A Jumbo Mortgage Conditional Approval Letter confirms that a lender is willing to finance a high-value property pending specific documentation. This document validates your purchasing power for luxury real estate while outlining required steps to finalize your loan. It provides sellers with confidence in your financial stability and high-limit borrowing capacity. Below are some ready to use templates.

Image cover: Mastering Jumbo Mortgage Conditional Approvals: Essential Templates and Letter Samples

Letter Samples List

- Standard Jumbo Mortgage Conditional Approval Letter

- Self-Employed Jumbo Mortgage Conditional Approval Letter

- High Net Worth Jumbo Mortgage Conditional Approval Letter

- Investment Property Jumbo Mortgage Conditional Approval Letter

- Primary Residence Jumbo Mortgage Conditional Approval Letter

- Second Home Jumbo Mortgage Conditional Approval Letter

- Jumbo Mortgage Rate and Term Refinance Conditional Approval Letter

- Jumbo Mortgage Cash-Out Refinance Conditional Approval Letter

- Foreign National Jumbo Mortgage Conditional Approval Letter

- Physician Program Jumbo Mortgage Conditional Approval Letter

- Fixed Rate Jumbo Mortgage Conditional Approval Letter

- Adjustable Rate Jumbo Mortgage Conditional Approval Letter

- Portfolio Product Jumbo Mortgage Conditional Approval Letter

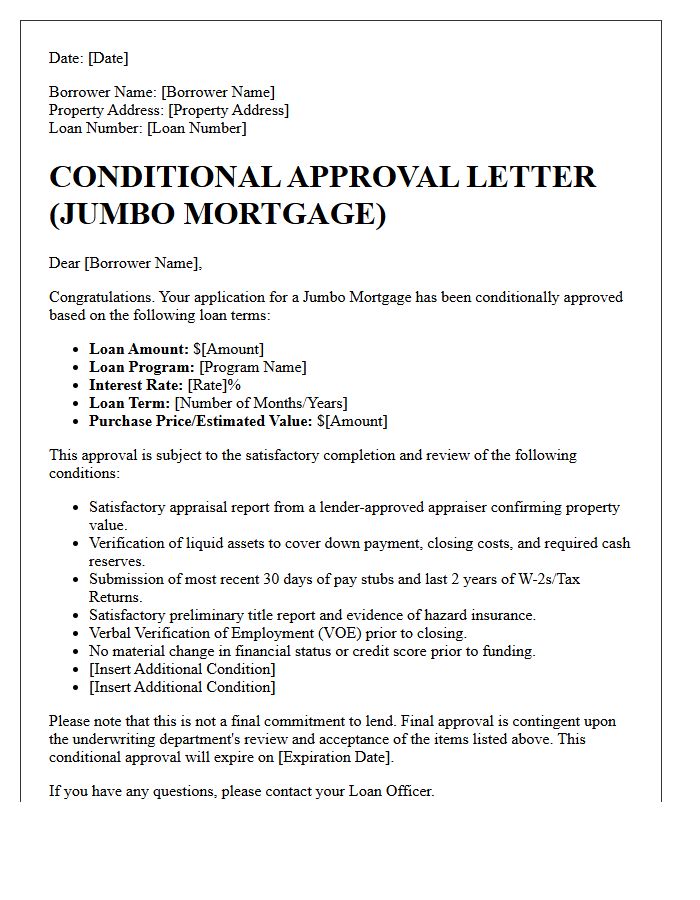

Standard Jumbo Mortgage Conditional Approval Letter

A Standard Jumbo Mortgage Conditional Approval Letter is a formal document indicating a lender's intent to fund high-value loans exceeding federal limits. It confirms your initial creditworthiness but remains subject to specific conditions like property appraisals, verified reserves, and tax documentation. This letter is a vital financial milestone, signaling to sellers that you are a qualified buyer for luxury real estate. However, final funding is only guaranteed once all underwriting requirements are met and a formal "clear to close" is officially issued by the mortgage institution.

