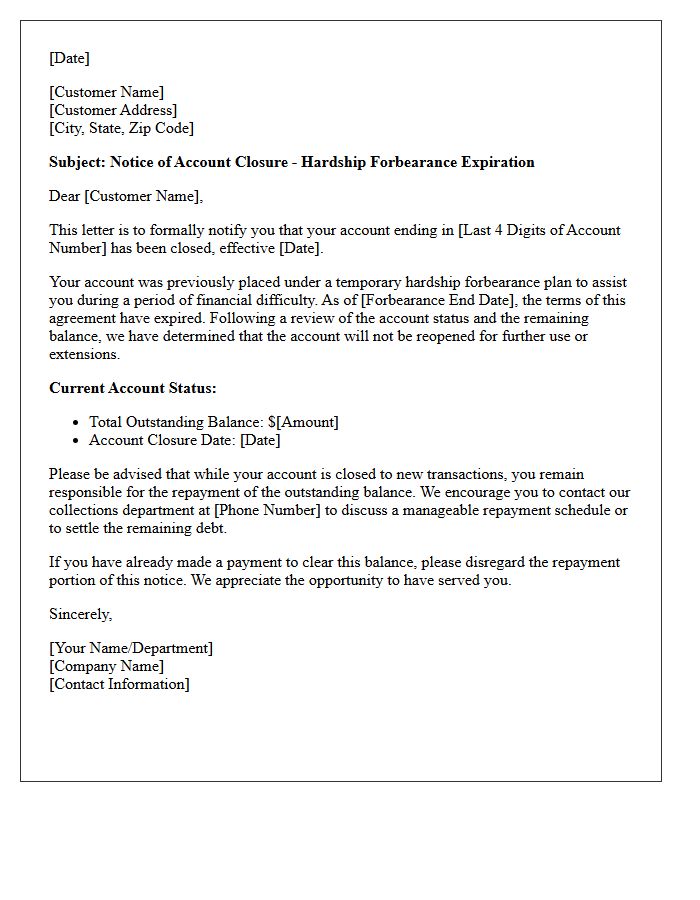

Notice of Account Closure Following Hardship Forbearance Expiration Letter

A Notice of Account Closure Following Hardship Forbearance Expiration is a formal notification sent when a temporary relief period ends without a viable repayment solution. This letter signifies that the creditor is permanently terminating your charging privileges. It is crucial to review the final repayment terms and understand the impact on your credit score. To avoid further legal action or debt collection, you must address the remaining outstanding balance immediately according to the specified deadline. Contact your lender to discuss potential settlement options or alternative payment arrangements before the closure is finalized.

