A Post-Forbearance Reinstatement Amount Notice informs borrowers of the total past-due balance required to bring their mortgage current after a forbearance period ends. This formal communication details missed payments, fees, and the deadline for lump-sum repayment to avoid default. Understanding these requirements is essential for maintaining homeownership and evaluating alternative repayment options. Below are some ready to use templates.

Image cover: Official Reinstatement Amount Notice Templates and Communication Guide

Letter Samples List

- Standard Post-Forbearance Reinstatement Amount Notice Letter

- Initial Post-Forbearance Reinstatement Amount Notice Letter

- Updated Post-Forbearance Reinstatement Amount Notice Letter

- Final Post-Forbearance Reinstatement Amount Notice Letter

- Urgent Post-Forbearance Reinstatement Amount Demand Letter

- Loss Mitigation Post-Forbearance Reinstatement Amount Letter

- Conventional Loan Post-Forbearance Reinstatement Amount Letter

- FHA Post-Forbearance Reinstatement Amount Notice Letter

- VA Post-Forbearance Reinstatement Amount Notice Letter

- Partial Payment Post-Forbearance Reinstatement Amount Letter

- Post-Forbearance Reinstatement Amount Calculation Letter

- Post-Forbearance Reinstatement Amount Expiration Notice Letter

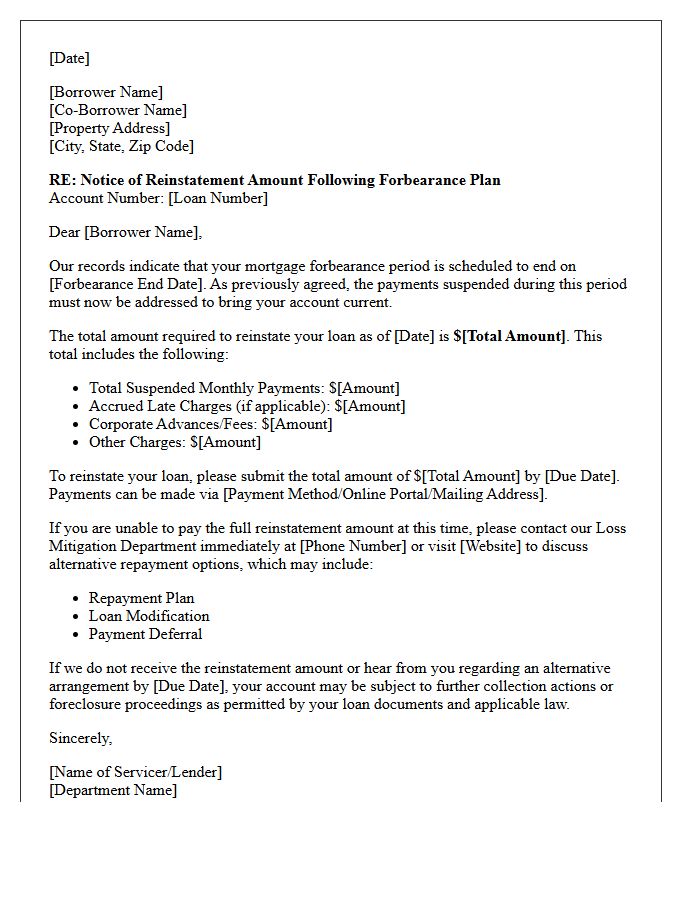

Standard Post-Forbearance Reinstatement Amount Notice Letter

A Standard Post-Forbearance Reinstatement Amount Notice Letter is a critical document sent to borrowers after a mortgage pause. It details the total delinquency amount required to bring the loan current immediately. This notice outlines specific payment instructions, deadlines, and the reinstatement figures, including missed principal, interest, and escrow advances. Understanding this letter is essential for homeowners to avoid foreclosure proceedings by either paying the lump sum or transitioning into a repayment plan or loan modification to resolve the outstanding debt balance effectively.

Initial Post-Forbearance Reinstatement Amount Notice Letter

The Initial Post-Forbearance Reinstatement Amount Notice Letter is a critical document sent by mortgage servicers after a period of payment suspension. It informs homeowners of the total past-due balance required to bring the loan current immediately. This notice outlines available repayment options, such as deferrals or loan modifications, to avoid foreclosure. It serves as a formal transition from temporary relief to a permanent loss mitigation solution, ensuring borrowers understand their financial obligations and the specific reinstatement deadline to maintain their property ownership rights.

