A Subject To Appraisal Commitment Letter is a conditional mortgage approval stating that the loan is guaranteed only if the property's appraised value meets the purchase price. This document protects lenders by ensuring the collateral covers the loan amount and informs buyers of potential funding gaps. Understanding these contingencies is essential for successful real estate transactions. Below are some ready to use template.

Image cover: Professional Subject To Appraisal Commitment Letter Templates and Samples

Letter Samples List

- Standard Subject To Appraisal Commitment Letter

- Conditional Mortgage Approval Subject To Appraisal Letter

- Residential Loan Commitment Subject To Appraisal Letter

- Commercial Mortgage Commitment Subject To Appraisal Letter

- Refinance Loan Commitment Subject To Appraisal Letter

- Jumbo Mortgage Commitment Subject To Appraisal Letter

- Federal Housing Administration Loan Commitment Subject To Appraisal Letter

- Veterans Affairs Mortgage Commitment Subject To Appraisal Letter

- Rural Housing Conditional Commitment Subject To Appraisal Letter

- Investment Property Commitment Subject To Appraisal Letter

- New Construction Loan Commitment Subject To Appraisal Letter

- Home Equity Line Of Credit Subject To Appraisal Letter

- Portfolio Mortgage Commitment Subject To Appraisal Letter

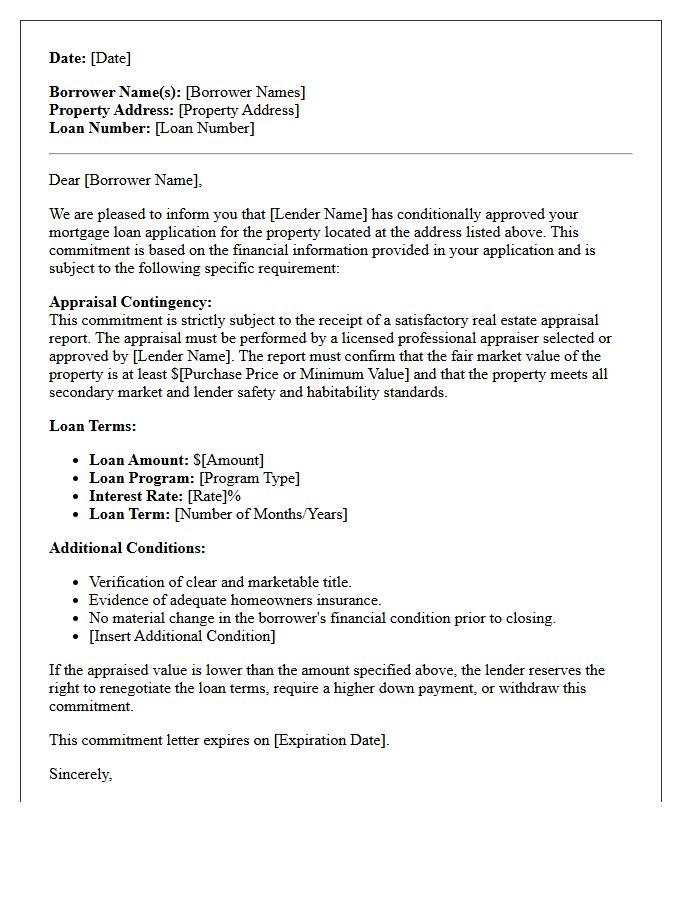

Standard Subject To Appraisal Commitment Letter

A Standard Subject To Appraisal Commitment Letter is a conditional agreement where a lender approves a mortgage, provided the property's market value meets or exceeds the purchase price. This document ensures the collateral secures the loan amount sufficiently. If the formal appraisal report comes in lower than expected, the lender may reduce the financing or require a larger down payment. Understanding this contingency is vital for buyers to mitigate financial risk during the closing process, as it protects the bank's investment while finalizing the borrower's creditworthiness and property eligibility.

