Receiving a Notice of Default Due to Junior Lien Attachment occurs when a secondary debt, such as a judgment or second mortgage, jeopardizes the primary lender's security interest. This legal action can trigger foreclosure if the underlying breach is not resolved immediately. Understanding your contractual obligations is vital to protecting your property equity. Below are some ready to use templates.

Image cover: Formal Notice of Default: Junior Lien Attachment Templates and Compliance Guide

Letter Samples List

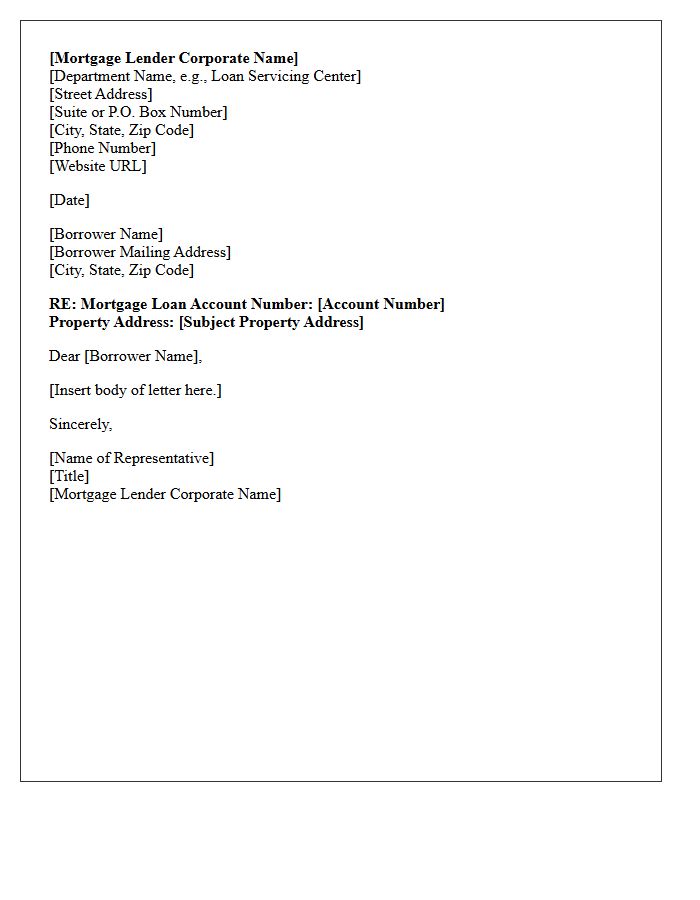

- Mortgage Lender Corporate Name And Return Address

- Date Of Formal Letter Issuance

- Borrower Name And Mortgaged Property Address

- Subject Notice Of Default Letter Due To Junior Lien Attachment

- Formal Borrower Salutation

- Identification Of Original Mortgage Loan Account Details

- Notification Of Unauthorized Junior Lien Attachment

- Citation Of Specific Mortgage Covenant Breach

- Demand For Immediate Junior Lien Satisfaction Or Removal

- Specific Deadline For Curative Action Requirements

- Consequences Of Failure To Cure Account Default

- Notice Of Intent To Accelerate Mortgage Loan Balance

- Lender Loss Mitigation And Contact Information

- Formal Letter Closing And Authorized Representative Signature

Mortgage Lender Corporate Name And Return Address

When reviewing loan documents, the mortgage lender corporate name identifies the legal entity funding your home loan. This official title must appear accurately on all contracts to ensure legal validity. Accompanying this is the return address, which serves as the designated location for official correspondence and original security instruments. Verifying these details prevents processing delays and ensures your payments or legal notices reach the correct department. Always confirm the registered business name matches your loan estimate to avoid potential clerical errors during the closing process.

Date Of Formal Letter Issuance

The Date of Formal Letter Issuance is the most critical element for establishing legal and chronological records. It must be placed at the top of the document, typically formatted as Day Month Year to avoid ambiguity. This specific date marks the official start of a notice period or contractual obligation. Accurate dating ensures compliance with regulatory deadlines and provides a verifiable timeline for correspondence. Always ensure the date reflects when the letter is actually signed or dispatched to maintain procedural integrity in professional communication.

