Receiving a Mid-Period Forbearance Status Update Letter is a critical step in managing your mortgage relief plan. This document provides an essential overview of your remaining balance and upcoming deadlines to ensure a smooth transition toward repayment or extension. Staying informed helps protect your long-term financial health. To help you draft or understand this notice, below are some ready to use template.

Image cover: Mid-Period Forbearance Status Update: Essential Letter Samples and Templates

Letter Samples List

- Standard Mid-Period Forbearance Status Update Letter

- Mid-Period Forbearance Account Review Letter

- Mid-Period Forbearance Payment Deferral Letter

- Mid-Period Forbearance Repayment Plan Options Letter

- Mid-Period Forbearance Hardship Reassessment Letter

- Mid-Period Forbearance Expiration Warning Letter

- Mid-Period Forbearance Loss Mitigation Transition Letter

- Mid-Period Forbearance Escrow Account Analysis Letter

- Mid-Period Forbearance Outstanding Balance Notification Letter

- Mid-Period Forbearance Post-Disaster Status Update Letter

- Mid-Period Forbearance Credit Reporting Informational Letter

- Mid-Period Forbearance Modification Assessment Letter

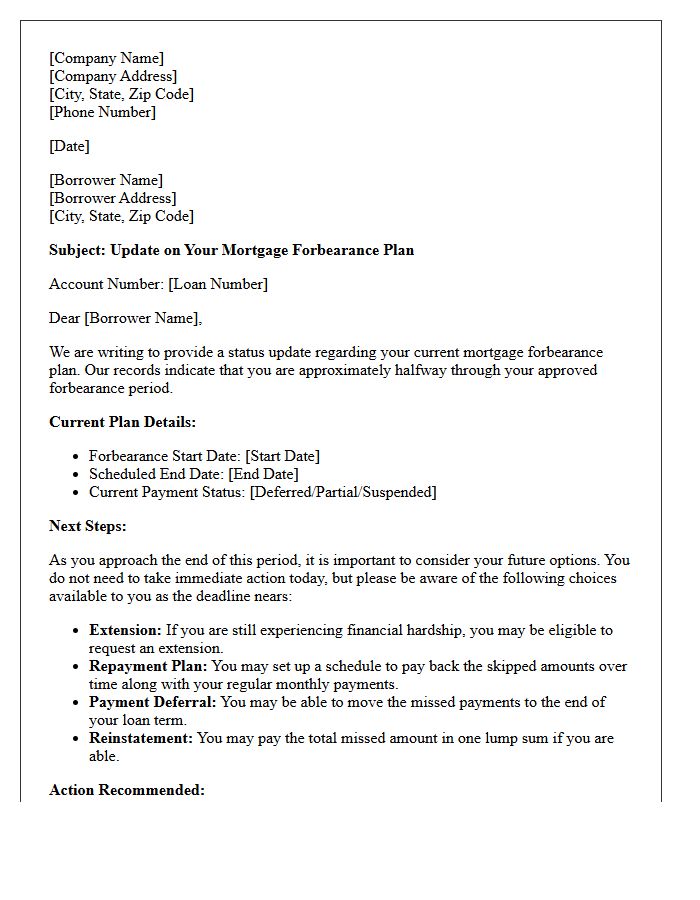

Standard Mid-Period Forbearance Status Update Letter

A Standard Mid-Period Forbearance Status Update Letter is a critical communication sent by mortgage servicers to homeowners during a forbearance plan. This document provides a timely account summary, detailing the remaining duration of the pause and total missed payments. It ensures borrowers understand their upcoming obligations and available repayment options, such as deferrals or loan modifications. Receiving this letter serves as a vital reminder to evaluate your financial situation before the relief period expires to avoid foreclosure and maintain long-term housing stability.

