A Final Notice of Default and Intent to Accelerate is a critical legal warning sent by lenders when a borrower fails to cure missed payments. This formal document signifies the final step before the entire loan balance becomes due immediately, often leading to foreclosure proceedings. Understanding your rights during this stage is essential. To assist you, below are some ready to use template.

Image cover: Final Notice of Default and Intent to Accelerate: Essential Templates and Legal Guidelines

Letter Samples List

- Mortgage Default and Intent to Accelerate Final Notice Letter

- Final Demand and Loan Acceleration Warning Letter

- Residential Mortgage Default Intent to Accelerate Letter

- Commercial Property Final Default and Acceleration Letter

- Pre-Foreclosure Intent to Accelerate Demand Letter

- Delinquent Mortgage Final Notice of Default Letter

- Intent to Accelerate and Foreclose Final Warning Letter

- Mortgage Account Final Default Notice Letter

- Secured Property Intent to Accelerate Default Letter

- Final Notice of Mortgage Breach and Acceleration Letter

- Borrower Final Default and Loan Acceleration Letter

- Past Due Mortgage Intent to Accelerate Letter

- Real Estate Loan Final Default and Acceleration Letter

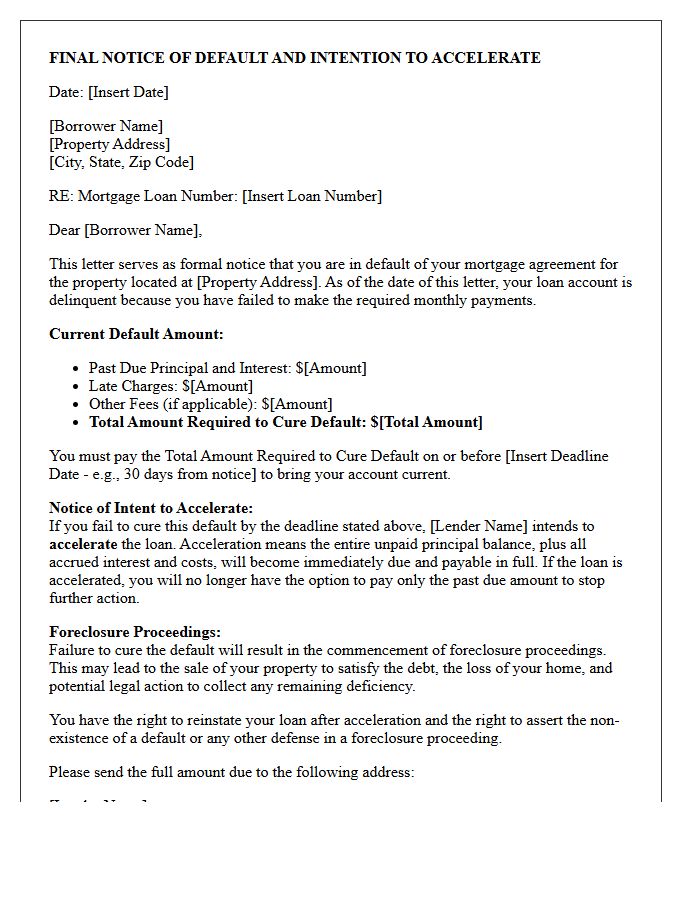

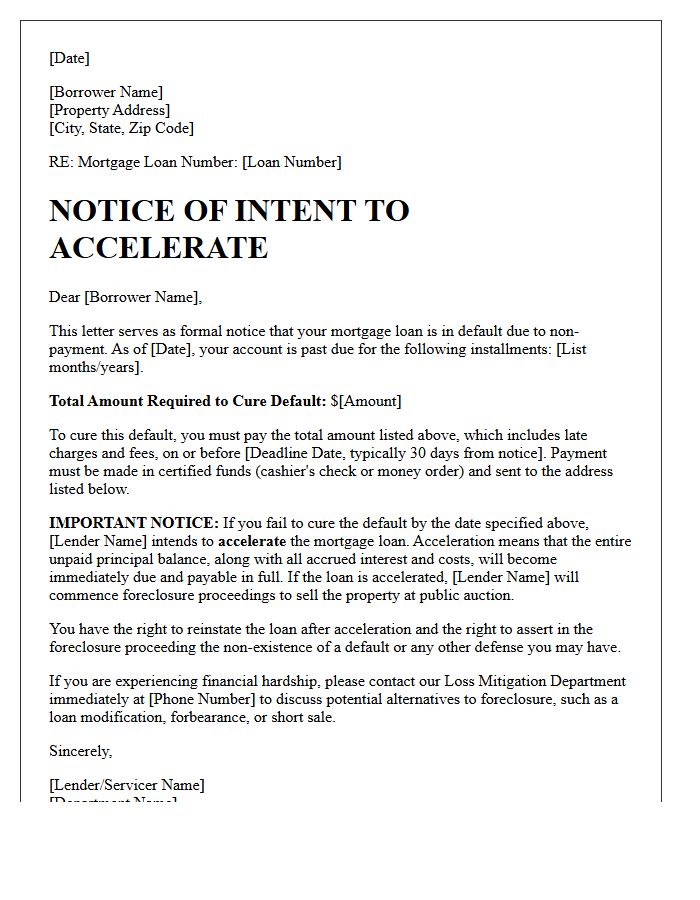