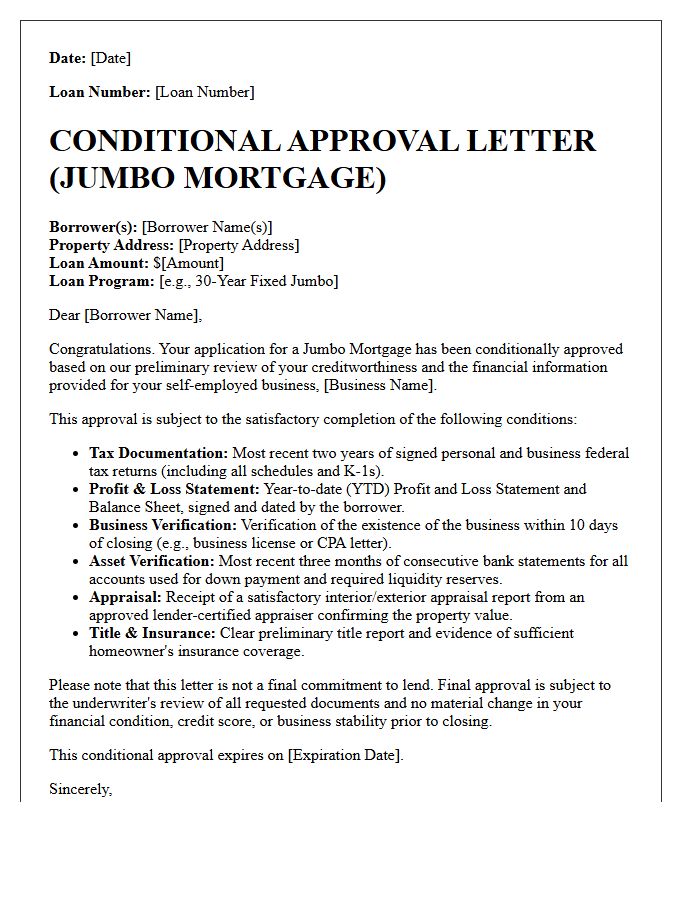

Self-Employed Jumbo Mortgage Conditional Approval Letter

A Self-Employed Jumbo Mortgage Conditional Approval Letter confirms a lender's intent to fund high-balance loans after reviewing complex tax returns. Unlike basic pre-approvals, this document verifies your debt-to-income ratio and liquidity through rigorous underwriting. It outlines specific conditions, such as updated profit and loss statements or asset verification, required for final funding. Receiving this letter signals that your business income meets strict non-conforming loan standards, providing the necessary credibility to negotiate high-end real estate transactions with confidence.

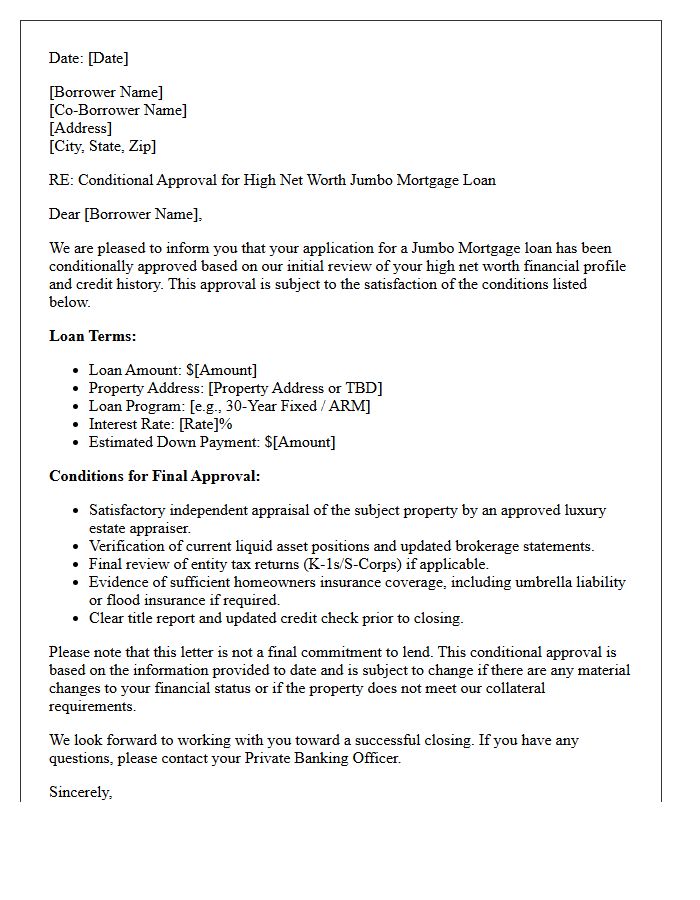

High Net Worth Jumbo Mortgage Conditional Approval Letter

A High Net Worth Jumbo Mortgage Conditional Approval Letter is a critical document proving a lender's preliminary commitment to financing luxury real estate. Unlike pre-qualification, this letter signifies that an underwriter has verified your asset liquidity, complex tax returns, and creditworthiness. Securing this conditional approval strengthens your negotiating position in competitive markets by demonstrating elite financial stability. It outlines specific conditions, such as a property appraisal or updated financial statements, that must be satisfied before the final loan commitment is issued for high-balance financing.

