A Final Demand Notice is the last formal warning issued to a debtor before a creditor initiates asset repossession. This critical document outlines outstanding debts and provides a final deadline to prevent legal seizure of property. Understanding your rights and responsibilities is essential to resolving the delinquency. To help you take immediate action, below are some ready to use template.

Image cover: Official Final Demand Notice Before Asset Repossession: Templates and Compliance Guide

Letter Samples List

- Final Demand Letter Prior to Asset Repossession

- Last Notice and Asset Repossession Warning Letter

- Pre-Repossession Final Demand Collection Letter

- Urgent Letter of Final Demand for Collateral Surrender

- Asset Recovery and Final Repossession Notice Letter

- Default Notice and Final Repossession Demand Letter

- Final Warning Letter Before Involuntary Asset Repossession

- Secured Debt Final Demand and Repossession Letter

- Notice of Intent to Repossess Final Demand Letter

- Delinquent Account Final Repossession Action Letter

- Final Collection Letter Before Collateral Repossession

- Voluntary Surrender or Repossession Final Demand Letter

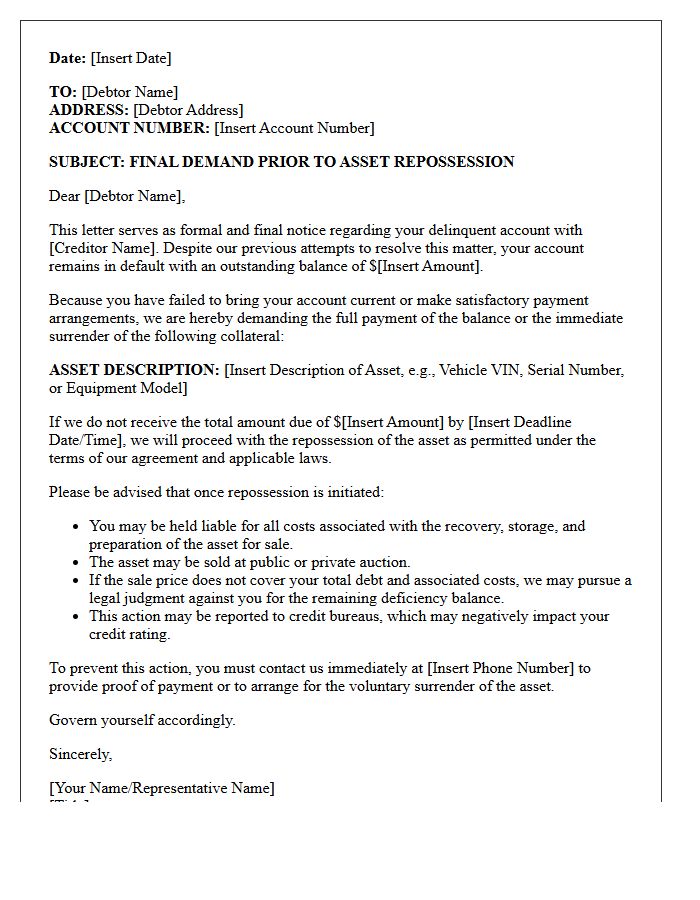

Final Demand Letter Prior to Asset Repossession

A final demand letter is a critical legal notice issued by creditors before initiating the seizure of collateral. It serves as the ultimate warning, detailing the outstanding debt, specific breach of contract, and a strict deadline for payment. Failure to resolve the arrears or surrender the property by the specified date allows the lender to commence asset repossession procedures. Receiving this document signifies that your window for negotiation is closing, making it essential to contact the financial institution immediately to discuss potential settlements or restructuring to avoid the loss of your property.

