Receiving an Initial Notice of Payment Default and Right to Cure is a critical legal step in the foreclosure or repossession process. This document informs borrowers of their missed payments and outlines the specific timeframe allowed to resolve the debt and reinstate the contract. Understanding your consumer rights can help prevent further legal action. Below are some ready to use templates.

Image cover: Official Notice of Default and Right to Cure: Professional Templates and Samples

Letter Samples List

- Initial Notice of Payment Default and Right to Cure Letter

- Date of Notice Issuance

- Borrower Full Name and Mortgaged Property Address

- Dear Mortgage Borrower

- This Letter Serves as Your Formal Notice of Payment Default

- Your Mortgage Account is Currently Past Due and Delinquent

- You Have the Right to Cure This Default Prior to Loan Acceleration

- The Total Past Due Amount Required to Cure is Provided Herein

- You Must Remit This Exact Payment by the Specified Deadline Date

- Failure to Cure This Default May Result in Loan Acceleration

- Subsequent Acceleration Will Lead to Property Foreclosure Proceedings

- Please Contact Our Loss Mitigation Department for Immediate Assistance

- Approved Housing Counselor Information is Enclosed With This Letter

- Sincerely the Mortgage Lending Collections Department

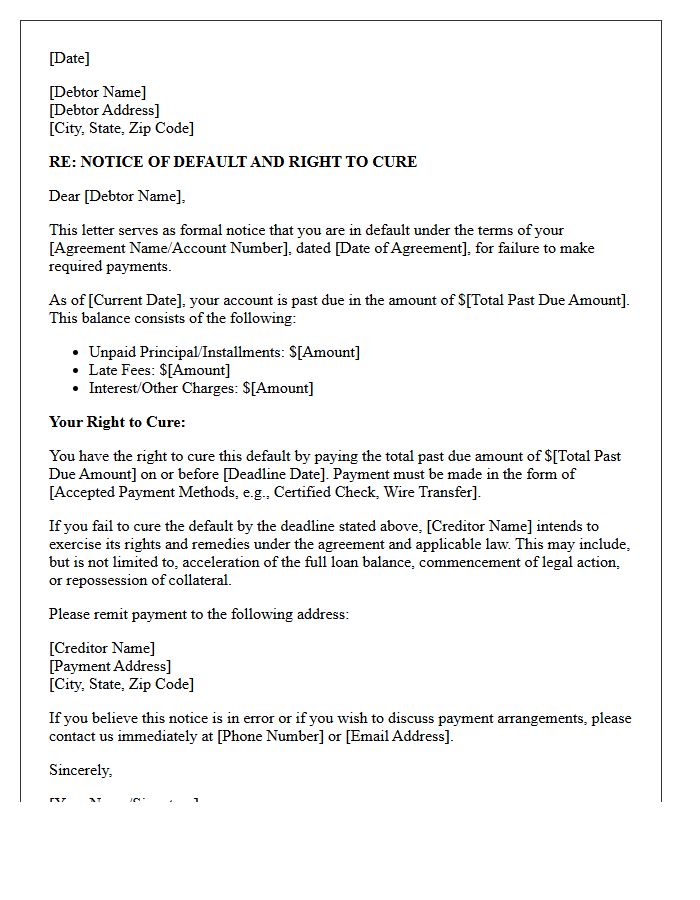

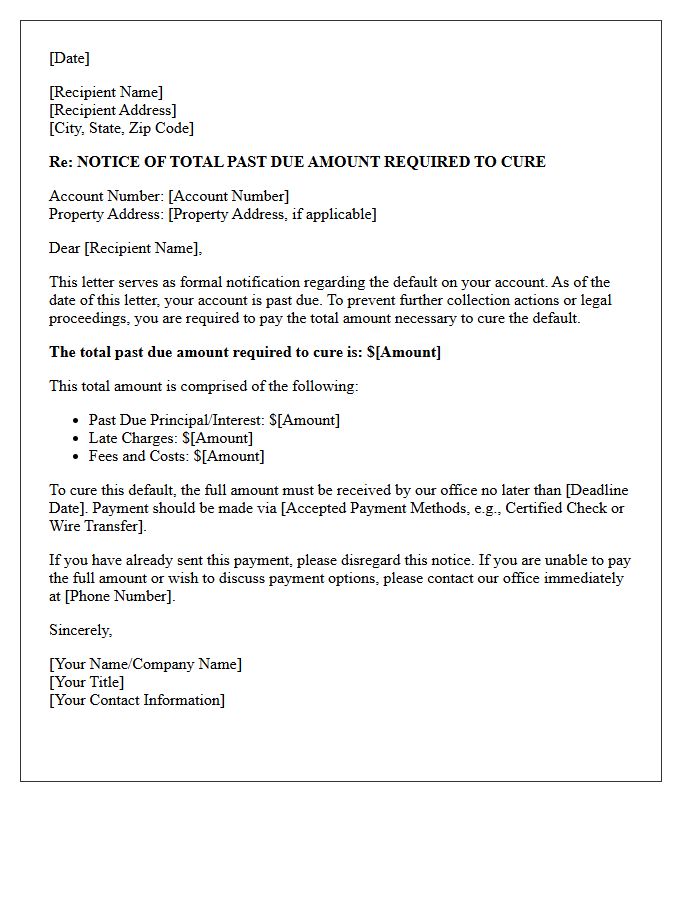

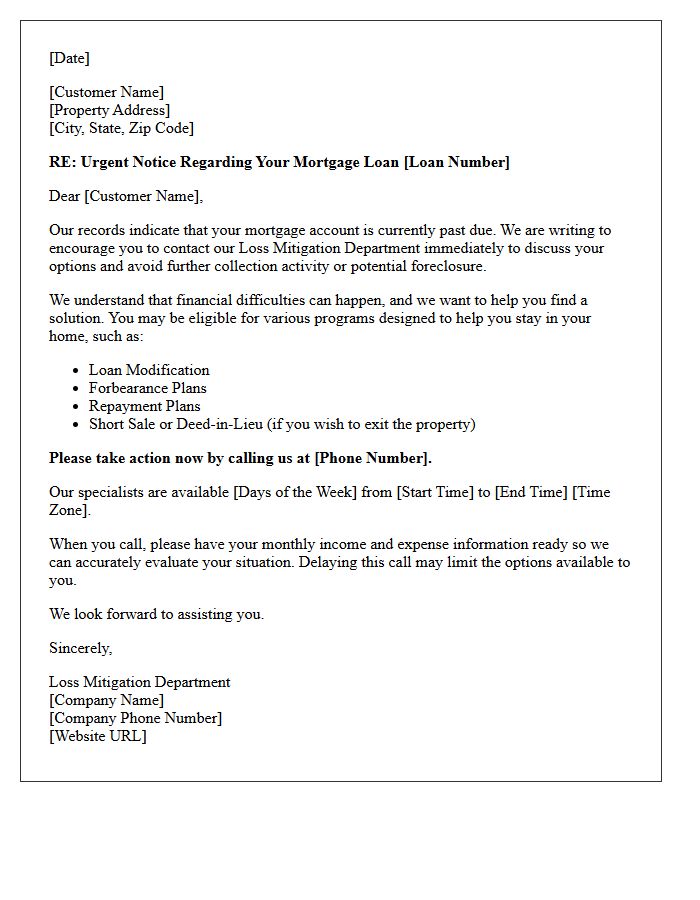