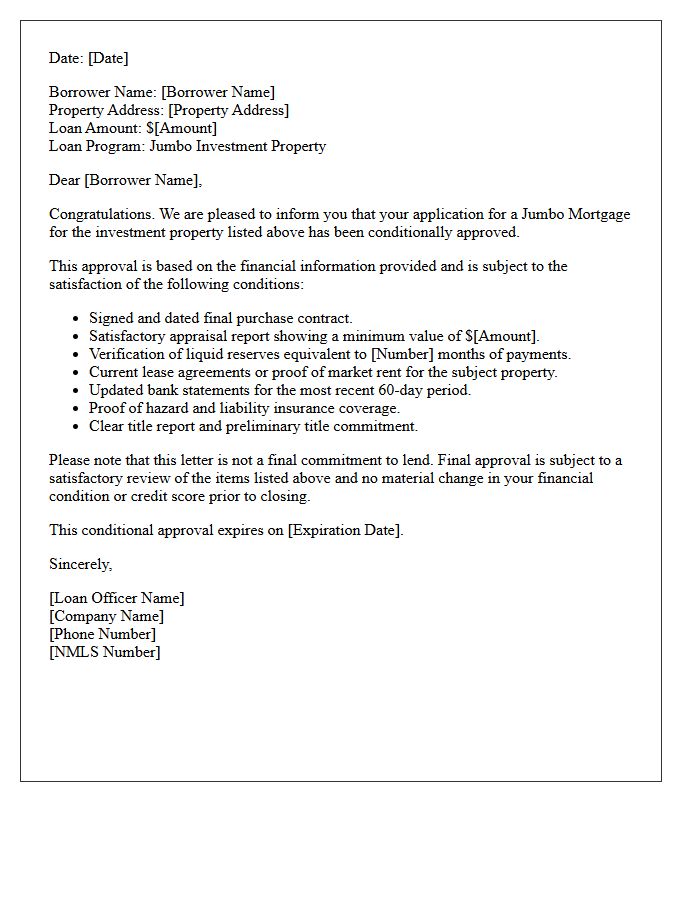

Investment Property Jumbo Mortgage Conditional Approval Letter

An Investment Property Jumbo Mortgage Conditional Approval Letter is a critical document indicating a lender's intent to finance high-value non-owner occupied real estate. It confirms that the borrower meets credit score and income requirements, pending specific conditions like a formal appraisal or title search. For investors, this letter provides the necessary financial credibility to negotiate competitive offers on luxury rentals. Unlike a pre-qualification, it involves a rigorous manual underwriting process, ensuring that the loan exceeds conforming limits while accounting for the unique risks associated with secondary market investment properties.