Mortgage Default and Intent to Accelerate Final Notice Letter

Receiving a Mortgage Default and Intent to Accelerate Final Notice is a critical warning that your loan is in jeopardy. This formal document signifies that the lender will demand full repayment of the remaining balance if the specified arrears are not paid by the deadline. It serves as the final step before the foreclosure process officially begins. To prevent losing your home, you must immediately address the default by paying the total overdue amount, requesting a loan modification, or contacting your servicer to discuss loss mitigation options before the acceleration occurs.

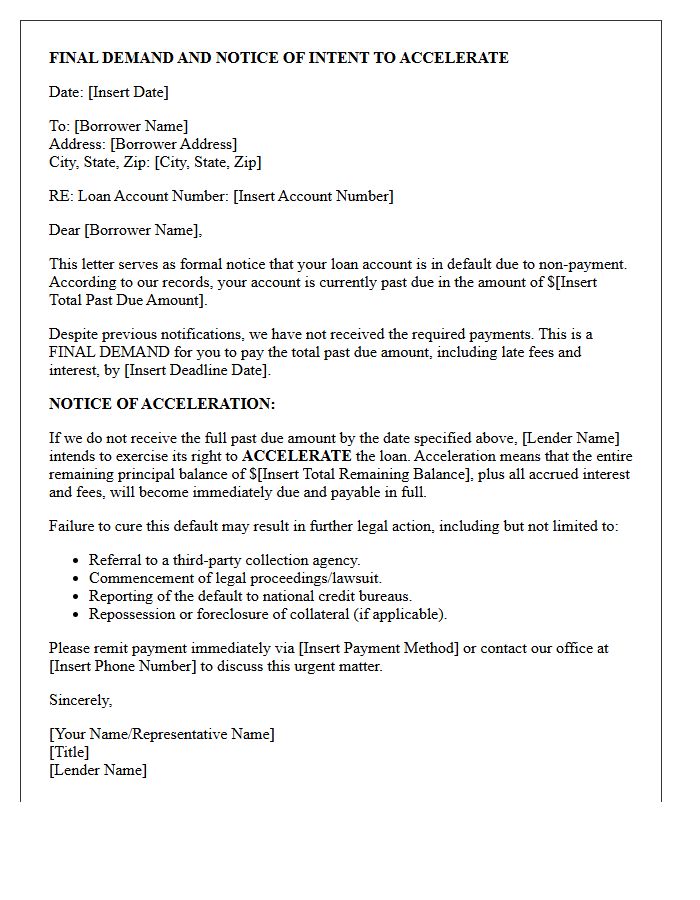

Final Demand and Loan Acceleration Warning Letter

A Final Demand and Loan Acceleration Warning Letter is a critical formal notice issued by lenders when a borrower defaults. This document serves as a final legal warning before the creditor demands immediate repayment of the entire outstanding balance. It highlights that failure to resolve the delinquency will trigger loan acceleration, making the full debt due instantly rather than through installments. Receiving this letter indicates that the lender is preparing for foreclosure or litigation, making it essential to contact the servicer immediately to discuss loss mitigation or repayment options to avoid legal action.