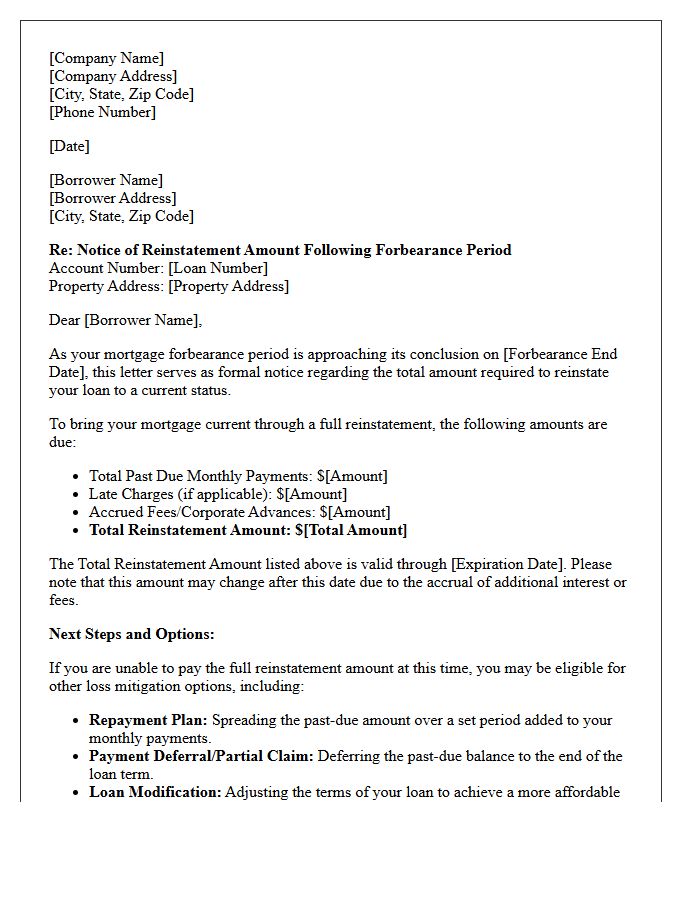

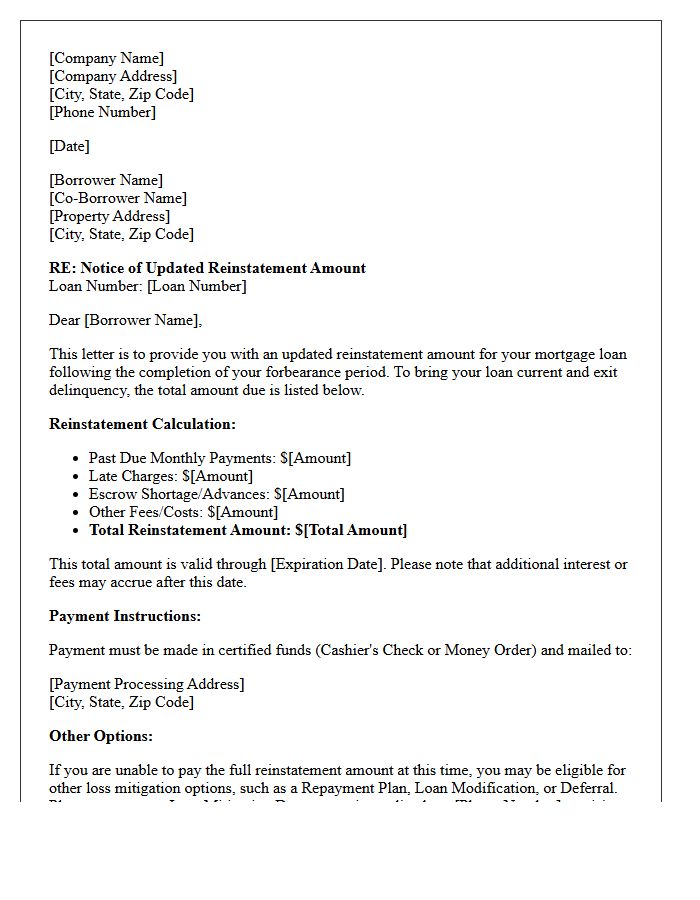

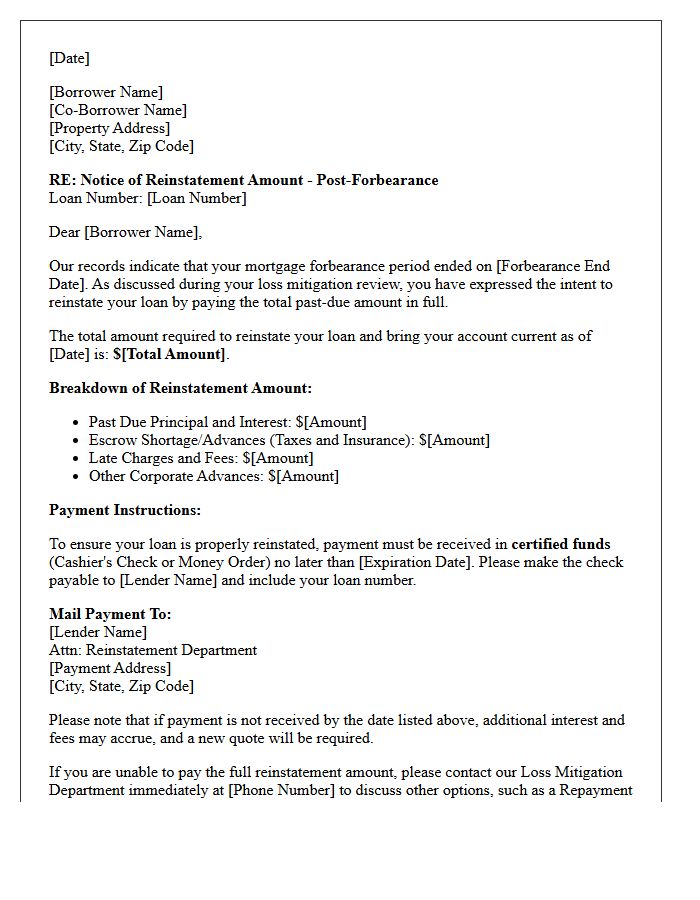

Updated Post-Forbearance Reinstatement Amount Notice Letter

The Updated Post-Forbearance Reinstatement Amount Notice Letter is a critical communication informing borrowers of the exact repayment total required to restore their mortgage status. This document outlines the total delinquency, including missed principal, interest, and escrow advances accrued during the pause. Understanding this figure is essential for transitioning to a permanent loss mitigation solution or avoiding foreclosure. Borrowers must review the reinstatement deadline and payment instructions carefully to ensure their account returns to good standing after the forbearance period officially expires.