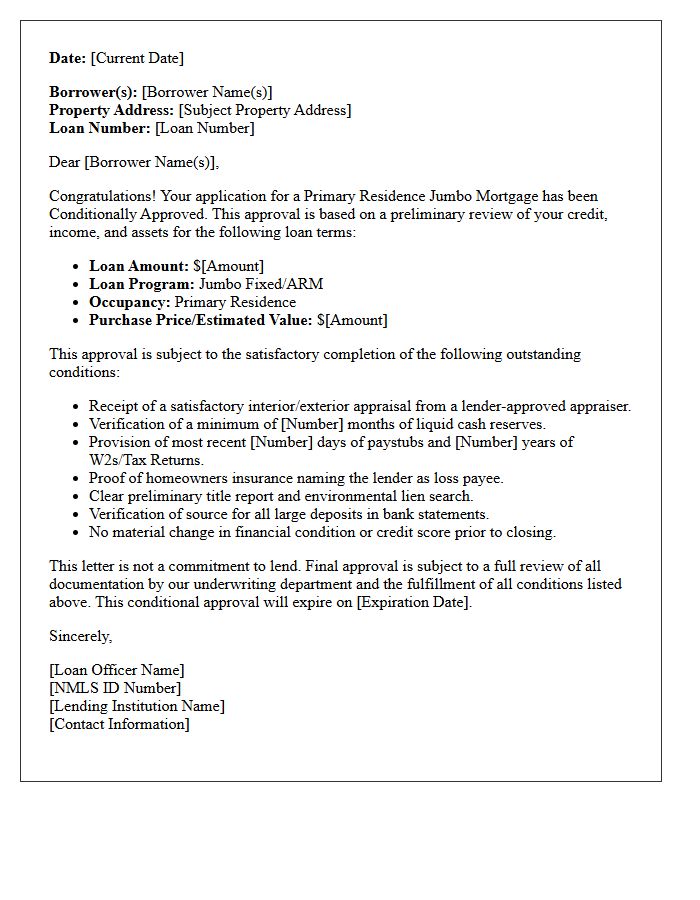

Primary Residence Jumbo Mortgage Conditional Approval Letter

A Primary Residence Jumbo Mortgage Conditional Approval Letter is a formal document from a lender indicating you are qualified for a high-value loan exceeding conforming limits. It confirms that your creditworthiness, income, and assets meet specific guidelines, pending final verifications like a home appraisal. This letter strengthens your position when bidding on luxury properties by proving financial capability. Obtaining this underwritten status early is crucial because jumbo loans involve stricter manual reviews. It signals to sellers that your financing is secure, provided you meet the remaining loan conditions before closing.

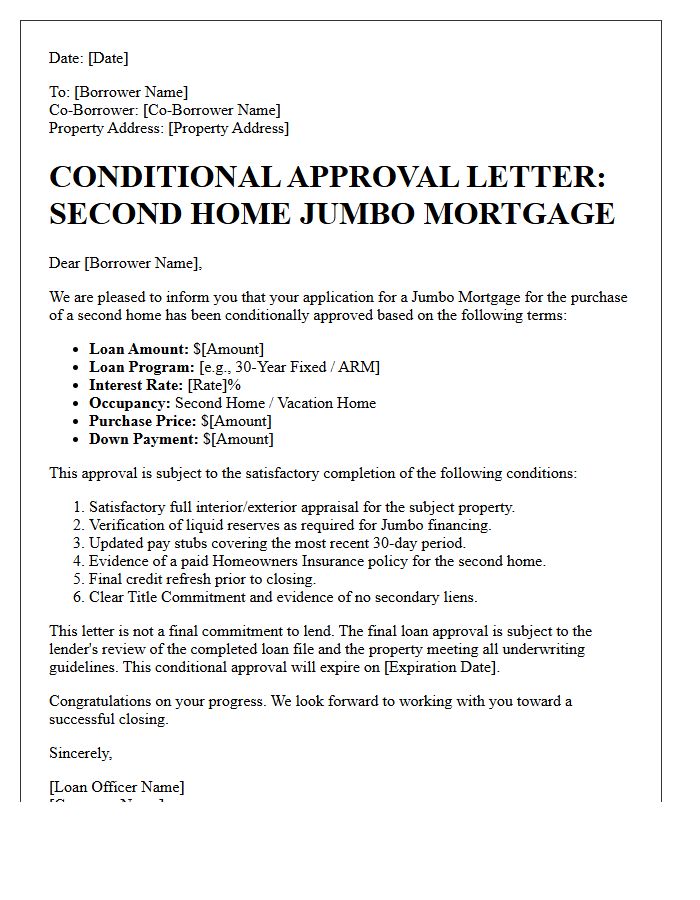

Second Home Jumbo Mortgage Conditional Approval Letter

A Second Home Jumbo Mortgage Conditional Approval Letter is a formal document from a lender indicating you meet specific underwriting criteria for a high-value property loan. It signifies that your creditworthiness, income, and assets have been verified, though final funding depends on meeting remaining conditions like a satisfactory appraisal. For jumbo loans, which exceed standard conforming limits, this letter provides sellers with financial certainty. It demonstrates that you are a qualified buyer capable of securing premium financing for a non-primary residence, strengthening your negotiating position in competitive luxury real estate markets.