Borrower Name And Mortgaged Property Address

The Borrower Name and Mortgaged Property Address are fundamental identifiers in any loan agreement. Legal accuracy is essential to ensure the security instrument is enforceable and properly recorded. The borrower's legal name must match their official identification to prevent title issues, while the property address defines the specific collateral securing the debt. Any discrepancy in these details can lead to funding delays or legal challenges regarding ownership rights and lien priority. Always verify these fields against the deed to maintain a valid and legally binding mortgage contract.

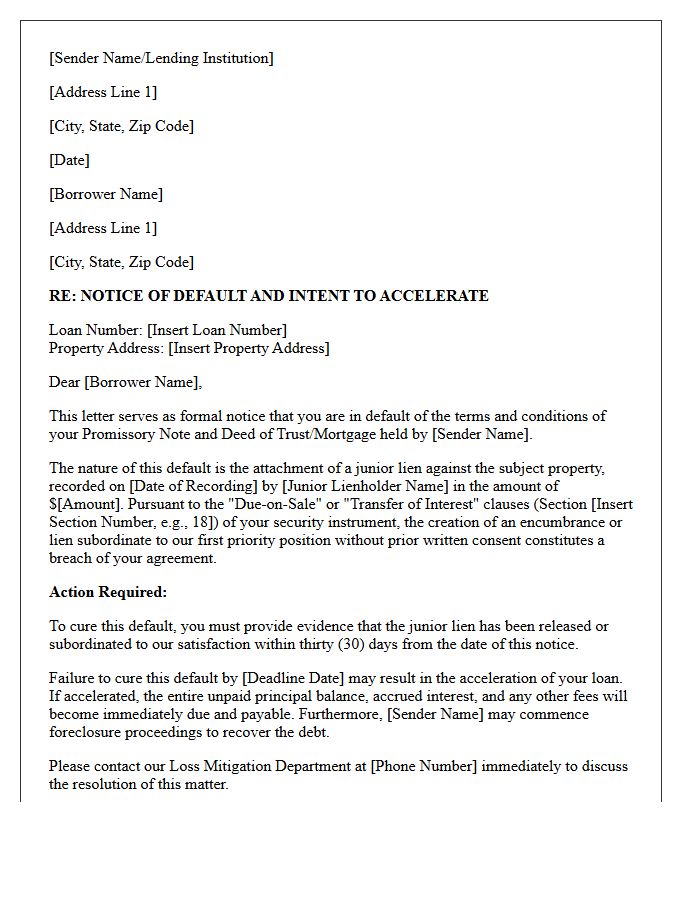

Subject Notice Of Default Letter Due To Junior Lien Attachment

Receiving a Notice of Default due to a junior lien attachment signifies that a secondary creditor, such as a second mortgage or judgment holder, has initiated foreclosure proceedings. Even though the lien is in a subordinate position, the junior lender retains the legal right to sell the property to satisfy their debt. Homeowners must act immediately to negotiate a reinstatement or settlement, as this action can jeopardize your primary mortgage standing and ownership. Seeking legal counsel is essential to protect your equity and explore options like refinancing or debt restructuring before the auction occurs.

Formal Borrower Salutation

A Formal Borrower Salutation is a professional greeting used in loan documents and financial correspondence. It typically employs the recipient's legal name preceded by formal titles like Mr., Ms., or Dr. to maintain a serious tone. Establishing professional rapport through accurate salutations ensures legal clarity and respect. In structured finance, using "Dear [Full Name]" is common practice to avoid ambiguity. Proper formatting reflects the credibility of the lending institution and ensures that communications are legally binding and professionally addressed to the primary obligor.