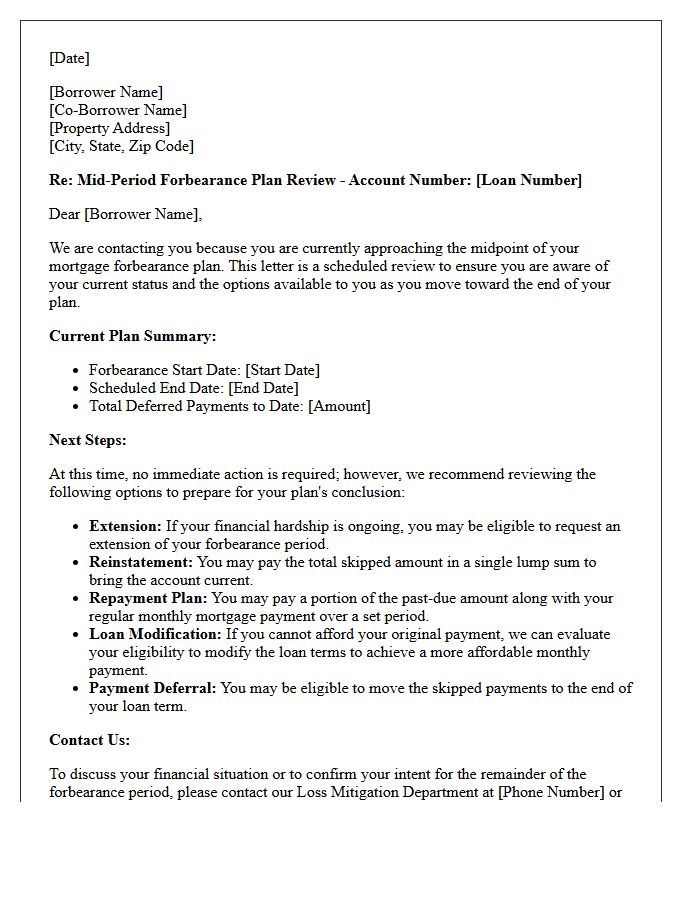

Mid-Period Forbearance Account Review Letter

A Mid-Period Forbearance Account Review Letter is a critical communication from your mortgage servicer used to evaluate your financial status during a loss mitigation plan. This document ensures you are on track to complete your temporary payment relief while identifying long-term repayment options. It is essential to respond promptly to this review to avoid potential foreclosure and to determine if you qualify for a formal loan modification or an extension of your current assistance period. Accurate documentation is required to finalize your post-forbearance strategy.

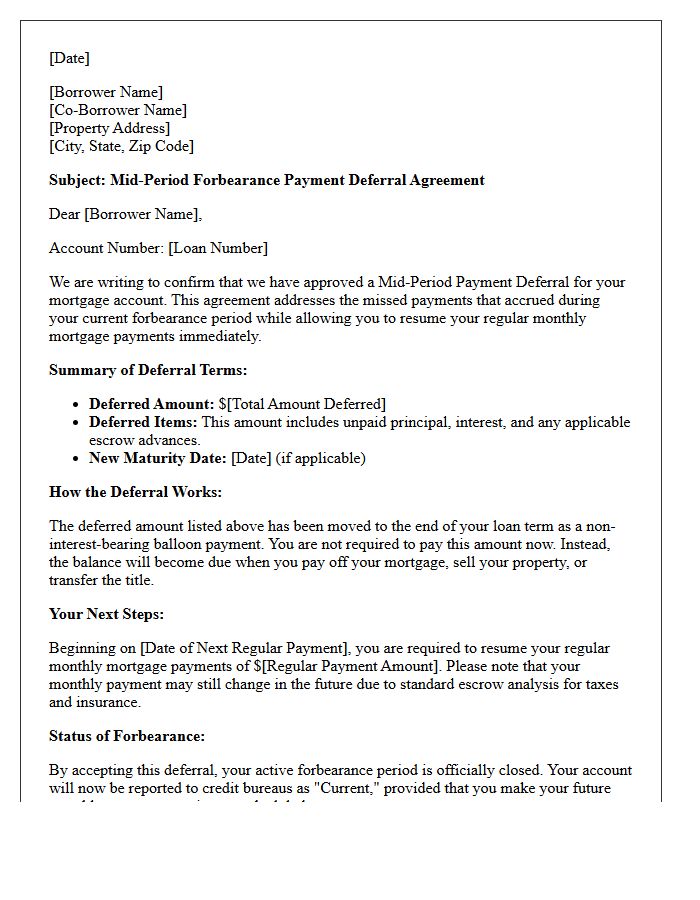

Mid-Period Forbearance Payment Deferral Letter

A Mid-Period Forbearance Payment Deferral Letter is a critical notice confirming that your missed mortgage payments are moved to the end of the loan term. This deferral allows you to resume regular monthly payments immediately without paying a lump sum. The most important thing to know is that while it resolves delinquency, the deferred balance becomes a non-interest-bearing lien payable upon home sale, refinance, or loan maturity. Review the letter carefully to ensure your repayment terms and escrow adjustments are accurately documented to maintain long-term financial stability.

