If you are denied coverage, a lender must provide an Adverse Action Letter explaining the specific reasons for the rejection. This document is a legal requirement under the FCRA, typically triggered by low credit scores or high debt-to-income ratios. Understanding these notices helps you rectify errors and improve your financial standing. To simplify your process, below are some ready to use template.

Image cover: Private Mortgage Insurance Denial: Adverse Action Templates and Notice Samples

Letter Samples List

- Standard Adverse Action Letter for Private Mortgage Insurance Denial

- Credit Score Deficient Adverse Action Letter for Private Mortgage Insurance Denial

- High Debt-to-Income Ratio Adverse Action Letter for Private Mortgage Insurance Denial

- Insufficient Down Payment Adverse Action Letter for Private Mortgage Insurance Denial

- Unacceptable Property Appraisal Adverse Action Letter for Private Mortgage Insurance Denial

- Incomplete Documentation Adverse Action Letter for Private Mortgage Insurance Denial

- Past Foreclosure Record Adverse Action Letter for Private Mortgage Insurance Denial

- Unverified Income Adverse Action Letter for Private Mortgage Insurance Denial

- Inadequate Cash Reserves Adverse Action Letter for Private Mortgage Insurance Denial

- Derogatory Credit History Adverse Action Letter for Private Mortgage Insurance Denial

- Recent Bankruptcy Adverse Action Letter for Private Mortgage Insurance Denial

- Maximum Loan-to-Value Exceeded Adverse Action Letter for Private Mortgage Insurance Denial

Standard Adverse Action Letter for Private Mortgage Insurance Denial

A Standard Adverse Action Letter for private mortgage insurance (PMI) is a mandatory notice sent when an application is denied or approved under less favorable terms. Under the Equal Credit Opportunity Act and the Fair Credit Reporting Act, lenders must disclose the specific reasons for the denial, such as credit score issues or insufficient collateral. This document ensures transparency and allows borrowers to dispute inaccuracies within their credit reports. Understanding these notices is essential for addressing financial barriers and improving future eligibility for mortgage insurance coverage during the home-buying process.

Credit Score Deficient Adverse Action Letter for Private Mortgage Insurance Denial

A credit score deficient adverse action letter is a formal notice explaining why your application for Private Mortgage Insurance (PMI) was denied. Under the Fair Credit Reporting Act, lenders must disclose if your credit score fell below the required threshold. This document identifies the specific credit reporting agency used and the key factors negatively impacting your rating. Receiving this letter allows you to request a free credit report to dispute inaccuracies. Understanding these risk factors is essential for improving your eligibility for future mortgage financing and securing lower insurance premiums.

High Debt-to-Income Ratio Adverse Action Letter for Private Mortgage Insurance Denial

Receiving an adverse action letter for Private Mortgage Insurance (PMI) denial indicates that your debt-to-income ratio (DTI) exceeds the insurer's established threshold. Even if a lender approves your loan, PMI providers maintain independent underwriting standards. This notice is a legal requirement under the FCRA, explaining that your monthly debt obligations are too high relative to your gross income to mitigate default risk. To resolve this, you must either reduce outstanding debt, increase documented income, or provide a larger down payment to eliminate the PMI requirement entirely.

Insufficient Down Payment Adverse Action Letter for Private Mortgage Insurance Denial

An Insufficient Down Payment Adverse Action Letter is a formal notice sent when a lender denies Private Mortgage Insurance (PMI) coverage. This occurs because the borrower's cash contribution fails to meet the specific equity requirements or loan-to-value thresholds set by the insurer. Under the Equal Credit Opportunity Act, lenders must disclose the specific reasons for this denial. Receiving this letter indicates that while your credit may be sufficient, the lack of upfront capital increases the insurer's risk profile, necessitating a larger down payment or a different loan structure to proceed.