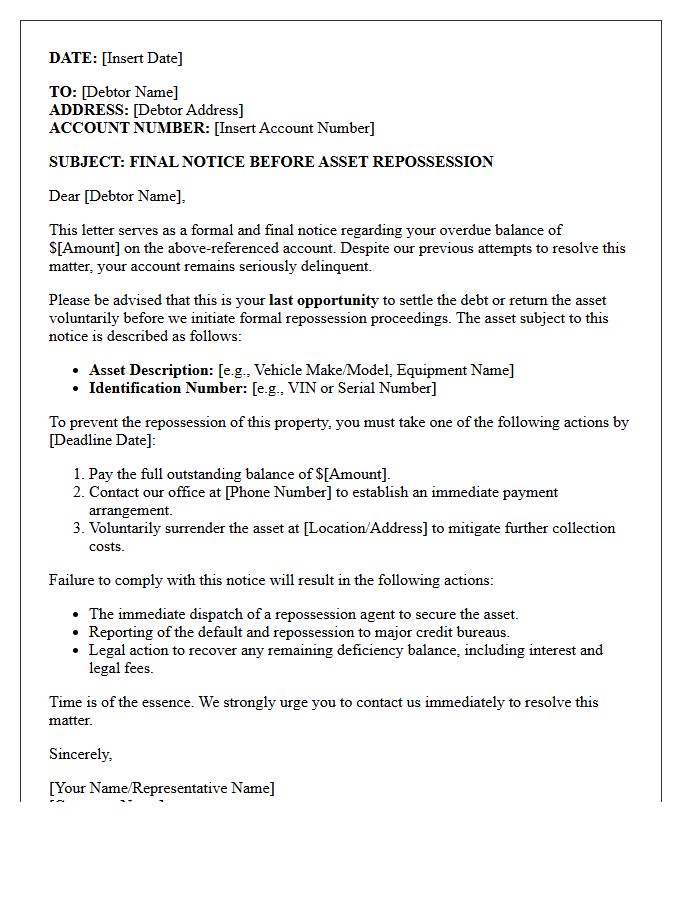

Last Notice and Asset Repossession Warning Letter

A Last Notice and Asset Repossession Warning Letter is a final legal communication demanding immediate payment of overdue debt. This formal document notifies the borrower that the lender intends to seize collateral, such as a vehicle or property, to recover losses. Receiving this notice indicates that the grace period has expired and legal action is imminent. To prevent asset repossession and severe credit damage, the recipient must urgently contact the creditor to settle the balance or negotiate an alternative repayment plan before the specified deadline.

Pre-Repossession Final Demand Collection Letter

A Pre-Repossession Final Demand Collection Letter is the last formal notification sent to a debtor before a lender seizes collateral. This document serves as a statutory requirement to inform the borrower of their default status and the total amount due to prevent loss. It outlines specific deadlines for payment and warns of imminent asset recovery. Receiving this letter is a critical warning; failure to settle the arrears or negotiate a repayment plan immediately will result in the involuntary repossession of the property or vehicle, significantly damaging the borrower's credit score.