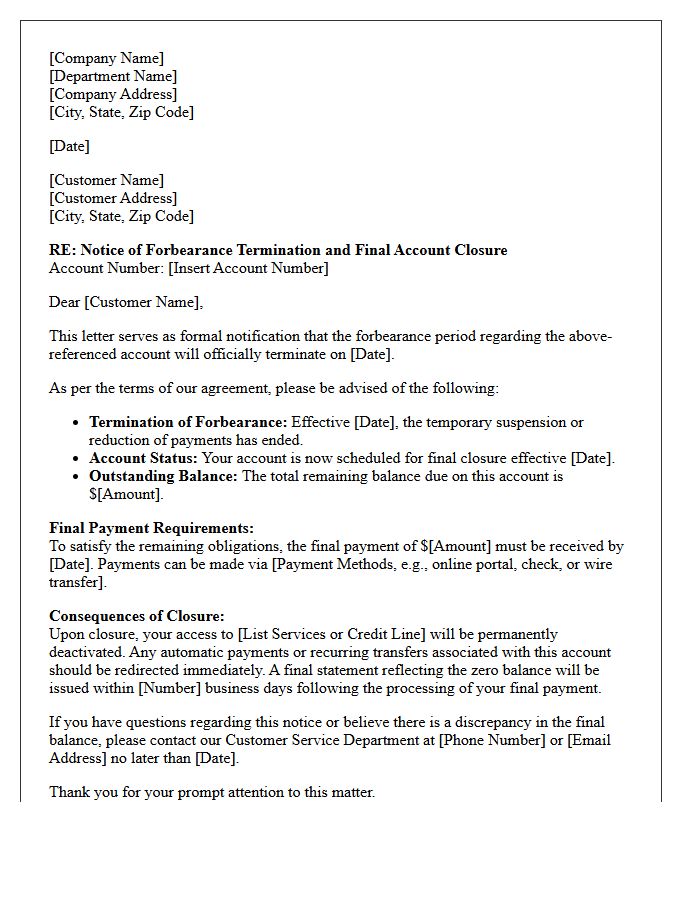

Final Account Closure and Forbearance Termination Notice Letter

The Final Account Closure and Forbearance Termination Notice Letter is a critical legal document signaling the end of temporary payment relief. It informs borrowers that their forbearance period has expired and outstanding balances must now be addressed. Recipients must immediately review repayment options, such as loan modification or deferral, to avoid delinquency. Failure to act upon receiving this notice can lead to foreclosure or permanent account termination. Prioritizing communication with your servicer is essential to protect your credit standing and ensure long-term financial stability during this transition.

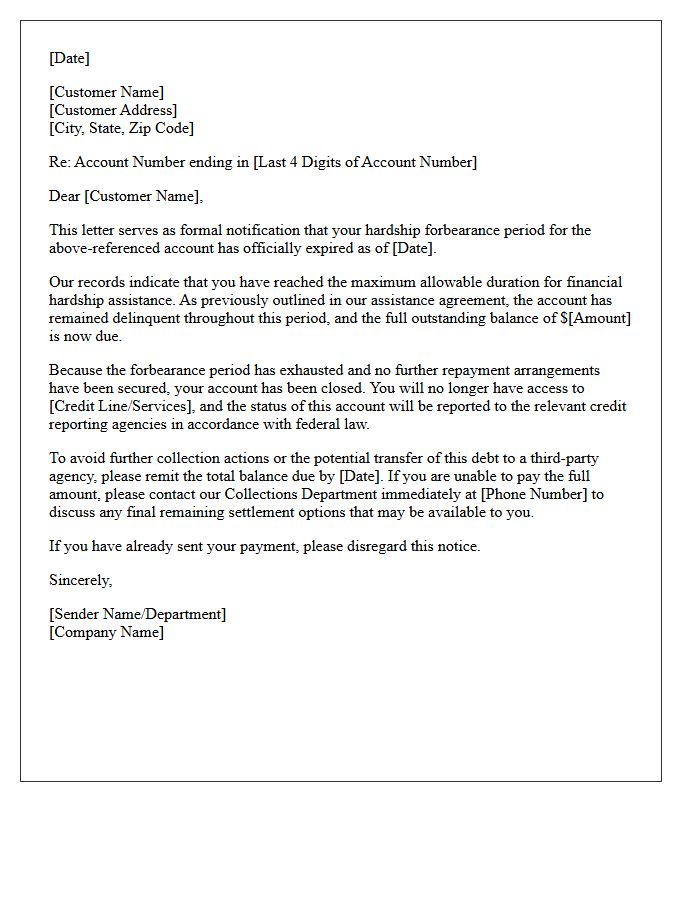

Hardship Forbearance Exhaustion and Account Closure Letter

Receiving a Hardship Forbearance Exhaustion and Account Closure Letter indicates your temporary relief period has ended and the creditor is permanently terminating your credit line. This occurs when you have reached the maximum allowable time for reduced payments without returning to standard terms. The account closure prevents further charges while you enter a final repayment phase. It is critical to contact your lender immediately to discuss long-term debt restructuring or settlement options to avoid default and minimize negative impacts on your credit score.