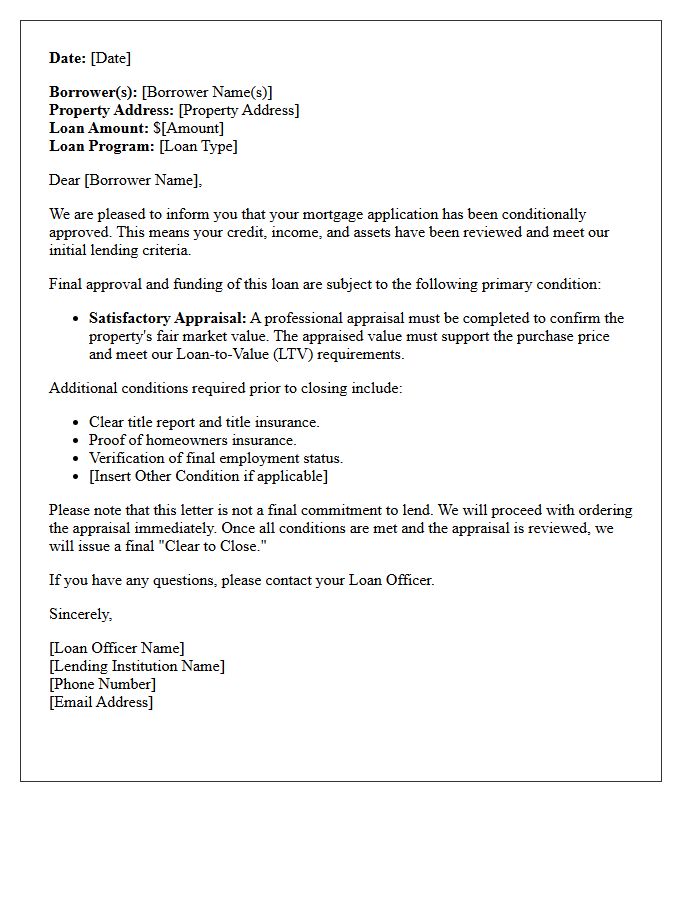

Conditional Mortgage Approval Subject To Appraisal Letter

A conditional mortgage approval subject to appraisal means your loan is approved pending a professional valuation of the property. The lender issues this letter to confirm you meet credit and income requirements, but the collateral must support the purchase price. If the home's appraised value is lower than the offer, you may need to increase your down payment or renegotiate the price. This document is a critical step, signaling that the final loan commitment depends on the home's condition and market worth meeting the lender's specific guidelines.