Initial Notice of Payment Default and Right to Cure Letter

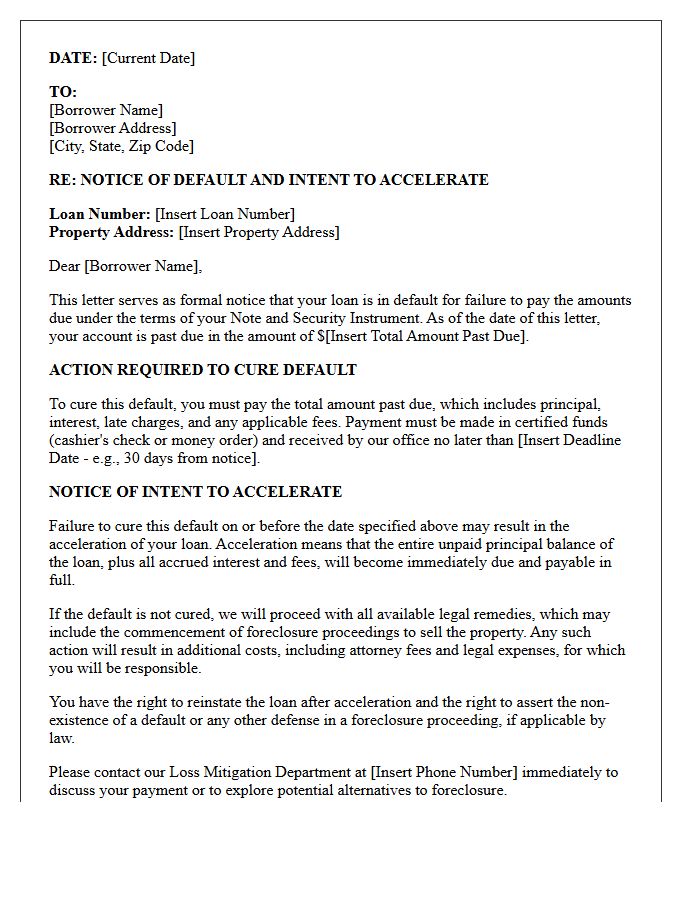

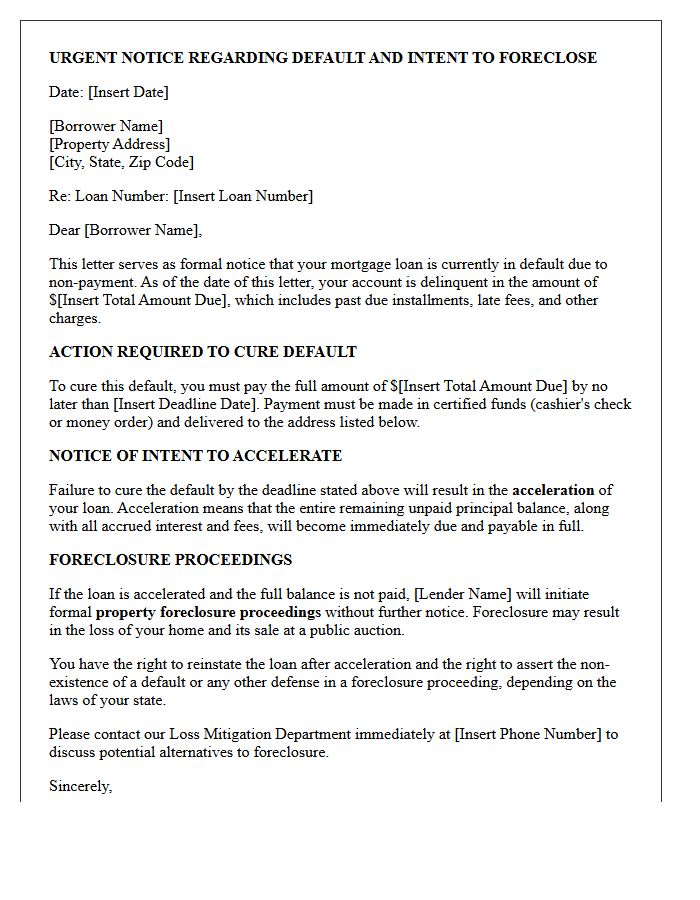

An Initial Notice of Payment Default and Right to Cure Letter is a formal legal document sent to borrowers who miss loan payments. It serves as a mandatory warning before foreclosure or repossession proceedings begin. The letter details the specific amount overdue, including late fees, and provides a strict deadline to rectify the delinquency. Successfully paying the total arrears within this timeframe restores the loan's standing. Ignoring this notice forfeits your legal protections, allowing the lender to accelerate the debt and seize collateral to satisfy the outstanding balance.