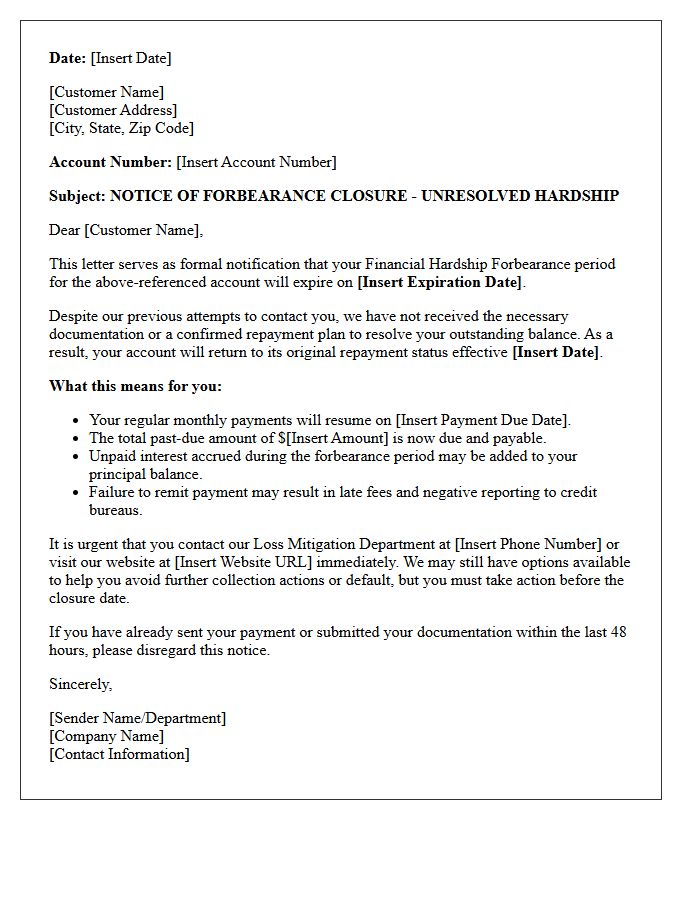

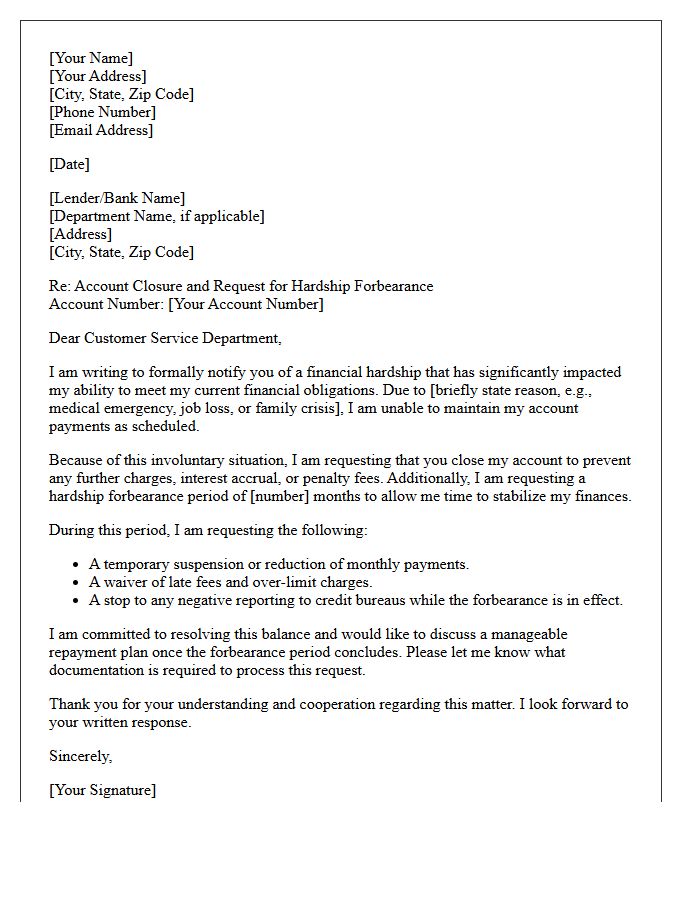

Unresolved Financial Hardship Forbearance Closure Notice Letter

An Unresolved Financial Hardship Forbearance Closure Notice Letter officially informs a borrower that their temporary payment relief period has ended without a permanent resolution. Receiving this mandatory notification means your account will return to regular billing status, and any deferred balance may become due. It is critical to contact your servicer immediately to discuss repayment options, such as loan modification or extension, to avoid delinquency. Ignoring this notice can lead to negative credit reporting or foreclosure, so proactive communication is essential to protect your financial standing.