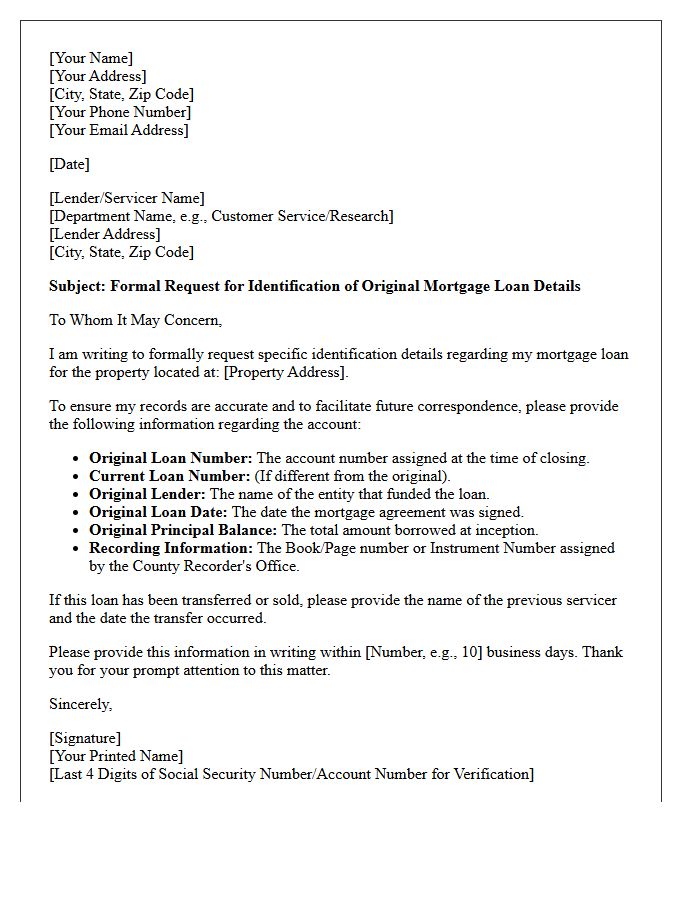

Identification Of Original Mortgage Loan Account Details

Accurate Identification Of Original Mortgage Loan Account Details is essential for effective debt management and legal compliance. Borrowers must verify the unique loan number, the identity of the initial lending institution, and the precise origination date. These records confirm the legal chain of ownership, especially if the debt was sold or transferred. Retaining the original promissory note and closing disclosures ensures you can cross-reference financial statements, prevent billing discrepancies, and protect your equity during loan servicing transitions or potential refinancing processes.