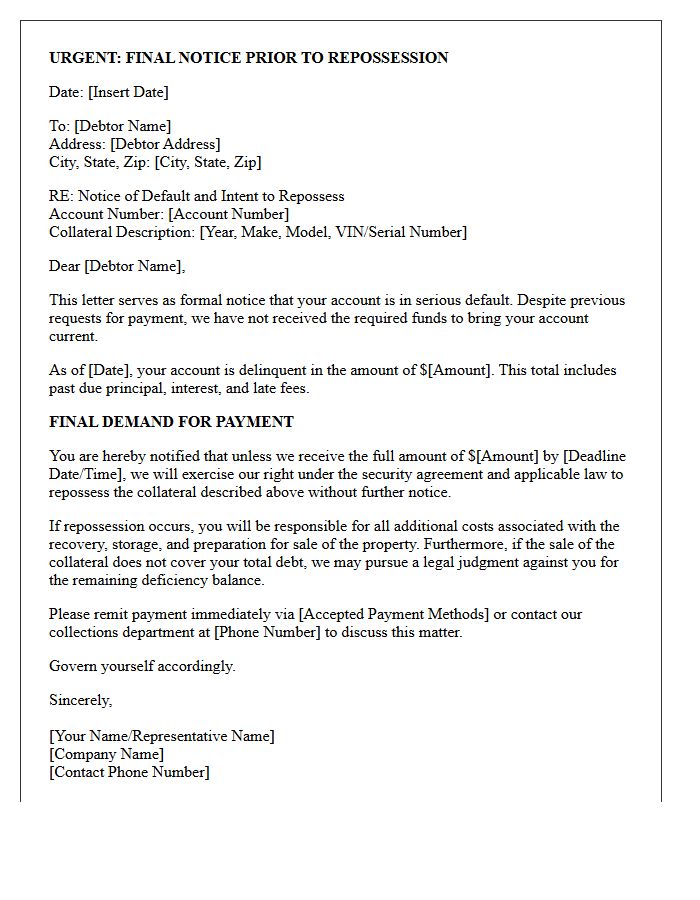

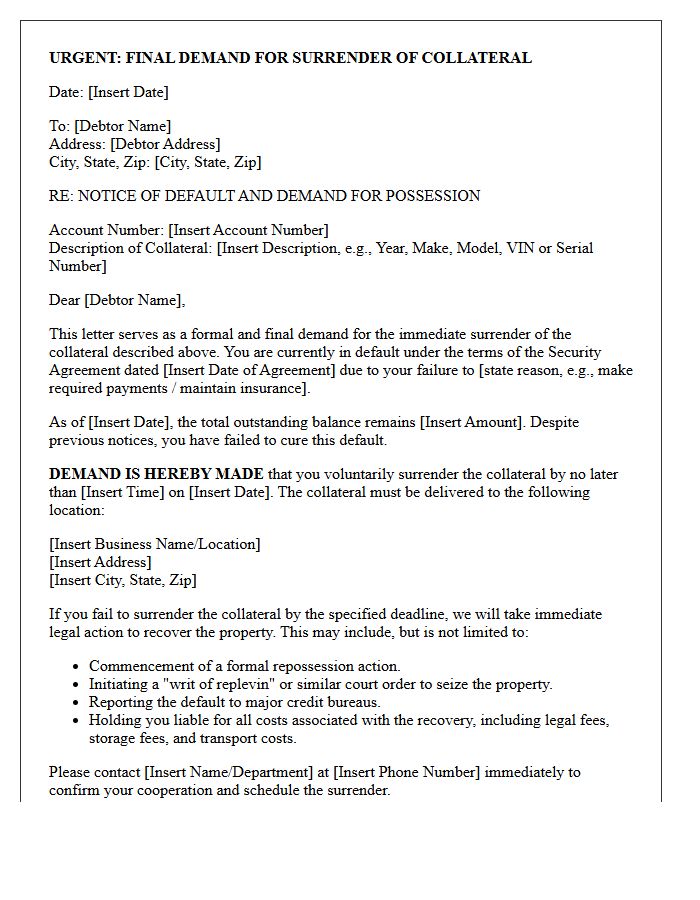

Urgent Letter of Final Demand for Collateral Surrender

An Urgent Letter of Final Demand for Collateral Surrender is a formal legal notice issued when a borrower defaults on a secured loan. It serves as the last warning before a creditor initiates repossession or litigation to seize assets. Recipients must act immediately to settle the debt or negotiate terms to prevent the loss of property. Ignoring this document often leads to mandatory asset forfeiture and significant damage to credit ratings. Providing a timely response is essential to exploring restructuring options or avoiding immediate judicial enforcement actions.