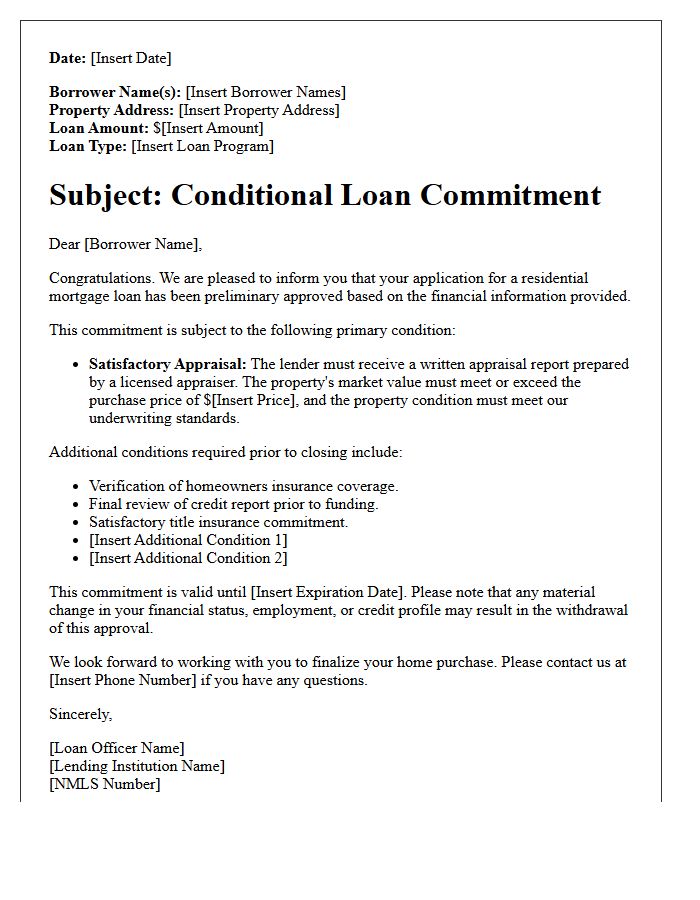

Residential Loan Commitment Subject To Appraisal Letter

A residential loan commitment subject to appraisal letter is a conditional approval from a lender. It indicates that your financing is secured, provided the property's market value meets or exceeds the purchase price. This document is a critical milestone in the mortgage process, but it remains contingent on a professional valuation. If the appraisal comes in low, the loan amount may be reduced, requiring a larger down payment or price renegotiation. Always verify the expiration date and any additional underwriting conditions to ensure a successful closing.

Commercial Mortgage Commitment Subject To Appraisal Letter

A Commercial Mortgage Commitment Letter serves as a formal agreement from a lender to provide financing, yet it remains conditional until the property value is verified. The most critical contingency is the Appraisal Letter, which ensures the asset's market value supports the requested loan-to-value ratio. If the independent valuation falls short of the purchase price, the lender may reduce the loan amount or revoke the offer entirely. Borrowers must prioritize this valuation phase to confirm that the underlying collateral secures the debt according to the primary underwriting guidelines and risk mitigation standards.

Refinance Loan Commitment Subject To Appraisal Letter

A Refinance Loan Commitment Subject To Appraisal Letter is a conditional approval from a lender. It indicates that while your credit and income meet requirements, the final loan amount depends on a professional property valuation. The lender must verify that the home's current market value provides sufficient collateral to support the requested loan-to-value ratio. If the appraisal comes in lower than expected, the loan terms may change or require a higher equity contribution to proceed. This document is a critical milestone before reaching the final closing disclosure phase.

Jumbo Mortgage Commitment Subject To Appraisal Letter

A Jumbo Mortgage Commitment Subject To Appraisal Letter is a conditional approval for high-value loans exceeding conforming limits. It confirms the lender's intent to fund, provided the property valuation matches or exceeds the purchase price. Since jumbo loans carry higher risk, this document ensures the collateral value secures the debt. Borrowers must finalize the appraisal to clear this contingency and move to closing. It proves financial backing to sellers while protecting the lender against over-leveraging on luxury real estate investments.

Federal Housing Administration Loan Commitment Subject To Appraisal Letter

A Federal Housing Administration (FHA) Loan Commitment Subject to Appraisal letter is a conditional approval indicating a borrower meets credit and income requirements. However, final funding is contingent upon a HUD-compliant appraisal. This evaluation ensures the property meets specific Minimum Property Standards regarding safety, security, and structural integrity. If the home's appraised value falls below the purchase price or requires mandatory repairs, the loan terms may change. This document serves as a critical milestone, signaling that the mortgage is approved provided the collateral value and condition satisfy federal guidelines.