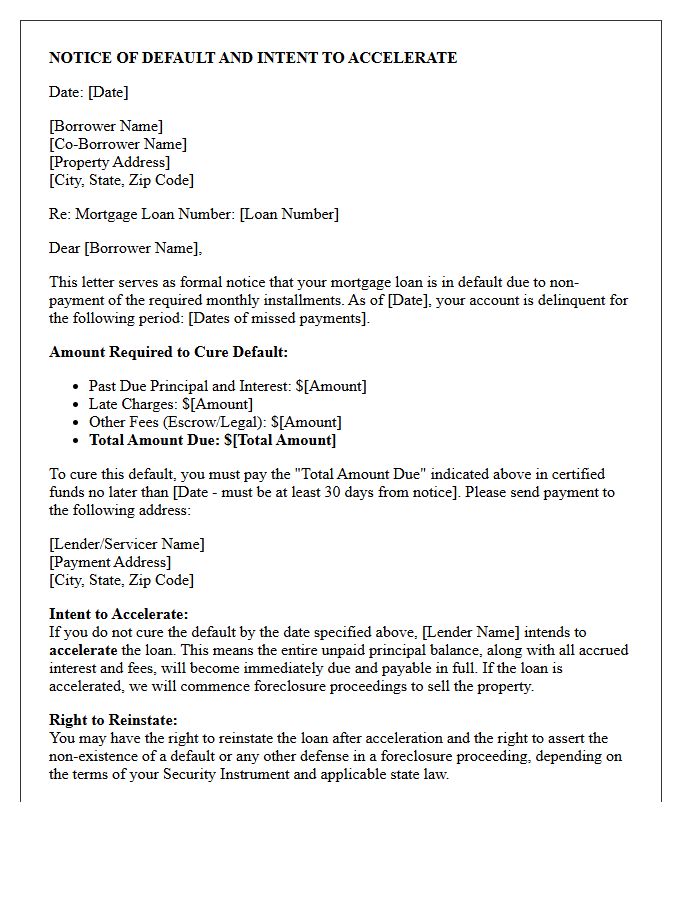

Residential Mortgage Default Intent to Accelerate Letter

A Residential Mortgage Default Intent to Accelerate Letter is a formal notice sent by lenders when a borrower misses payments. This critical document warns that unless the delinquency is cured by a specific deadline, the bank will demand the full loan balance immediately. It serves as a mandatory legal step before the foreclosure process begins. To avoid losing the property, borrowers must pay the total overdue amount, including late fees. Receiving this letter indicates that your homeownership is at serious risk, requiring urgent communication with your loan servicer.