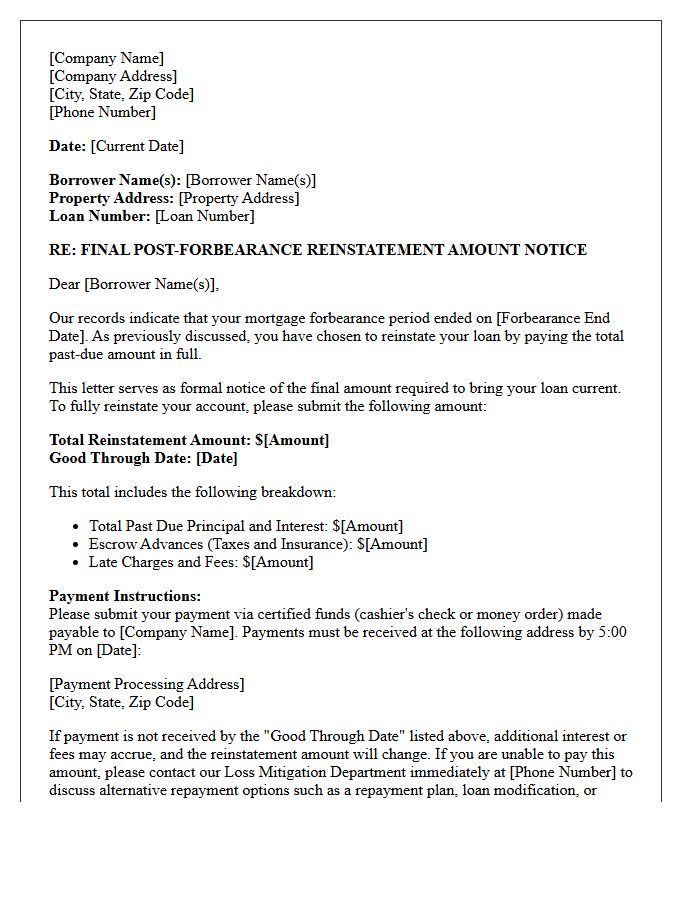

Final Post-Forbearance Reinstatement Amount Notice Letter

A Final Post-Forbearance Reinstatement Amount Notice Letter is a critical document sent by mortgage lenders following a forbearance period. It specifies the total past-due balance required to bring the loan current immediately. This notice outlines repayment options, including lump-sum payments, deferrals, or loan modifications. Homeowners must review this letter carefully to understand their financial obligations and deadlines to avoid potential foreclosure proceedings. Proper communication with your loan servicer at this stage is essential for maintaining homeownership and securing a sustainable long-term repayment solution.

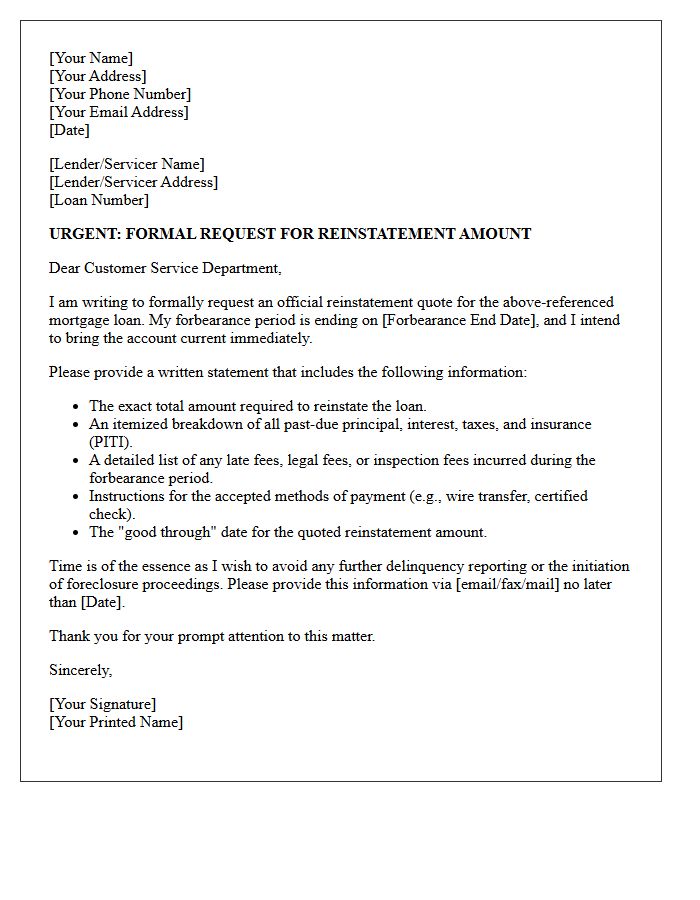

Urgent Post-Forbearance Reinstatement Amount Demand Letter

An Urgent Post-Forbearance Reinstatement Amount Demand Letter is a critical legal notice issued by mortgage servicers when a relief period ends. This document specifies the total past-due balance required to bring the loan current immediately. Homeowners must review this letter to understand their repayment deadlines and avoid potential foreclosure proceedings. It outlines the reinstatement figures, including principal, interest, and fees. Promptly contacting your lender to discuss loss mitigation options, such as loan modifications or repayment plans, is essential to protecting your property rights and financial stability.

Loss Mitigation Post-Forbearance Reinstatement Amount Letter

A Loss Mitigation Post-Forbearance Reinstatement Amount Letter is a formal notice sent by loan servicers to homeowners exiting a COVID-19 or traditional pause. It details the total delinquency required to bring the mortgage current in a single payment. Understanding this document is critical because it outlines your reinstatement options, deadline dates, and potential late fees. If you cannot afford the full amount, this letter serves as the starting point for negotiating loan modifications or payment plans to prevent foreclosure and ensure long-term housing stability.