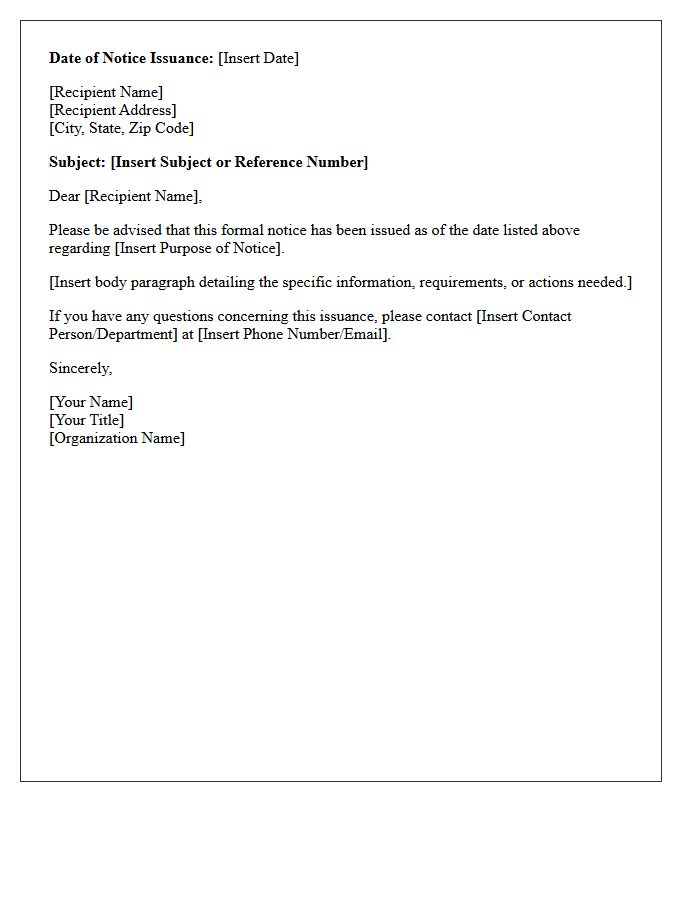

Date of Notice Issuance

The Date of Notice Issuance marks the official start of a legal or administrative process. It is the specific day a formal document is processed and dispatched, serving as the primary reference point for deadlines and statutory response periods. Knowing this date is essential for ensuring compliance, as missing a timeframe calculated from this issuance can result in the loss of rights or penalties. Always verify this date to accurately track your obligations and protect your interests in any formal proceeding.

