Protect your organization by issuing a formal Response to Fraudulent Account Dispute Notice. This essential document verifies claim details, outlines investigation results, and clarifies the account's status to resolve identity theft or unauthorized activity claims efficiently. Maintaining clear records ensures legal compliance and protects consumer rights. To help you draft a professional reply quickly, below are some ready to use template.

Image cover: Professional Templates: Formal Responses to Fraudulent Account Disputes

Letter Samples List

- Acknowledgment of Fraudulent Account Dispute Letter

- Request for Identity Theft Report Letter

- Fraud Affidavit Request Letter

- Suspension of Collection Activities Letter

- Confirmation of Account Closure Due to Fraud Letter

- Credit Bureau Tradeline Deletion Notice Letter

- Rejection of Fraud Dispute Due to Insufficient Evidence Letter

- Request for Additional Fraud Investigation Information Letter

- Investigation Conclusion and Debt Validation Letter

- Original Creditor Fraud Claim Notification Letter

- Account Return to Original Creditor Letter

- Fraud Dispute File Closure Letter

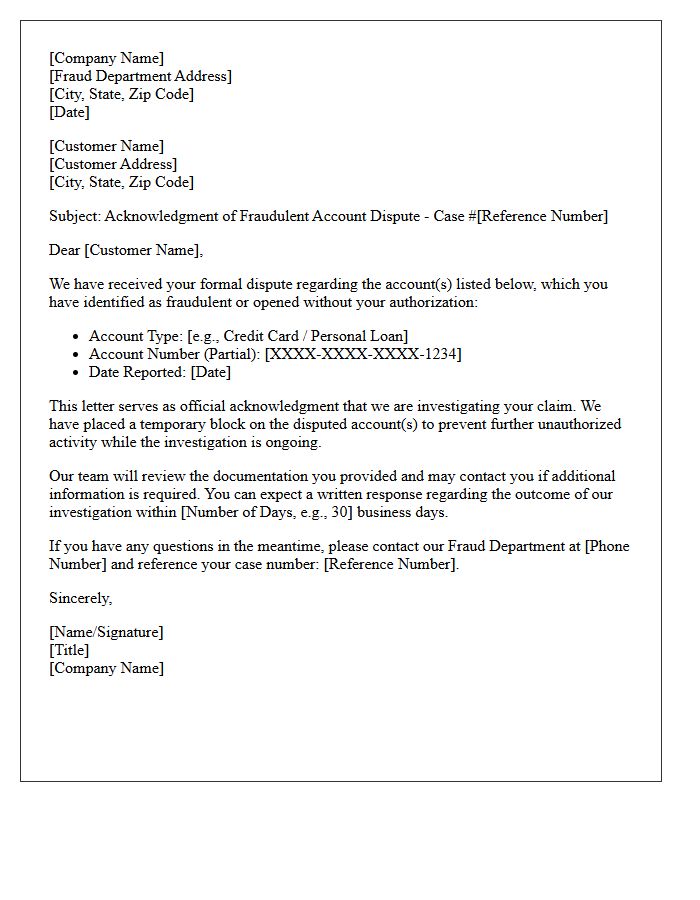

Acknowledgment of Fraudulent Account Dispute Letter

An Acknowledgment of Fraudulent Account Dispute Letter is a formal document issued by a financial institution or credit bureau confirming they have received your identity theft claim. This letter is crucial because it initiates the legal investigation period required under the Fair Credit Reporting Act. It serves as your official proof of filing, ensuring the organization must investigate and respond within specific timelines. Always retain this receipt to protect your rights, track the case progress, and provide evidence if you need to escalate the dispute to regulatory authorities or legal counsel.