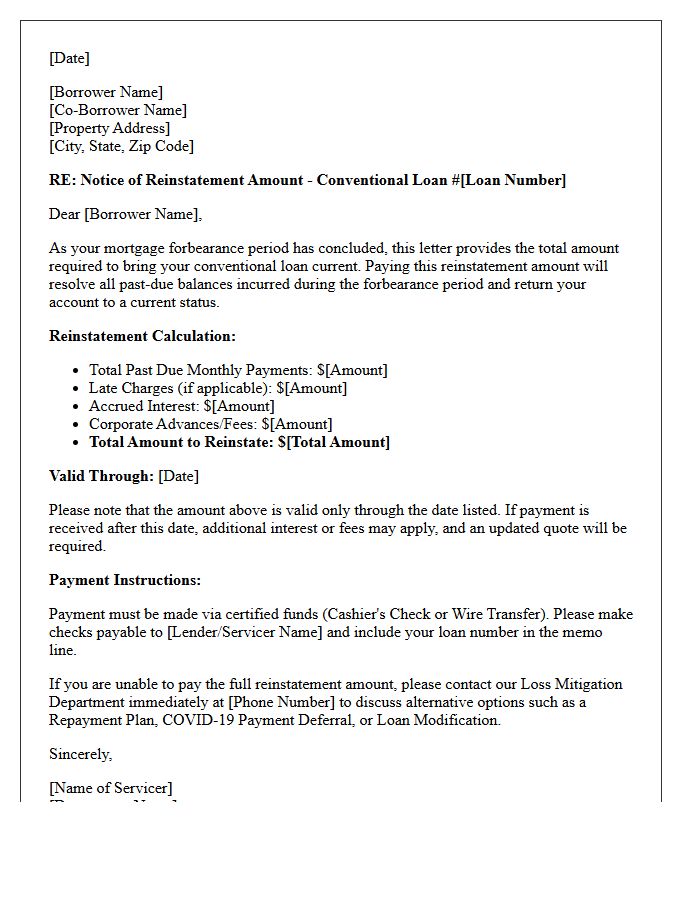

Conventional Loan Post-Forbearance Reinstatement Amount Letter

A Conventional Loan Post-Forbearance Reinstatement Amount Letter is a formal document detailing the total sum required to bring a delinquent mortgage current after a forbearance period ends. It explicitly lists the past-due principal, interest, escrow shortages, and any late fees. This letter is crucial for homeowners opting for reinstatement, as it provides a specific deadline and payment instructions. Understanding this amount ensures the loan returns to "performing" status, effectively stopping potential foreclosure actions and verifying the exact financial obligation needed to satisfy the lender's requirements immediately.