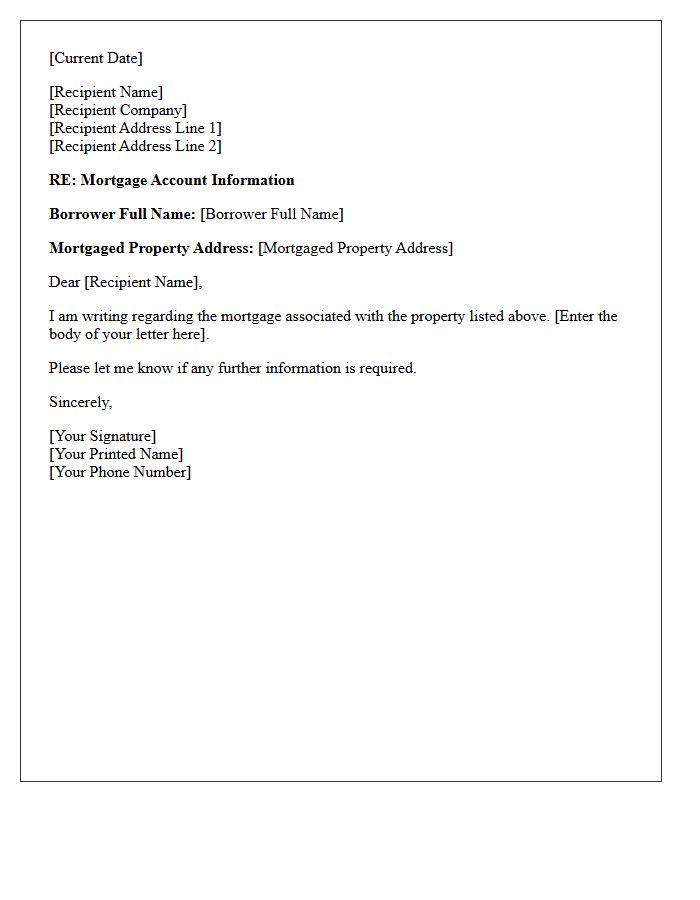

Borrower Full Name and Mortgaged Property Address

The Borrower Full Name and Mortgaged Property Address are critical identifiers in loan documentation. The name must match official government identification exactly to ensure legal accountability. The property address specifies the collateral securing the debt, defining the physical location where the lender holds a lien. Accuracy in these fields is essential to prevent legal disputes, ensure proper title registration, and validate the enforceability of the mortgage contract. Always verify these details against the property deed to maintain data integrity during the closing process.

Dear Mortgage Borrower

As a mortgage borrower, your most critical priority is maintaining a healthy credit score to secure favorable interest rates. Consistently making on-time payments and managing your debt-to-income ratio are essential factors that influence loan approval and long-term affordability. Before committing, ensure you understand the full scope of closing costs and the impact of private mortgage insurance. Staying informed about market fluctuations allows you to make strategic decisions regarding fixed versus adjustable rates, ultimately protecting your financial stability throughout the life of your home loan.

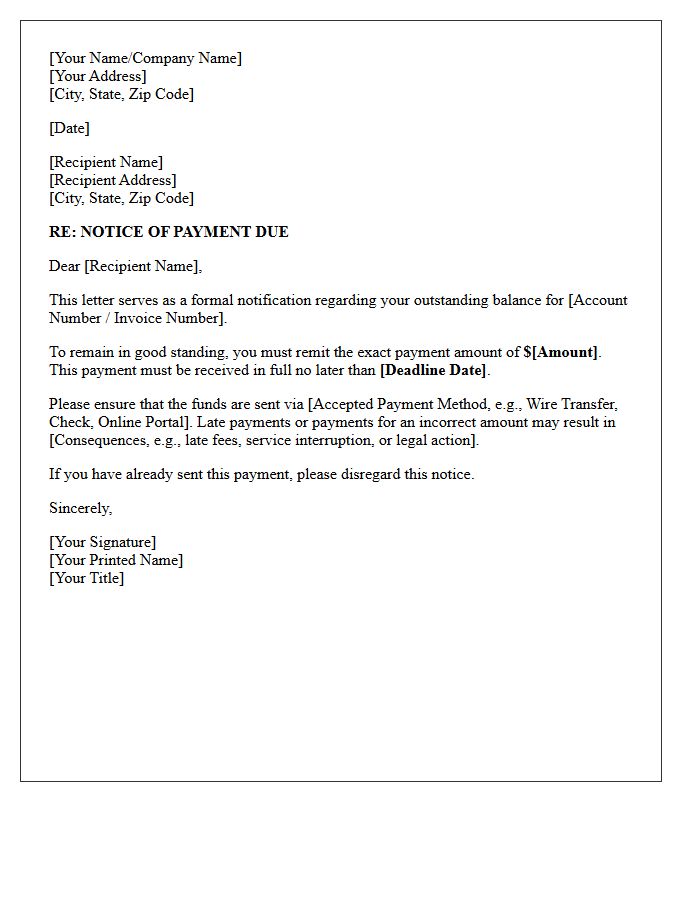

This Letter Serves as Your Formal Notice of Payment Default

This Notice of Payment Default serves as a critical legal warning regarding your overdue balance. It signifies that you have failed to meet your contractual financial obligations by the specified deadline. Failure to resolve this delinquency immediately may result in severe consequences, including late penalties, service suspension, or formal debt collection actions. To prevent further escalation and potential damage to your credit rating, you must remit the outstanding amount or contact the creditor to arrange a repayment plan before the remedy period expires.