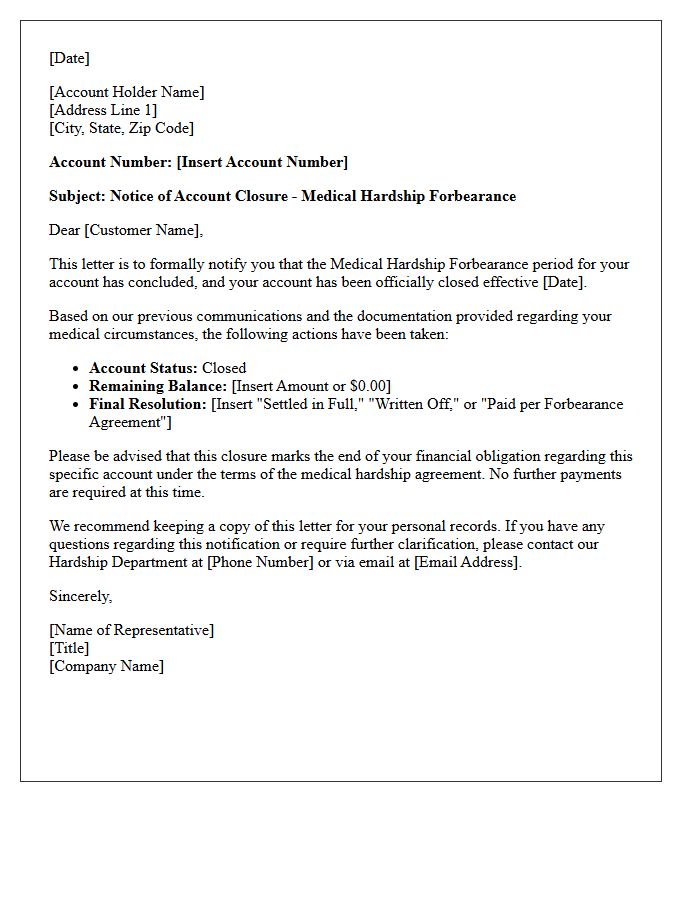

Medical Hardship Forbearance Account Closure Notification Letter

A Medical Hardship Forbearance Account Closure Notification Letter informs borrowers that their temporary payment relief has ended due to account closure or expiration. It is crucial to understand that interest accrual typically continues during forbearance, potentially increasing the total balance. Upon receiving this notice, you must immediately coordinate with your loan servicer to select a new repayment plan. Failure to act can lead to delinquency or default. Always verify the remaining balance and the effective date of the next scheduled payment to maintain financial stability after a medical crisis.

Permanent Account Closure Post Hardship Forbearance Letter

A Permanent Account Closure Post Hardship Forbearance Letter notifies borrowers that their credit line is being terminated following a temporary relief period. Receiving this notice means the lender has decided to permanently close the account to mitigate risk, even if payments have resumed. This action often results from the initial financial instability that triggered the forbearance. It is crucial to understand that while the debt may be settled or restructured, the loss of available credit can impact your credit score and overall financial profile moving forward.