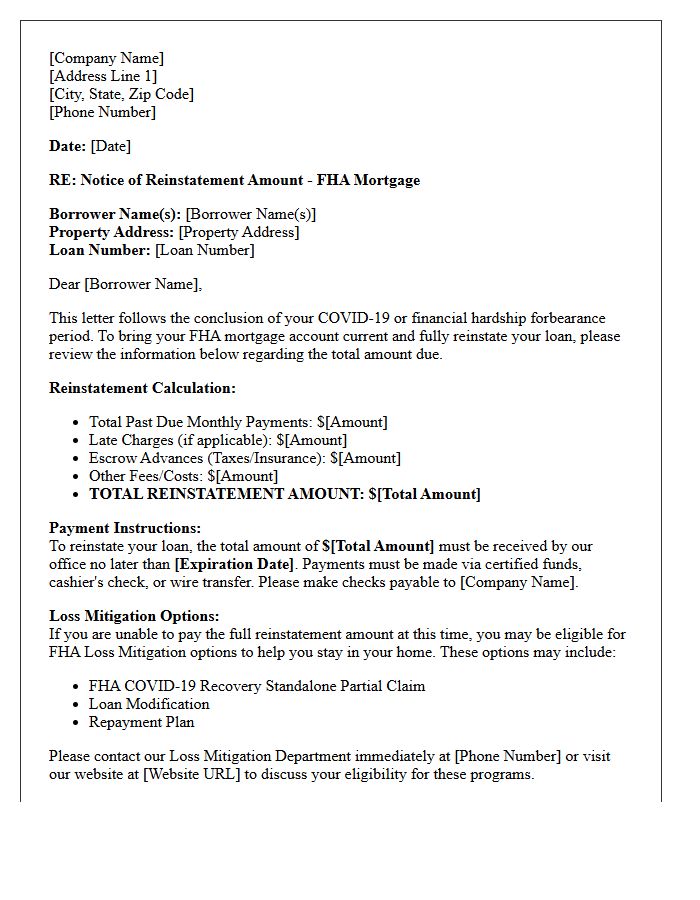

FHA Post-Forbearance Reinstatement Amount Notice Letter

An FHA Post-Forbearance Reinstatement Amount Notice Letter is a critical document sent by servicers to homeowners exiting a COVID-19 recovery period. It specifies the total delinquent balance required to bring the mortgage current immediately. While reinstatement is one option, the letter must also outline alternative loss mitigation strategies, such as a partial claim or loan modification. Borrowers must review this notice to understand their exact repayment obligations and legal deadlines to avoid foreclosure proceedings after their protected forbearance period concludes. Understanding these figures is essential for maintaining long-term homeownership.

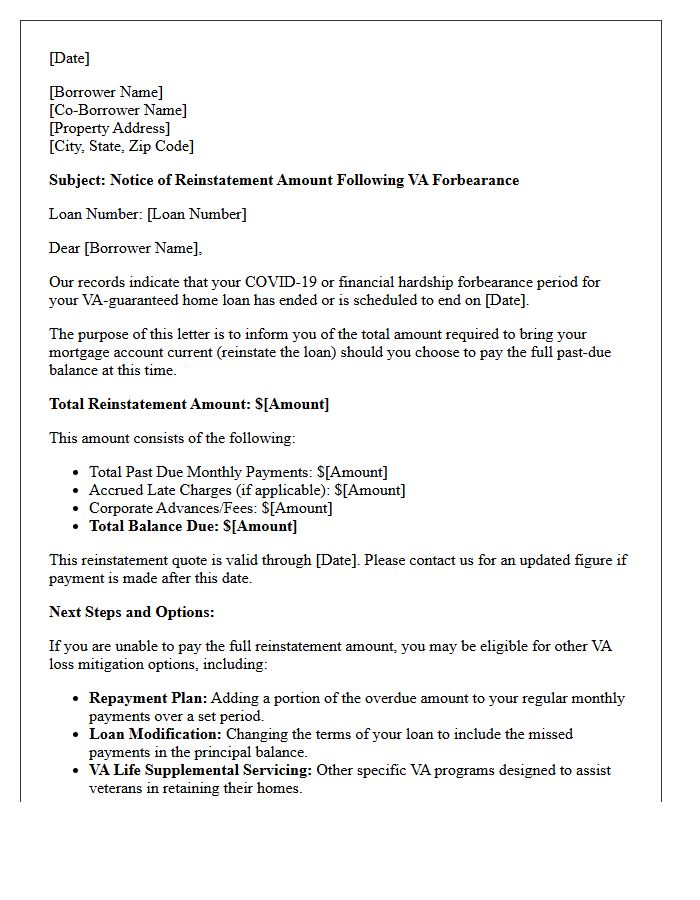

VA Post-Forbearance Reinstatement Amount Notice Letter

A VA Post-Forbearance Reinstatement Amount Notice Letter is a critical document sent by your mortgage servicer after a COVID-19 pause. This letter specifies the reinstatement amount required to bring your loan current. It details the total past-due balance, including principal, interest, and any applicable fees. Understanding this notice is vital because the Department of Veterans Affairs offers various loss mitigation options, such as repayment plans or loan modifications, to help veterans avoid foreclosure if they cannot pay the full amount immediately upon the forbearance period ending.