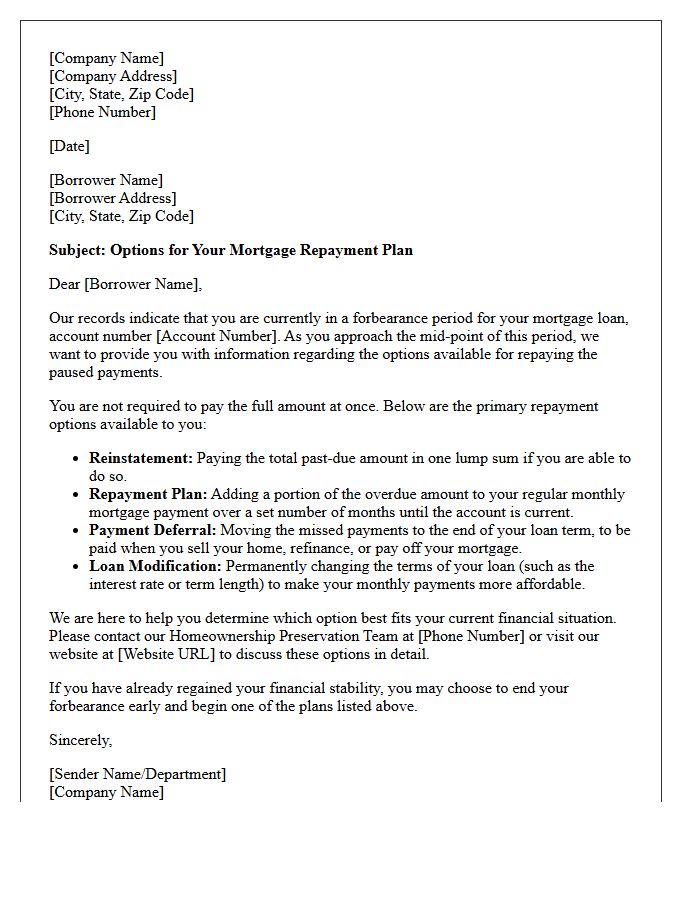

Mid-Period Forbearance Repayment Plan Options Letter

A Mid-Period Forbearance Repayment Plan Options Letter provides essential guidance for homeowners exiting a mortgage forbearance. This document outlines specific repayment strategies to address missed payments. Key options typically include a repayment plan to catch up gradually, a payment deferral moving the balance to the end of the loan, or a formal loan modification. Understanding these loss mitigation choices is crucial for maintaining housing stability. Borrowers should review the letter immediately to select the best option for their financial situation and avoid potential foreclosure proceedings.