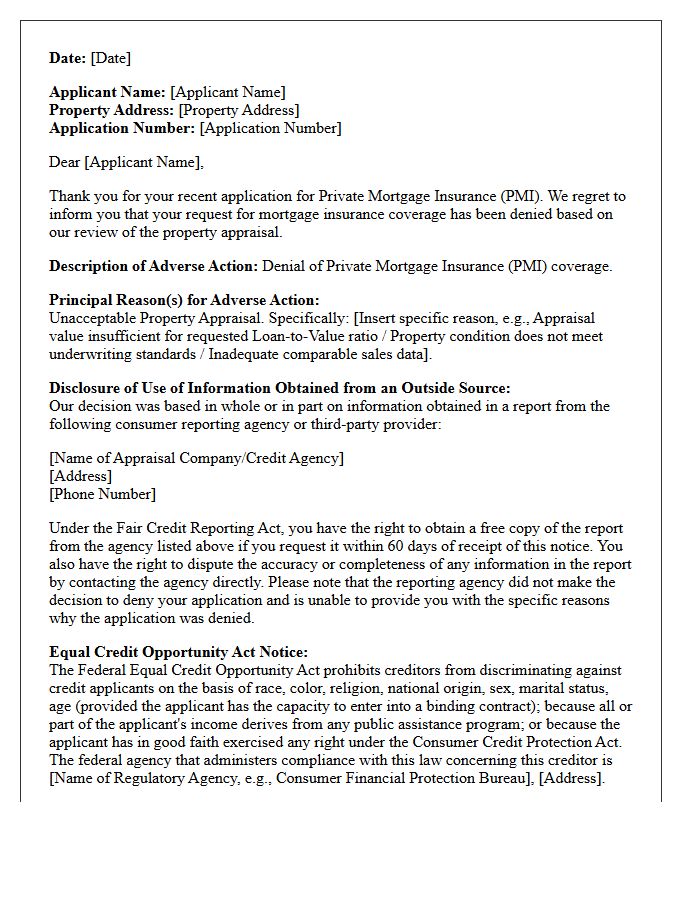

Unacceptable Property Appraisal Adverse Action Letter for Private Mortgage Insurance Denial

An adverse action letter serves as formal notification when an application for Private Mortgage Insurance (PMI) is declined due to an unacceptable property appraisal. This document is legally required under the ECOA and FCRA. It informs the borrower that the property's valuation, condition, or marketability failed to meet the insurer's specific risk guidelines. Receiving this letter means the lender cannot secure necessary mortgage insurance, potentially halting the loan process. Borrowers have the right to request a copy of the appraisal to review for errors or valuation discrepancies that led to the denial.