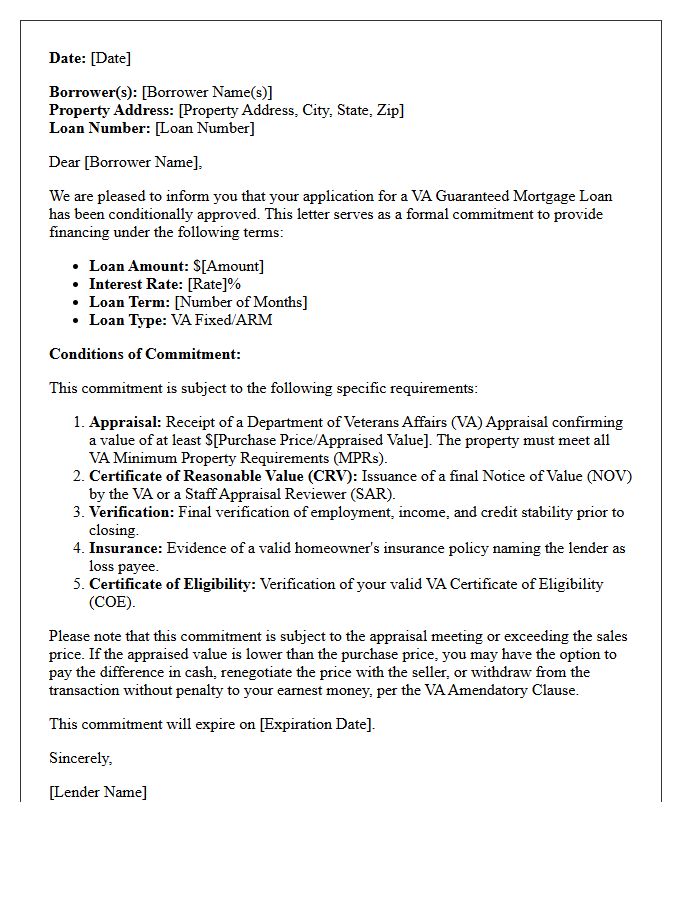

Veterans Affairs Mortgage Commitment Subject To Appraisal Letter

A Veterans Affairs Mortgage Commitment Subject to Appraisal Letter is a conditional approval indicating a lender intends to fund your loan. The most critical factor is the Notice of Value, which determines the property's worth. This document remains subject to appraisal, meaning the final loan amount depends on the home meeting specific VA minimum property requirements and valuation standards. If the appraised value comes in lower than the purchase price, the buyer may need to negotiate the price, pay the difference in cash, or exercise their right to cancel the contract without penalty.

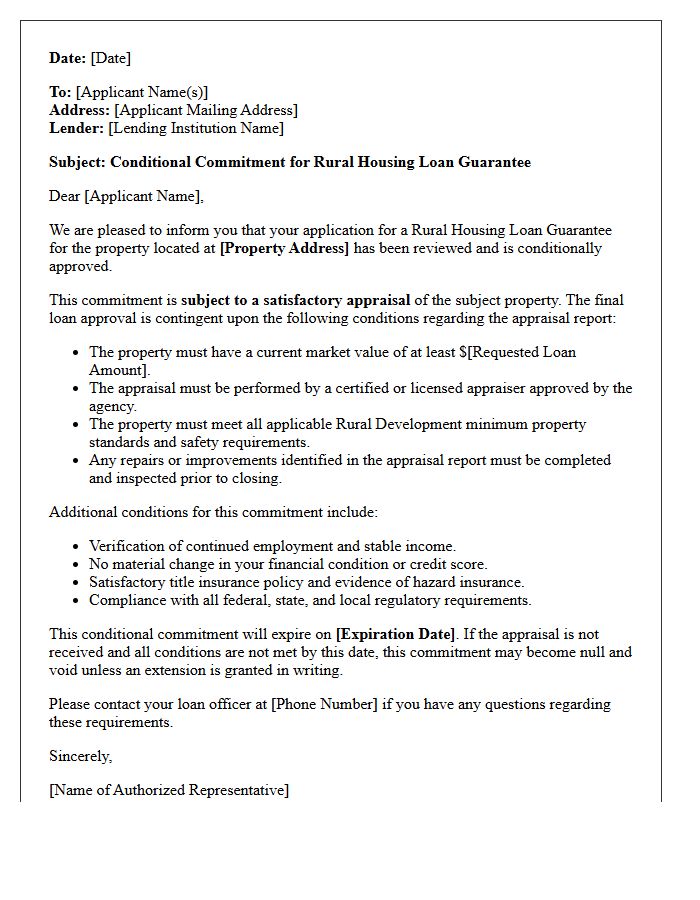

Rural Housing Conditional Commitment Subject To Appraisal Letter

A Rural Housing Conditional Commitment Subject to Appraisal letter is a preliminary approval issued by the USDA. It signifies that the applicant meets credit and income requirements, but final loan backing is contingent upon the property's market value. The appraisal must confirm the home meets specific safety standards and supports the purchase price. This document is a vital milestone, yet funding remains conditional until the formal valuation is reviewed and the property is deemed eligible for federal guarantee under the Rural Development program.