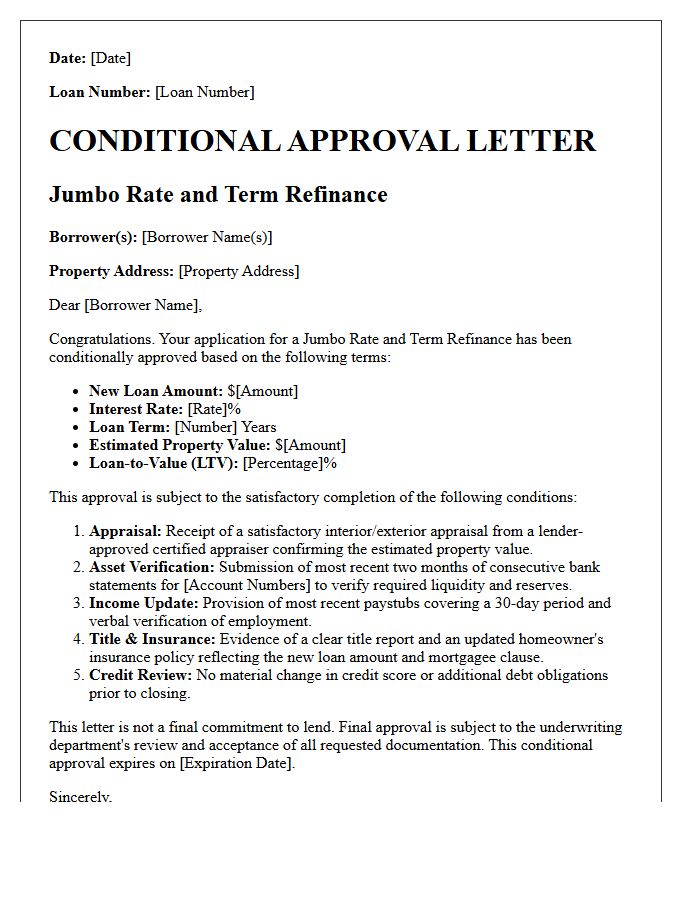

Jumbo Mortgage Rate and Term Refinance Conditional Approval Letter

A Jumbo Mortgage Rate and Term Refinance Conditional Approval Letter confirms a lender's intent to lower your interest rate or adjust loan duration for high-balance financing. Since these loans exceed conforming limits, the letter outlines specific underwriting conditions you must meet, such as updated appraisals or asset verification. Obtaining this document proves your creditworthiness and financial stability, signaling that your refinance is likely to close once all listed contingencies are cleared. It is a vital milestone in securing competitive terms for luxury or high-cost real estate debt restructuring.

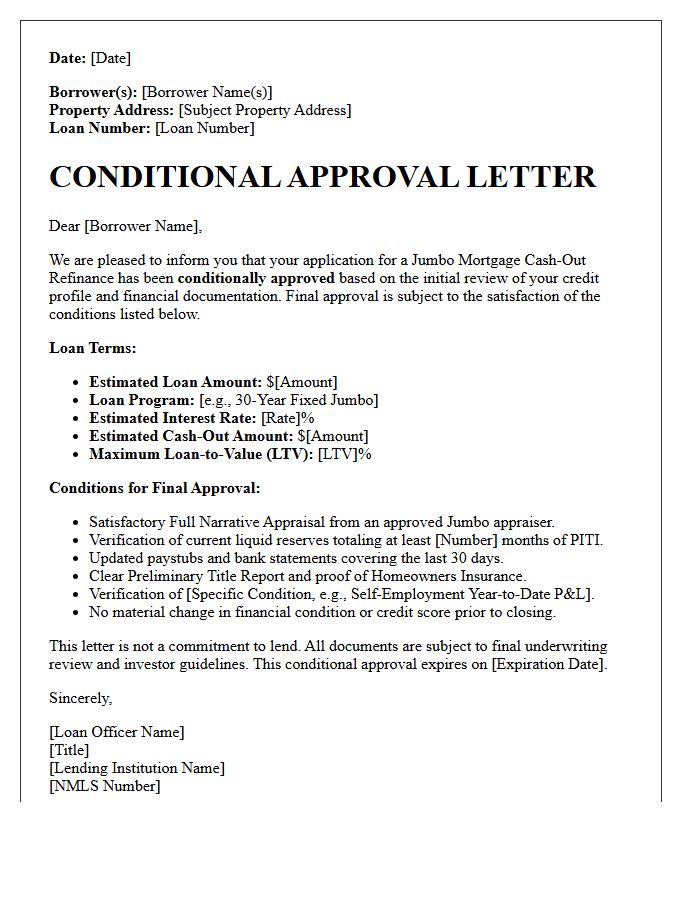

Jumbo Mortgage Cash-Out Refinance Conditional Approval Letter

A Jumbo Mortgage Cash-Out Refinance Conditional Approval Letter is a formal document from a lender indicating your refinancing application is approved pending specific underwriting requirements. Since jumbo loans exceed conforming limits, this letter confirms you meet strict debt-to-income ratios and credit score benchmarks. It details the maximum equity you can withdraw while outlining final steps like a property appraisal or income verification. Having this letter proves your financial eligibility to access large-scale liquidity against your luxury property's value before the final loan funding occurs.