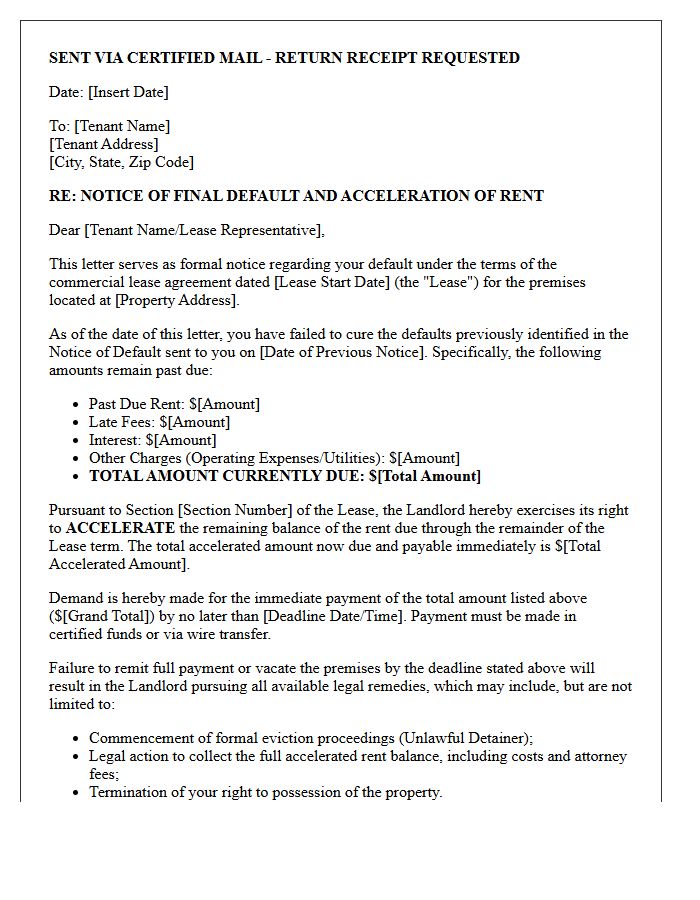

Commercial Property Final Default and Acceleration Letter

A Commercial Property Final Default and Acceleration Letter is a formal legal notice issued when a borrower fails to cure a breach. It officially triggers acceleration, demanding the immediate repayment of the entire outstanding loan balance. This document signifies the end of the reinstatement period and serves as a mandatory prerequisite for initiating foreclosure proceedings. It is critical for lenders to ensure strict compliance with contractual notice requirements to uphold their rights during litigation. For tenants and owners, this letter represents the final warning before legal action or property seizure begins.

Pre-Foreclosure Intent to Accelerate Demand Letter

A Pre-Foreclosure Intent to Accelerate Demand Letter is a formal notice sent by a lender warning that the entire loan balance will become due if payment defaults are not cured. This legal requirement serves as a final opportunity for homeowners to resolve delinquencies before the formal foreclosure process begins. It typically outlines the specific amount owed, the deadline for payment, and the consequences of inaction. Understanding this document is critical because it marks the transition from standard collection efforts to potential legal action against your property title.

