An Early Intervention Loss Mitigation Notice is a critical regulatory requirement sent to delinquent borrowers within 45 days of a missed payment. This document informs homeowners of available foreclosure alternatives and provides specific contact details for assistance. Timely communication helps bridge the gap between lenders and homeowners to prevent property loss. To streamline your compliance, below are some ready to use template.

Image cover: Mastering Early Intervention Loss Mitigation Notices: Essential Templates and Best Practices

Letter Samples List

- Initial Early Intervention Delinquency Notice Letter

- Loss Mitigation Options Available Letter

- Forbearance Plan Offer Letter

- Loan Modification Application Request Letter

- Incomplete Loss Mitigation Application Notice Letter

- Complete Loss Mitigation Application Acknowledgment Letter

- Short Sale Options Information Letter

- Deed-in-Lieu of Foreclosure Inquiry Letter

- Repayment Plan Agreement Notice Letter

- Loss Mitigation Denial and Appeal Rights Letter

- Loss Mitigation Approval and Trial Period Plan Letter

- Housing Counseling Resources Information Letter

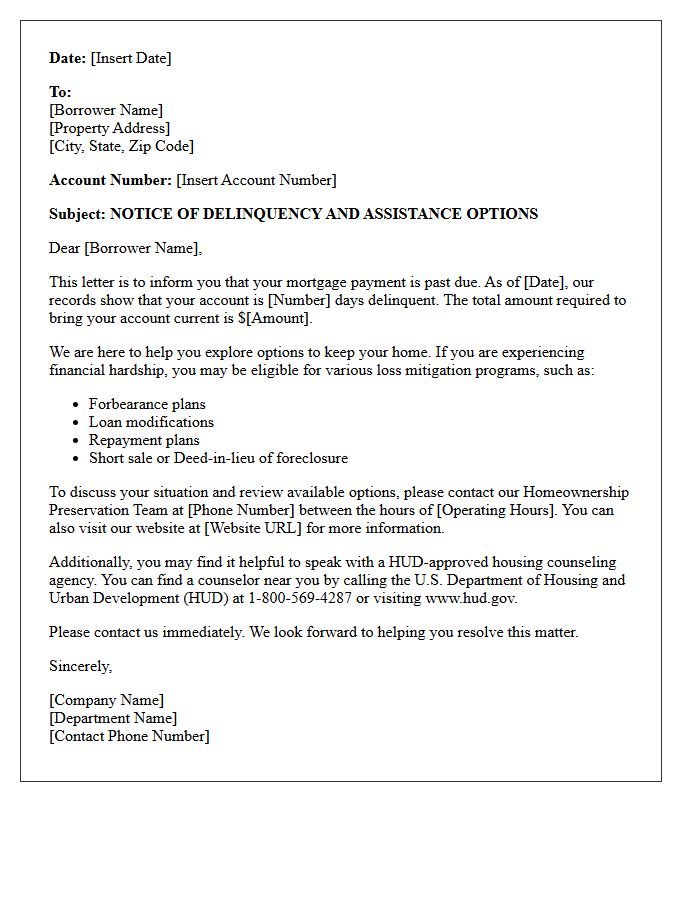

Initial Early Intervention Delinquency Notice Letter

An Initial Early Intervention Delinquency Notice Letter is a formal notification sent by mortgage servicers when a borrower misses a payment. Required under federal law, this loss mitigation tool must be mailed within 45 days of delinquency. Its primary purpose is to inform homeowners of available repayment options and foreclosure alternatives. The notice provides a dedicated point of contact to help resolve financial hardship. Acting promptly upon receiving this letter is crucial for protecting property rights and initiating a workout plan to prevent formal legal action against the home.