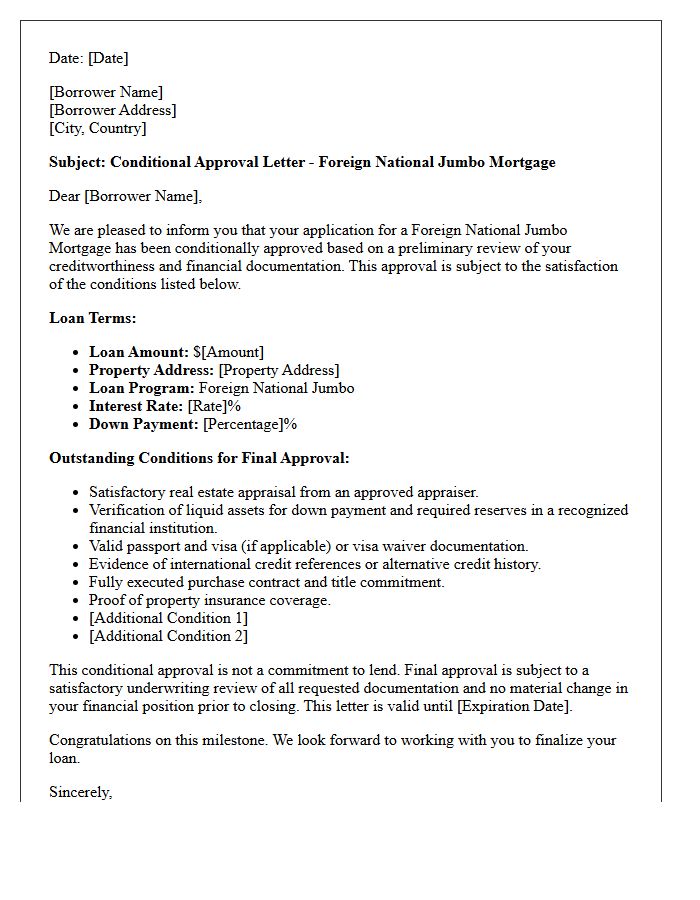

Foreign National Jumbo Mortgage Conditional Approval Letter

A Foreign National Jumbo Mortgage Conditional Approval Letter is a critical document verifying a non-resident borrower's pre-qualification for high-value financing. It confirms that a lender has reviewed your creditworthiness, liquid assets, and foreign income sources. While not a final commitment, it outlines specific conditions-such as visa verification or property appraisals-required to secure the loan. Having this letter demonstrates to sellers that you are a qualified buyer capable of closing complex, large-scale real estate transactions in the United States despite lacking a domestic credit history.