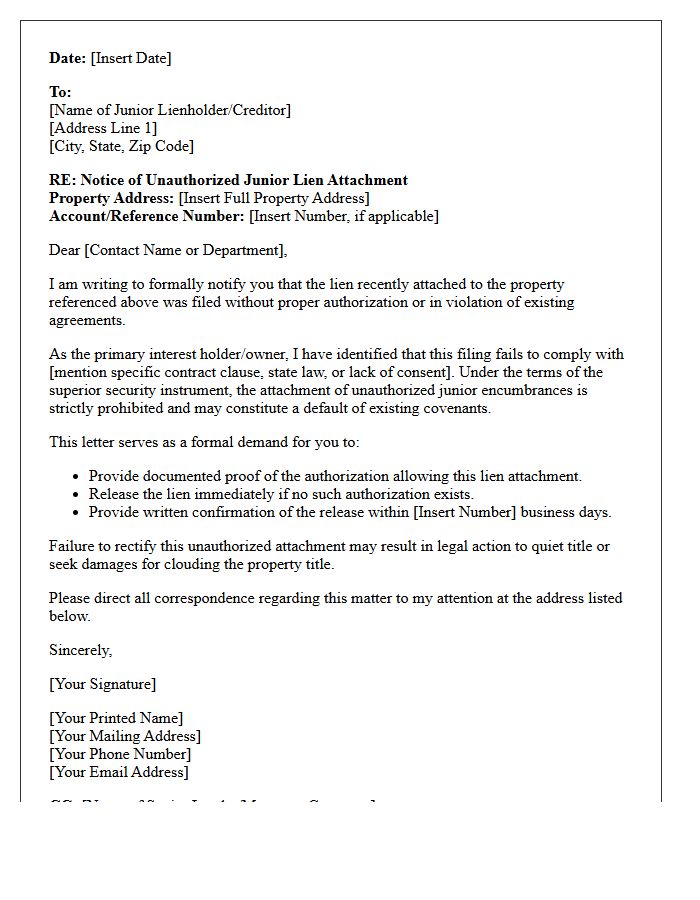

Notification Of Unauthorized Junior Lien Attachment

A Notification Of Unauthorized Junior Lien Attachment is a critical legal alert issued when an unapproved secondary debt is recorded against your property. This document signals a potential breach of your primary mortgage covenants, as senior lenders typically prohibit additional encumbrances without prior consent. Such filings can jeopardize your equity and trigger a technical default. It is essential to monitor your title records to ensure no fraudulent claims or subordinate liens compromise your legal ownership or financial standing during a real estate transaction.

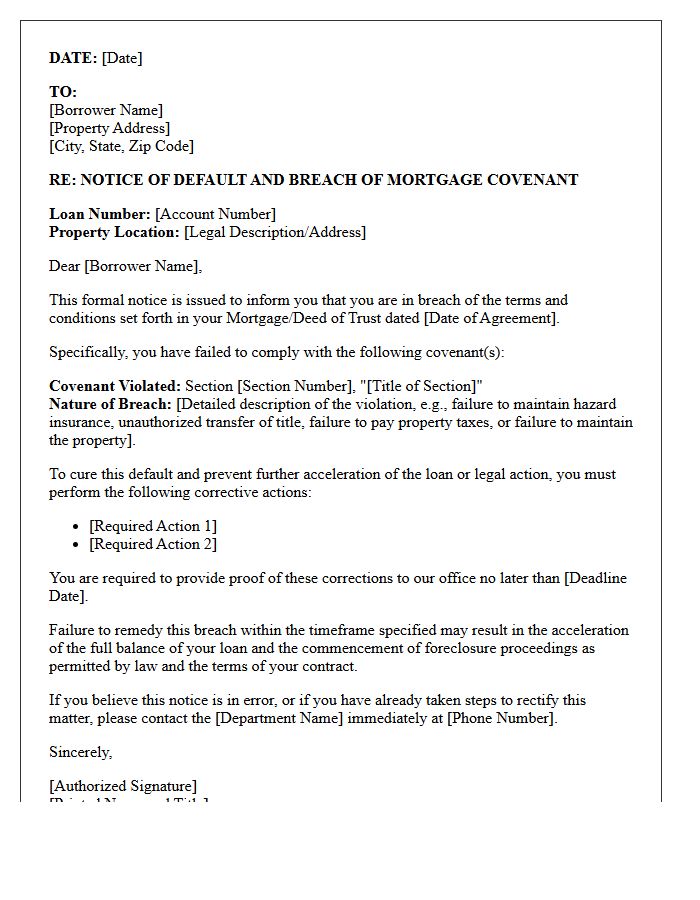

Citation Of Specific Mortgage Covenant Breach

A citation of a specific mortgage covenant breach is a formal legal notice issued when a borrower violates non-payment terms. Beyond monthly installments, homeowners must maintain property insurance and pay property taxes to avoid technical default. Lenders issue this citation to identify the exact contractual violation, such as unauthorized structural alterations or transferring titles without consent. Addressing these breaches immediately is vital, as they grant the lender the legal right to accelerate the loan balance or initiate foreclosure proceedings to protect their financial interest in the collateral.