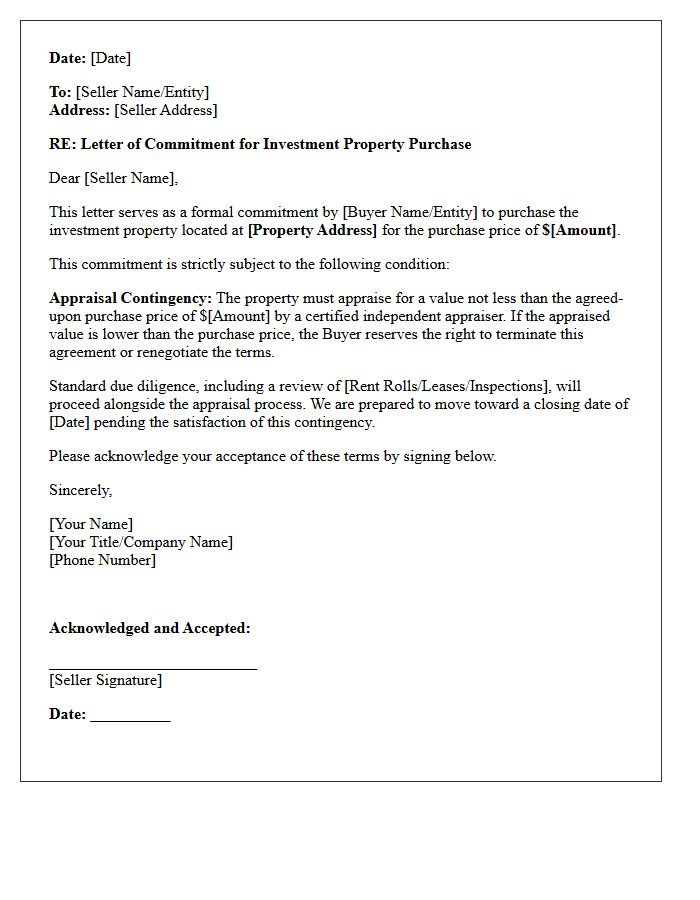

Investment Property Commitment Subject To Appraisal Letter

An appraisal contingency is a vital clause in a real estate commitment letter that protects the buyer's capital. It ensures the loan amount is strictly based on the property's professional valuation rather than the purchase price. If the appraisal comes in lower than expected, this letter allows the investor to renegotiate the deal, request a larger down payment, or legally withdraw without penalty. Understanding this valuation requirement is essential for securing financing and mitigating financial risk during an investment property acquisition.