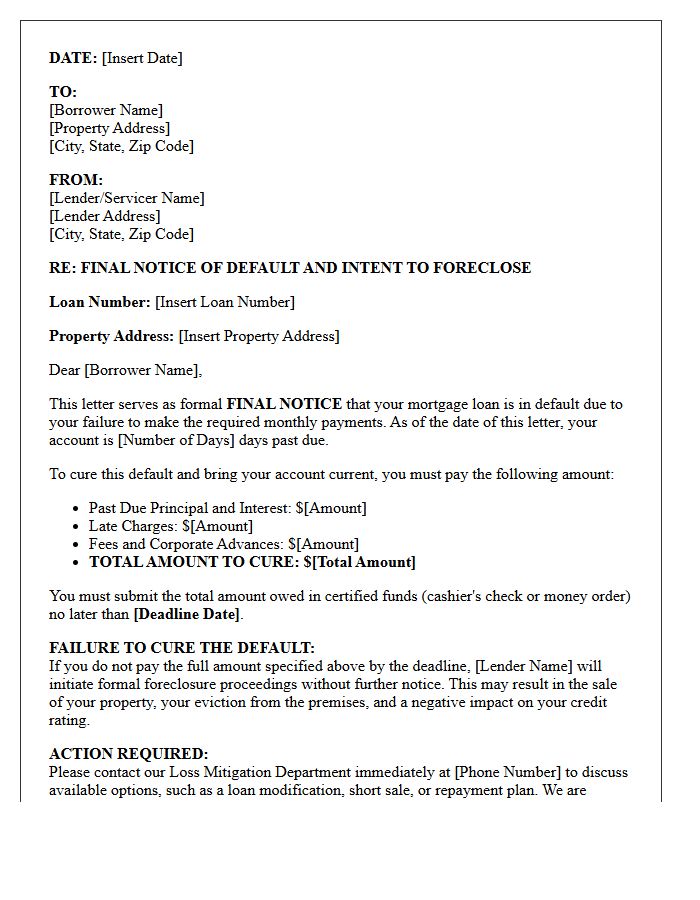

Delinquent Mortgage Final Notice of Default Letter

A Final Notice of Default is a critical legal warning sent by lenders when a mortgage is severely delinquent. This document signals the end of the grace period and the formal commencement of foreclosure proceedings. It outlines the total amount required to reinstate the loan and provides a strict deadline for payment. Ignoring this notice can lead to the loss of your property. Homeowners should immediately seek legal advice or contact their servicer to discuss loss mitigation options and avoid a public auction.

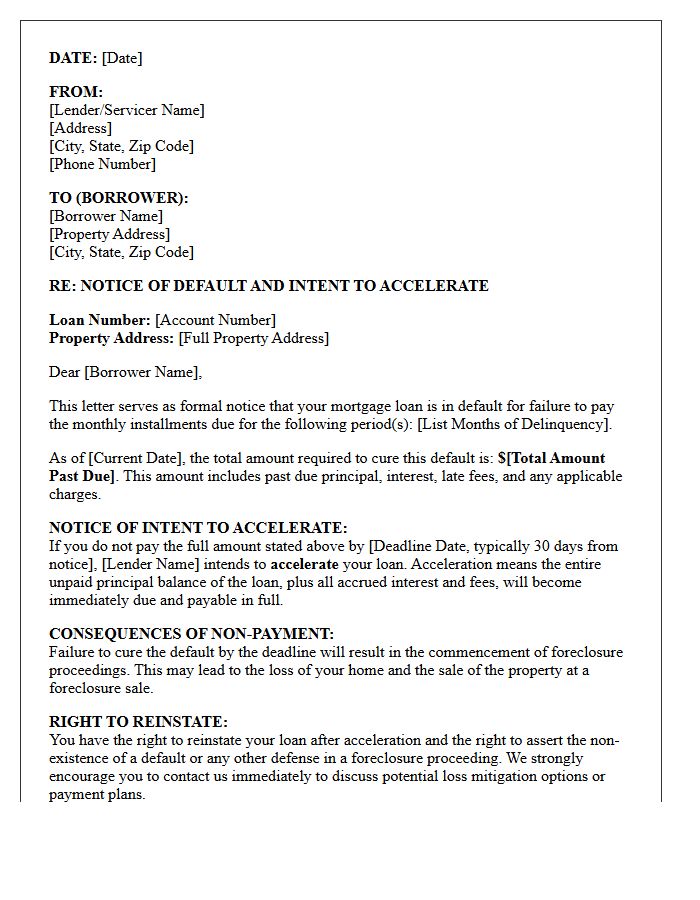

Intent to Accelerate and Foreclose Final Warning Letter

An Intent to Accelerate and Foreclose Final Warning Letter is a formal legal notice issued by a mortgage lender when a borrower defaults on payments. This document serves as the final notification that the entire remaining loan balance is becoming due immediately. It outlines the specific default amount required to reinstate the loan and provides a strict deadline to cure the delinquency. Failure to pay the requested sum by the specified date typically results in the lender initiating foreclosure proceedings to seize the property and recover their investment.

Mortgage Account Final Default Notice Letter

A Mortgage Account Final Default Notice Letter is a critical legal warning indicating that your lender is initiating foreclosure proceedings. This formal document confirms you have failed to resolve past-due payments within the required timeframe. It serves as the last opportunity to settle the outstanding debt or negotiate a loss mitigation plan before losing your home. Upon receiving this notice, immediate action is essential to explore options like loan modification or repayment plans to prevent a legal seizure of the property and permanent damage to your credit score.

Secured Property Intent to Accelerate Default Letter

A Secured Property Intent to Accelerate Default Letter is a formal legal notice sent by lenders to borrowers in arrears. This document serves as a final warning that the entire outstanding loan balance will become due immediately unless the default is cured. It typically outlines the specific amount required to reinstate the loan and provides a strict deadline for payment. Receiving this letter is a critical stage in the foreclosure process, signaling that the lender is prepared to seize the collateralized property if the delinquency persists.