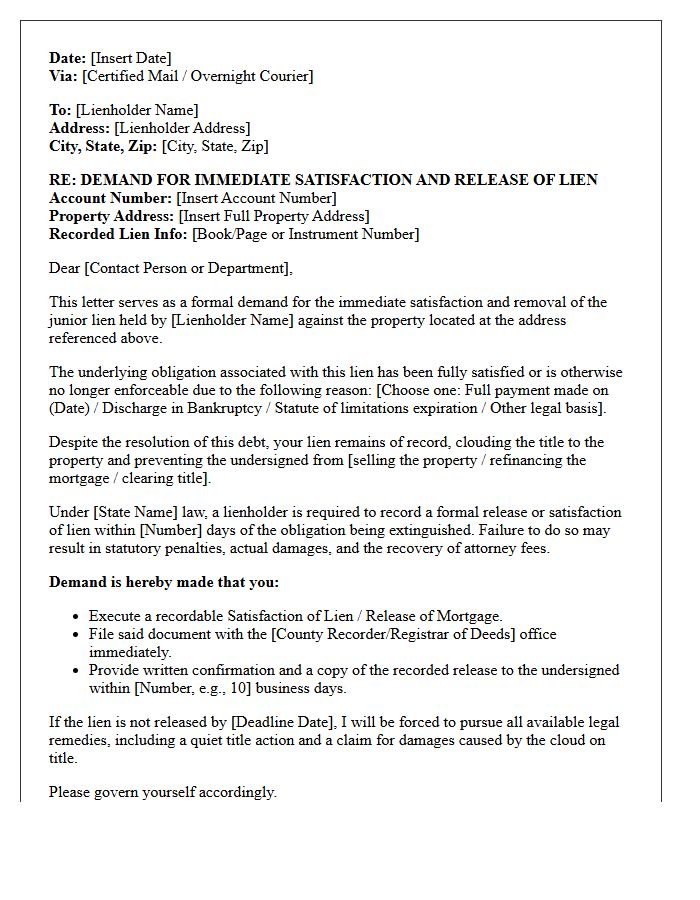

Demand For Immediate Junior Lien Satisfaction Or Removal

A Demand for Immediate Junior Lien Satisfaction or Removal is a critical legal notice used to clear property titles. When a primary mortgage is paid or a junior lien is legally unenforceable, the owner must ensure the cloud on title is eliminated. Failure to release these subordinate claims can derail refinancing or property sales. This formal demand compels the lienholder to file a reconveyance or satisfaction document within specific statutory deadlines. Promptly resolving these encumbrances is essential to restoring full marketable title and protecting the owner's financial interests.

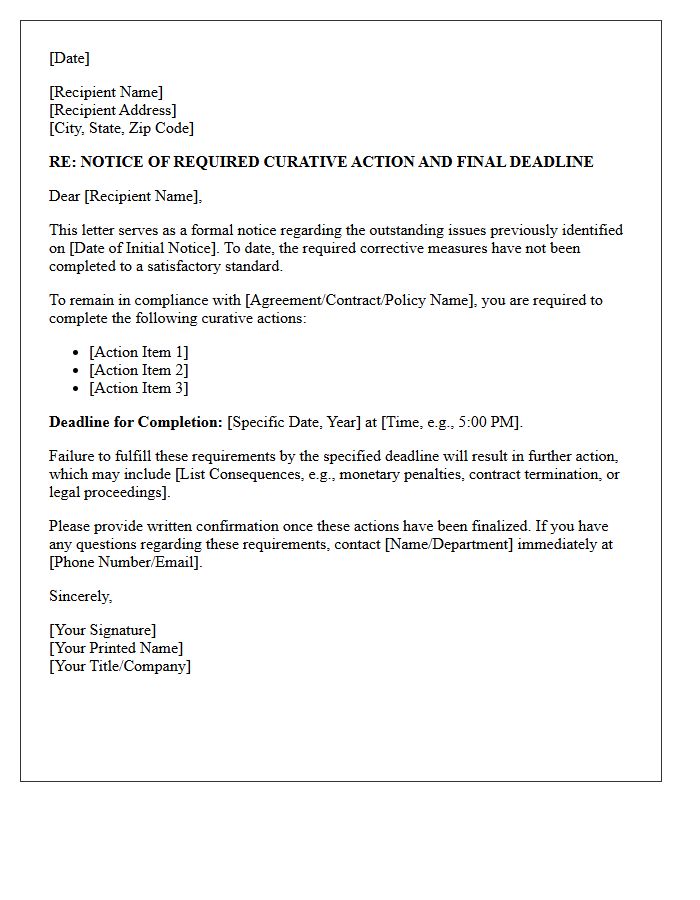

Specific Deadline For Curative Action Requirements

To maintain regulatory compliance, businesses must strictly adhere to the Specific Deadline For Curative Action. Once a deficiency is identified during an audit or inspection, the remediation period begins immediately. Failure to implement corrective measures within the mandated timeframe can result in severe penalties or legal sanctions. Organizations should prioritize documented evidence of resolution to demonstrate full adherence. Monitoring these statutory timelines is essential for risk mitigation and ensuring operational continuity. Always verify industry-specific regulations to confirm the exact number of days permitted for necessary technical or administrative rectifications.