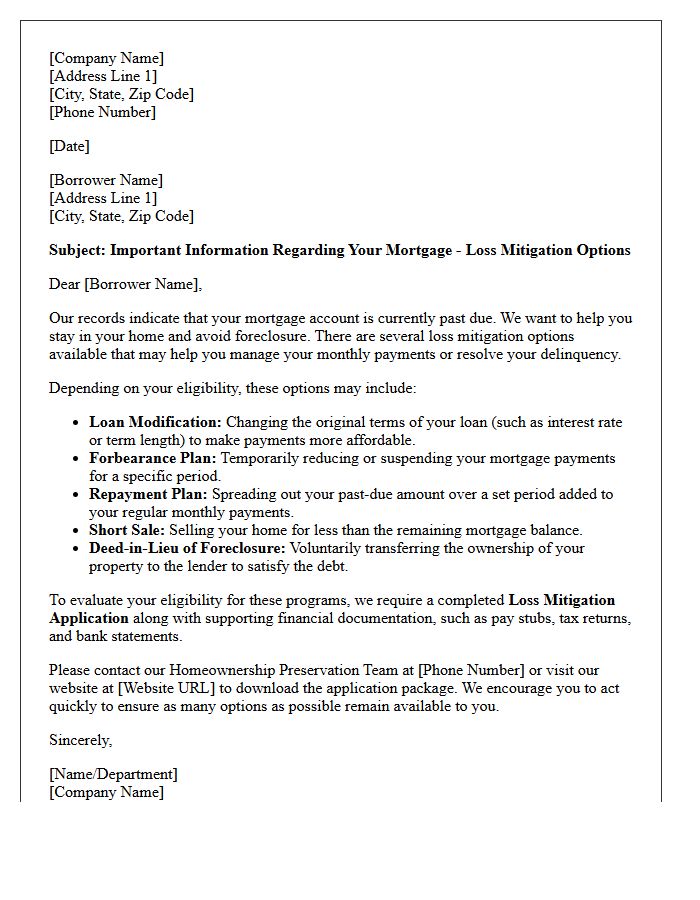

Loss Mitigation Options Available Letter

A Loss Mitigation Options Available Letter is a formal notice from your mortgage servicer outlining programs to avoid foreclosure. This document typically lists alternatives like loan modifications, repayment plans, or short sales. It is crucial to respond immediately, as the letter includes specific deadlines and required documentation for your application. Reviewing these options helps you understand how to resolve delinquencies and stabilize your housing situation. Acting early ensures you maintain legal protections and increases your chances of securing a sustainable payment solution for your home.

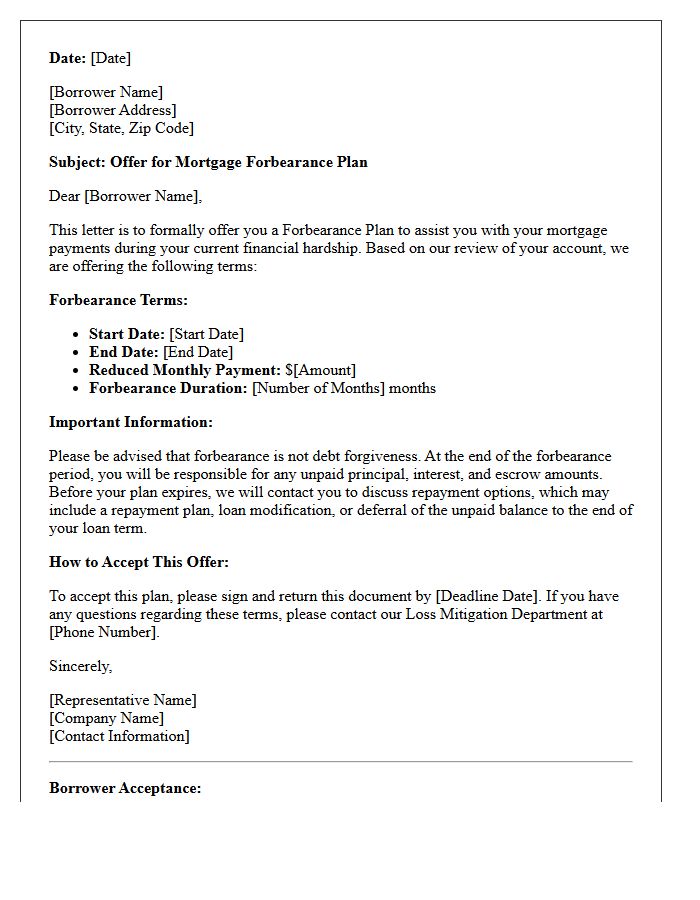

Forbearance Plan Offer Letter

A Forbearance Plan Offer Letter is a formal document from your mortgage servicer outlining a temporary agreement to pause or reduce monthly payments. It is crucial to understand that this is not debt forgiveness; the deferred balance must be repaid later. Review the repayment terms carefully to determine if you will face a lump-sum payment, a loan modification, or a repayment plan once the period ends. Always sign and return the acceptance notice promptly to ensure your credit report reflects the arrangement accurately and avoids foreclosure proceedings during the protection period.

Loan Modification Application Request Letter

A Loan Modification Application Request Letter is a formal document sent to your lender to request a change in original mortgage terms. It is essential to clearly explain your financial hardship, such as job loss or medical expenses, and provide evidence of your inability to meet current payments. The primary goal is to demonstrate a sincere intent to pay if terms are adjusted. Including a detailed budget and supporting documentation improves your chances of securing a lower interest rate, extended loan term, or a reduced monthly payment to prevent foreclosure.

Incomplete Loss Mitigation Application Notice Letter

An Incomplete Loss Mitigation Application Notice is a critical letter from your mortgage servicer identifying missing documentation required to evaluate foreclosure alternatives. This formal notice stops the foreclosure clock only once the file is deemed complete. It lists specific outstanding items and provides a strict deadline for submission. Homeowners must respond immediately to protect their legal rights and ensure a full review for programs like loan modifications. Providing all requested data transforms the application into a "complete" status, triggering mandatory federal protections against dual tracking and unauthorized foreclosure sales.