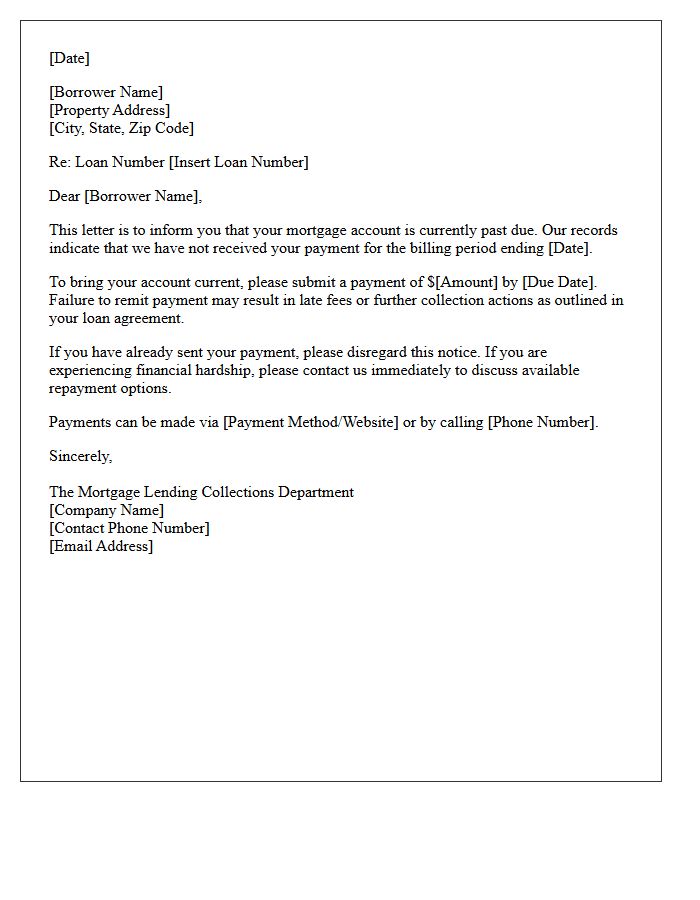

Your Mortgage Account is Currently Past Due and Delinquent

A mortgage becomes delinquent when a scheduled payment is missed. Being past due triggers late fees and negatively impacts your credit score. If the account remains unresolved, the lender may initiate formal foreclosure proceedings to reclaim the property. It is critical to communicate with your servicer immediately to explore loss mitigation options, such as loan modification or forbearance plans. Prompt action is the most effective way to protect your home equity and restore your financial standing before the legal process advances further.