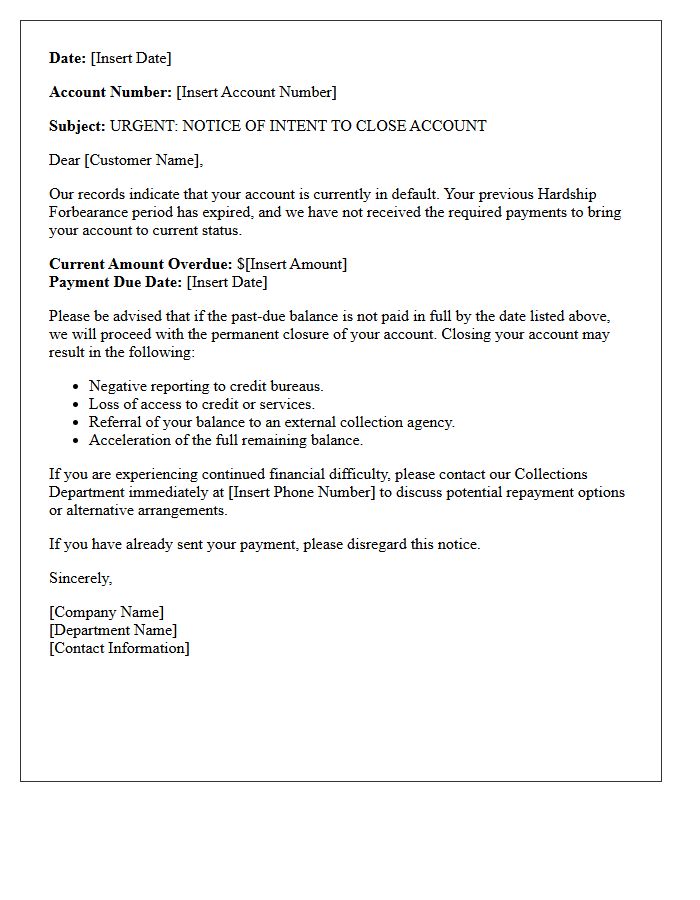

Defaulted Hardship Forbearance Account Closure Warning Letter

A Defaulted Hardship Forbearance Account Closure Warning Letter is a formal notice indicating that your temporary payment relief has ended without a resolution. Receiving this means your account is at immediate risk of permanent closure and being sent to collections. This status severely damages your credit score and eliminates future flexible repayment options. To prevent final termination, you must contact your creditor instantly to negotiate a reinstatement plan or settlement. Ignoring this final warning typically leads to legal action or the total loss of account privileges and financial standing.

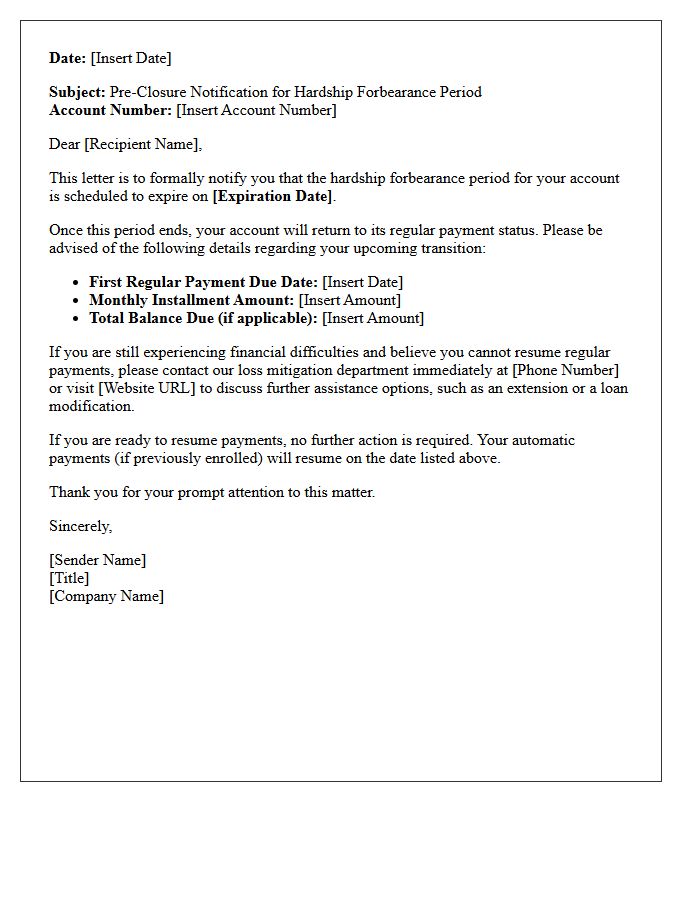

Pre-Closure Notification for Hardship Forbearance Account Letter

A Pre-Closure Notification for a hardship forbearance account is a critical legal alert sent before your temporary payment relief ends. This letter outlines the exact reinstatement date when regular billing resumes. It is essential to review the document for updated repayment terms, potential balloon payments, or loan modification options. Failing to respond or prepare for the expiration of forbearance can lead to immediate delinquency or foreclosure proceedings. Always contact your servicer promptly to discuss a repayment plan or extension to protect your financial standing and credit score.