Complete Loss Mitigation Application Acknowledgment Letter

A Complete Loss Mitigation Application Acknowledgment Letter is a formal notice sent by your mortgage servicer. It confirms they have received all required documents to evaluate your account for foreclosure alternatives. Receiving this letter is critical because it triggers dual tracking protections under federal law, preventing the lender from initiating or continuing foreclosure proceedings while your application is under review. Always verify the letter includes a specific timeline for a decision, typically within thirty days, to ensure your homeowner rights are fully protected during the workout process.

Short Sale Options Information Letter

A Short Sale Options Information Letter is a critical notice from a mortgage lender explaining alternatives to foreclosure. It outlines specific eligibility requirements and the necessary documentation needed to initiate a short sale process. This document serves as a formal invitation for distressed homeowners to mitigate debt by selling their property for less than the remaining loan balance. Understanding these legal options early can help protect your credit score and potentially provide relocation assistance or debt forgiveness through a structured settlement agreement with your servicer.

Deed-in-Lieu of Foreclosure Inquiry Letter

A Deed-in-Lieu of Foreclosure Inquiry Letter is a formal request sent by a homeowner to their mortgage lender to initiate a voluntary property transfer. This document explores an alternative to foreclosure, allowing the borrower to surrender the deed in exchange for debt cancellation. It serves as a preliminary step to determine eligibility based on financial hardship. Using this method can help mitigate severe credit damage and potentially eliminate deficiency judgments. Homeowners should use this letter to request specific application requirements and transition assistance options while seeking to resolve their mortgage delinquency proactively.

Repayment Plan Agreement Notice Letter

A Repayment Plan Agreement Notice Letter is a formal document outlining a structured schedule to settle outstanding debts. It serves as a legally binding confirmation between a creditor and debtor, detailing specific installment amounts, due dates, and applicable interest rates. Receiving this notice signifies that a mutually agreed solution has been established to avoid further collection actions or legal consequences. To maintain financial standing, it is critical to adhere strictly to the repayment timeline specified in the letter to ensure the total balance is successfully cleared over time.

Loss Mitigation Denial and Appeal Rights Letter

A loss mitigation denial letter is a formal notice from your mortgage servicer explaining why a loan modification or assistance plan was rejected. The most critical element is the denial reason, which often involves eligibility criteria or Net Present Value calculations. Federal law grants homeowners specific appeal rights, typically allowing 14 to 30 days to challenge the decision. To successfully appeal, you must provide new documentation or prove the servicer made a calculation error. Acting quickly is essential to pause the foreclosure process and protect your property rights.

Loss Mitigation Approval and Trial Period Plan Letter

A Loss Mitigation Approval letter confirms your mortgage servicer has granted an alternative to foreclosure. A critical component is the Trial Period Plan (TPP), which typically requires three consecutive, on-time monthly payments to demonstrate financial stability. Successfully completing the TPP is mandatory to finalize a permanent loan modification. Review the letter carefully for specific deadlines, payment amounts, and required documentation. Failure to meet these strict requirements can result in the denial of permanent relief and the resumption of foreclosure proceedings. Always maintain proof of timely payments during this evaluation phase.

Housing Counseling Resources Information Letter

The Housing Counseling Resources Information Letter is a mandatory disclosure required by the FHA to assist delinquent borrowers. It provides contact information for HUD-approved counseling agencies that offer free expert advice on debt management and foreclosure prevention. This resource is essential for homeowners facing financial hardship, as it outlines loss mitigation options to help stabilize their housing situation. Receiving this letter ensures borrowers are informed about professional support available to help them navigate mortgage restructuring or repayment plans effectively.

What is an Early Intervention Loss Mitigation Notice?

An Early Intervention Loss Mitigation Notice is a formal communication sent by mortgage servicers to borrowers who have missed one or more payments. The notice is designed to inform the borrower about available foreclosure prevention options, such as loan modifications, forbearance, or short sales, to help them resolve the delinquency before the legal foreclosure process begins.

When am I required to receive an Early Intervention Notice?

Under federal CFPB guidelines, mortgage servicers are generally required to send a written loss mitigation notice no later than the 45th day of a borrower's delinquency. This follows the "live contact" requirement, where the servicer must attempt to speak with the borrower by the 36th day of missed payments to discuss potential solutions.

What information must be included in a Loss Mitigation Notice?

A legally compliant notice must include a statement urging the borrower to contact the servicer, a description of available loss mitigation programs, instructions on how to apply for assistance, and contact information for HUD-approved housing counseling agencies. It also typically provides a direct link to the servicer's loss mitigation application portal.

Does receiving this notice mean my home is in foreclosure?

No, receiving an Early Intervention Loss Mitigation Notice does not mean your home is currently in foreclosure. Rather, it serves as a proactive warning and an invitation to negotiate a solution. In most cases, a servicer cannot officially start the foreclosure process (filing the first legal notice) until a borrower is more than 120 days delinquent.

How should I respond to an Early Intervention Loss Mitigation Notice?

The most effective response is to contact your mortgage servicer immediately using the information provided in the notice. You should request a Loss Mitigation Application packet and begin gathering financial documentation, such as pay stubs and tax returns, to prove your eligibility for a repayment plan or loan restructure.

Comments