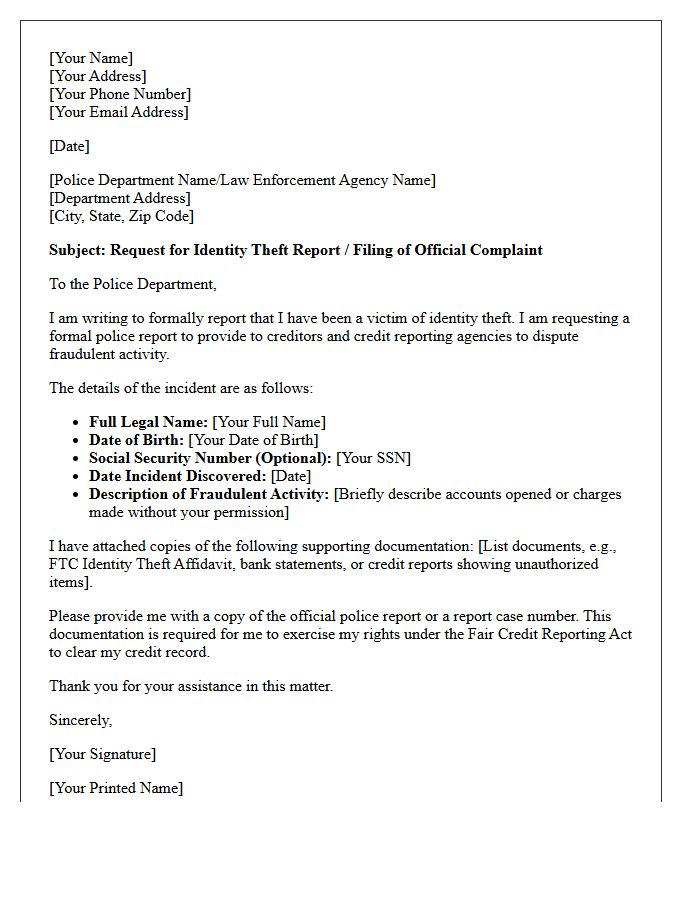

Request for Identity Theft Report Letter

A Request for Identity Theft Report Letter is a formal document sent to law enforcement to document fraudulent activity. It serves as essential legal evidence when disputing unauthorized transactions with creditors or credit bureaus. To be effective, the letter must include your full contact details, a summary of the compromised accounts, and a sworn statement of the facts. Having an official police report is the most critical step in restoring your financial integrity and exercising your rights under the Fair Credit Reporting Act to remove inaccurate data from your profile.

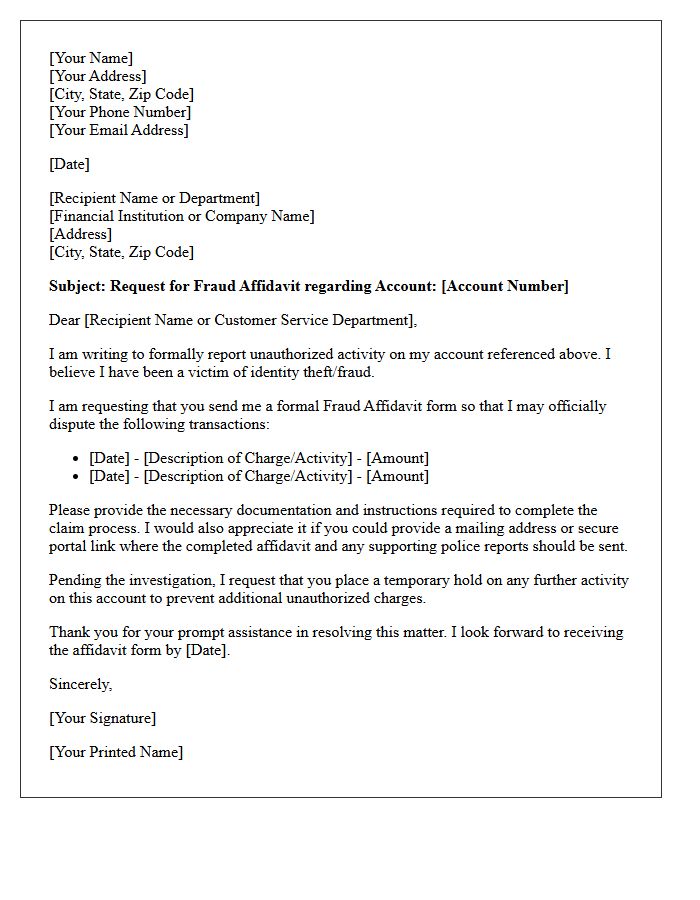

Fraud Affidavit Request Letter

A Fraud Affidavit Request Letter is a formal document sent to a financial institution to initiate an identity theft investigation. This written notice disputes unauthorized transactions and provides a legal statement under penalty of perjury. It is essential to include specific account details and police report numbers to validate your claim. Sending this letter via certified mail ensures a paper trail for the recovery process, helping you restore credit and secure your financial identity against further malicious activity.