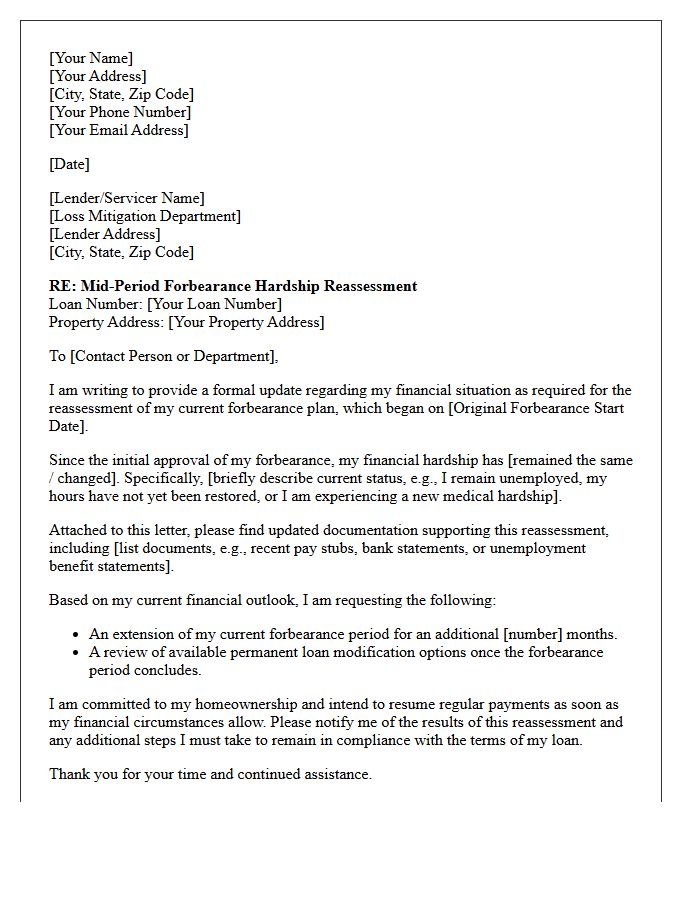

Mid-Period Forbearance Hardship Reassessment Letter

A Mid-Period Forbearance Hardship Reassessment Letter is a critical communication sent by mortgage servicers to evaluate a borrower's ongoing financial stability. This document requires you to confirm if your financial hardship persists or if your situation has improved. It is the most important step for determining eligibility for further payment relief or a permanent loan modification. Timely response is essential to avoid delinquency, as it allows lenders to transition you from temporary assistance to a sustainable long-term repayment plan, ensuring you retain your home and maintain credit health.

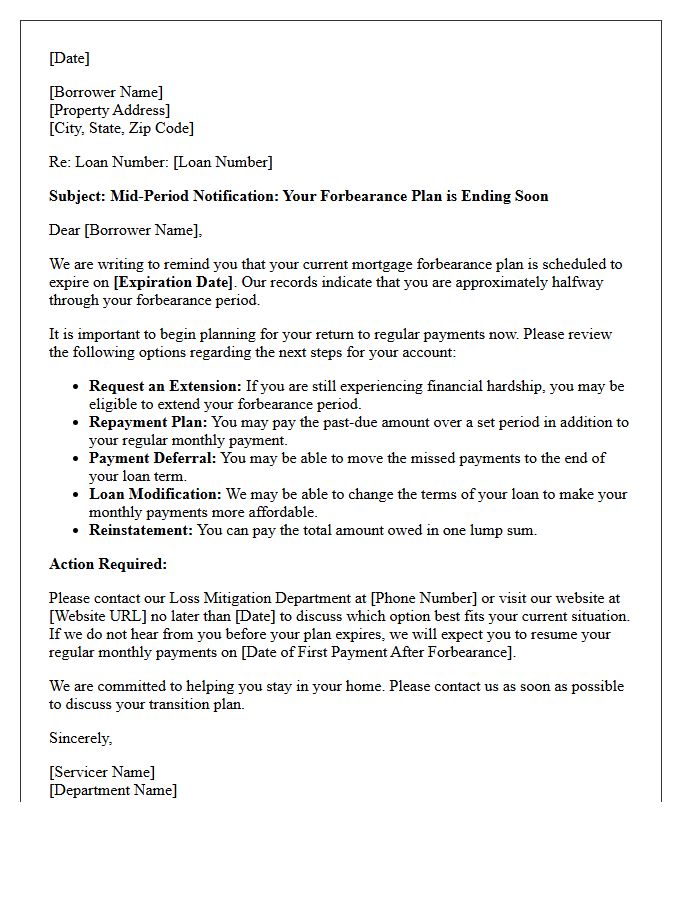

Mid-Period Forbearance Expiration Warning Letter

A Mid-Period Forbearance Expiration Warning Letter is a critical notice sent by mortgage servicers to homeowners nearing the end of their temporary payment pause. This document acts as a final notice to help borrowers prepare for resuming monthly payments. It outlines available loss mitigation options, such as loan modifications or repayment plans, to prevent default. Understanding this letter is essential for maintaining homeownership, as it provides a clear timeline for when the forbearance period concludes and details the specific actions required to transition back to regular billing cycles effectively.