Final Notice of Mortgage Breach and Acceleration Letter

A Final Notice of Mortgage Breach and Acceleration is a critical legal warning issued by lenders when a borrower defaults. It signifies that the entire loan balance is now due immediately, stripping away the right to make monthly installments. This document is the final step before the formal commencement of foreclosure proceedings. To prevent the loss of the property, homeowners must pay the full delinquent amount or negotiate a loss mitigation plan during this narrow window. Ignoring this notice typically leads to a legal summons and the forced sale of the home.

Borrower Final Default and Loan Acceleration Letter

A Borrower Final Default and Loan Acceleration Letter is a formal legal notice issued when a debtor fails to cure a breach. It signifies the end of the grace period, officially declaring the loan acceleration process. This means the entire outstanding balance, including principal and interest, becomes due immediately. Receiving this document is a critical warning that the lender may initiate foreclosure or legal action to recover the debt. Borrowers must act urgently to negotiate a settlement or face the permanent loss of their collateral and severe credit damage.

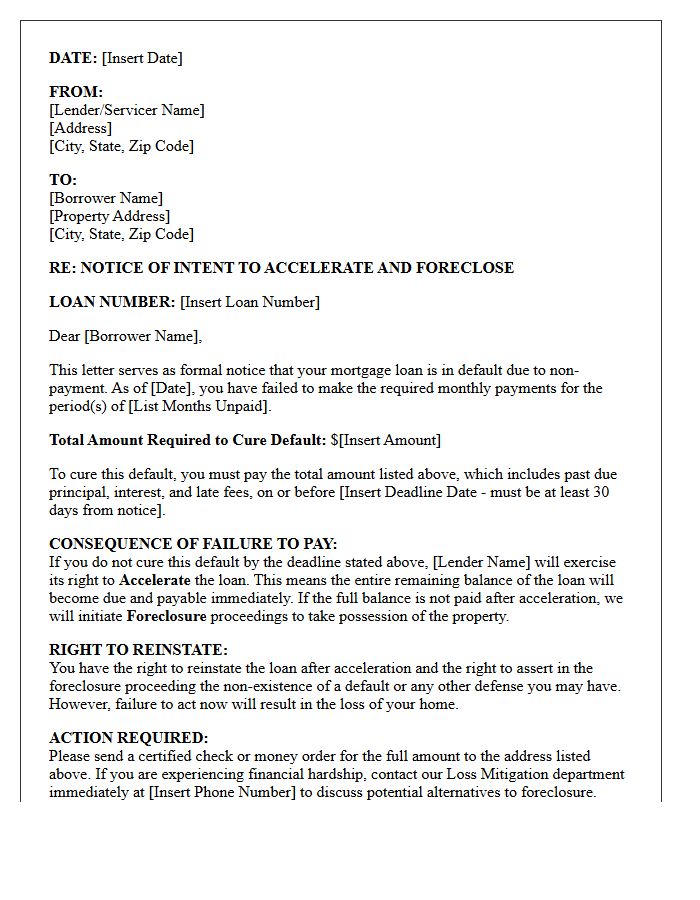

Past Due Mortgage Intent to Accelerate Letter

A Notice of Intent to Accelerate is a formal warning from your lender that your mortgage loan is at risk of being called due in full. This document is the final step before the foreclosure process officially begins. It outlines the total amount needed to cure the default and provides a specific deadline. To protect your home, you must pay the arrears or negotiate a loss mitigation plan before the expiration date. Ignoring this letter allows the bank to accelerate the debt, demanding the entire remaining balance immediately.

Real Estate Loan Final Default and Acceleration Letter

A Real Estate Loan Final Default and Acceleration Letter is a formal legal notice sent by a lender when a borrower fails to cure a delinquency. It signifies the end of the grace period, declaring the entire loan balance immediately due. This critical document serves as a final warning before the lender initiates foreclosure proceedings. Receiving this letter means you have lost the right to make monthly installments; you must now pay the full debt or seek a legal workout to prevent losing the property through a judicial or non-judicial sale.