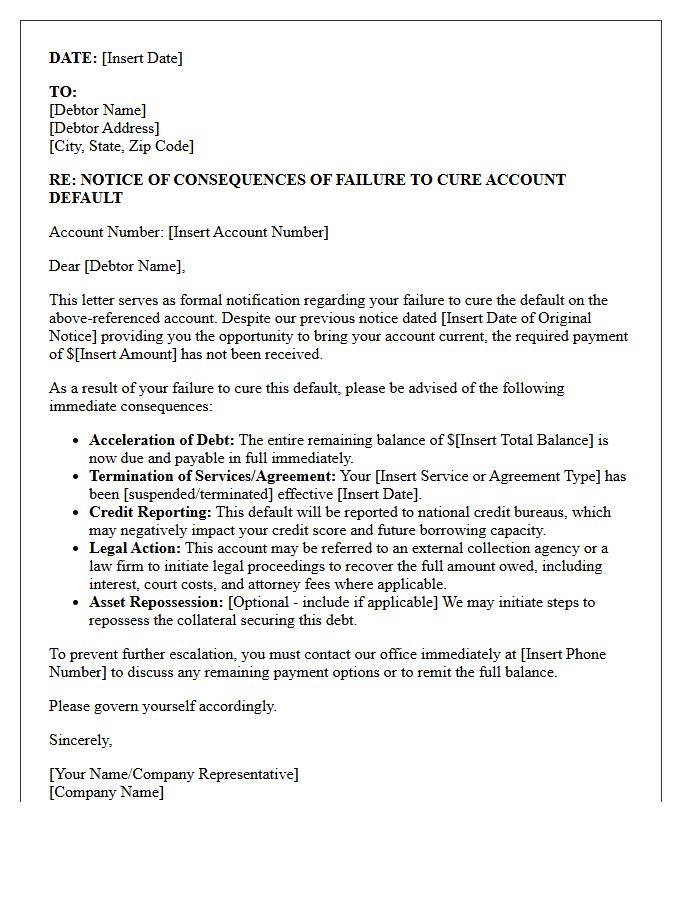

Consequences Of Failure To Cure Account Default

Failure to cure an account default can lead to severe financial and legal repercussions. Initially, creditors may impose heavy penalties and increased interest rates, significantly inflating your total debt. If the breach persists, the lender often initiates foreclosure or repossession to recover collateral. Furthermore, a formal default severely damages your credit score, restricting future borrowing capacity for years. Persistent non-payment may also result in litigation, leading to wage garnishments or asset seizures. Timely intervention is essential to prevent these escalations and maintain long-term financial stability.