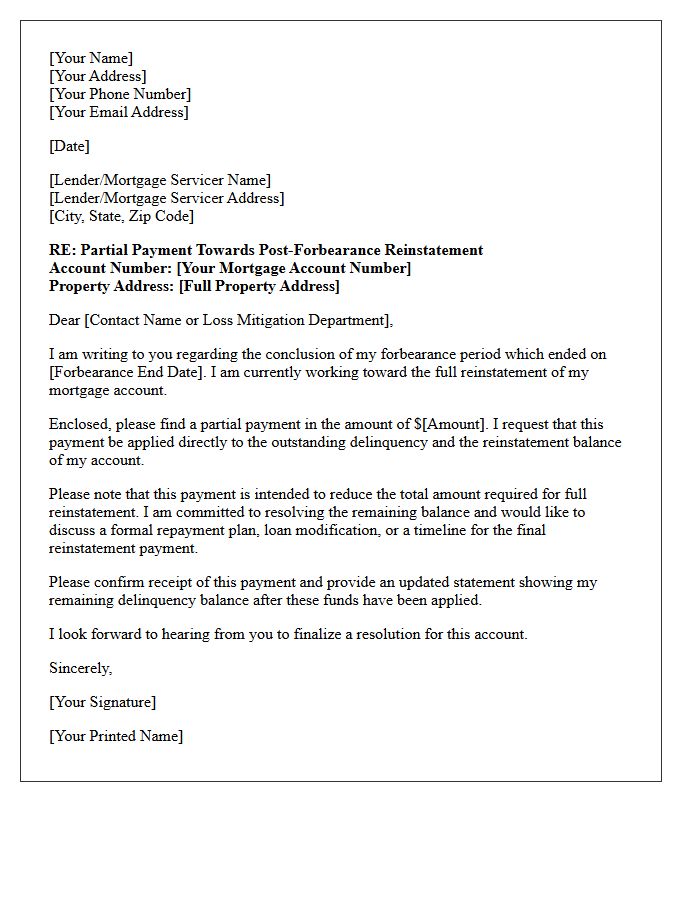

Partial Payment Post-Forbearance Reinstatement Amount Letter

A Partial Payment Post-Forbearance Reinstatement Amount Letter informs borrowers of the remaining balance required to fully reinstate their mortgage after a forbearance period ends. It highlights that a partial payment was received but was insufficient to cure the total delinquency. This document is essential for financial transparency, outlining the exact outstanding funds, applicable late fees, and legal costs needed to bring the account current. Failure to pay the specified amount may result in continued foreclosure proceedings or the requirement to enter a formal loss mitigation repayment plan.

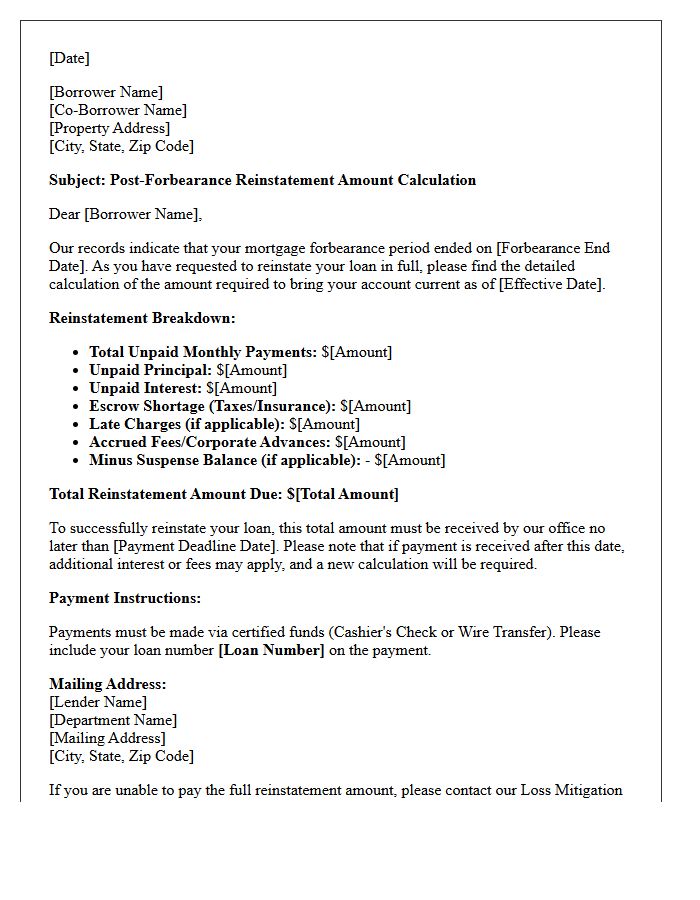

Post-Forbearance Reinstatement Amount Calculation Letter

A Post-Forbearance Reinstatement Amount Calculation Letter provides a detailed breakdown of the total delinquent balance owed after a pause in payments. This document outlines the reinstatement figure, including missed principal, interest, and escrow advances. It is essential for homeowners to verify these calculations to ensure accuracy before making a lump-sum payment. Understanding this statement helps borrowers transition into long-term repayment plans or loan modifications, preventing potential foreclosure actions. Always review the specified due date to maintain legal compliance and protect your home equity effectively.