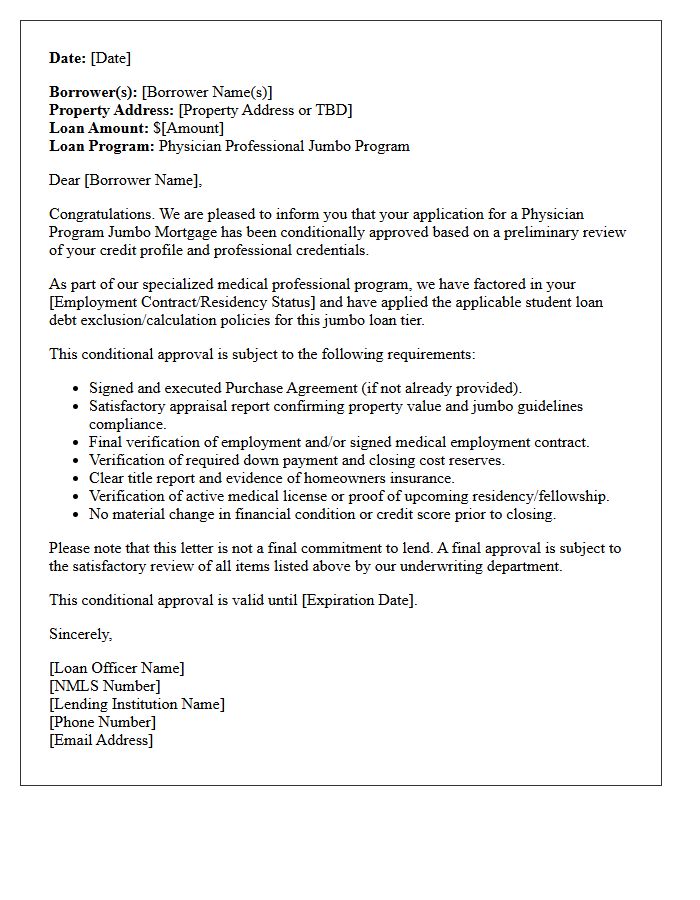

Physician Program Jumbo Mortgage Conditional Approval Letter

A Physician Program Jumbo Mortgage Conditional Approval Letter is a critical document for medical professionals seeking high-value financing. This letter confirms that a lender has preliminarily verified your specialized employment contract, credit, and debt-to-income ratio. It highlights your eligibility for low down payment options and the exclusion of student loans from qualifying calculations. Obtaining this letter demonstrates financial credibility to sellers, proving you are pre-approved for a jumbo loan despite unique residency or starting salary structures. It serves as a formal commitment pending final property appraisal and updated financial documentation.

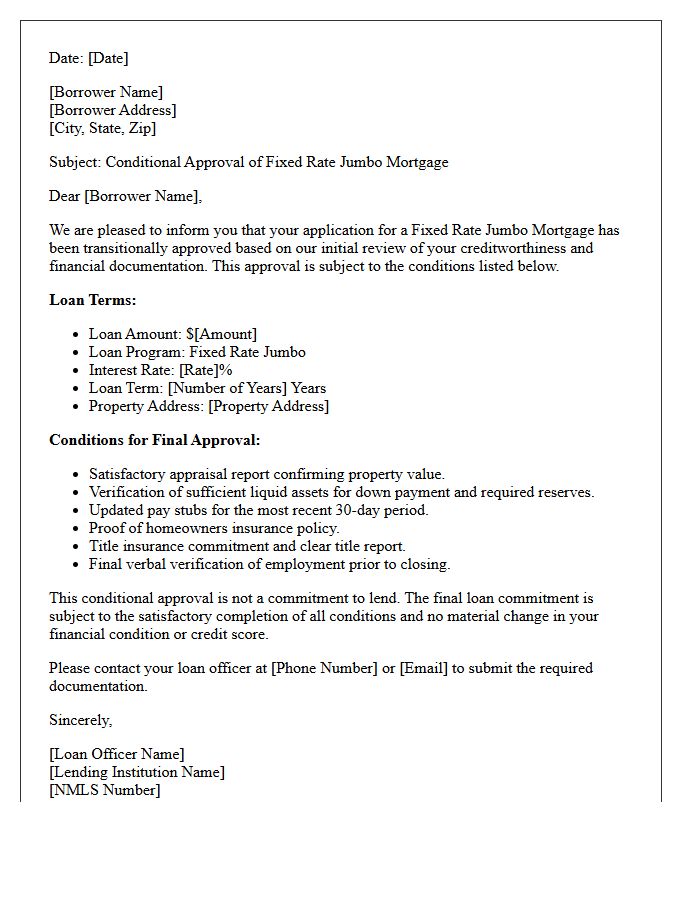

Fixed Rate Jumbo Mortgage Conditional Approval Letter

A Fixed Rate Jumbo Mortgage Conditional Approval Letter is a formal document issued by a lender after a preliminary underwriting review. It signifies that a borrower is approved for a high-value loan exceeding conforming limits, provided specific financial conditions are met. This letter strengthens your bargaining position by proving you have the verified income, assets, and credit to secure financing at a stable interest rate. However, final funding remains contingent upon a successful property appraisal and final verification of your financial status before closing.