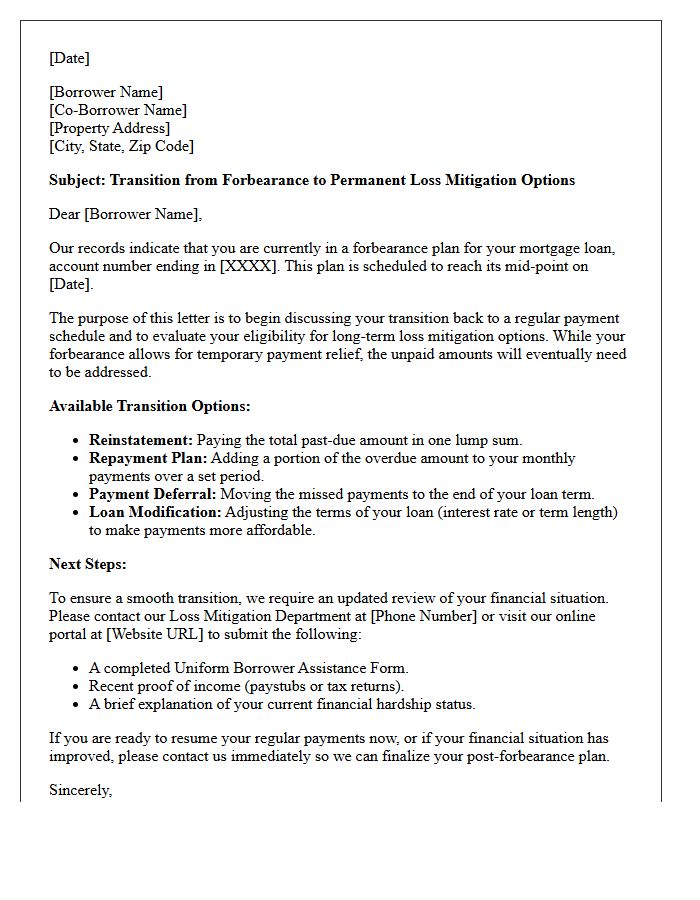

Mid-Period Forbearance Loss Mitigation Transition Letter

A Mid-Period Forbearance Loss Mitigation Transition Letter is a critical notice sent to borrowers during their forbearance plan. It explains that the temporary payment pause is ending and outlines available loss mitigation options to resolve missed payments. This document serves as a bridge to long-term stability, detailing steps for a loan modification, deferral, or repayment plan. Timely action is essential to avoid foreclosure and ensure a smooth transition back to regular monthly installments while maintaining homeownership eligibility through specific servicer guidelines and federal requirements.