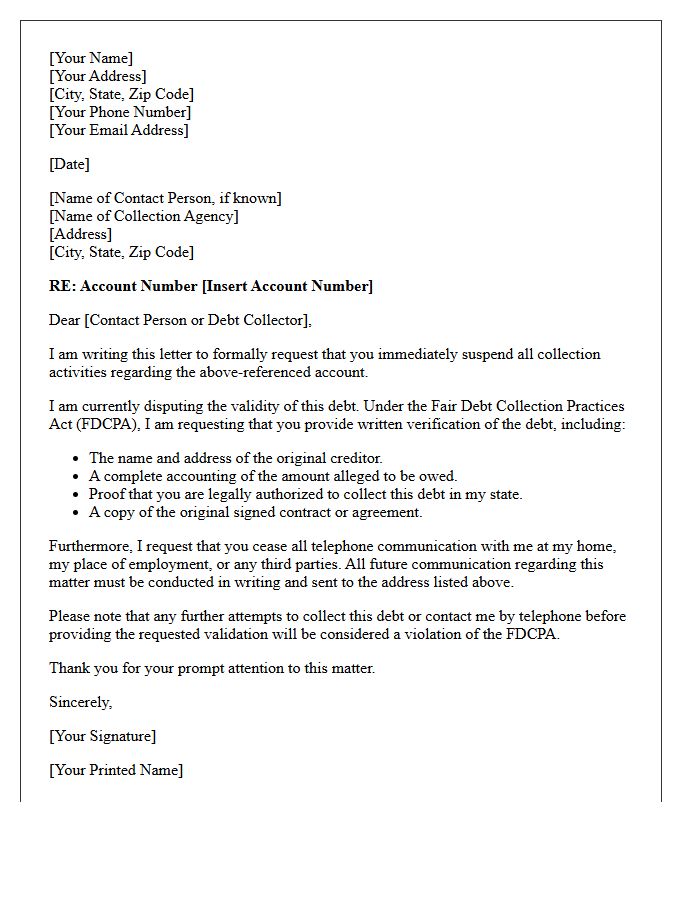

Suspension of Collection Activities Letter

A Suspension of Collection Activities Letter is a formal notice confirming that a creditor or agency has temporarily paused recovery efforts. This occurs during a dispute process or while verifying debt details. It provides legal protection by stopping hounding calls and enforcement actions until the investigation concludes. It is crucial to retain this document as proof that your account status is currently protected under consumer rights. Always ensure the letter specifies the duration of the hold and the next steps required to resolve the outstanding balance permanently.