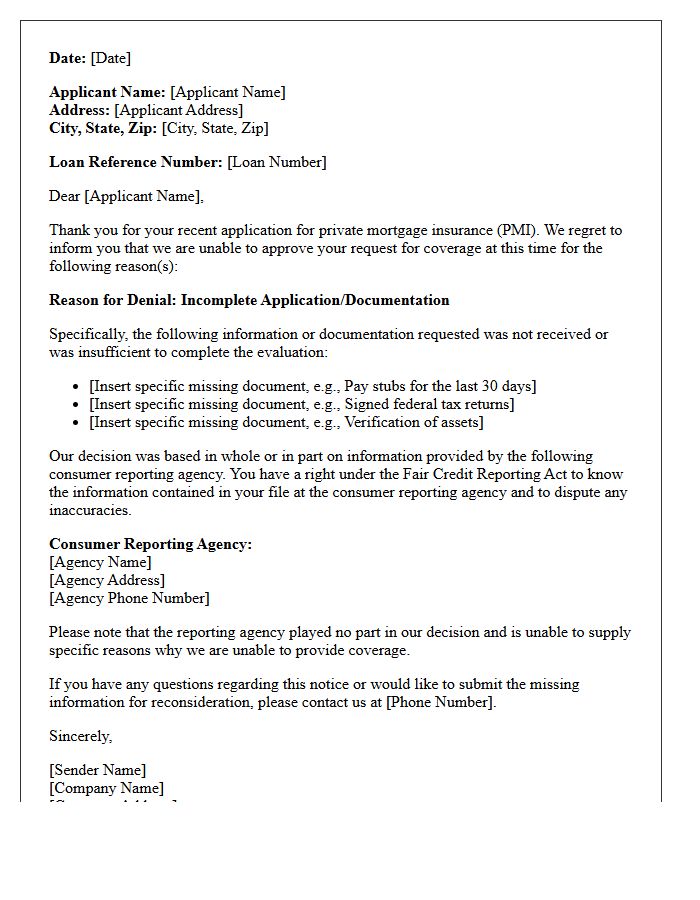

Incomplete Documentation Adverse Action Letter for Private Mortgage Insurance Denial

When a private mortgage insurance application is denied due to Incomplete Documentation, the lender must issue an Adverse Action Letter. This formal notice specifies exactly which financial records or verification forms were missing. To resolve this, you must quickly provide the outstanding items, such as updated pay stubs or tax returns, to restart the underwriting process. Under the Equal Credit Opportunity Act, you have the right to request a detailed explanation within sixty days to ensure your mortgage approval remains on track.

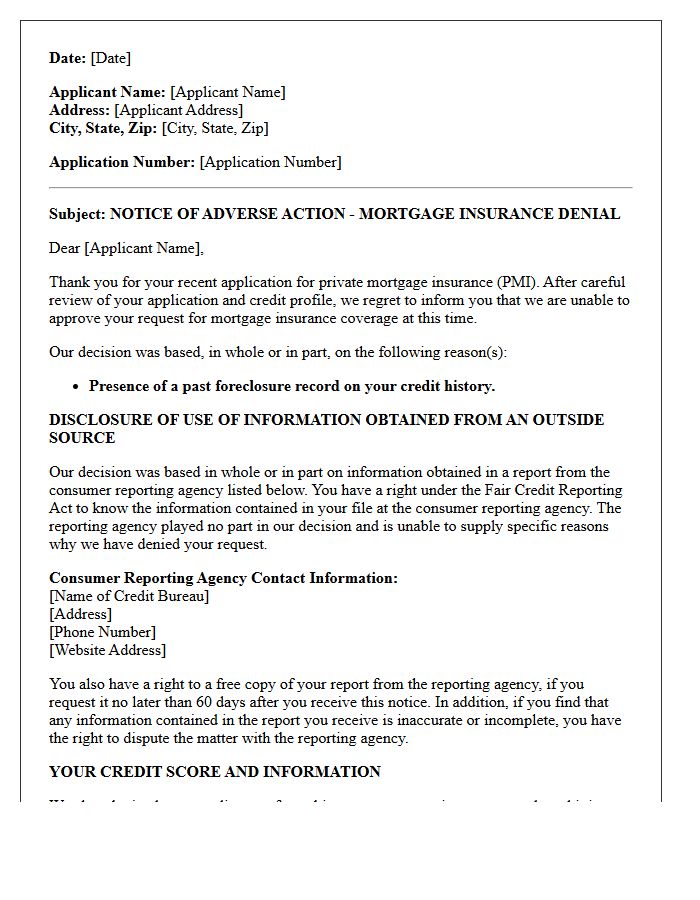

Past Foreclosure Record Adverse Action Letter for Private Mortgage Insurance Denial

Receiving an adverse action letter for Private Mortgage Insurance (PMI) denial due to a past foreclosure is a critical legal notification. Federal law requires insurers to disclose specific reasons for rejecting your application or charging higher premiums. This document highlights how a foreclosure record impacts your creditworthiness and risk profile. Understanding these details is essential for identifying reporting errors and taking steps to rebuild credit. If denied, you are entitled to a free credit report copy to verify the accuracy of the negative information impacting your mortgage eligibility.