What is a Final Notice of Default and Intent to Accelerate?

A Final Notice of Default and Intent to Accelerate is a formal legal document sent by a mortgage lender notifying the borrower that they have breached their loan contract. It serves as a final warning that if the total past-due balance is not paid by a specific deadline, the lender will demand the immediate payment of the entire remaining loan balance and initiate foreclosure proceedings.

How long do I have to respond to a Notice of Intent to Accelerate?

The timeframe to cure the default is typically 30 days from the date the notice was mailed. However, the exact duration depends on the specific terms of your deed of trust or mortgage contract and applicable state laws. If the "cure period" expires without payment, the lender officially accelerates the debt, meaning the option to simply pay the arrears is no longer available.

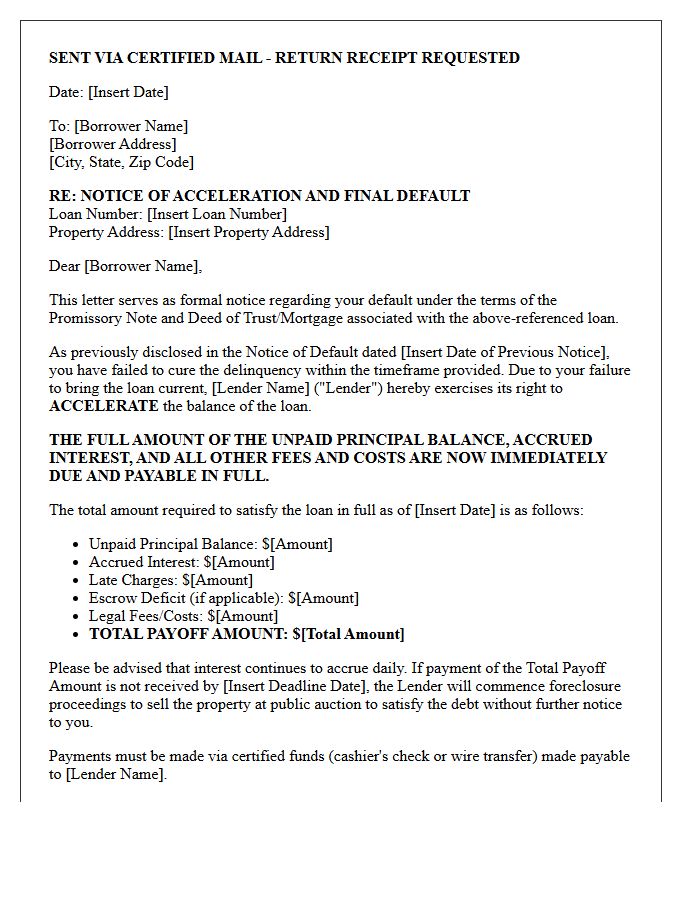

What happens after a mortgage loan is accelerated?

Once a loan is accelerated, the full balance of the mortgage becomes due immediately, and the borrower loses the right to make monthly installment payments. If the debt is not settled or a loss mitigation agreement is not reached, the lender will transition the account to a trustee or attorney to begin the legal foreclosure process to sell the property.

Can I stop foreclosure after receiving a Final Notice of Default?

Yes, foreclosure can still be prevented after receiving this notice. Options include "curing the default" by paying the full delinquent amount, applying for a loan modification, requesting a repayment plan, or seeking a short sale. It is critical to contact your loan servicer immediately to discuss loss mitigation options before the acceleration deadline expires.

What is the difference between a Notice of Default and an Acceleration Notice?

A Notice of Default informs the borrower of the specific amount owed and the intent to accelerate the loan if the debt isn't settled. An Acceleration Notice is the subsequent step where the lender confirms that the cure period has passed, the full balance is now due, and the foreclosure process is moving forward. The "Intent to Accelerate" acts as the final bridge between delinquency and active foreclosure.

Comments