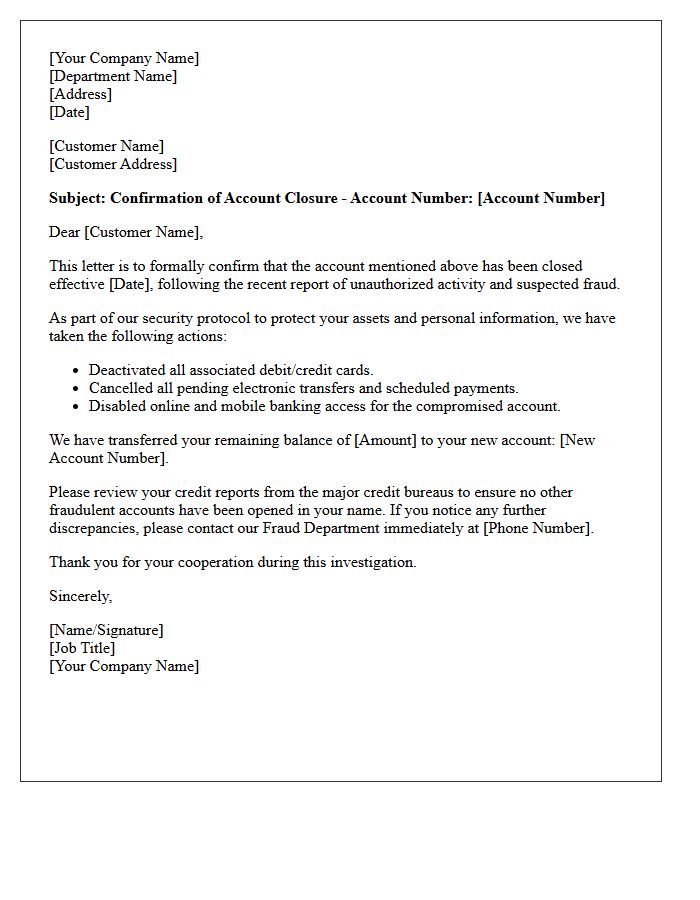

Confirmation of Account Closure Due to Fraud Letter

A Confirmation of Account Closure Due to Fraud letter is a critical legal document verifying that a compromised account has been permanently terminated. It serves as official proof that you are no longer liable for unauthorized transactions occurring after the closure date. This notification confirms that the institution has completed its security investigation and secured your personal data. Always retain this letter for your records to resolve future credit reporting inaccuracies and to protect your financial identity during the recovery process following identity theft or fraudulent activity.

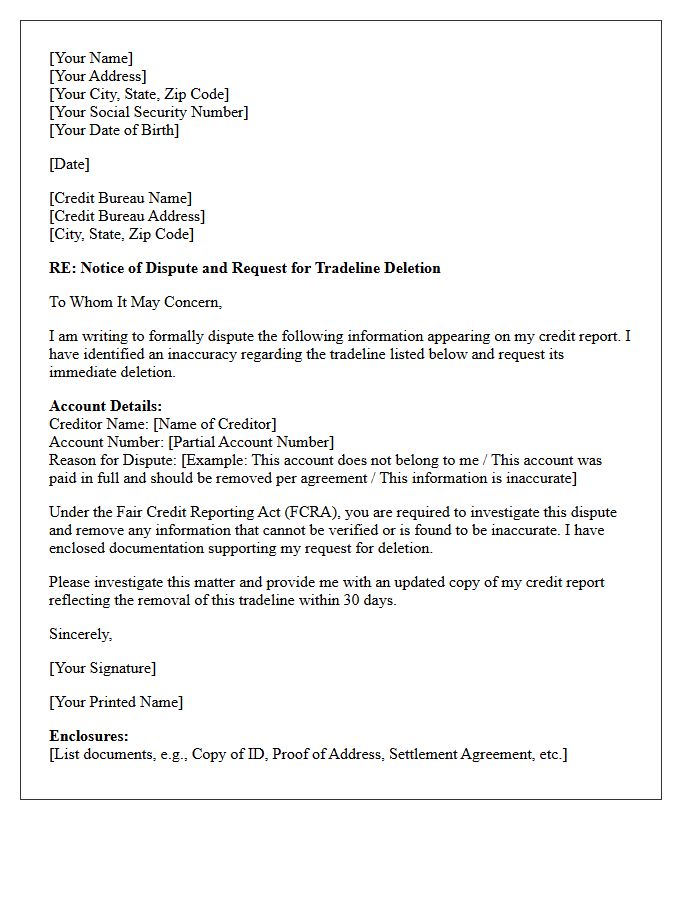

Credit Bureau Tradeline Deletion Notice Letter

A Credit Bureau Tradeline Deletion Notice Letter is a formal document confirming that a specific account has been permanently removed from your credit report. This notice is essential for verifying that inaccurate, outdated, or disputed information is no longer affecting your credit score. Always retain this letter as legal proof of the update, as it ensures the bureau has complied with the Fair Credit Reporting Act. Validating these deletions helps maintain an accurate financial profile and facilitates better loan approvals and interest rates in the future.