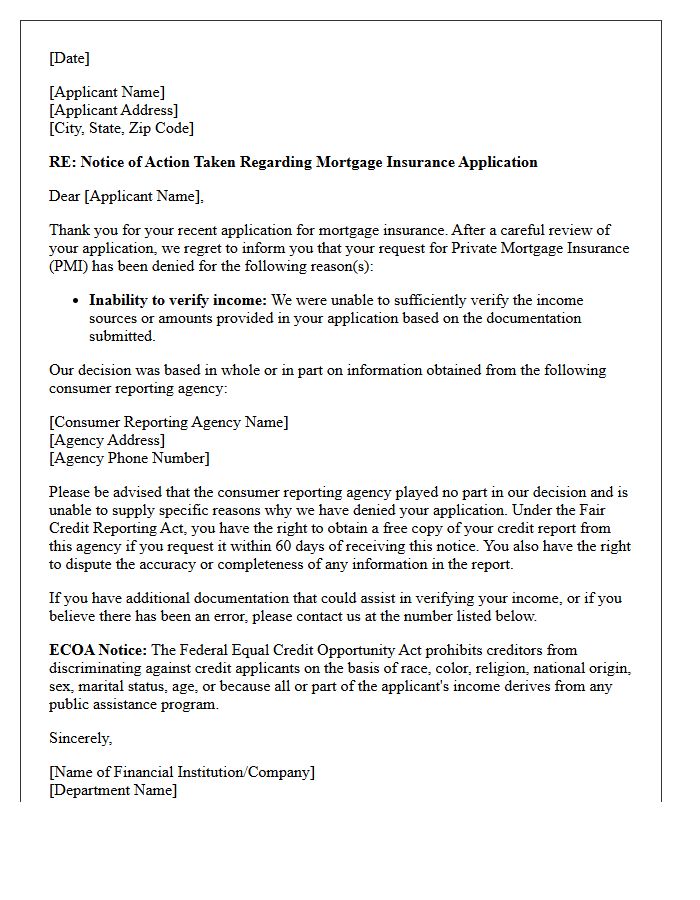

Unverified Income Adverse Action Letter for Private Mortgage Insurance Denial

An Unverified Income Adverse Action Letter is a formal notice issued when a private mortgage insurance (PMI) provider denies coverage. This typically occurs because the PMI company cannot independently confirm your earnings or employment history. Without this insurance, your mortgage lender may decline your loan application or require a higher down payment. To resolve this, you must provide supplemental documentation, such as tax returns or pay stubs, to prove financial stability. Receiving this letter does not mean your credit is poor, but rather that your income documentation was insufficient for risk assessment.

Inadequate Cash Reserves Adverse Action Letter for Private Mortgage Insurance Denial

An inadequate cash reserves adverse action letter is a formal notice issued when a Private Mortgage Insurance (PMI) application is denied. This rejection occurs because the borrower lacks sufficient liquid assets to cover potential financial emergencies after closing. Lenders and insurers require a specific safety net to mitigate default risk. Under the Equal Credit Opportunity Act, this letter must clearly state the specific reasons for denial. Applicants should review their financial statements and consider increasing their savings or reducing debt to improve future eligibility for mortgage insurance approval.

Derogatory Credit History Adverse Action Letter for Private Mortgage Insurance Denial

A private mortgage insurance denial due to a derogatory credit history triggers a mandatory adverse action letter. This document explains that your application was rejected or offered less favorable terms because of negative marks like late payments, collections, or bankruptcies. Legally required by the FCRA, the letter must identify the specific credit reporting agency used and outline your right to dispute inaccuracies. Understanding these findings is essential for improving your financial standing and securing future home loan approval with better insurance premiums.

Recent Bankruptcy Adverse Action Letter for Private Mortgage Insurance Denial

Receiving a Private Mortgage Insurance (PMI) denial due to a recent bankruptcy is a common adverse action. Lenders use these letters to disclose that your credit risk profile falls outside their underwriting guidelines. Most insurers require a mandatory waiting period, typically two to four years post-discharge, before approving coverage. To improve future eligibility, focus on maintaining re-established credit and low debt-to-income ratios. Understanding the specific reasons cited in the notice is essential for correcting inaccuracies and planning your eventual homeownership timeline effectively.