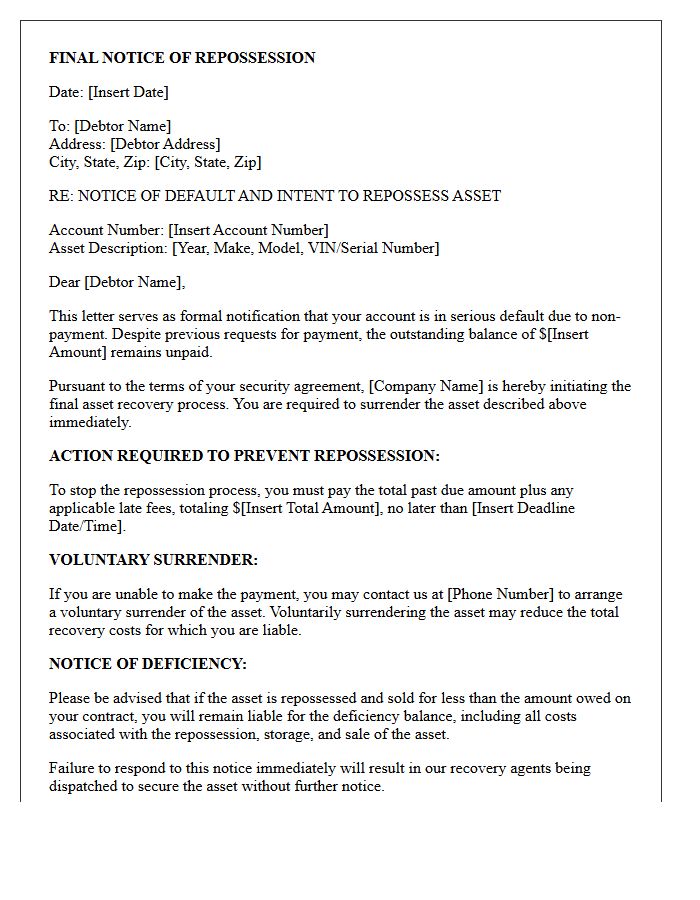

Asset Recovery and Final Repossession Notice Letter

An Asset Recovery and Final Repossession Notice Letter is a formal legal notification sent to a debtor before a lender seizes collateral. This document serves as a final warning, detailing the outstanding balance, the specific assets at risk, and a strict deadline for payment. It is a critical step in the enforcement process, signaling that repossession is imminent unless immediate action is taken. Receiving this letter indicates that the grace period has ended, making it essential to contact the creditor or seek legal advice to prevent the loss of property.

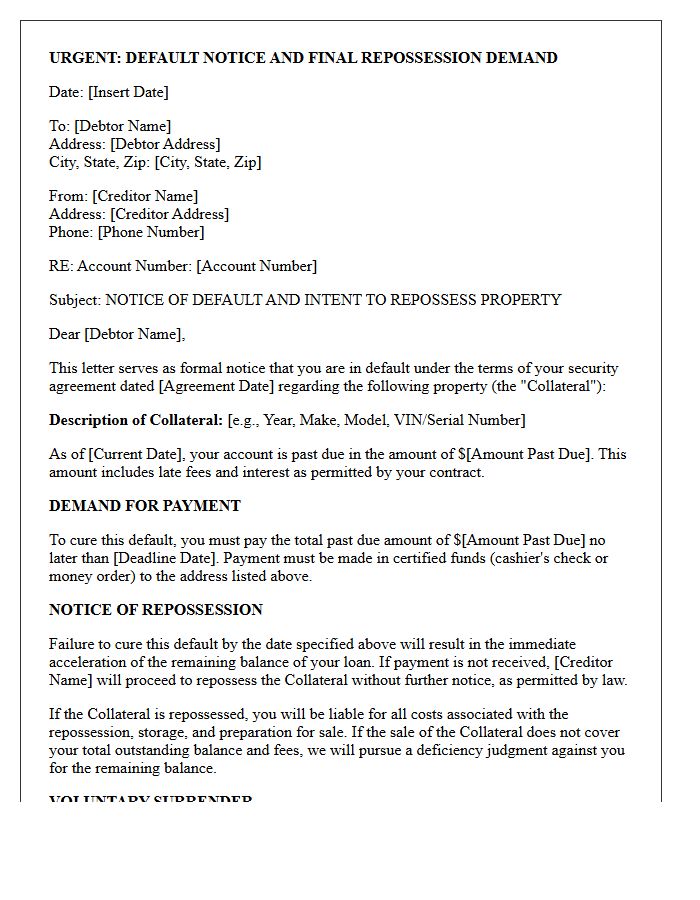

Default Notice and Final Repossession Demand Letter

A Default Notice is a formal warning issued when you miss payments on a credit agreement, providing a specific timeframe to rectify the breach. Failing to settle the arrears leads to a Final Repossession Demand Letter, which terminates the contract and requires immediate full repayment. This legal step precedes asset seizure or court action. Understanding these documents is vital because they represent the final opportunity to negotiate a repayment plan or seek debt advice before losing your property or collateral. Prompt action is essential to prevent permanent credit damage and foreclosure.