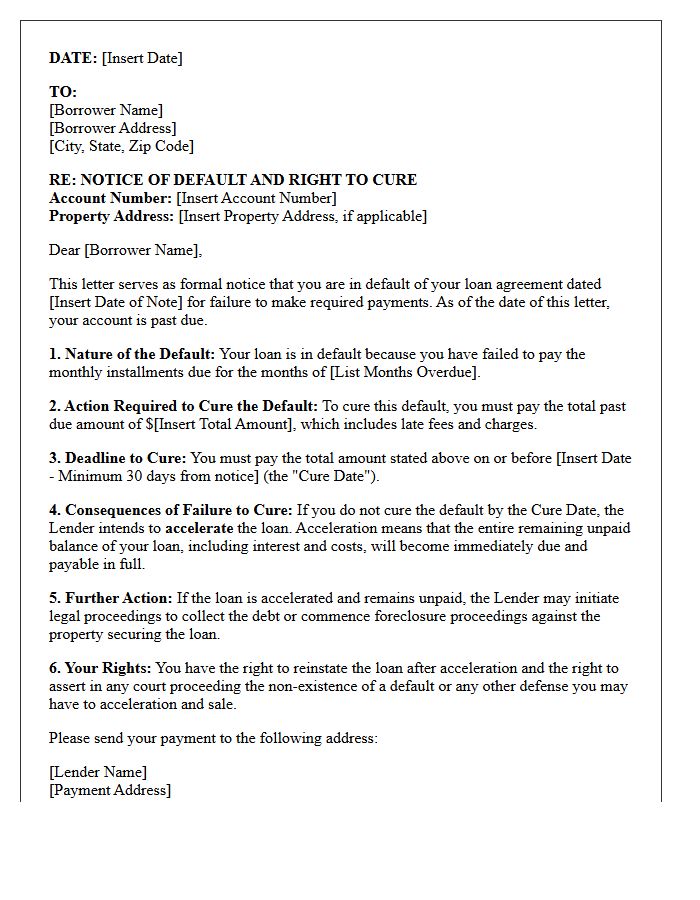

You Have the Right to Cure This Default Prior to Loan Acceleration

If you receive a notice stating you have the Right to Cure, it means you can rectify a missed payment before the lender demands the full balance. To avoid loan acceleration, you must pay the specified arrears, including interest and late fees, by the deadline. Successfully curing the default reinstates your original loan terms and stops foreclosure proceedings. Failure to act allows the lender to "accelerate" the debt, making the entire amount due immediately. Always verify the exact amount required to protect your property ownership and credit standing.

The Total Past Due Amount Required to Cure is Provided Herein

The Total Past Due Amount Required to Cure represents the exact sum necessary to resolve a financial default and reinstate an agreement. This figure typically encompasses missed principal payments, accumulated interest, and late fees. To effectively cure the default, the debtor must submit this specific payment by the designated deadline to prevent further legal action or foreclosure. Understanding this balance is vital for maintaining contractual compliance and ensuring financial stability. Always verify the breakdown of costs to ensure the reinstatement process is successfully completed and your account returns to good standing.

You Must Remit This Exact Payment by the Specified Deadline Date

To maintain your account in good standing, you must remit the exact payment amount indicated on your statement. Failure to provide the full balance by the specified deadline date may result in immediate service interruptions, late fees, or legal penalties. Ensure your funds are transferred through authorized channels early to account for potential processing delays. Accurate and timely compliance is essential to avoid additional financial liabilities or negative credit reporting. Always verify your transaction confirmation once the payment is finalized.

Failure to Cure This Default May Result in Loan Acceleration

Receiving a notice that failure to cure a default may result in loan acceleration is a critical warning for borrowers. This legal process means the lender can demand immediate full repayment of the entire remaining mortgage balance, not just the missed payments. To prevent this, you must pay the specified amount by the deadline mentioned in the demand letter. Ignoring this notice often leads to foreclosure proceedings. Always contact your servicer immediately to explore loss mitigation options or repayment plans to protect your property and credit standing.

Subsequent Acceleration Will Lead to Property Foreclosure Proceedings

When a borrower defaults on a mortgage, the lender may issue a notice of acceleration. This legal process demands immediate payment of the entire remaining loan balance. Failure to settle this debt or reach a workout agreement triggers foreclosure proceedings, allowing the creditor to seize and sell the property to recover losses. Understanding this timeline is crucial, as subsequent actions lead to the permanent loss of ownership. Homeowners must act quickly during this phase to seek legal counsel or loan modification options to stop the final foreclosure sale.

Please Contact Our Loss Mitigation Department for Immediate Assistance

When you receive a notice to contact our Loss Mitigation Department, it signifies an urgent opportunity to explore foreclosure prevention options. Our specialized team provides personalized financial solutions, such as loan modifications or repayment plans, to help you maintain homeownership. Prompt communication is essential to evaluate your eligibility for assistance programs and resolve delinquency issues. Act quickly to protect your credit and secure your property's future by discussing available alternatives with our dedicated experts today.