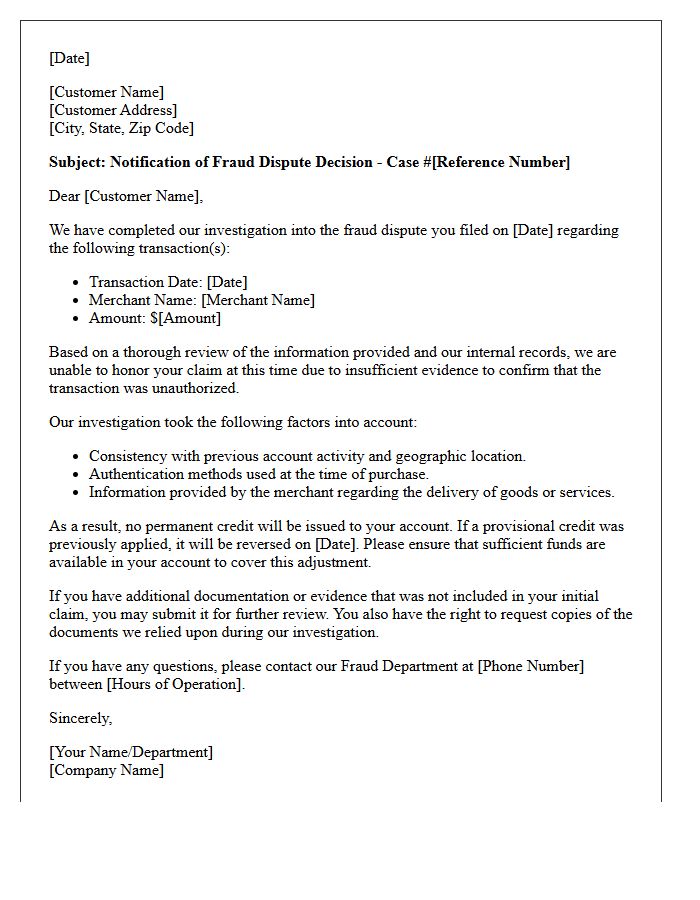

Rejection of Fraud Dispute Due to Insufficient Evidence Letter

Receiving a letter stating your fraud dispute was rejected due to insufficient evidence means the financial institution found no clear proof of unauthorized activity. To challenge this, you must promptly provide additional documentation, such as police reports, communication logs, or identity theft affidavits. Review the bank's specific reasoning to address their concerns directly. Strict federal timelines apply to appeals, so acting quickly is essential to protect your consumer rights and potentially reverse the decision. Always maintain detailed records of all transactions and correspondence to strengthen your case during the reconsideration process.

Request for Additional Fraud Investigation Information Letter

A Request for Additional Fraud Investigation Information Letter is a formal notification sent by financial institutions to clarify suspicious activity. When receiving this, it is crucial to provide accurate evidence promptly to protect your account. The document typically asks for transaction details, identification, or affidavits to support your claim. Responding thoroughly ensures a timely resolution of the inquiry and helps mitigate potential financial loss. Always verify the sender's authenticity before sharing sensitive data to avoid phishing scams during the investigation process.

Investigation Conclusion and Debt Validation Letter

When an investigation concludes, creditors must provide a Debt Validation Letter to confirm the debt's legitimacy. This document is crucial because it serves as legal proof that you owe the specific amount to the named collector. Under the Fair Debt Collection Practices Act, you have the right to dispute inaccuracies within thirty days. Reviewing this letter ensures your financial records are accurate and protects you from fraudulent claims or expired debts. Always keep a copy of this correspondence to maintain your consumer rights during the credit repair process.

Original Creditor Fraud Claim Notification Letter

An Original Creditor Fraud Claim Notification Letter is a formal document sent to a lending institution to report unauthorized accounts or transactions. It serves as essential legal notice under the Fair Credit Reporting Act, requiring the creditor to investigate identity theft claims. When submitting this letter, include specific account details and an identity theft report to ensure your consumer rights are protected. Timely notification is critical to dispute fraudulent debts, prevent further credit damage, and halt collection activities while the financial institution verifies the identity theft claim.

Account Return to Original Creditor Letter

An Account Return to Original Creditor Letter is a formal request sent to a collection agency to stop their pursuit of a debt. This letter demands that the agency cease collections and transfer the account back to the primary lender. It is a strategic tool used when a third party cannot provide debt validation or when you prefer negotiating directly with the original source. Successfully returning the account can help you protect your credit score and simplify the settlement process by dealing with the entity that initially issued the credit.