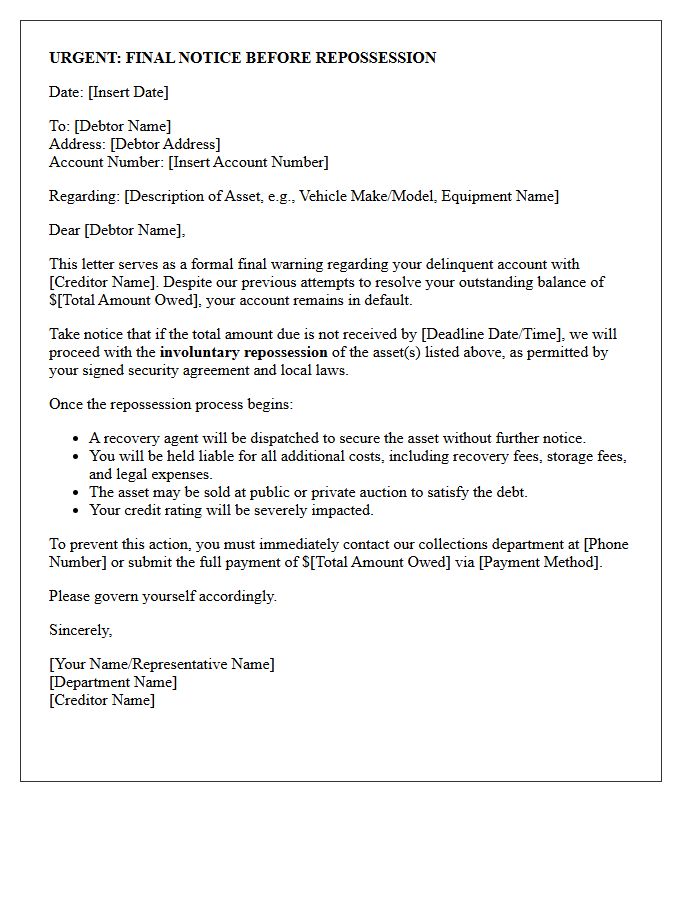

Final Warning Letter Before Involuntary Asset Repossession

A final warning letter serves as a formal notice that a lender intends to initiate involuntary asset repossession. This document signifies that the borrower has failed to resolve a default within the required timeframe. It is the last opportunity to settle the outstanding debt or negotiate a payment plan to avoid the physical seizure of property, such as a vehicle or equipment. Receiving this notice means legal protection periods have likely expired, making immediate communication with the creditor essential to prevent the loss of ownership and significant damage to your credit profile.

Secured Debt Final Demand and Repossession Letter

A Secured Debt Final Demand is a formal legal notice issued when a borrower defaults on a loan backed by collateral. This letter serves as a final warning before the lender initiates the repossession process to seize the asset. It specifies the total arrears due and provides a strict deadline for payment. Failing to settle the debt or negotiate a repayment plan immediately grants the creditor the right to reclaim property, such as a vehicle or home, to recover losses. Receiving this document signifies that legal action is imminent.

Notice of Intent to Repossess Final Demand Letter

A Notice of Intent to Repossess Final Demand Letter is a critical legal document sent by a lender when a borrower defaults on a loan. This final warning notifies you that the lender plans to seize the collateral, typically a vehicle, to satisfy the debt. It provides a brief window to pay the arrears or the full balance to prevent repossession. Ignoring this notice can lead to the loss of your asset and significant damage to your credit score. Acting immediately to negotiate a payment plan is essential to avoid legal action.

Delinquent Account Final Repossession Action Letter

A Delinquent Account Final Repossession Action Letter serves as the final formal notice before a lender seizes collateral due to non-payment. This critical document outlines the total outstanding balance, the specific default details, and a strict deadline for remediation. Receiving this letter indicates that internal collection efforts have failed and legal recovery is imminent. To avoid losing the asset, the borrower must immediately pay the deficiency or negotiate a settlement. Ignoring this notice typically leads to immediate property recovery, legal fees, and severe long-term damage to your credit score.

Final Collection Letter Before Collateral Repossession

A Final Collection Letter Before Collateral Repossession is a critical legal notice issued by lenders when a loan is severely delinquent. It serves as a last warning, informing the borrower that their vehicle, equipment, or property will be seized to satisfy the debt. This document outlines the total amount due, includes a strict deadline for payment, and explains the consequences of non-compliance. Receiving this letter indicates that the repossession process is imminent, making immediate communication or full payment essential to prevent the loss of the underlying collateral and severe credit damage.