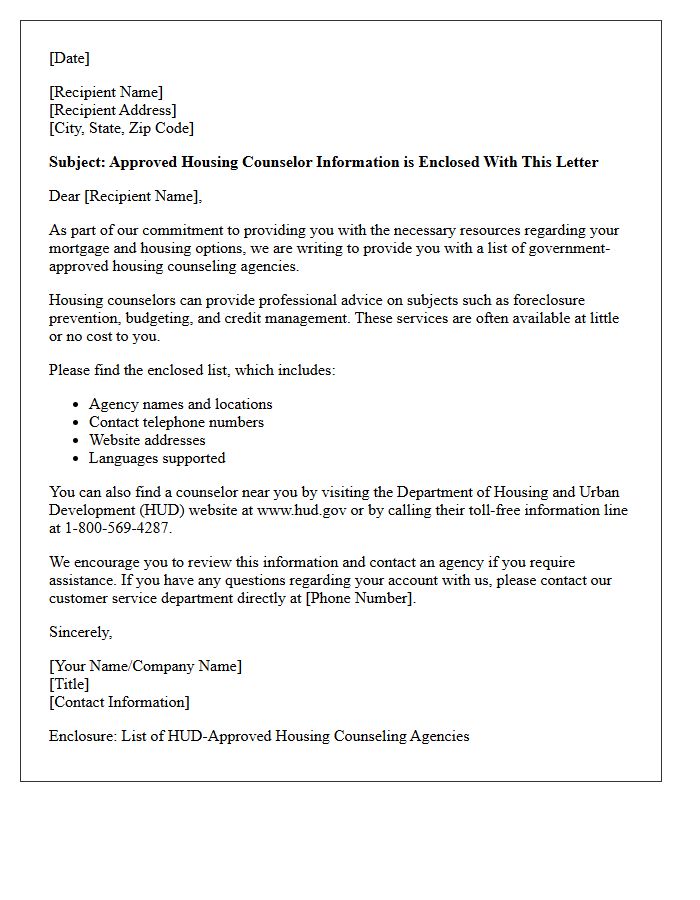

Approved Housing Counselor Information is Enclosed With This Letter

Receiving Approved Housing Counselor Information is a critical step in managing your mortgage or rental challenges. These U.S. Department of Housing and Urban Development (HUD) certified professionals provide expert guidance on foreclosure prevention, debt management, and credit repair at little to no cost. Reviewing the enclosed details immediately allows you to access free, unbiased support tailored to your financial situation. Contacting a counselor early increases your chances of securing a loan modification or a sustainable repayment plan. This letter provides the essential resources needed to protect your home and ensure long-term housing stability.

Sincerely the Mortgage Lending Collections Department

The Mortgage Lending Collections Department acts as a vital resource for homeowners facing financial challenges. Their primary objective is to offer repayment solutions and loss mitigation options to prevent foreclosure. Early communication is essential; contacting this department immediately allows you to explore loan modifications, forbearances, or specialized payment plans. They prioritize maintaining homeownership while ensuring debt recovery through professional guidance. Understanding your financial obligations and proactively discussing alternatives can safeguard your credit score and secure your property during difficult times.

What is an Initial Notice of Payment Default and Right to Cure?

An Initial Notice of Payment Default and Right to Cure is a formal legal document sent by a lender to a borrower stating that a payment has been missed. It serves as an official warning that the loan is in default while providing a specific timeframe during which the borrower can pay the overdue amount to avoid further legal action or foreclosure.

How long is the typical cure period after receiving a default notice?

The duration of the cure period varies by state law and the specific terms of the loan agreement, but it typically ranges from 15 to 30 days. During this window, the borrower has the legal right to reinstate the loan by paying the total past-due balance plus any applicable late fees.

What information must be included in a Right to Cure notice?

A legally compliant notice must include the total amount currently due, the specific date by which the payment must be received, the method of payment accepted, and a clear statement explaining the consequences of failing to "cure" the default, such as acceleration of the loan or repossession of collateral.

Can a lender start foreclosure before the Right to Cure period expires?

No, a lender is generally prohibited from initiating foreclosure proceedings or repossessing property until the deadline specified in the Right to Cure notice has passed. This period acts as a mandatory grace period designed to protect consumer rights and provide a final opportunity for debt resolution.

What happens if I fail to cure the payment default by the deadline?

If the default is not cured by the specified date, the lender may "accelerate" the debt, meaning the entire remaining balance of the loan becomes due immediately. Once the right to cure expires, the creditor can move forward with legal remedies, including filing a foreclosure lawsuit or reporting the delinquency to credit bureaus.

Comments