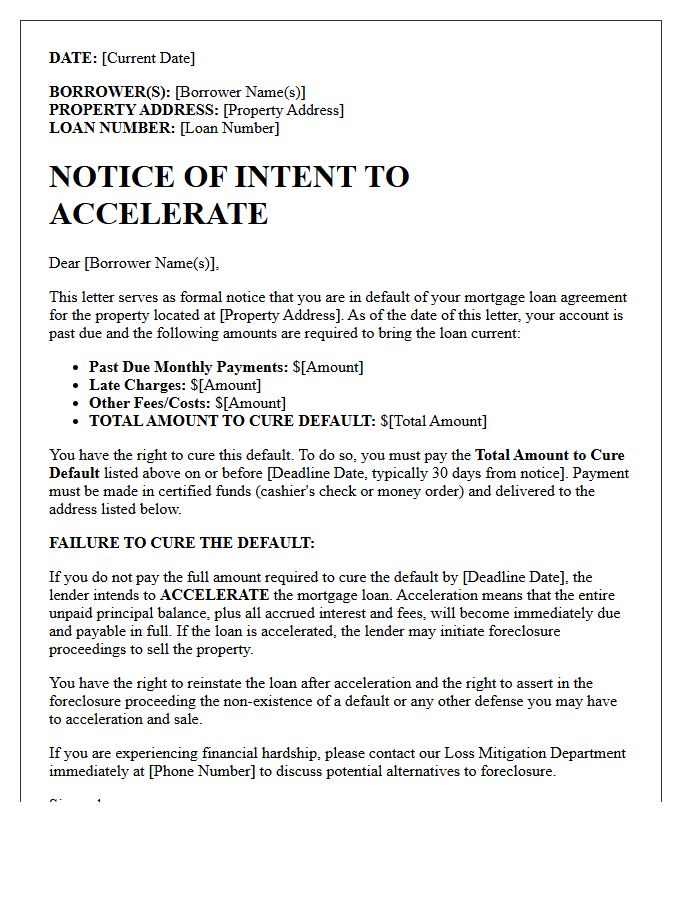

Notice Of Intent To Accelerate Mortgage Loan Balance

A Notice of Intent to Accelerate is a formal warning from your lender indicating that your mortgage is in default. It signifies the final step before the bank demands the entire loan balance immediately. To prevent foreclosure, you must pay the specified arrears by the deadline. Ignoring this letter allows the lender to "accelerate" the debt, meaning you lose the right to monthly installments and must pay the full amount to keep the home. Prompt communication or loan reinstatement is essential to stop legal action.

Lender Loss Mitigation And Contact Information

When facing mortgage hardship, loss mitigation offers alternatives to foreclosure, such as loan modifications or short sales. Borrowers should immediately seek their servicer's contact information found on monthly billing statements or the official website. Proactive communication is essential to access relief programs and stabilize finances. Always verify the lender's identity before sharing sensitive documents to avoid scams. Timely outreach ensures you understand all available workout options to protect your home and credit standing during financial distress.

Formal Letter Closing And Authorized Representative Signature

When finalizing a formal letter, the closing must reflect professional etiquette. Use "Sincerely" for known recipients or "Yours faithfully" for formal outreach. The Authorized Representative Signature validates the document, confirming legal authority to act on behalf of an organization. This section must include the printed name, official job title, and the organization's name below the handwritten signature. Ensuring these elements are present maintains legal compliance and professional credibility, establishing a clear chain of responsibility for all business correspondence and contractual agreements.

What is a Notice of Default due to a junior lien attachment?

A Notice of Default due to a junior lien attachment is a formal legal notification sent by a senior mortgage lender when a secondary lien-such as a judgment lien, second mortgage, or tax lien-is recorded against the property, potentially violating the "due-on-sale" or "encumbrance" clauses of the primary loan agreement.

Can a junior lien trigger a foreclosure on my primary mortgage?

Yes, most standard deed of trust agreements contain clauses that prohibit further encumbering the property without the senior lender's consent. If a junior lien is attached, the senior lender may view it as a breach of contract and issue a Notice of Default to protect their priority position, which can lead to acceleration of the debt and foreclosure.

How does a junior lien affect the priority of my existing mortgage?

Generally, a junior lien does not change the priority of an existing first mortgage; however, it creates a "cloud on title" and reduces the owner's equity. Senior lenders often issue a Notice of Default because a junior lien increases the financial risk to the property and may complicate future refinancing or sale efforts.

What should I do if I receive a Notice of Default because of a judgment lien?

You should immediately review your original loan agreement to see if it prohibits junior encumbrances. To cure the default, you typically must either satisfy the judgment to have the lien released, negotiate a subordination agreement with the senior lender, or obtain a bond to set aside the lien while it is being contested.

Does a junior lien holder have the right to foreclose if the senior mortgage is current?

Yes, a junior lien holder (such as a second mortgage holder or a judgment creditor) has the legal right to initiate foreclosure proceedings to satisfy their debt, even if the primary mortgage is in good standing. If they do so, they must usually pay off the senior lien or sell the property subject to the existing first mortgage.

Comments