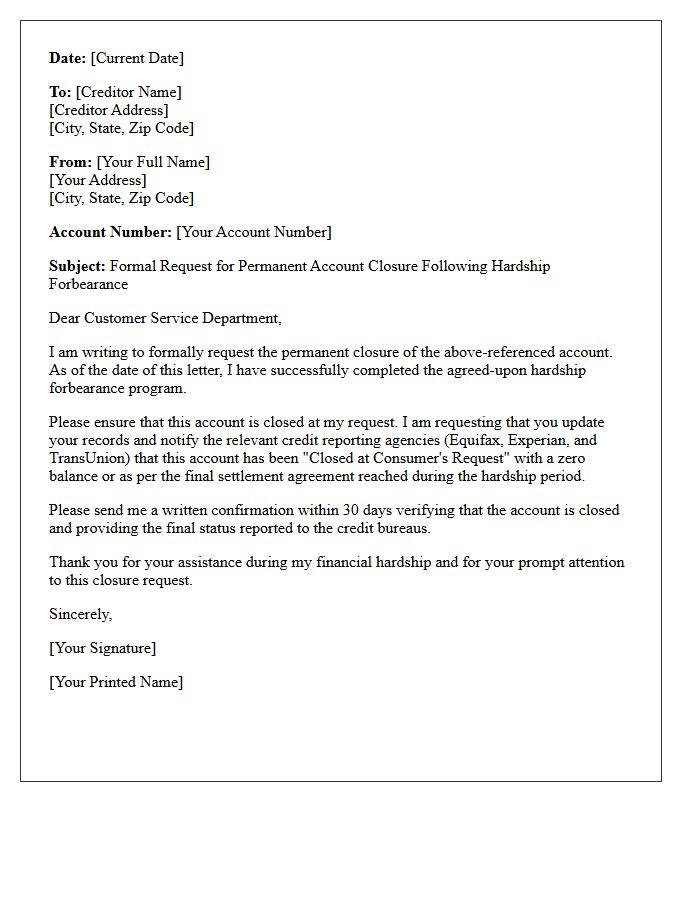

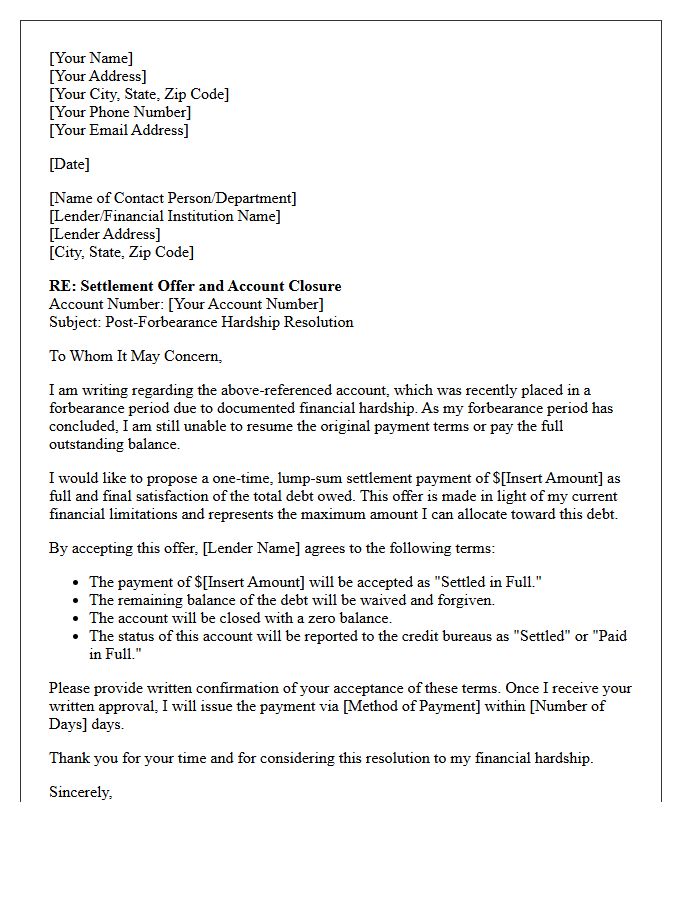

Post-Forbearance Hardship Account Settlement and Closure Letter

A Post-Forbearance Hardship Account Settlement and Closure Letter is a legal document confirming you have successfully resolved delinquent debt following a financial grace period. This letter provides written proof that the creditor accepted a final payment to satisfy the balance, preventing further collection efforts. It is essential for verifying your account status with credit bureaus to improve your credit score. Always retain this record to ensure your financial obligations are permanently closed and to protect against future disputes regarding the settled deficiency balance.

Involuntary Account Closure Due to Hardship Forbearance Letter

An involuntary account closure following a hardship forbearance letter typically occurs when a lender determines that your financial instability poses a long-term risk. While forbearance provides temporary payment relief, many credit card issuers include clauses allowing