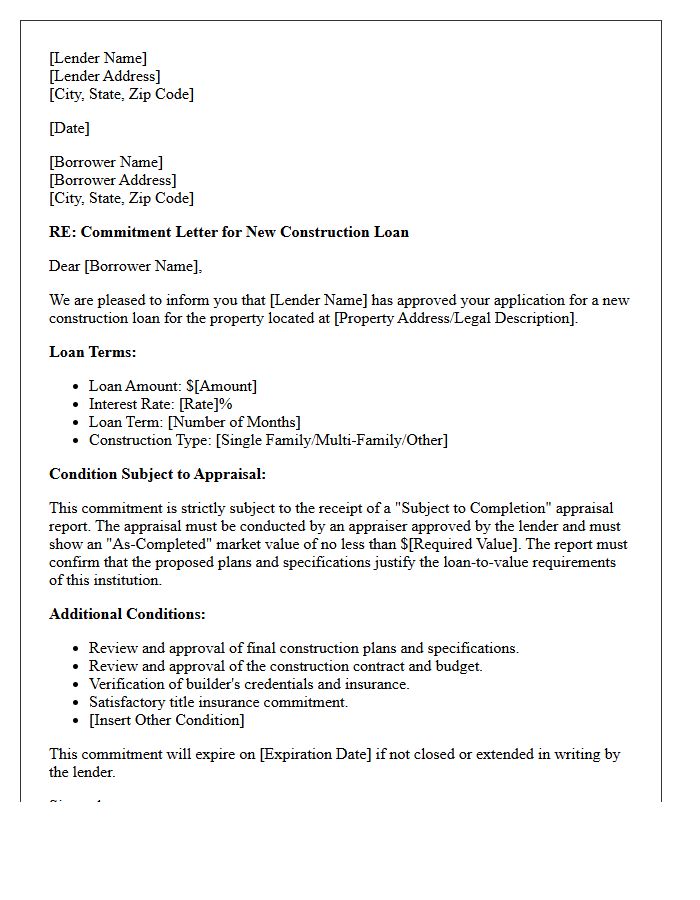

New Construction Loan Commitment Subject To Appraisal Letter

A new construction loan commitment subject to appraisal letter is a conditional approval from a lender. It signifies that your financing is secured, provided the completed property's market value aligns with the loan amount. This document is essential for builders to begin work, as it guarantees funding once the final appraisal confirms the home's worth. Ensuring the structure meets all plans and specifications is critical, as any discrepancy between the estimated and final value could impact your loan-to-value ratio and overall financing terms before closing.

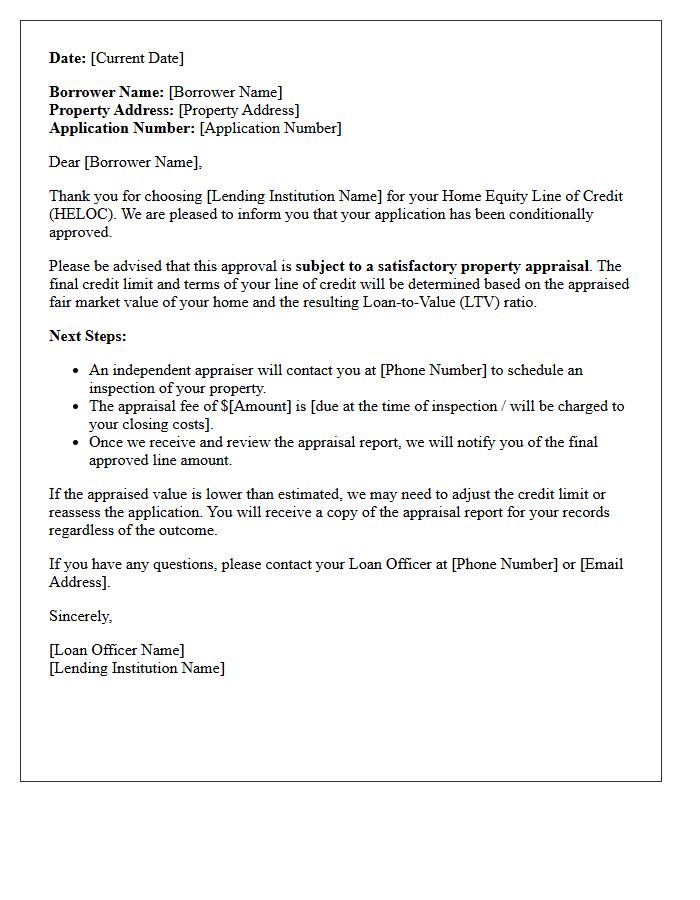

Home Equity Line Of Credit Subject To Appraisal Letter

A home equity line of credit subject to appraisal letter informs applicants that their HELOC approval depends on a professional valuation of their property. Lenders use this document to verify the current market value and determine the available equity. The appraisal ensures the loan-to-value ratio meets specific underwriting guidelines. If the appraised value is lower than expected, your credit limit may be reduced or the application denied. Reviewing this letter is essential to understand potential closing costs and the timeline for final funding of your line of credit.