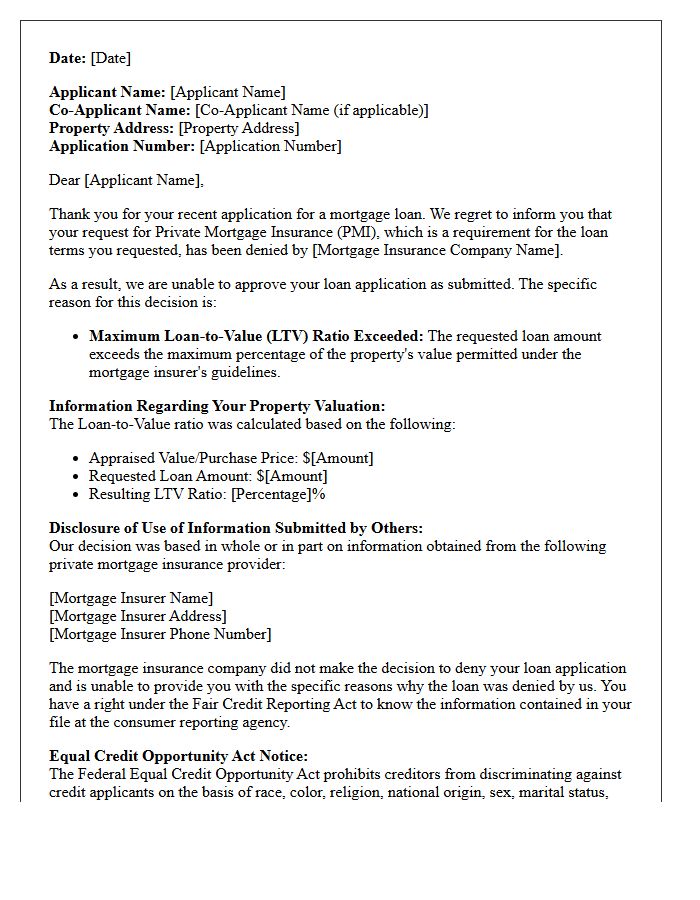

Maximum Loan-to-Value Exceeded Adverse Action Letter for Private Mortgage Insurance Denial

A Maximum Loan-to-Value Exceeded Adverse Action Letter is a formal notice issued when a lender denies Private Mortgage Insurance (PMI) coverage. This occurs because the loan amount exceeds the specific LTV threshold required by the insurer's guidelines. Since PMI is essential for high-leverage financing, this denial typically halts the loan approval process. The letter must legally disclose the specific reasons for the rejection and provide information on the credit reporting agency used, ensuring transparency under federal consumer protection laws regarding your mortgage application status.

What is an Adverse Action Letter for Private Mortgage Insurance (PMI)?

An Adverse Action Letter is a formal notification sent by a mortgage lender informing an applicant that their request for private mortgage insurance has been denied, or that the terms offered are less favorable than requested, based on specific risk factors.

Why did I receive an Adverse Action notice regarding my mortgage insurance?

You received this notice because a mortgage insurance provider reviewed your loan application and determined that you do not meet their specific underwriting guidelines, often due to credit score requirements, debt-to-income ratios, or loan-to-value limitations.

Does a PMI denial mean my entire mortgage application is rejected?

Not necessarily. While a PMI denial prevents you from obtaining a conventional loan with less than a 20% down payment, your lender may suggest alternative options such as a larger down payment, a different loan program like FHA, or a different mortgage insurance provider.

What specific information must be included in a PMI Adverse Action Letter?

Legally, the letter must include the specific reasons for the denial, the name and contact information of the mortgage insurance company that made the decision, and a notice of your rights under the Fair Credit Reporting Act (FCRA).

Can I dispute the reasons listed in my PMI denial letter?

Yes. If the denial was based on information in your credit report that you believe is inaccurate, you have the right to dispute that information with the relevant credit bureau and request a free copy of your report within 60 days of receiving the letter.

Comments