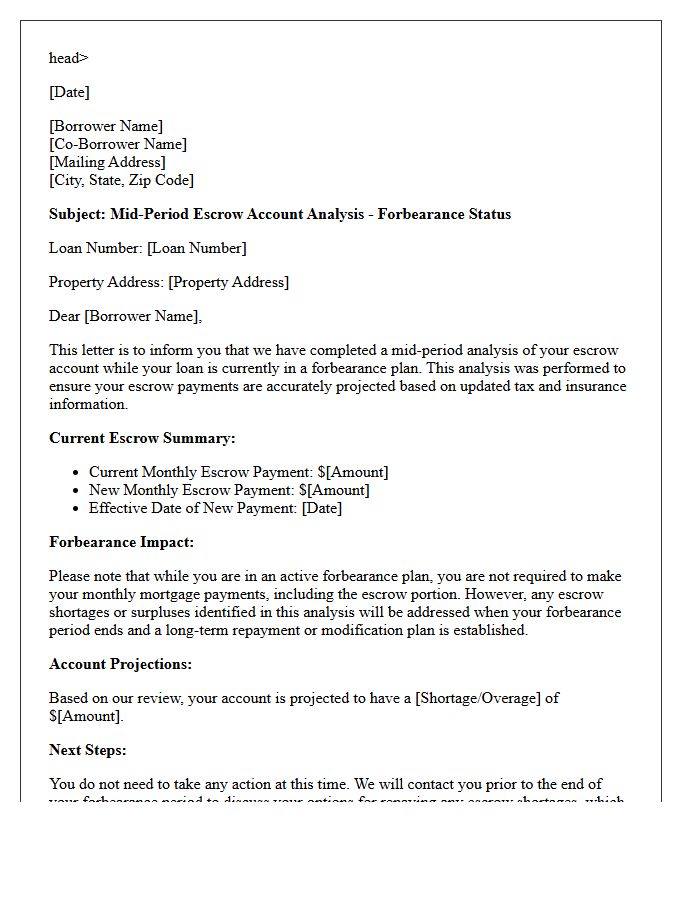

Mid-Period Forbearance Escrow Account Analysis Letter

A Mid-Period Forbearance Escrow Account Analysis Letter is a critical notice sent when your mortgage assistance ends. It details how escrow shortages or surpluses resulting from paused payments will affect your future housing costs. The analysis calculates new monthly payment amounts by incorporating missed taxes or insurance premiums. Reviewing this document is essential to understand your repayment options, as it explains whether you can pay the deficiency upfront or spread it over a new payment schedule to maintain financial stability.

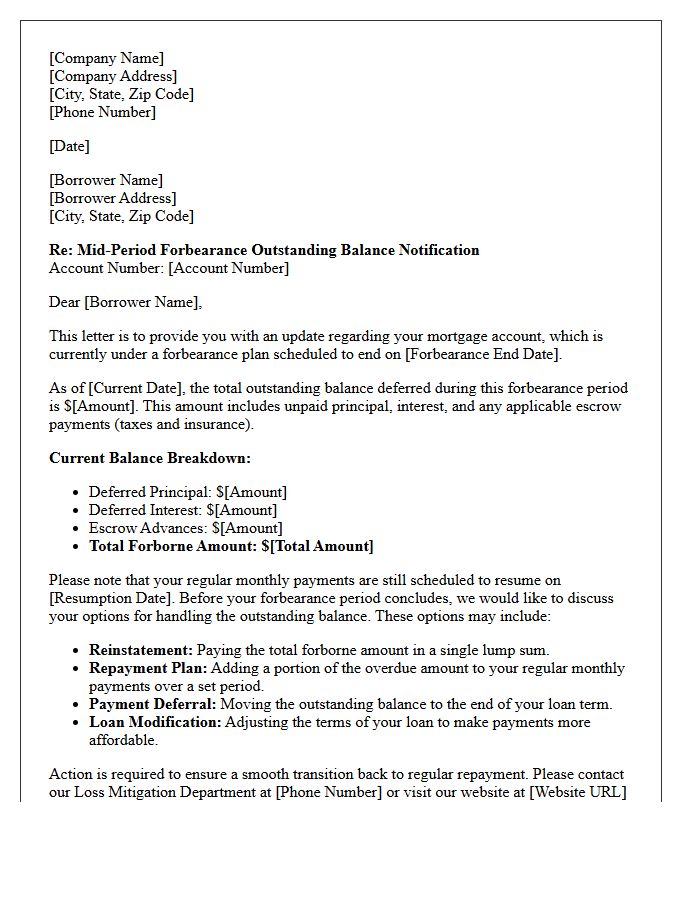

Mid-Period Forbearance Outstanding Balance Notification Letter

A Mid-Period Forbearance Outstanding Balance Notification Letter is a critical mortgage compliance document sent to borrowers during an active repayment pause. This notice provides a real-time statement of the total unpaid interest and principal deferred to date. Its primary purpose is to ensure financial transparency, helping homeowners understand their accumulating debt before the plan expires. Reviewing this letter is essential for effective loss mitigation planning and selecting the right repayment option, such as a loan modification or deferral, to avoid future default or foreclosure risks.