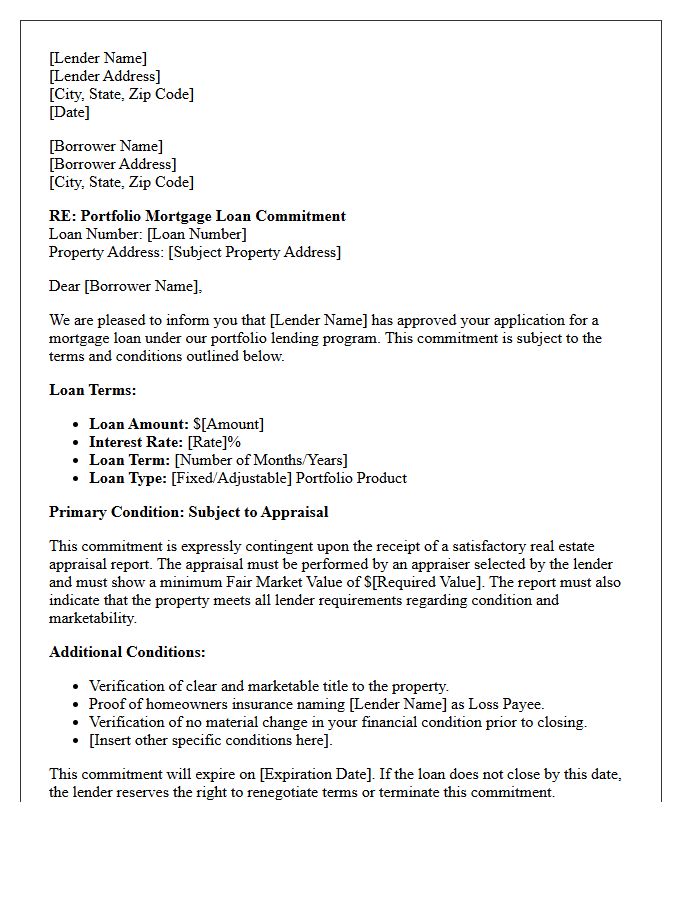

Portfolio Mortgage Commitment Subject To Appraisal Letter

A Portfolio Mortgage Commitment Subject To Appraisal Letter is a conditional approval from a lender who manages loans in-house rather than selling them to investors. This document confirms your financial eligibility for a mortgage, provided the property's value meets specific criteria. The primary contingency is a satisfactory appraisal report to secure the loan-to-value ratio. Because portfolio lenders set their own underwriting standards, these commitments often offer more flexibility for unique properties or complex borrower profiles, serving as a critical step toward final closing once the valuation is finalized.

What is a Subject to Appraisal Commitment Letter?

A Subject to Appraisal Commitment Letter is a formal document issued by a mortgage lender stating that your home loan is approved, provided the property's appraised value meets or exceeds the agreed-upon purchase price.

Why do lenders include an appraisal contingency in a commitment letter?

Lenders include this contingency to ensure the property serves as sufficient collateral for the loan amount, protecting the financial institution from lending more money than the home is actually worth.

What happens if the appraisal comes in lower than the purchase price?

If the appraisal is low, the commitment letter terms are not met. The buyer must either pay the difference in cash, negotiate a lower price with the seller, or exercise their right to withdraw from the contract without losing their earnest money.

Does a Subject to Appraisal Commitment Letter mean the loan is fully approved?

No, it is a conditional approval. While your credit and income have been verified, the final funding is dependent on the "Subject To" condition being cleared through a satisfactory professional home appraisal report.

How long does it take to clear the appraisal condition in a commitment letter?

Once the appraisal report is submitted to the lender, it typically takes 48 to 72 hours for an underwriter to review the document and officially remove the appraisal contingency from the commitment letter.

Comments