them to revoke borrowing privileges to mitigate potential losses. This action can negatively impact your credit score by reducing available credit and increasing your utilization ratio. It is essential to communicate with your creditor to understand if the closure is permanent or if the account can be reinstated after completing the assistance program.

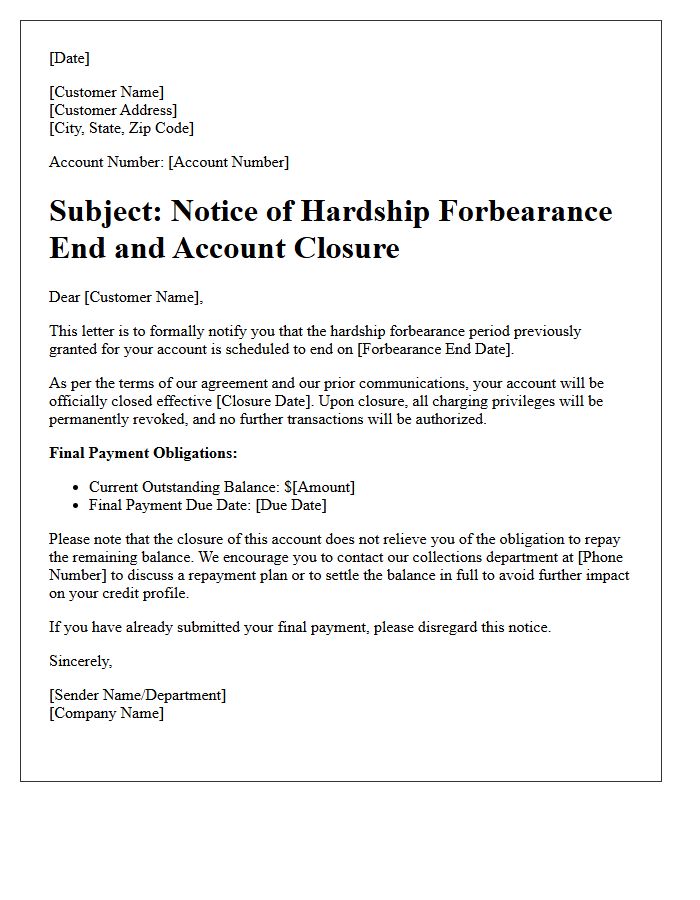

Hardship Forbearance Period End Account Closure Notice Letter

Receiving a Hardship Forbearance Period End Account Closure Notice signifies that your temporary payment relief has expired. This formal communication warns that without immediate action or a repayment plan, your account faces permanent closure. It is critical to contact your creditor to discuss extension options or settlement terms to prevent severe credit score damage. Failure to resolve the balance post-forbearance often leads to debt collection or legal action. Always review the specific deadline mentioned in the letter to preserve your financial standing and avoid involuntary account termination.