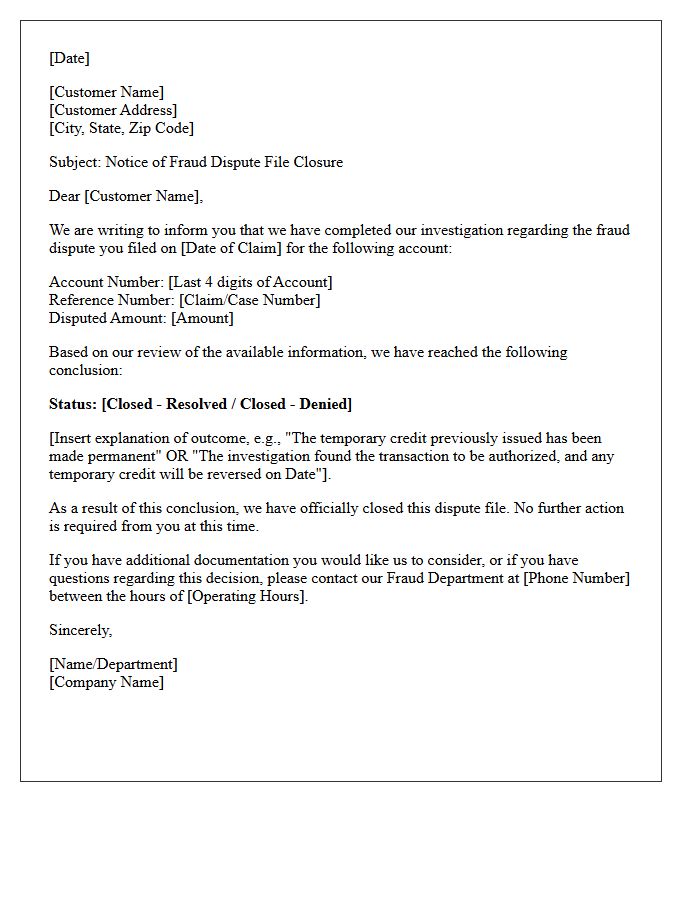

Fraud Dispute File Closure Letter

A Fraud Dispute File Closure Letter is a formal notification from a financial institution confirming the end of an investigation. It is crucial to review the final resolution to understand if the claim was approved or denied. If the bank denies the claim, the letter must outline the specific reasons and evidence used. Always verify your account balance and credit report after receiving this document to ensure all unauthorized charges were successfully reversed. Retain this letter as permanent legal proof of the dispute's outcome and your proactive steps against identity theft.

What is a Fraudulent Account Dispute Notice?

A Fraudulent Account Dispute Notice is a formal notification sent by a consumer to a financial institution or credit bureau stating that a specific account was opened using their identity without authorization. This document initiates a formal investigation under the Fair Credit Reporting Act (FCRA) or the Electronic Fund Transfer Act (EFTA).

How should a bank respond to a reported fraudulent account?

Upon receiving a dispute notice, the institution must immediately place a temporary freeze on the account, conduct a thorough internal investigation, and provide a written response within 10 to 30 business days. The response must confirm whether the account has been closed, if the fraudulent debt has been cleared, and if the negative information has been removed from credit reports.

What documentation is required to resolve a fraudulent account dispute?

To process a response to a dispute, the institution typically requires a completed Identity Theft Affidavit, a copy of a formal police report, and valid government-issued identification. Providing these documents ensures the bank can verify the claim and expedite the removal of the unauthorized account from the victim's record.

What happens if the bank denies a fraudulent account dispute?

If the investigation concludes that the account is valid, the institution will issue a denial notice explaining the evidence used to reach that decision. If the consumer disagrees, they have the right to request all documents used in the investigation and can file a secondary appeal or a complaint with the Consumer Financial Protection Bureau (CFPB).

Will a fraudulent account dispute affect my credit score?

While the dispute process is ongoing, the account may be marked as "disputed" on credit reports, which can temporarily impact credit scoring. However, once the institution confirms the fraud and instructs the credit bureaus to delete the account, any negative impact associated with that specific fraudulent account should be fully removed.

Comments