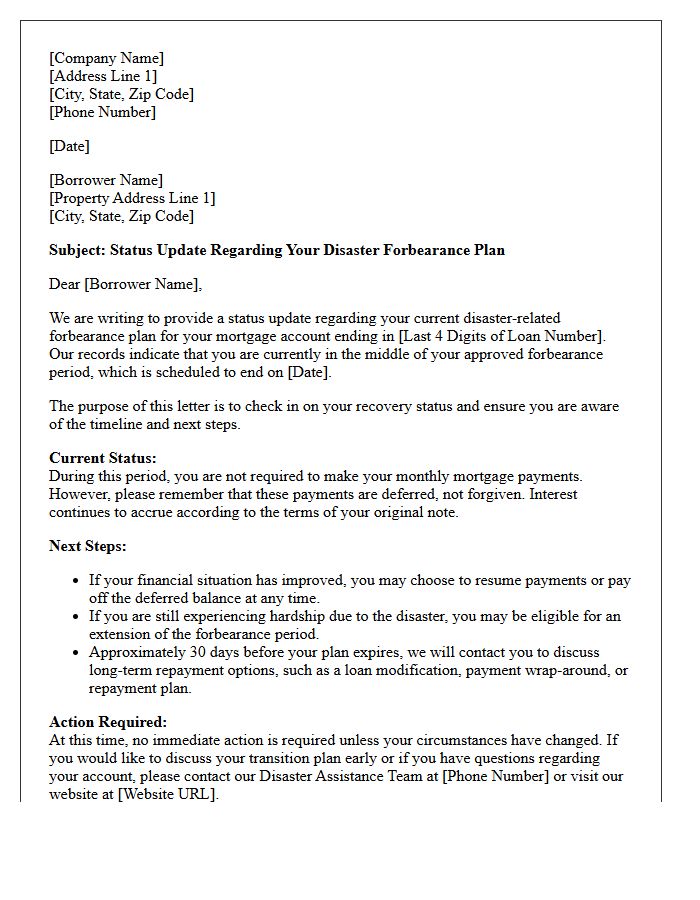

Mid-Period Forbearance Post-Disaster Status Update Letter

A Mid-Period Forbearance Post-Disaster Status Update Letter is a compliance notification sent to borrowers during an active disaster-related payment pause. Its primary purpose is to provide a status update regarding the remaining duration of the relief period. This letter outlines available loss mitigation options and emphasizes the importance of contacting the servicer to discuss long-term repayment plans. Proactive communication helps homeowners understand their obligations before the forbearance expires, ensuring a smoother transition back to regular payments or permanent loan modifications following a natural disaster.

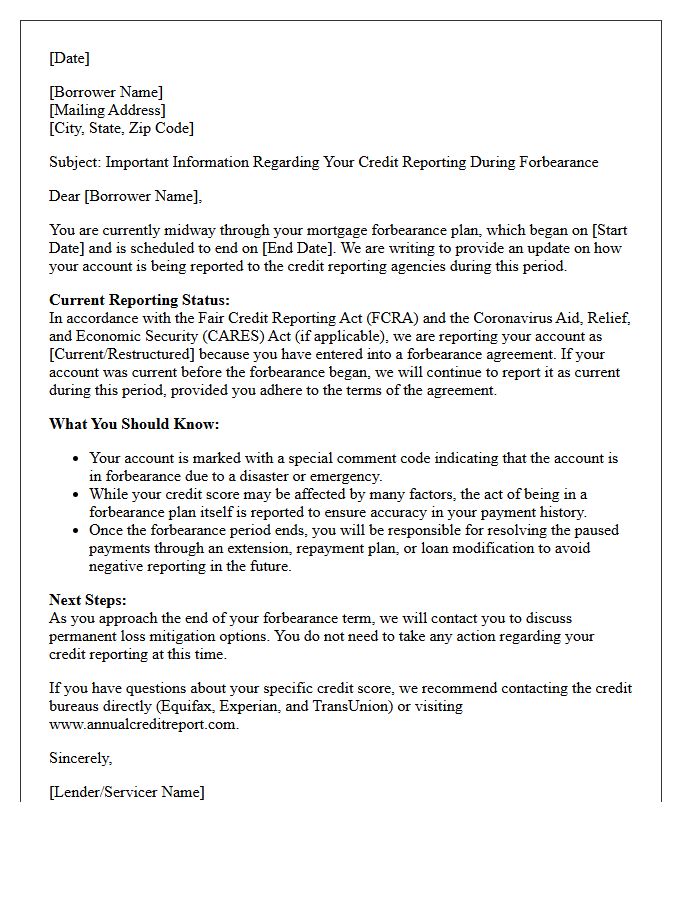

Mid-Period Forbearance Credit Reporting Informational Letter

The Mid-Period Forbearance Credit Reporting Informational Letter clarifies how lenders report your payment status during COVID-19 relief. It ensures that if your account was current before entering a plan, it remains reported as current. This document is vital for protecting your credit score while managing financial hardship. It outlines specific reporting guidelines under the CARES Act, preventing negative delinquency marks on your history during the forbearance period. Reviewing this letter helps homeowners verify that their mortgage servicer is accurately reflecting their payment status to credit bureaus.