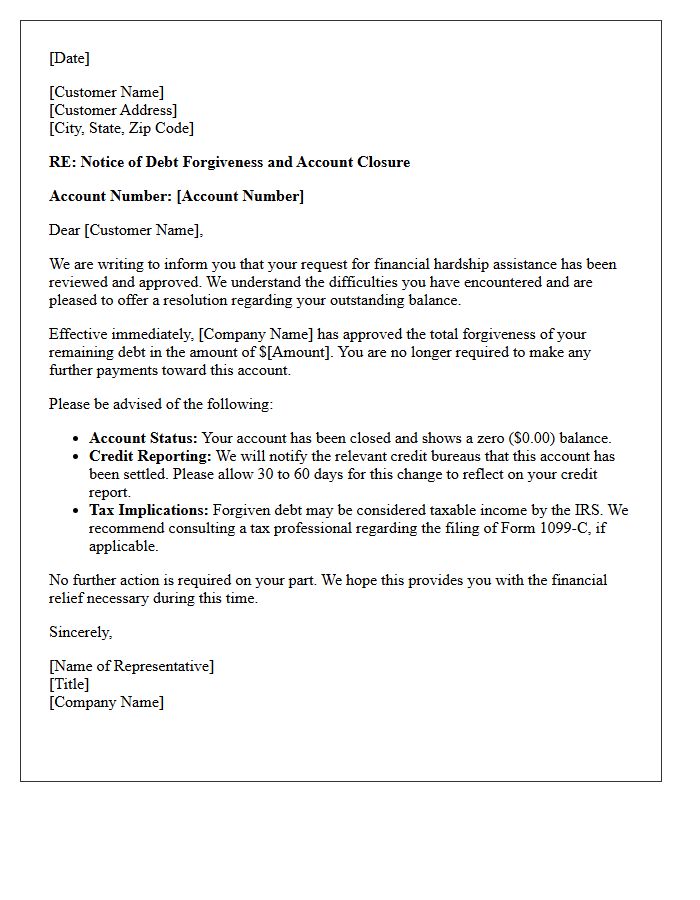

Approved Hardship Debt Forgiveness and Account Closure Letter

An Approved Hardship Debt Forgiveness and Account Closure Letter serves as official legal confirmation that a creditor has canceled your outstanding balance due to financial distress. This document is vital because it proves the debt is legally settled, preventing future collection attempts. It typically signifies that the account is closed and cannot be used again. Ensure you retain this letter for your records, as the forgiven amount may be considered taxable income by the IRS, and you must verify that your credit report accurately reflects the zero balance.

What is a Hardship Forbearance Account Closure Notice?

A Hardship Forbearance Account Closure Notice is a formal notification sent by a creditor or lender stating that your account will be closed to further charges while you are enrolled in a financial hardship program. This action is often a requirement for lowering interest rates or establishing a fixed repayment plan during periods of financial instability.

Does entering a hardship forbearance plan always result in account closure?

In most cases, yes. To prevent the accumulation of additional debt while providing relief benefits like reduced payments or waived fees, lenders typically close the line of credit permanently or suspend charging privileges until the balance is paid in full.

How does an account closure due to hardship forbearance affect my credit score?

The closure of an account can impact your credit score by reducing your total available credit and potentially shortening your average age of accounts. Additionally, while the "forbearance" status itself may be noted on your report, it is generally less damaging than a series of missed payments or a charge-off.

Can I reopen my account after completing the hardship forbearance program?

Most accounts closed under a hardship agreement are closed permanently and cannot be reopened. Once the balance is paid off, you may need to reapply for a new line of credit, subject to the lender's current underwriting criteria and your updated credit profile.

Will a hardship account closure stop interest from accruing?

While the notice confirms that you can no longer make new purchases, interest may still accrue unless your specific forbearance agreement includes an interest rate reduction or a total interest waiver. Review your notice carefully to see the specific terms applied to your remaining balance.

Comments