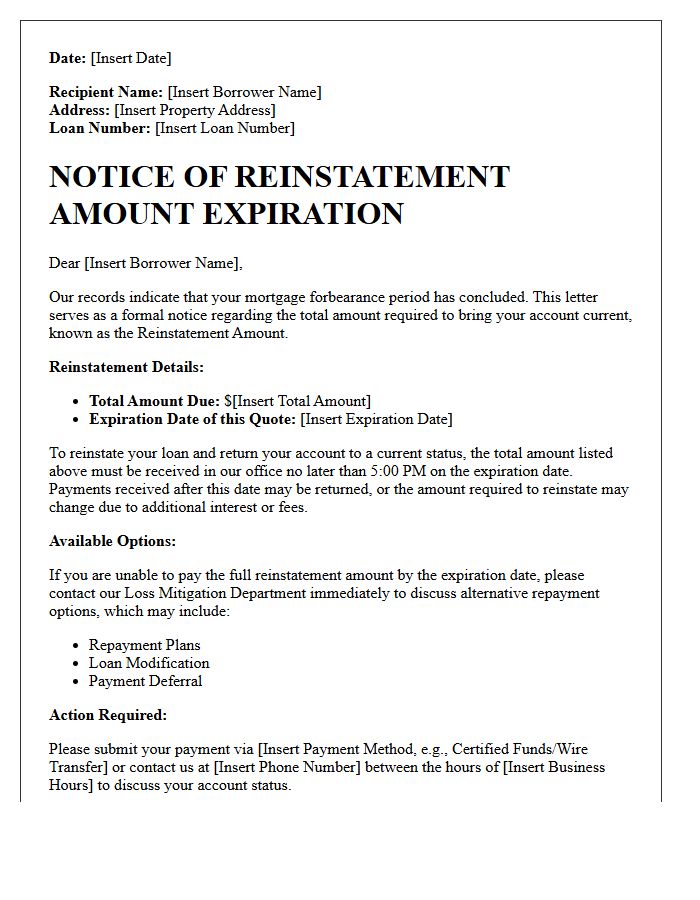

Post-Forbearance Reinstatement Amount Expiration Notice Letter

A Post-Forbearance Reinstatement Amount Expiration Notice Letter is a critical legal notification sent to homeowners. It specifies the deadline by which you must pay the total past-due balance to restore your mortgage status. This notice outlines the exact reinstatement amount, including missed principal, interest, and late fees accrued during the pause. Failure to act or secure a loss mitigation option, such as a loan modification or repayment plan, before this window closes may result in the lender initiating foreclosure proceedings to recover the debt.

What is a Post-Forbearance Reinstatement Amount Notice?

A Post-Forbearance Reinstatement Amount Notice is a formal document sent by a mortgage servicer notifying the borrower of the total past-due amount required to bring the loan current immediately following the conclusion of a forbearance period.

What costs are included in the reinstatement amount?

The reinstatement amount typically includes the sum of all skipped monthly principal and interest payments, escrow shortages for taxes and insurance, and any applicable late fees or corporate advances incurred during the forbearance term.

When must the reinstatement amount be paid?

Unless a borrower qualifies for a different loss mitigation option-such as a loan modification, payment deferral, or repayment plan-the full reinstatement amount is generally due by the expiration date specified in the notice to avoid further delinquency or foreclosure proceedings.

Does receiving this notice mean I am in foreclosure?

No, the notice itself is a disclosure of the amount owed to cure the delinquency. However, failure to address the reinstatement amount or secure an alternative workout plan by the deadline may result in the servicer initiating the foreclosure process.

Can I negotiate the amount shown on the Post-Forbearance Reinstatement Notice?

While the past-due balance itself is fixed based on missed contractual payments, borrowers can contact their servicer to request a "Loss Mitigation Application" to evaluate eligibility for programs that move the reinstatement amount to the end of the loan or spread it across a new payment schedule.

Comments