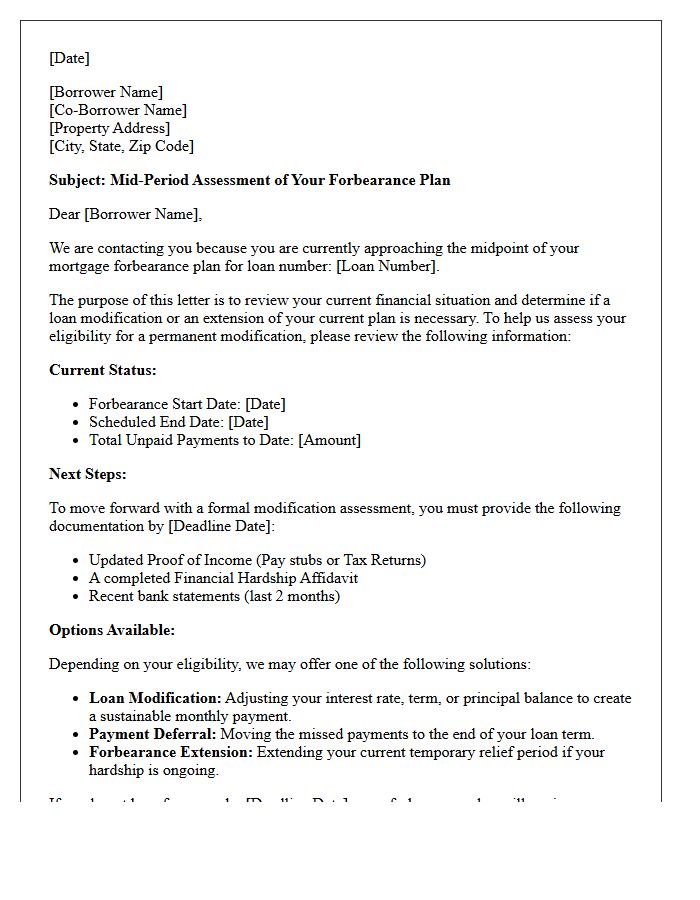

Mid-Period Forbearance Modification Assessment Letter

A Mid-Period Forbearance Modification Assessment Letter is a formal notice sent to borrowers evaluating their eligibility for a permanent loan modification before the initial relief period ends. This document analyzes financial stability to determine if reduced monthly payments or adjusted interest rates are sustainable. It serves as a critical bridge for homeowners transitioning from temporary payment suspension to long-term recovery. Reviewing this assessment is essential to understand specific repayment options, preventing potential foreclosure by securing a modified agreement that aligns with current income and ensures continued property ownership.

What is a Mid-Period Forbearance Status Update Letter?

A Mid-Period Forbearance Status Update Letter is a formal notification sent by mortgage servicers to borrowers during their forbearance term to provide an update on their account status, remaining duration of the plan, and available repayment options.

When will I receive my Mid-Period Forbearance Status Update?

Most loan servicers send this update letter approximately halfway through your scheduled forbearance period or 30 to 60 days before your current plan is set to expire to ensure you have adequate time to plan for next steps.

What should I do after receiving a forbearance status update letter?

You should review the letter to confirm your plan's expiration date and contact your mortgage servicer to either request an extension, if eligible, or discuss a repayment plan such as a deferral, loan modification, or reinstatement.

Does receiving this update letter mean my forbearance is ending immediately?

No, the mid-period update is not a cancellation notice. It is a proactive communication designed to inform you of your progress and remind you of the upcoming deadline to transition back to regular payments or apply for further assistance.

Can I request an extension after receiving a Mid-Period Forbearance Status Update?

Yes, if you are still experiencing financial hardship, you can use the contact information provided in the letter to request an extension of your forbearance, provided you have not yet reached the maximum limit allowed by your loan type or investor guidelines.

Comments