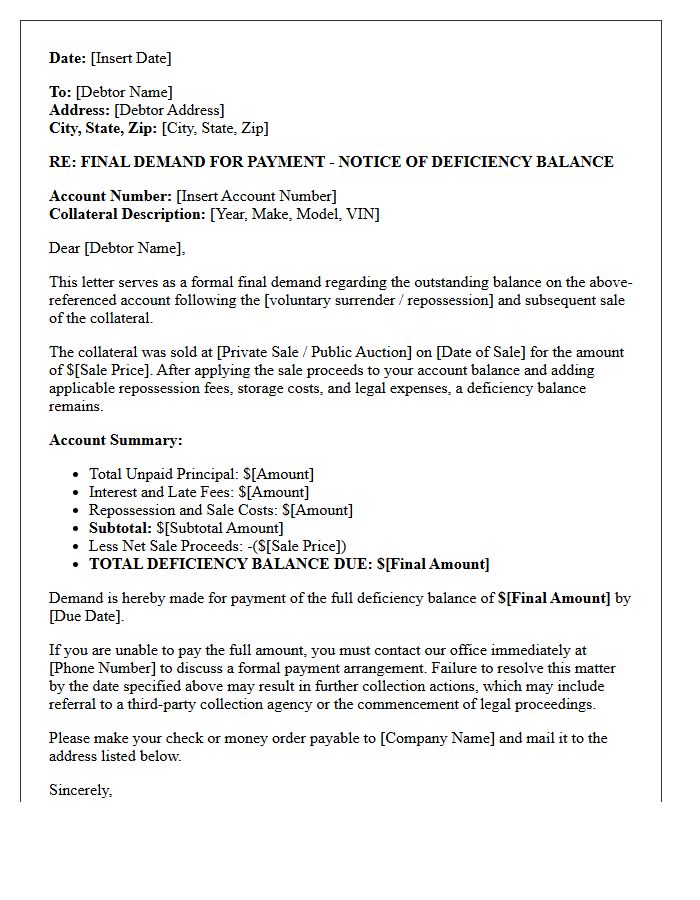

Voluntary Surrender or Repossession Final Demand Letter

A Voluntary Surrender or Repossession Final Demand Letter is a critical legal notice issued by lenders before the disposal of collateral. It informs the borrower that their vehicle or property has been seized and outlines the final opportunity to redeem the asset by paying the outstanding debt. This document specifies the deficiency balance, sale date, and potential legal consequences. Understanding this letter is vital for protecting your credit score and negotiating settlements to prevent further litigation or long-term financial liability following a loan default.

What is a Final Demand Notice Before Asset Repossession?

A Final Demand Notice is a formal legal document issued by a lender notifying a borrower that they have defaulted on their loan agreement. It serves as the last warning before the creditor initiates the physical repossession of the collateral, such as a vehicle or property, to satisfy the outstanding debt.

How many days do I have to respond to a Final Demand Notice?

The timeframe typically ranges from 7 to 14 days, depending on your state laws and the specific terms of your credit agreement. Failure to pay the full demanded amount or reach a settlement within this period grants the lender the legal right to seize the asset without further warning.

Can I stop asset repossession after receiving a final demand?

Yes, you can stop repossession by paying the total arrears plus any late fees to "reinstate" the loan, or by paying the entire remaining balance to "redeem" the asset. Alternatively, filing for bankruptcy triggers an automatic stay which temporarily halts all collection and repossession activities.

What happens if I ignore a Final Demand Notice Before Asset Repossession?

If you ignore the notice, the lender will dispatch a repossession agent to seize the asset. Once repossessed, the asset is typically sold at auction. If the sale price does not cover your total debt, you may still be held liable for a "deficiency balance" and your credit score will suffer significant damage.

Do lenders have to go to court before repossessing an asset?

In many jurisdictions, lenders can utilize "self-help repossession" for movable property like cars, meaning they do not need a court order as long as they do not "breach the peace." However, for real estate (foreclosure) or in specific states with strict consumer protection laws, a judicial court order may be required before the asset is seized.

Comments