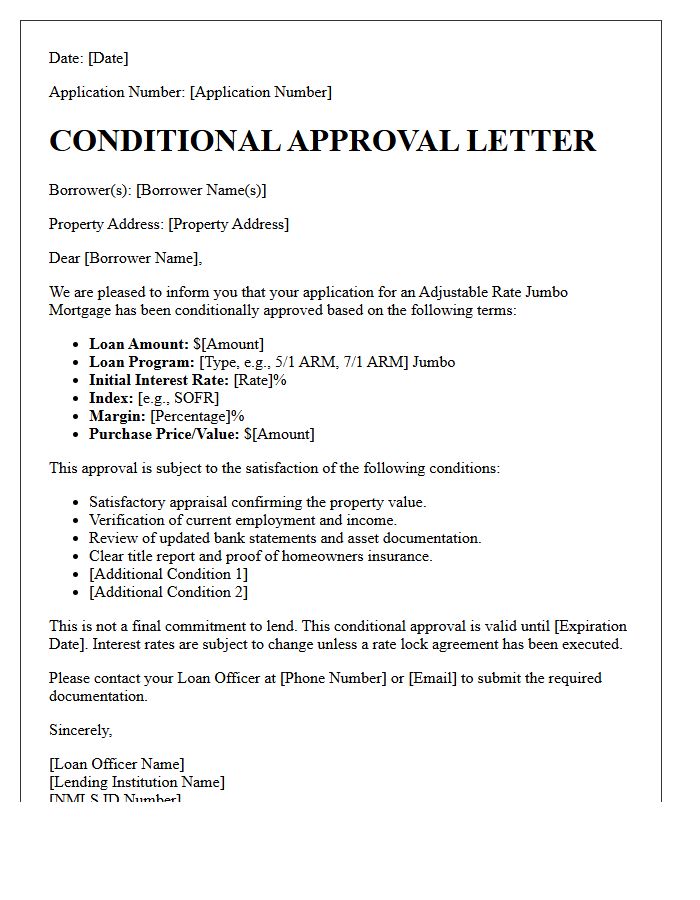

Adjustable Rate Jumbo Mortgage Conditional Approval Letter

An Adjustable Rate Jumbo Mortgage Conditional Approval Letter is a formal document indicating a lender's preliminary commitment to finance high-value properties exceeding conforming limits. It specifies a variable interest rate that adjusts after an initial fixed period. This letter confirms that your credit, assets, and income meet basic eligibility, but final funding depends on meeting specific underwriting conditions, such as a satisfactory property appraisal and verified documentation. Obtaining this letter strengthens your bargaining position in luxury real estate markets by proving financial readiness for a large-scale loan.

Portfolio Product Jumbo Mortgage Conditional Approval Letter

A Jumbo Mortgage Conditional Approval Letter is a critical document indicating a lender's preliminary commitment to financing high-value luxury real estate exceeding conforming loan limits. Issued after a rigorous underwriting review, it outlines specific conditions-such as updated appraisals, asset verification, or debt-to-income requirements-that must be met before final funding. For buyers using specialized portfolio products, this letter demonstrates financial credibility to sellers, signaling that the lender intends to hold and manage the loan internally rather than selling it on the secondary market, often allowing for flexible underwriting criteria.

What is a Jumbo Mortgage Conditional Approval Letter?

A Jumbo Mortgage Conditional Approval Letter is a formal document from a lender stating that your high-balance loan application is approved, provided you meet specific requirements. Unlike a pre-approval, this indicates that an underwriter has reviewed your financial file and determined you qualify for a loan exceeding standard conforming limits, subject to final verification.

What common conditions are listed in a Jumbo Conditional Approval?

Common conditions for jumbo loans often include updated bank statements, proof of liquidation of assets for the down payment, a satisfactory property appraisal, verification of high cash reserves (often 6-12 months of payments), and a final "soft pull" credit check to ensure your debt-to-income ratio hasn't changed.

How long does it take to receive a Jumbo Loan Conditional Approval?

The timeline for a jumbo conditional approval typically ranges from 7 to 14 business days. Because jumbo mortgages involve higher risk and larger loan amounts, the underwriting process is more rigorous than standard loans, requiring more detailed documentation of income, tax returns, and complex assets.

Does a Jumbo Mortgage Conditional Approval guarantee I will get the loan?

No, a conditional approval is not a final guarantee of funding. The loan will only close once you satisfy all the underwriter's "conditions to close." If your financial situation changes-such as taking on new debt, losing a job, or if the property appraisal comes in low-the lender may rescind the approval.

What is the difference between a Pre-Approval and a Conditional Approval for a Jumbo Loan?

A pre-approval is an initial estimate based on a preliminary review of your credit and stated income. A Jumbo Mortgage Conditional Approval is a much stronger commitment where an underwriter has fully vetted your tax returns, assets, and legal documents, moving you significantly closer to the final "Clear to Close" stage.

Comments